Written by: Rita

Trend Guide

On July 8, Goldman Sachs published an interpretation of IDC's preliminary data on PC shipments for Q2 2026. The PC shipment volume for the quarter was 68.2 million units, a year-on-year decline of 4.9%, ending nine consecutive quarters of positive growth. Goldman Sachs attributed the decline to the ongoing shortage of key components such as storage chips and memory, as well as the resulting increase in total machine prices which suppressed terminal demand. The tight supply situation is expected to last until early 2028, with large manufacturers leveraging their supply chain management capabilities to take away market share from smaller manufacturers.

End of Nine Quarters of Growth, Component Shortages as Main Reason

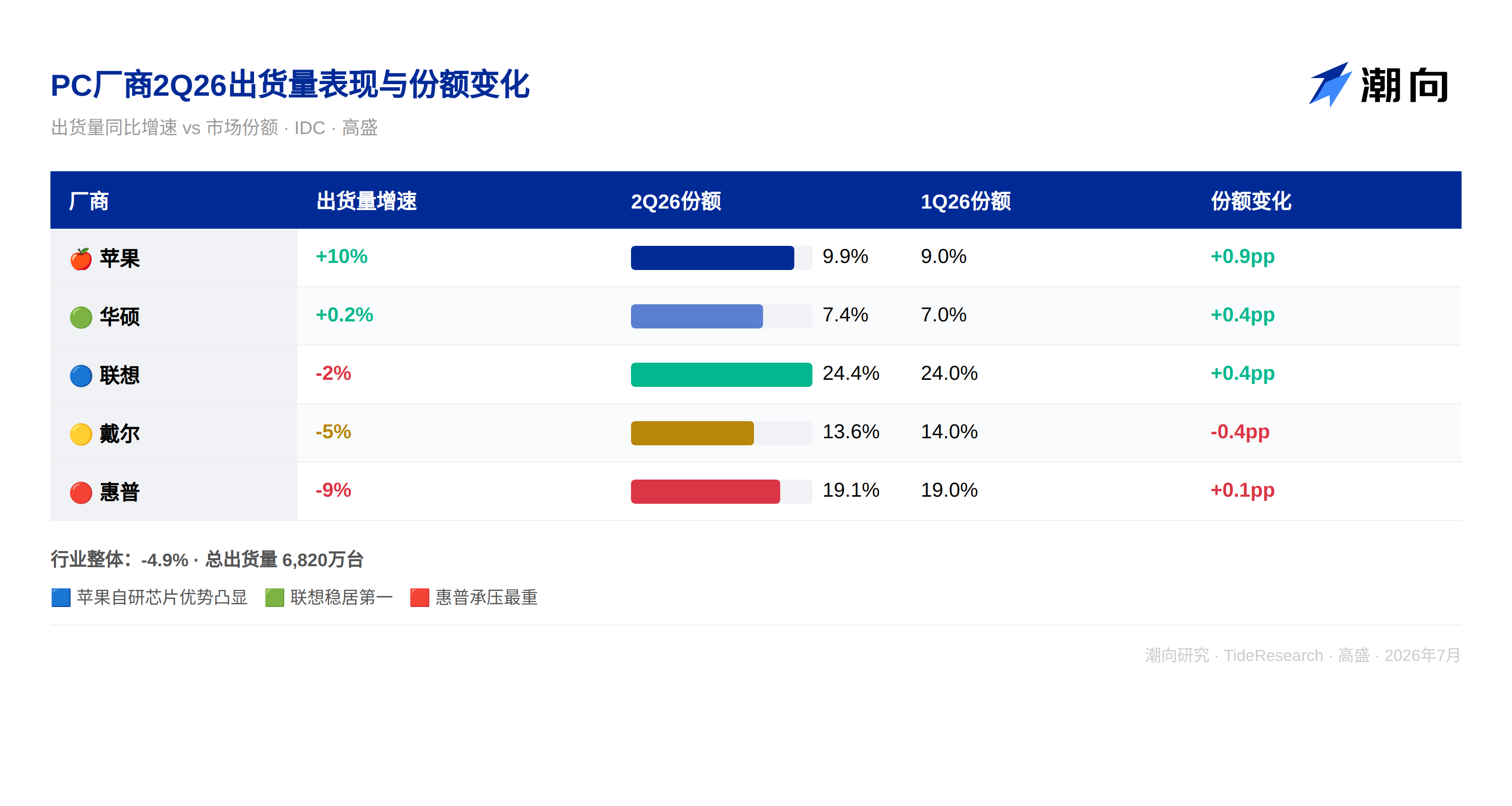

In Q2 2026, PC shipments were 68.2 million units, a year-on-year decline of 4.9%. Prior to this, the PC industry had maintained positive growth for nine consecutive quarters; the end of this trend signifies that the industry is entering a completely different phase. The last time the PC industry experienced a year-on-year decline in shipments was in Q4 2023, against a backdrop of post-pandemic demand exhaustion and excess inventory. This time, the logic behind the decline is entirely different: it’s not that demand has disappeared, but rather that production cannot keep up.

Goldman Sachs cited IDC's analysis, stating that the core driving force behind the decline is component shortages. The tight supply of storage chips and memory not only limits the number of complete units produced but also increases total machine prices. Although shipment volumes have declined, industry revenue continues to grow, with price effects offsetting quantity effects. This means that PC manufacturers are "selling less" but "selling at higher prices," with rising ASP potentially providing a positive contribution to the profitability of leading manufacturers.

Goldman Sachs predicts that supply shortages will last at least until early 2028, with PC shipments in the second half of 2026 likely to face a more significant decline. This represents a major structural change for the entire PC supply chain. The logic of inventory cycles is yielding to the logic of capacity allocation; production capacity for storage chips is being taken by AI servers, leaving PCs without sufficient components.

Apple Leads, HP Falls Behind

The performance of the five major manufacturers shows clear differentiation.

Apple's shipment volume grew by 10% year-on-year, with its market share rising to 9.9%, being the only leading manufacturer to achieve double-digit growth. Goldman Sachs believes that Apple benefits from the stability of its self-developed chip supply and the resilience of the high-end market demand. Apple does not need to scramble for Intel or AMD chips in the open market like other manufacturers; the production capacity for the M series chips is entirely secured by TSMC, and supply chain autonomy has translated into a tangible shipment advantage during times of shortage.

Lenovo's shipments decreased by 2%, but its share remains high at 24.4%, firmly holding the top spot globally. Dell saw a decline of 5%, with a market share of 13.6%, performing in line with the overall industry. ASUS slightly increased by 0.2%, with a share of 7.4%, barely maintaining positive growth among the majority of manufacturers facing negative growth. ASUS’s positioning in the gaming PC and high-end consumer markets has helped it maintain demand resilience amidst rising prices.

HP is the biggest loser, with a 9% decline in shipments, bringing its share down to 19.1%. Goldman Sachs believes that HP is relatively weaker in supply chain management and component procurement, thus being impacted more severely by shortages. HP's consumer PCs and small to medium-sized business customers are more sensitive to price increases, making them the most severely affected in a rising price cycle.

Large Manufacturers Are Taking Market Share

Goldman Sachs clearly pointed out that the ongoing supply shortages are reshaping the competitive landscape of the PC industry. Manufacturers with larger scales, richer product lines, and stronger supply chain management capabilities are benefiting from this.

Apple, Dell, and Lenovo have been identified by Goldman Sachs as companies to watch. They have stronger bargaining power to secure component supplies, more diverse product lines to flexibly allocate scarce resources, and more stable customer relationships to absorb price increases. Smaller manufacturers, under the same supply constraints, cannot secure components, cannot raise prices, and are losing customers, with their market share being gradually eroded.

IDC expects this trend to continue until supply levels return to normal. This means that before 2028, the concentration in the PC industry will continue to rise. For investors in the A-shares and Hong Kong stocks, this indicates that small and medium-sized OEMs in the domestic PC supply chain may face order contraction pressure, while large manufacturers that have already entered the core supply chains of Apple, Lenovo, and Dell (such as Luxshare Precision, Foxconn Industrial Internet, etc.) may gain more stable order allocations.

Trend Perspective

The end of nine consecutive quarters of growth in PC shipments signifies not just a momentary fluctuation in industry data, but rather the "siphoning effect" of AI computing power expansion on the traditional technology supply chain is becoming apparent. The production capacity for storage and memory is shifting towards HBM and AI servers, directly squeezing the supply side for PCs. Goldman Sachs's forecast of shortages lasting until early 2028 aligns with the expectation that the storage cycle will peak by the end of 2027, suggesting that the timeline for supply recovery in the PC industry entirely depends on when AI's demand for storage capacity eases.

The changes in market shares among leading manufacturers provide another perspective. The difference between Apple’s +10% and HP’s -9% indicates that under the same supply constraints, differences in supply chain management capabilities can directly translate into market share shifts. For investors focusing on the PC supply chain, this shortage is not merely a simple "industry downturn," but rather a reshuffling driven by supply-side dynamics, where large manufacturers feast, smaller ones sip broth, and those falling behind can't even get soup.

The combination of "growing revenue, declining shipment volumes" mentioned by Goldman Sachs is worth continuous observation. If the PC industry's revenue continues to grow while shipment volumes keep declining, this indicates that rising ASP is compensating for reduced volume, and the profitability of leading manufacturers may even increase. If this logic holds, the degree of benefit for component suppliers in the PC supply chain (especially for high-end components with higher unit prices) may exceed that of whole machine assemblers.

Disclaimer

This article is a整理与解读 of third-party brokerage research reports (Goldman Sachs, July 8, 2026) by Trend Research. The ratings, price targets, profit forecasts, and related judgments quoted in this article are solely the opinions of the analysts at that brokerage, representing the position of their respective institutions, and do not represent the views of Trend Research, nor do they constitute any investment advice.

The market has risks, and decisions should be made independently. This article should not serve as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。