Author: Victor (@vcmktasa), Mr. Z (@168MrZ), 168X

Jensen Huang and Lisa Su are heavily deploying forces, while the Taiwan stock market supply chain cashes in first

On October 4, 1957, the Soviet Union launched a metal sphere weighing 83 kilograms into near-Earth orbit. The signal of the first artificial satellite kept the entire Washington awake at night.

Eight years later, Kennedy declared, "We choose to go to the moon." Over the next decade, the Apollo program cost $257 billion (adjusted for today's value) and mobilized 400,000 people, just to plant the national flag on another planet.

The Cold War taught the world one thing: When great powers define a technology as "too big to fail," the scale of capital will detach from all commercial logic.

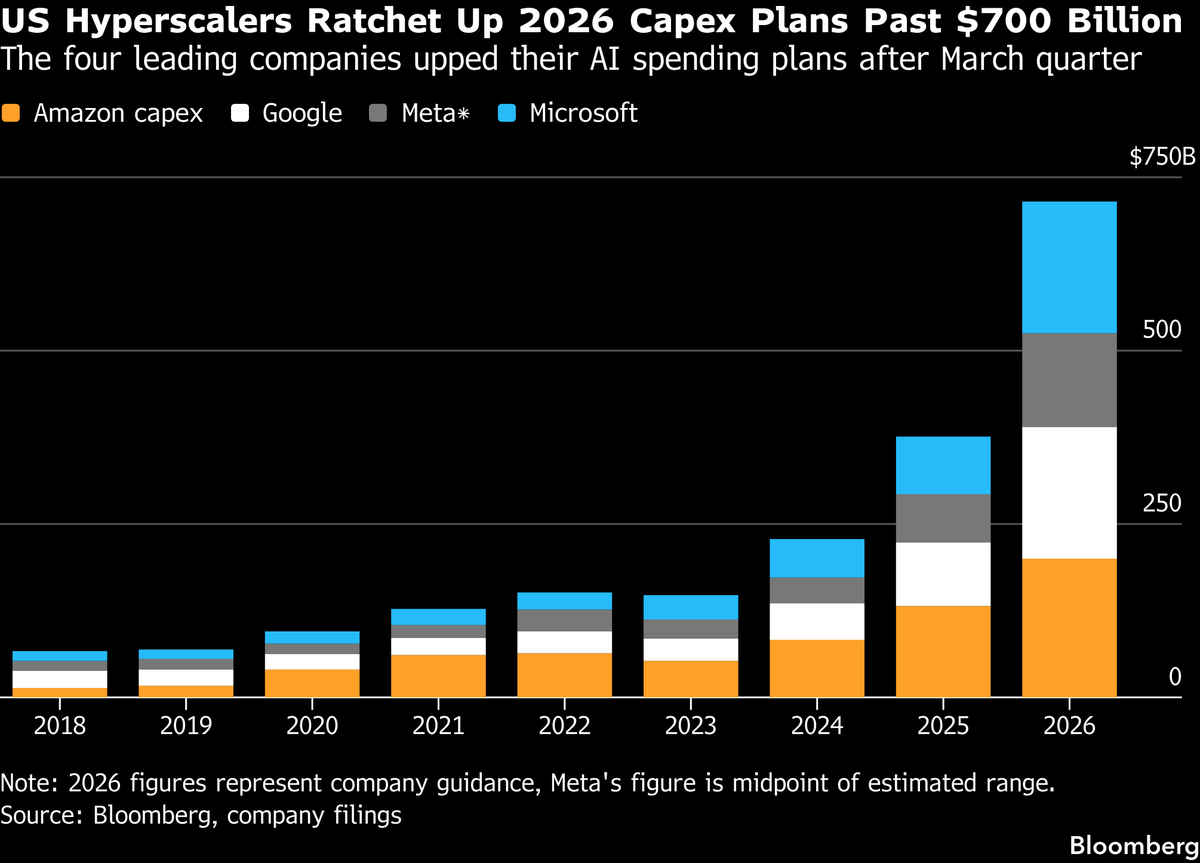

By 2026, the AI infrastructure Stargate plan backed by the U.S. government alone amounts to $500 billion over four years; Google, Amazon, and other major cloud service giants have annual capital expenditures exceeding $600 billion.

The same script is being replayed in AI, with a scale ten times that of the moon landing. The participants have shifted from the U.S. and the Soviet Union to the U.S. and China, along with the whole world.

In the Cold War era, the scarce resources that determined victory were uranium mines and rocket engineers. This time, they are advanced process wafers and advanced packaging capacity.

And 90% of them are produced on the same island, Taiwan.

1. The Mobilization Orders from the Leaders: Presidents Personally Support Factory Operations

The iconic image of the space race is Kennedy declaring the moon landing in Congress. The AI Cold War sees leaders of various countries personally urging chip factories to speed up production.

Washington. The Trump administration used CHIPS subsidies and a 25% tariff on chips to force manufacturing to return, while also backing Stargate. What’s even more interesting is the "Trump account": setting up an investment account with $1,000 for every newborn, directly invested in the U.S. stock index. This government is not only waging a tech war but also writing "the stock market must rise" into the rules.

Seoul. South Korea has rolled out a national investment plan worth 800 trillion won, with Samsung and SK Hynix each contributing 400 trillion to build new factories. At the end of June, Lee Jae-myung even commanded at a government meeting: the review of the semiconductor parks shifted from "proceeding step by step" to "processing simultaneously," with environmental assessments, land, water, and electricity all proceeding in parallel. He stated, "Victory depends on who runs faster."

Tokyo. Takagi Sanae has promoted Rapidus as a national strategic pillar, with government subsidies accumulating to 2.6 trillion yen, even recalling retired senior engineers for training in the U.S., just to catch up to the starting line for 2nm by 2027.

Taipei. The new ten major AI constructions aim for a production value of 15 trillion new Taiwan dollars, with the semiconductor vision targeting 300 billion over ten years, and a robust power grid aiming for 546.5 billion over ten years; ensuring power supply by 2032 and expanding the science park by 1,305 hectares over ten years.

Beijing. The National Strategic Fund Phase III amounts to 344 billion RMB, with the "14th Five-Year Plan" fully shifting toward domestic alternatives. China, blocked from advanced processes, is opting for a national system to compete in its own parallel race.

Abu Dhabi. The sovereign fund MGX completed the fundraising of a $49 billion AI fund on July 1, one of the largest in history, having invested in 14 companies including OpenAI, Anthropic, and xAI. Oil dollars are now officially trading in computing power.

Six governments are increasing their stakes in the same race. This is the first time since the 1960s that humanity has witnessed this level of national mobilization.

And the money from governments, as opposed to the money from the stock market, has a fundamental difference: Duration of 5 to 15 years. No quarterly reports, no fear of corrections; once the budget is approved, it must be spent.

The 2000 dot-com bubble was supported by stock market sentiment; once that sentiment shifted, the money evaporated. This round's foundation is national will.

In this race, no participating country can withdraw midway.

2. The Private Military Spending of Arms Dealers: Orders Extend to 2028

The Cold War had nations but also arms giants.

The arms dealers in the AI Cold War represent an entire industrial chain. And their military spending is fiercer than that of nations.

First, let's look at computing. Whether designing chips or wanting to produce their own chips, the world cannot avoid Taiwan.

On May 27, Jensen Huang spoke at an employee meeting in Taipei's Beishi Science Park:

"Four or five years ago, NVIDIA's annual spending in Taiwan was about $10 billion to $15 billion. Now, it has grown to $100 billion to $150 billion. Taiwan is booming."

NVIDIA's annual spending in Taiwan equates to about 10% of Taiwan's GDP. The product roadmap has been arranged up to 2028: Rubin, Rubin Ultra, and then to the Feynman using TSMC's A16 process, one generation per year, with each generation tied to Taiwan.

AMD's CEO Lisa Su was also born in Tainan, like Jensen Huang. She holds two contracts of 6GW each, along with one from Meta that exceeds $60 billion. And MI450, from computation core to packaging, is entirely manufactured by TSMC.

Intel's EMIB advanced packaging competes with TSMC's CoWoS, but once this technology is scaled, the biggest beneficiaries are Taiwan's ASE and Unimicron. Every step Intel takes to challenge TSMC pulls Taiwan’s packaging factories into its ecosystem.

Besides these three arms dealers, there are also buyers spending even more fiercely: Cloud service giants.

Google and Amazon are buying chips from NVIDIA while also developing their own to reduce dependency. Google’s capital expenditure skyrocketed to $175 billion in 2026, with TPU chips handed off to MediaTek and Creative; Amazon’s Trainium chips are given to SiFive. Ultimately, everything needs to go into TSMC for mass production.

Next, let’s look at the currently most in-demand storage. There are only three companies globally that can produce HBM: Micron, SK Hynix, and Samsung.

Micron considers Taiwan to be its largest DRAM base globally. It has deepened its investment in Taiwan for 31 years, investing over 1 trillion new Taiwan dollars, making it Taiwan's largest foreign investor. In January of this year, it announced an $1.8 billion acquisition of Powerchip's wafer factory in Tongluo, Miaoli, focusing on advanced DRAM and HBM production and R&D.

All the world’s HBM has to ultimately queue up on TSMC's CoWoS production line.

At the very top of all this are the cash-burning AI laboratories. In the first half of 2026, global venture capital financing reached $510 billion, setting a record, with OpenAI and Anthropic alone taking 43%, about $217 billion. Once this money is in, it all transforms into computing orders.

The state puts forth the will, arms dealers provide the orders. The final destination for the shipments is all Taiwan.

3. The Silicon Shield 2.0: The More Intense the Competition, the Thicker the Shield

Globally, 92% of advanced process chips and 45% of advanced packaging capacity come from Taiwan.

For the past twenty years, this set of figures has been referred to as the "Silicon Shield": the most cutting-edge chips can only be produced in Taiwan, thus TSMC is known as the "sacred mountain defending the nation." However, as TSMC builds factories in Arizona, Kumamoto, and Dresden, the market has begun to worry: Will the offshoring of production dilute this shield?

This is a misreading. The Silicon Shield is not disappearing; it is upgrading: from "Made in Taiwan" to "Made with Taiwan."

This is Kaohsiung. TSMC has five 2nm factories under construction simultaneously, with cleanrooms spanning the size of 46 football fields, and single-site investments exceeding 1.5 trillion new Taiwan dollars. Wei Zhejia repeatedly emphasizes that the most cutting-edge processes and core R&D will all remain on the island. The core of the shield has not moved an inch.

This is Arizona. TSMC's investment of $165 billion is the largest foreign manufacturing investment in U.S. history.

In the past, Taiwan bore the burden alone of the Silicon Shield; now, the Silicon Shield binds every country placing orders onto the same ship.

How tough is this shield? Even NVIDIA's request for TSMC to increase production capacity was rejected; Japan, which invested $16.3 billion in national capital, can only promise to "start" mass production of 2nm in 2027; while TSMC’s annual capital expenditure is three times that of the Japanese government's subsidy.

Every dollar invested by countries is extending Taiwan's economic strength outward by an inch.

4. Taiwan Stocks Rise to Fifth Globally: The Explosive Moment for the Sellers of Shovels

The most stable winners of the 1849 Gold Rush were not the gold diggers, but the sellers of shovels.

Taiwan is the seller of shovels in this AI arms race, but now it is even fiercer, because this time, golden shovels cannot be made by everyone.

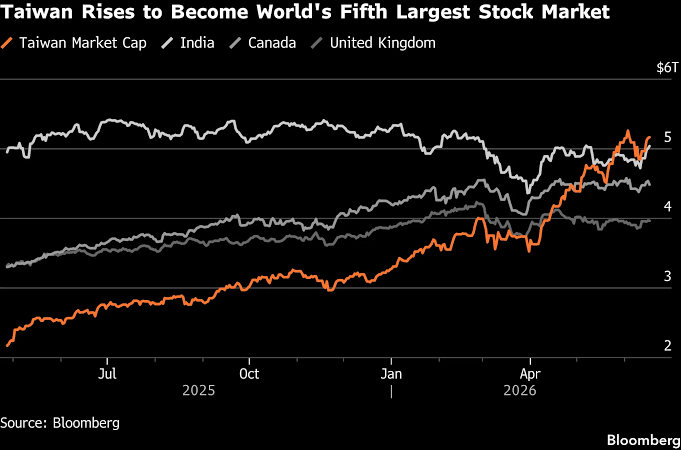

By the end of May this year, the total market value of Taiwan stocks exceeded India's, ranking fifth globally, only behind the United States, China, Japan, and Hong Kong.

Global capital is re-voting: The bottleneck of AI is in Taiwan. But this is just the first act; the second act is about to begin.

The first act is for the leaders to set the direction. NVIDIA has bound all the world’s computing orders into Taiwan’s processing, packaging, and server systems. Major weighted stocks like TSMC, MediaTek, and Delta Electronics have skyrocketed, re-evaluating Taiwan stocks from an "Asian manufacturing market" to an "AI infrastructure market." Once the leaders have proven the direction, capital will inevitably ask: As orders flow downwards, who has the most elasticity?

U.S. stocks experienced a similar script in 2020. In the first wave post-pandemic, the market bought companies like Apple, Amazon, Microsoft, and Tesla because they first demonstrated that cloud, digitalization, and electric vehicles were the major trends; but by the end of 2020, the market began to spill over, and the Russell 2000 small-cap stocks first rose above 2,000 points, reaching new historical highs in 2021.

The market is not ending; it’s switching from "buying leaders" to "buying elasticity." Today’s Taiwan stocks are in this rhythm as well.

The $100 billion to $150 billion Jensen Huang invests in Taiwan every year will not just stop at TSMC; it will spread to packaging, testing, servers, cooling, power supply, and factory engineering. While the leaders feast on the big sea, the smaller players eat the overflow; the same capital expenditure, when dropping on small-cap companies, has entirely different elasticity.

Moreover, it is even more favorable for Taiwan that cloud service giants still self-develop chips. Google TPU, Amazon Trainium, Meta MTIA—the AI arms race ultimately returns to Taiwan to grab shovels.

The leaders have already completed their task of showcasing Taiwan to the world; next, the market will need to reprice the smaller players that deliver for the leaders.

The sellers of shovels, who are quietly making big money, are hidden in an entire supply chain.

5. Money Enters Taiwan Stocks Second Act: A Generational Wealth Redistribution from the AI Cold War

In the last great power Cold War, humanity sent rockets to the moon. This time, the AI Cold War has no endpoint.

In the past, Taiwan was merely a manufacturing base; now, Taiwan has become the arms base of the AI Cold War. In the past, everyone asked whether Taiwan stocks could keep up with U.S. stocks; now the question has reversed: Without Taiwan, where will the U.S. giants realize their AI dreams?

This is the most critical truth behind this round of generational wealth redistribution: Money starts from all over the world and ultimately flows to places that can deliver.

2025 to 2026 is the first act, with markets re-evaluating TSMC and leading stocks.

2026 to 2028 is the second act, with global capital flowing into mid and small-cap stocks in the Taiwan stock supply chain.

Those who missed the first half of the AI craze cannot afford to miss the second half of Taiwan's stock surge.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。