Written by: Rita

Trend Guide

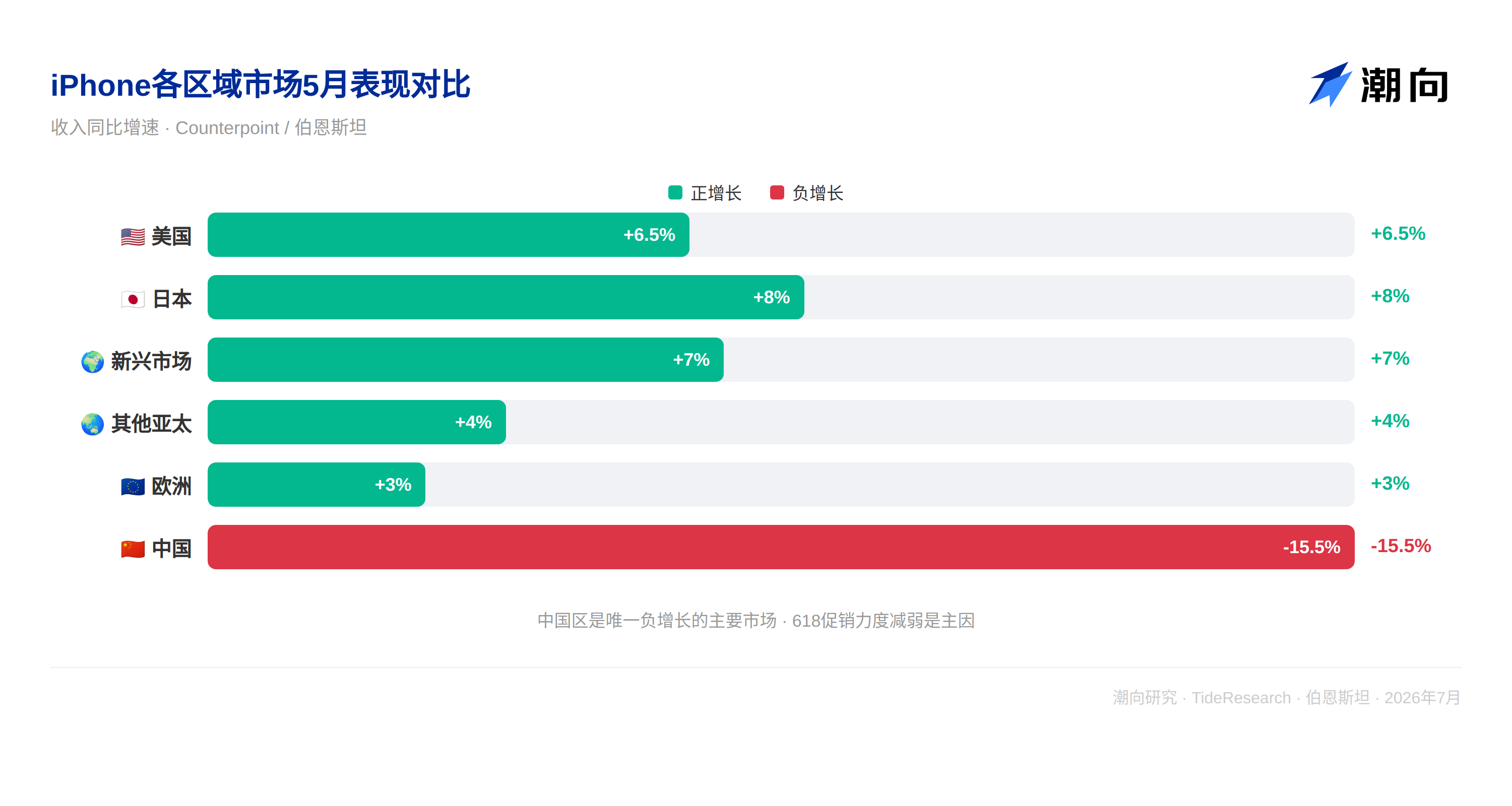

Bernstein released its May Apple tracking report on July 8, showing that iPhone shipments in May increased by 2% year-on-year and by 1% month-on-month, with its market share continuing to expand. However, the ASP fell slightly by 1.2% year-on-year, ending a streak of 6 months of ASP growth. Revenue in China decreased by 15.5% year-on-year, making it the only major market with negative growth, mainly due to a weakened 618 promotional effort. The data for the first two months of FQ3 was slightly below the historical seasonal average, which Bernstein believes may be a signal to watch, but it still holds a positive overall judgment on the supply chain.

Shipment growth slows, but share continues to expand

iPhone shipments in May increased by 2% year-on-year and by 1% month-on-month. Almost all markets achieved positive growth, with Japan and emerging markets performing the strongest, while the Chinese market clearly dragged down performance with a year-on-year revenue decline of 15.5%.

In the US market, iPhone sales increased by 6.5% year-on-year, with market share expanding from 50% in April to 53% in May, continuing to squeeze the Android camp. Europe and other Asia-Pacific markets also maintained positive growth.

The Japanese market showed the strongest growth, while emerging markets continued to contribute incremental gains. Bernstein believes that the differentiated performance of iPhone in different regional markets reflects the varying penetration depths of the Apple brand in markets with different price sensitivities, with loyalty in the high-end market and penetration in the low-end market both increasing.

Bernstein emphasizes that a slowdown in iPhone shipment growth does not mean a loss in share. In most markets, Apple's share is expanding, but the overall smartphone market's growth is also slowing, especially in China.

China is the biggest drag; weakened 618 promotional strength is the main reason

iPhone revenue in China in May decreased by 15.5% year-on-year, with sales declining by 19.1% year-on-year, and ASP rising by 4.4% year-on-year. This marks the first annual decline for the Chinese market since the release of the iPhone 17 series and is the only major market globally with negative growth.

The core reason lies in the 618 promotions. During the 2025 618 period, the iPhone 16 Pro had discounts of about 175-295 yuan and could enjoy an additional national subsidy of 500 yuan once the price dropped below 6000 yuan. In the 2026 618, the iPhone 17 Pro had a discount of only about 145 yuan, and the price remained above 6000 yuan, receiving no national subsidy. While the basic iPhone 17 did have a discount of about 30 yuan and dropped below the threshold, the overall promotional strength was far less than last year.

Bernstein interprets this as not a question of the competitiveness of Apple products, but more a phase mismatch in promotional strategies and subsidy policies. The conflict between Apple's pricing strategy for high-end models and the national subsidy threshold has temporarily weakened the cost-performance advantage, but Apple's share in the Chinese market still expanded from 16% in April to 18% in May, indicating that even with weakened promotional efforts, Apple continues to capture share from Android.

ASP drops for the first time; e series proportion rises is the main reason

The iPhone's ASP saw a slight decline of 1.2% year-on-year in May, ending a streak of 6 months of ASP growth. The main reason is the increased sales proportion of the iPhone 17e and 16e, with e series total sales rising from 1.7 million units in May 2025 to 1.9 million units in May 2026, increasing its proportion of total sales from 10% to 11%.

The ASP of the e series is significantly lower than that of other products in the iPhone family, and its rising proportion naturally brought down the overall ASP. Bernstein believes that the increased proportion of the e series itself is not a bad thing, as it indicates Apple's competitiveness in the mid-range market, finding new incremental space amidst near-saturation in the high-end market. However, the short-term drag on ASP is real, and there is a need to continuously observe whether the proportion of the e series will continue to rise.

Supply Chain: TSMC N3P under pressure but AI supplements, DRAM content continues to grow

For TSMC, the sales of the iPhone 17e did not reach those of the 16e, and with the discounts for the iPhone 17 during 618 being less than last year, the N3P wafer shipments were slightly weaker than the previous generation N3E. However, Bernstein believes that even if Apple or other phone clients release advanced process capacity, AI applications will fill the gap, and TSMC will not lose revenue as a result.

In terms of DRAM, the average DRAM capacity of the iPhone in May reached 9.6GB, a year-on-year increase of 27%. The proportion of models equipped with 12GB DRAM rose to 43%, while models with 8GB and above reached 95%. Bernstein pointed out that Apple is accelerating the increase of DRAM content to support edge-side AI, but it needs to be noted whether the rising prices of storage chips will impact this trend.

Regarding individual stocks in the supply chain, Bernstein believes that Luxshare Precision and lens manufacturers have strong sentiment, as iPhone shipments outperform Android, and both have made steady progress in AI-related businesses. Sony will not have an upgrade in its CIS this year, potentially losing market share to Samsung in 2027. Qualcomm's proportion in Apple's revenues will decrease as Apple's in-house chip development progresses, and the softness in the Android market also puts pressure on phones.

Bernstein sets a target price of $350 for Apple, corresponding to a P/E ratio of about 35 times for 2026, based on the judgment that demand for the iPhone 17 is stronger than expected, and the software and services ecosystem continues to expand.

Trend Perspective

The most valuable aspect of this report from Bernstein is its distinction between the concepts of "iPhones selling less" and "iPhones selling poorly." The growth rate of shipments has dropped from double digits to single digits, yet the share is expanding; ASP has declined for the first time, but the e series strategy is helping Apple reach a broader user base; revenue in China is declining, but share is still rising.

The fundamental problem Apple faces is not that iPhone shipments have peaked, but that the valuation logic is shifting from hardware growth to ecosystem and service monetization. Bernstein's target price of $350 corresponds to a P/E ratio of 35 times, implying the market's expectation for continued growth in service revenue, rather than the continued expansion of iPhone shipments. If the growth rate of service revenue shows a slowdown in subsequent quarters, the margin of safety at a 35 times P/E ratio will quickly narrow.

For investors, this report provides an important observation framework: during the cycle of device replacement driven by AI features, a slowdown in iPhone shipment growth is a normal phenomenon; the key question is whether Apple can enhance the value of individual devices and increase service subscription rates through AI features. The extent of AI feature upgrades when the iPhone 18 series is released in the second half of 2026 will be a crucial window to validate this logic.

Disclaimer

This article is a整理 and interpretation of a third-party brokerage research report (Bernstein, July 8, 2026) by Trend Research. The ratings, target prices, earnings forecasts, and related judgments quoted in this article are solely the views of the brokerage's analysts and do not represent the views of Trend Research, nor do they constitute any investment advice.

The market has risks, and decisions need to be independent. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。