Author: Zhao Ying, Wallstreet Insights

On July 6, the well-known semiconductor research institution SemiAnalysis posted six tweets on the X platform, revealing that the Nvidia Kyber NVL144 rack has been delayed for over 12 months due to manufacturing issues with PCB mid-boards. The Asian AI hardware supply chain responded with a significant drop.

Nvidia subsequently responded, stating that "the roadmap remains unchanged," but did not disclose specific progress details.

The controversy did not subside. On July 7, SemiAnalysis released another paid long article, aiming its "spotlight" on Nvidia. But this time, it no longer played the role of a "bearish" entity.

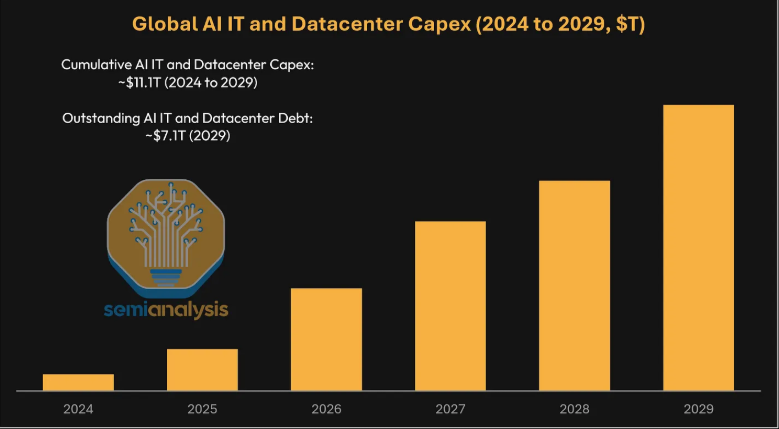

SemiAnalysis predicts: by 2029, the global AI debt financing scale will surpass $7 trillion. What does $7 trillion signify? It will be second only to the U.S. mortgage market (about $13 trillion), becoming the world's second-largest asset-backed debt market.

What role does Nvidia play in this? SemiAnalysis disclosed a strategic layout of Nvidia—the "Backstop Plan." Nvidia is using its AA/Aa2 investment-grade credit rating to provide minimum income guarantees for AI computing power leasing firms, thereby leveraging bank lending. In other words, Nvidia is acting as the ultimate lender and insurer for the entire AI ecosystem, booking substantial sales while absorbing a portion of the risk from insufficient downstream demand. SemiAnalysis likens Nvidia to a "central bank in the AI field."

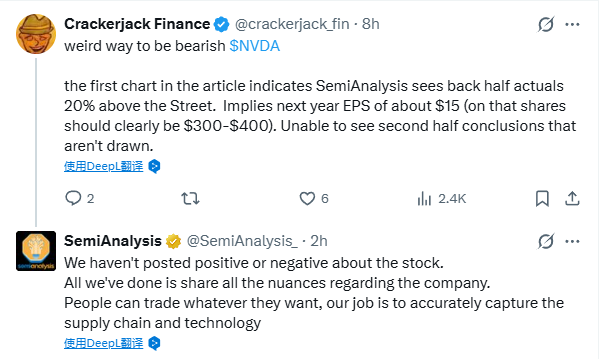

Regarding the discussions on the X platform about whether SemiAnalysis is "bearish on Nvidia," the institution stated:

it has not issued any positive or negative views on Nvidia's stock, but is accurately capturing supply chain and technology details, leaving the market to trade on its own.

AI Debt Snowball: Surpassing $7 Trillion by 2029, Pressing on the U.S. Mortgage Market

SemiAnalysis believes that AI infrastructure development is forming a multi-trillion-dollar level credit market. By 2029, AI-related outstanding debt could reach about $7.1 trillion, exceeding all other U.S. asset-backed debt markets except for the U.S. mortgage financing market.

This portion of debt mainly comes from two types of capital expenditures. One type is AI IT capital expenditures, including GPUs, networks, storage, and supporting CPUs; the other type is AI data center capital expenditures, including the infrastructure needed for housing these GPUs, such as power and cooling.

In the past, cloud giants like Google, Amazon, Meta, Microsoft, and Oracle mainly relied on their cash flow to build AI clusters. However, in the past year, Oracle, Meta, and even Google have increasingly started to use debt. As project scales continue to expand, market constraints are no longer simply about whether GPUs can be obtained, or whether a data center can be found, but rather whether enough cheap and long-term money can be borrowed.

SemiAnalysis concludes that the financing methods for AI capital expenditures are changing. The balance sheets of cloud giants are not limitless; if all AI clusters rely on a few investment-grade cloud vendors for endorsements, new projects will eventually encounter credit bottlenecks.

The "Trinity" Dilemma: Capital, Clients, and Data Centers are Indispensable

SemiAnalysis breaks down AI project financing into the "Trinity": capital, underwriting contracts, and data centers.

The first is capital. Lenders usually need to see long-term take-or-pay contracts from investment-grade cloud vendors, or similar credit guarantees, before they are willing to lend. In other words, what lenders truly value is not the credit of Neocloud itself, but the credit of the customers behind it.

The second is underwriting. Neocloud often needs to first prove its capability to pay GPU deposits and secure equipment to acquire customers. However, to obtain equity funding, it also needs to prove that it has customers and loans. This easily leads to a loop in the early stages of the project.

The third is data centers. Neocloud must either convince data center operators to rent capacity with customer contracts and financing, or build its own data center. The latter incurs more financial pressure and has a longer cycle.

This model locks the market into a "5-year term, cloud giants endorsement" template. The problem is, many VC-backed AI startups and inference service providers need short-cycle, large-scale computing power, rather than 5-year long-term contracts. Inference service providers are particularly unwilling to bear long-term price and demand risks, often preferring to forego computing power than sign leases longer than 1 year.

"AI Central Bank" Nvidia: Leveraging AA Rated Credit to Propel the Entire Market

Nvidia has proposed the "Backstop Plan" to fill this financing gap.

According to SemiAnalysis, Nvidia provides a minimum income guarantee for GPU leasing revenues to Neocloud. If third-party customer demand is insufficient, Nvidia promises to purchase computing power at a preset price; if Neocloud leases out the computing power at a higher price, Nvidia will share a portion of the excess revenue.

This type of arrangement is typically for a 6-year term, providing minimum income guarantees based on a pre-agreed price curve for the underlying GPU capacity. Neocloud can still rent the computing power to any customer and can offer more flexible lease terms. Only when market demand is insufficient and the computing power cannot be rented out at market prices will Nvidia's backstop be triggered.

This is the origin of the "AI central bank" metaphor. Nvidia is not actually issuing currency, but is playing a role similar to that of an ultimate buyer and credit guarantor in the AI computing power credit system. Lenders can base their assessments of the worst-case scenarios for projects on Nvidia's AA/Aa2 level credit, thereby being more willing to lend.

For Nvidia, this helps expand the buyer base for GPUs. If the market can only rely on a few ultra-large cloud vendors to sign 5-year underwriting contracts, GPU demand will soon hit financing constraints; meanwhile, these cloud vendors are also using self-developed chips to hedge against Nvidia's systems. Supporting Neocloud and more enterprise customers is tantamount to opening a new financing channel for GPU demand.

Dissecting the "Backstop Plan": How Much Nvidia Earns, How Much NeoCloud Earns

SemiAnalysis emphasizes that Neocloud is not using Nvidia's credit for free. Under the backstop structure, Neocloud must sacrifice a portion of its upward revenue to exchange for project financing capability.

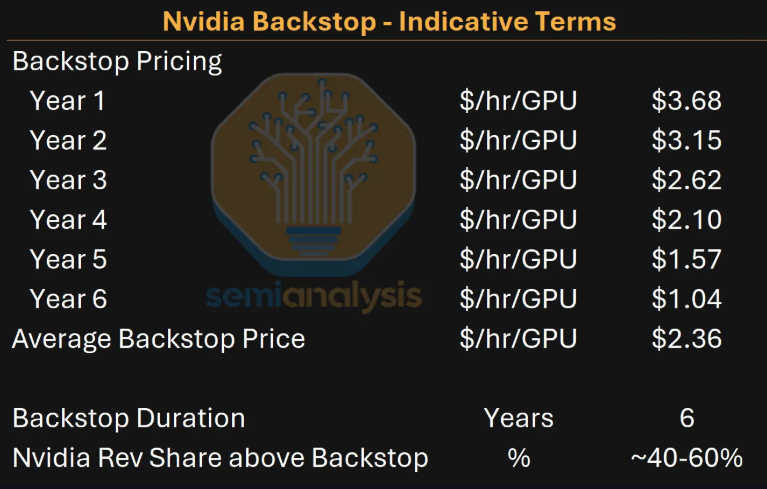

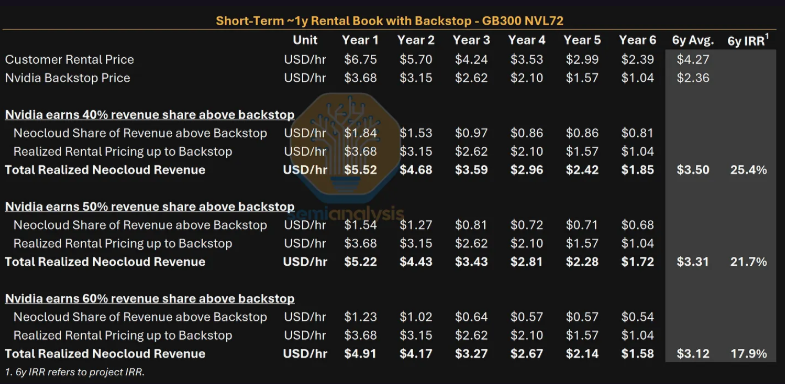

In a sample price curve, the average backstop price over 6 years is $2.36 per GPU per hour. If the first-year 1-year rental price for GB300 is $6.75 per hour, with a first-year backstop price of $3.68 per hour, then the difference between the customer price and the backstop price is $3.07. If Nvidia takes 40% of the amount above the backstop price, Nvidia would earn $1.23, Neocloud would earn $1.84, and Neocloud's actual income in the first year would be $5.52 per hour, lower than the $6.75 without the backstop.

Over six years, in this scenario, Nvidia's average fee is about 18%. Neocloud's project IRR would also decrease. In scenarios where Nvidia provides the backstop and primarily focuses on 1-year short-term rentals, the project IRR would be 25.4%; if there is no backstop but financing and leasing proceed smoothly, the IRR could reach 40.7%.

The key lies in the worst-case scenario. If demand is insufficient, Neocloud may have to rent the computing power only to Nvidia, resulting in project returns potentially approaching zero or even slightly negative. Lenders do not require the project to be profitable in the worst-case scenario; they only require it to be able to repay its debts. Thus, whether the debt can be established ultimately depends increasingly on the reliability of Nvidia's backstop.

This is also the core that investors should focus on: Nvidia's arrangement helps to boost GPU sales and Neocloud's expansion in the short term; however, if computing power demand falls short of expectations, the income gap will be borne by Nvidia. The debt may not be directly recorded on Nvidia's books, but the safety net of the financing model is increasingly concentrating on Nvidia's credit.

The Pricing of GPU Financing Essentially Depends on Who is Endorsing

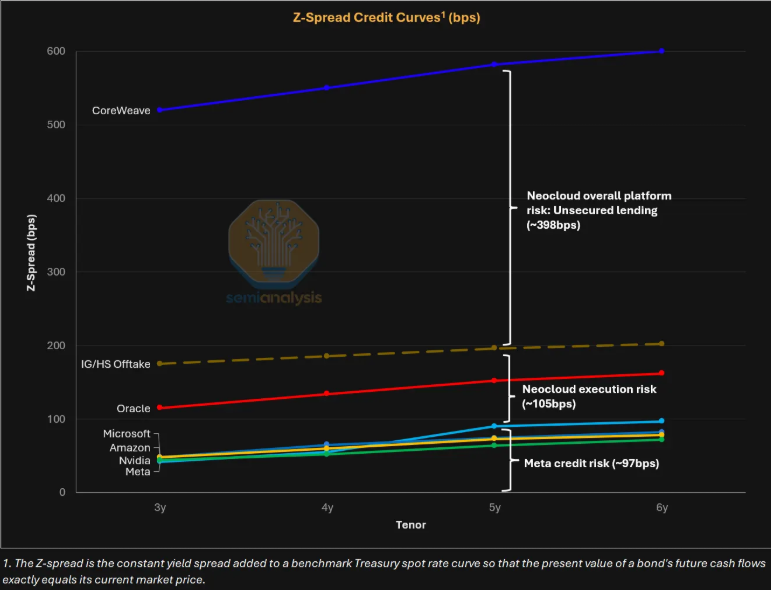

SemiAnalysis states that the current pricing of the GPU financing market primarily does not look at Neocloud's credit but rather who has signed long-term underwriting contracts.

CoreWeave is a reference. Its 5-year unsecured bond yield is about 10%; however, the fixed rate portion of the $8.5 billion DDTL 4.0 delayed draw term loan backed by Meta has a cost of about 5.9%, only 90 basis points higher than Meta's 5-year bond yield of around 5.0%. This 90 basis points approximately reflects the market's pricing of the execution risk for CoreWeave.

If Neocloud deviates from long-term cloud vendor underwriting, financing costs will rise significantly. For leading Neoclouds, unsecured financing might require an interest rate of about 10%, approximately 4 percentage points higher than financed endorsements. At a loan-to-value ratio of 70% to 80%, financing costs rise from 5.62% to 10%, pre-tax profit margins would drop from 14.8% to 5.4%.

Nvidia's backstop would position the pricing between the two: higher than the current cloud vendor endorsement transaction yield of about 5.9%, lower than the yield of 10% for CoreWeave's unsecured bonds. Banks are most concerned with the debt service coverage ratio (DSCR). For projects with Nvidia's backstop, the loan amount is usually calculated based on the scenario where the backstop is triggered, with the DSCR needing to reach at least 1.3 times in the initial years, corresponding to a typical loan-to-value ratio of 70% to 80%.

Public Projects Amplify in Asia-Pacific, the Backstop Model Begins to Materialize

Currently, the publicly announced Nvidia backstop projects are concentrated in the Asia-Pacific region.

The first is the 72MW AI plant of SharonAI in Australia. The project was announced in June 2026, aiming to expand to up to 40,000 GB300s under a 6-year backstop agreement. SharonAI disclosed a total backstop value of $4.88 billion, which translates to an average base price of about $2.33 per GPU per hour over six years.

Another is Firmus's 360MW AI cluster in Batam, Indonesia, possibly located within DayOne's facilities at Kabil Industrial Tech Park. This project was announced on June 29, 2026, showing that Nvidia's backstop is entering larger scales.

Firmus expects the project's customer revenue over six years to be between $25 billion to $30 billion, targeting customers that include AI-native companies, enterprise clients, and inference service providers, offering different lease terms. However, before deploying GPUs, Firmus still needs to determine the data center provider or continue to build its own.

SemiAnalysis also pointed out that Nvidia is not the only GPU vendor utilizing backstop arrangements. AMD has also provided similar arrangements to customers like AWS, OCI, DigitalOcean, Vultr, Tensorwave, and Crusoe last year: customers purchase more AMD GPUs, and if Neocloud cannot fully sell the capacity, AMD is willing to rent back a portion under long-term contracts for internal software development.

SemiAnalysis Denies Being Bearish, but the Market is More Sensitive to Its Signals

At the time of this article's publication, SemiAnalysis itself was embroiled in controversy.

On the morning of July 6, SemiAnalysis posted consecutive tweets on the X platform, stating that Nvidia's Kyber NVL144 rack architecture had encountered significant delays, pushed back over 12 months to 2028. This news garnered attention pre-market and led to declines in multiple AI hardware supply chain stocks in Japan, South Korea, and Taiwan. Nvidia subsequently responded, stating that its product roadmap had not changed, denying that core progress was affected.

This made it easier for the market to interpret SemiAnalysis's subsequent articles as either bearish or bullish on Nvidia. In response, SemiAnalysis stated on X that it has not published any positive or negative views on Nvidia's stock, but merely shared details about the company's supply chain and technology.

Crackerjack Finance countered the "bearish" interpretation, stating that SemiAnalysis's charts showed that actual data for the second half of the year was about 20% higher than market expectations, and based on this inferred that next year's earnings per share could be around $15, with stock prices expected to be between $300 and $400. THE Grand Poobah commented that, "the circular financing among three parties seems no longer sufficient," pointing towards market concerns over the complexity of financing structures.

The problem is that AI-related assets have undergone years of increases, with valuations and expectations at high levels. Any signals of supply chain risk or changes in financing structure will be quickly amplified. SemiAnalysis's clarifications may demonstrate that it has not directly issued stock opinions, but the market influence and credibility controversy of its supply chain revelations will continue to coexist after the Kyber NVL144 incident.

For investors, the true meaning of this "long article" is: AI competition is no longer just about "who has GPUs," but rather "who can piece together GPUs, debt, customer contracts, and data centers simultaneously." Nvidia's backstop mechanism may continue to amplify GPU demand but may also concentrate the tail pressure of the AI debt cycle more on Nvidia's own credit.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。