The cryptocurrency market once again experienced a "bull death spiral" in mid-November.

Written by: Murphy

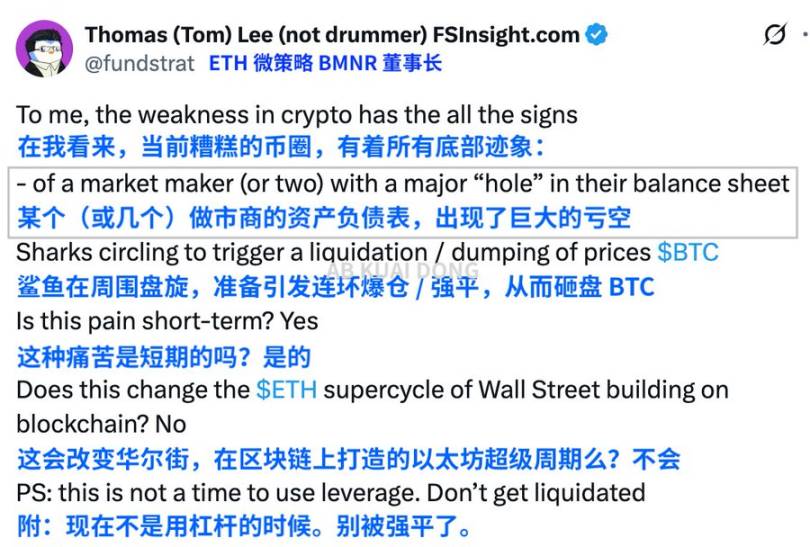

Bitcoin fell below $100,000, and Ethereum dropped by 10% in a week. The cryptocurrency market once again witnessed a "bull death spiral" in mid-November. Tom Lee, chairman of BitMine, the leading Ethereum reserve institution, and a Wall Street analyst, believes that the real pressure comes from the shrinking liquidity of market makers and the arbitrage sell-off by large traders.

Source: X

The price of Bitcoin (BTC) plummeted from its peak of $126,000 in early October, falling below the $100,000 mark in just three days. The bull traders and market makers faced a series of liquidations, with prices dipping to $97,000, resulting in a weekly decline of over 5%. After a surge of $524 million into Bitcoin spot ETFs on the 11th, there were outflows of $278 million and $866.7 million on the 12th and 13th, respectively, accelerating the selling pressure.

Some attribute this market movement to "whale sell-offs," "reversal of Federal Reserve expectations," and "market maker withdrawals," but if we only look at the present, it is easy to overlook a more fundamental historical pattern: bull markets never abruptly stop at a peak; instead, they automatically digest themselves in a "liquidation chain" manner after reaching a high.

And the order of the liquidation chain never changes.

The First to Fall: "Bull Believers"

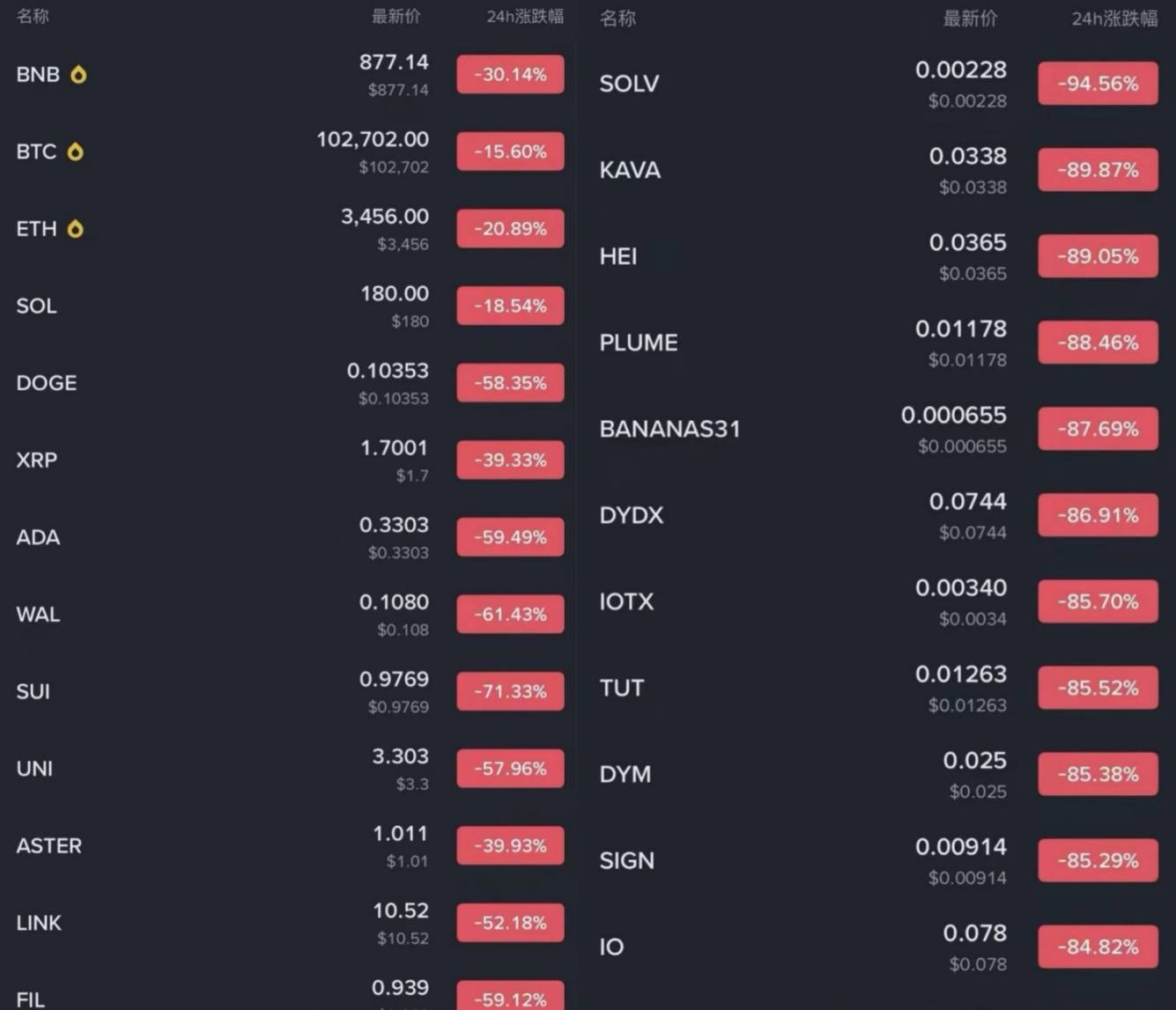

Source: Binance

Those who were still shouting "to $140,000" and "the ETF bull market is taking off" at $120,000 were the first to be buried. They increased their positions and leveraged heavily at high prices, and with a high leverage ratio, any slight price movement could trigger a chain reaction of liquidations. Next were those who thought they were safe with low leverage. Just like the flash crash on October 10-11, I was one of the low-leverage gamblers during this black swan event, "coin-based, 3X contracts, opening positions with liquidation." Multiple accounts received a barrage of liquidation notifications in just a few minutes, and once the price broke through, it spread horizontally.

The painful lesson: low leverage is not safe; liquidation may be delayed but will eventually come.

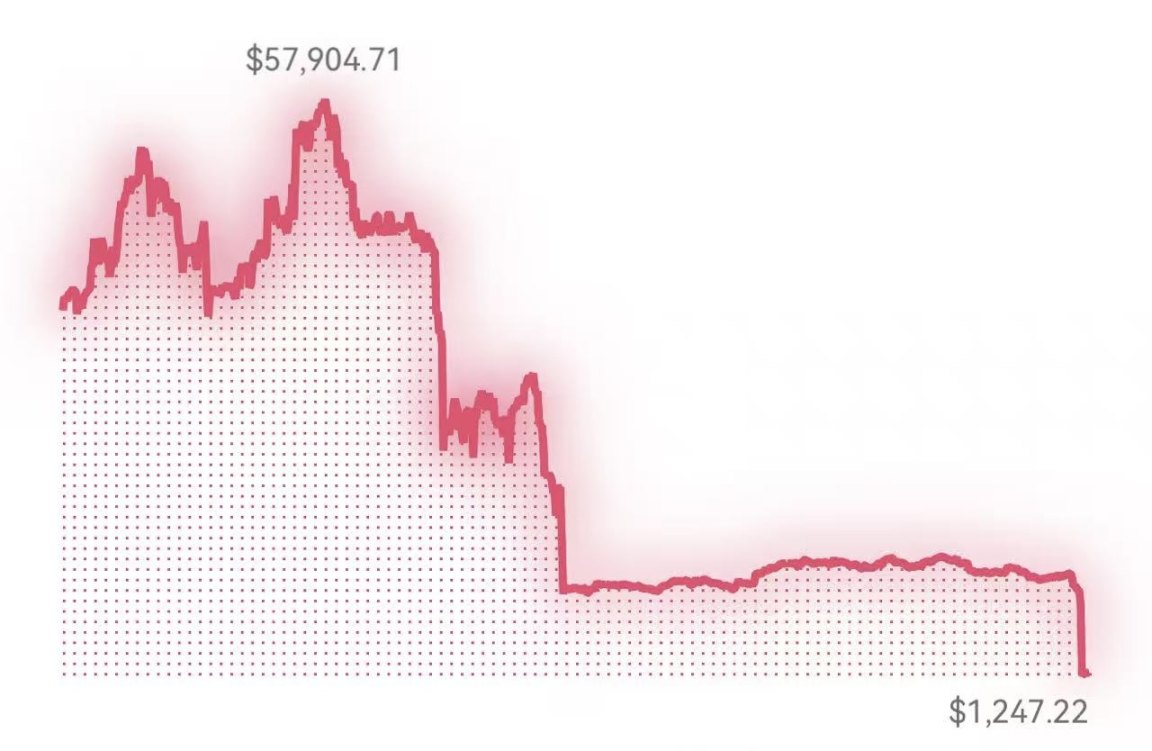

Source: Author

The Second Group: Market Makers and Quantitative Institutions

Do you think market makers are invincible? Remember March 12, 2020? Market makers saw their depth drop to negligible levels.

During the liquidation wave in 2021, even Alameda couldn't hold on.

In 2022, during the LUNA collapse, even crypto banks were swept away.

With stablecoins decoupling in a chain reaction, market makers, lending whales, and quantitative institutions all retreated in succession, and they themselves became the "spark" for accelerating the crash. "Market supporters" are not "eternal bottom feeders." When depth begins to thin and hedging costs rise, they are not stabilizing the market but fighting for survival.

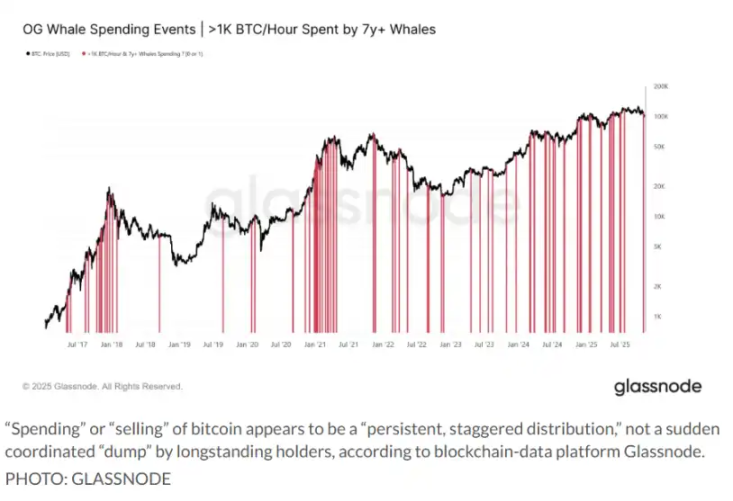

The Third Group: DAT Model Institutions, Token Reserve Institutions, Family Funds

They are the "accelerators" of a bull market, but don't forget that, as institutions, they have no beliefs, only spreadsheets. Once the logic for rising prices halts, they are the first to withdraw. In the past two weeks, their on-chain selling and transfer data have been rising, almost identical to the patterns seen in December 2021 and early 2022.

So when you put all of this together, you will find that the current market situation is very similar to the aftershocks following the 2019 ICO bubble, and it resembles the prelude to the liquidation wave that started in 2021.

By combining these three groups, we can see the essential state of the current market: it’s not that the bull market is over; it’s that the vehicle is too heavy and needs to "unload."

The strength of the bulls has been exhausted, market depth has been drained, and the structured demand from institutions has weakened, leading to a temporary depletion of upward momentum.

Of course, this is not yet the kind of "chaos" that marks the end of a bear market. There hasn't been extreme panic on-chain, funds have not fully retreated, and whales are not panic selling. It feels more like the bull market story is only halfway told; the narrative isn't dead, but the main characters are starting to exit, leaving behind a chaotic battle among secondary characters.

Returning to the most critical question: is this a new bear market liquidation chain?

From historical experience, on-chain data, market maker reactions, and institutional stances, this indeed exhibits characteristics of "early bear market liquidation." It’s not the kind of crash that is immediately obvious, but rather a "chronic ischemia," gradually making the market aware that the logic for rising prices has been completely consumed.

In the next 1-2 months, if BTC continues to test the $90,000 support repeatedly, and the rebounds remain weak, it can be confirmed that:

The first half of the bull market has ended, and the market has entered a "structural reconstruction period."

However, if funds flow back in, depth is restored, and institutions resume buying (albeit with some effort, as they have mostly bought what they needed), then this downward movement will just be a "mid-bull market liquidation," similar to the "halftime breaks" seen in September 2017 and September 2020.

Everything now is at a watershed moment.

Regardless, the trend of Bitcoin is always more complex than the charts. The market is deciding who will take on the next liquidation target: will it be the complete liquidation of market makers? DAT model institutions? Crypto banks? Reserve-based small countries?

We cannot predict the trend clearly, but what we can do is to reduce leverage and avoid taking chances.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。