Author: Chloe, ChainCatcher

The KOSPI index has surged approximately 95% since the beginning of the year, nearly doubling. Just as the South Korean stock market is on a roll, another group of publicly listed companies in South Korea is gradually being pushed out of the market.

According to the Chosun Ilbo, the revision of listing regulations to raise the market retention threshold took effect on July 1, and some KOSDAQ DAT listed companies that profited through investments in cryptocurrencies are facing delisting risks. They are grappling with plummeting coin prices while also enduring capital outflow from the KOSDAQ market, with their market capitalization continuously falling below the new thresholds, making them susceptible to being kicked out of the market at any moment.

The South Korean government tightens policies, making it difficult to maintain listing status

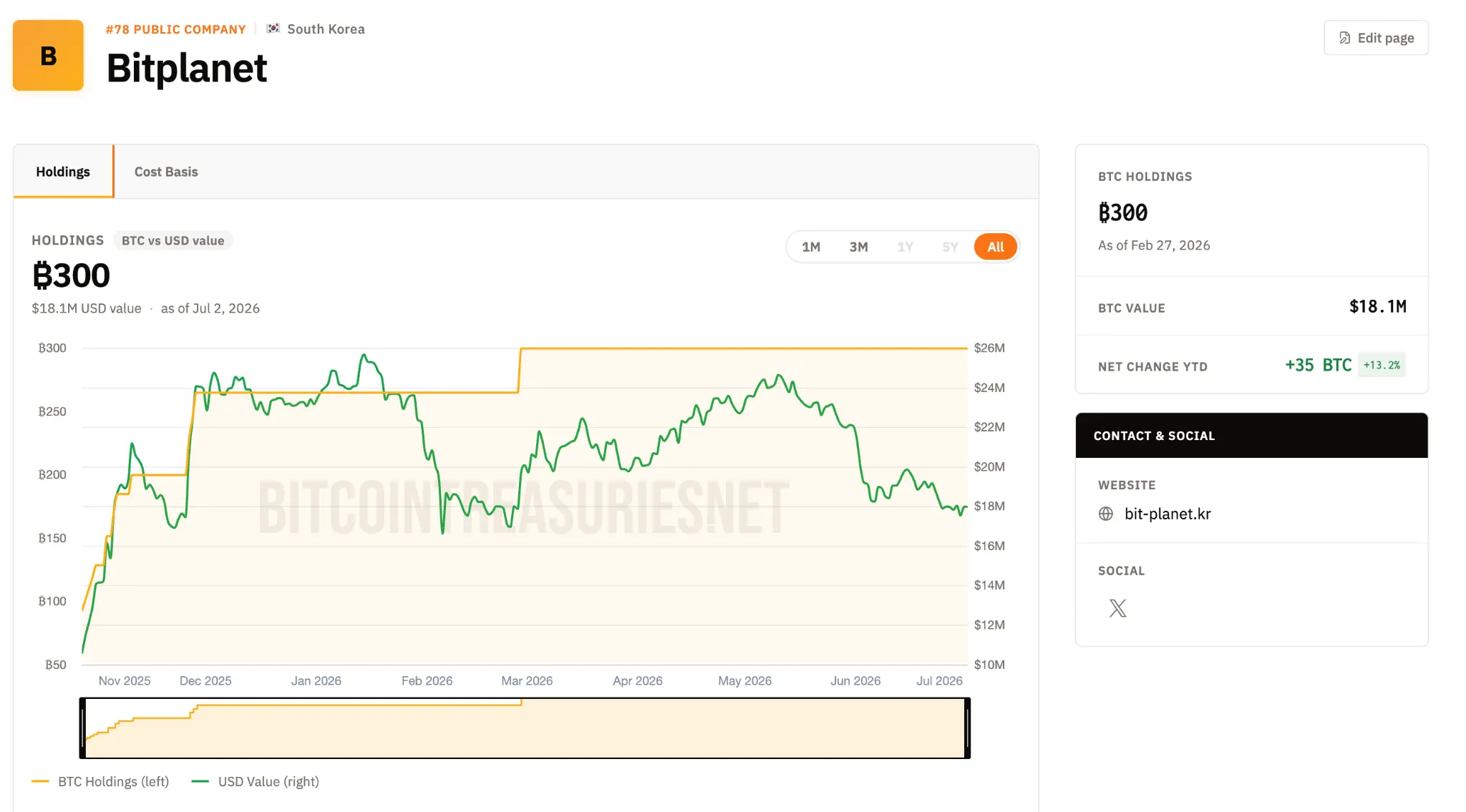

The DAT was initiated by Strategy, followed by Japan's Metaplanet, and South Korea's DAT companies are replicating the same script. For example, BitPlanet was acquired in July 2025 by a consortium led by Asia Strategy and Sora Ventures from the KOSDAQ listed company SGA, currently holding 300 bitcoins, with a long-term goal of accumulating 10,000; its CEO Lee Seong-hoon publicly stated that the inspiration for the company model came from Strategy and Metaplanet.

The issue is that this "issuing stocks to raise funds, buying coins, and a rising stock price" flywheel is highly dependent on rising coin prices; once coin prices reverse, many of these medium to small-sized DAT companies in South Korea must not only deal with financing issues but also the question of "can they maintain their listing status."

According to The Herald Business, this reform has tightened four major delisting criteria comprehensively, with the most lethal for DAT companies being the market capitalization threshold. The KOSDAQ maintained listing market capitalization standard rises from the current 15 billion won to 20 billion won (over 13 million USD), and will jump to 30 billion won again in January next year.

The new determination mechanism is quite strict: if a stock's price is below 1,000 won for 30 consecutive trading days, or its market capitalization is below 20 billion won for 30 consecutive trading days, it will be designated as a "managed stock (Caution)"; there is a 90 trading day recovery period after being designated, and if it cannot meet the standard for 45 consecutive trading days during this period, it officially enters the delisting process. The key point is that both the price and market capitalization criteria must be met "simultaneously"; as long as one of them fails, it is sufficient to constitute grounds for delisting.

At the same time, the common tactic of companies in the past to "manipulate stock prices" has also been shut down. When stock prices were too low and close to the delisting line, companies could consolidate multiple shares into one, instantly hiking the price per share, but the overall value of the company remained unchanged. The Herald Business explains that the new rules are designed to block this loophole: for example, if a company's stock price is 300 won, even if it consolidates the shares to raise the price to 1,200 won, as long as the adjusted per share value remains low, it will also be subject to delisting. Additionally, companies that have conducted a consolidation or reduction of capital within the past year are not allowed to use the same tactic if placed on the watchlist; even if allowed, the consolidation ratio cannot exceed 10 to 1.

The other criteria have also been tightened: the timing for assessing whether a company has fully suffered capital erosion has expanded from only looking at year-end financial reports to half-year reports also needing to be examined; the delisting penalty threshold accumulated due to financial report inaccuracies or violations has lowered from 15 points to 10 points, and a significant or intentional violation in a single instance is enough to trigger a review; the longest improvement period a company can seek after being placed on the delisting review list has been shortened from 18 months to 1 year.

KOSDAQ itself is weak, coupled with a weakening cryptocurrency market

According to the Chosun Ilbo, the risk of delisting is no longer hypothetical. Many companies are currently in a "compliant but unsafe" status: Parataxis Ethereum has a market capitalization of approximately 26.8 billion won, and BitPlanet about 33.1 billion won; both are above the 20 billion won threshold for the second half of the year, but Parataxis Ethereum faces potential risks when compared to the revised 30 billion won standard next January. The worst situation belongs to Parataxis Korea, which was already placed under substantive review for listing eligibility due to capital erosion in April, and its stock has been suspended. The Chosun Ilbo notes that if the trend of declining market capitalization continues, these DAT companies may face delisting procedures starting from BitMax in early next year.

Looking back, the direct trigger for this crisis is the weakening of coin prices. According to Bloomingbit, Bitcoin reached over $120,000 last July, driven by the U.S. Trump administration's pro-crypto policies; however, it has fallen back since the trade friction between the U.S. and China became a turning point last October, dropping to around $50,000 this month. Due to declines in coin prices in both the first and second quarters of this year, DAT companies are required to recognize large-scale valuation losses on their books, which may lead to further stock price impacts during the earnings season.

Adding insult to injury is the inherent weakness of KOSDAQ itself. While KOSPI has nearly doubled (up about 95%) this year, KOSDAQ has actually declined by about 10%, with capital concentrating toward major KOSPI stocks like Samsung Electronics and SK Hynix, marginalizing KOSDAQ and its DAT companies. These companies had attempted to fill the funding gap by issuing convertible bonds (CB) and preferred stocks but have been unable to withstand the overall decline in cryptocurrency asset prices.

The overall weakness of KOSDAQ is evident in the numbers. The Herald Business reports that the KOSDAQ index fell from 945.57 at the beginning of January to 851.37 as of last Friday, a decrease of nearly 10%, dragging down the market cap of constituent stocks. As of last week, excluding SPACs and special stocks, there were 178 KOSDAQ companies with a market capitalization of less than 20 billion won, about 10% of the total 1,748, a nearly threefold increase from 66 companies at the beginning of the year; there are also 180 "penny stocks" with prices below 1,000 won, with a total market capitalization of 6.14 trillion won.

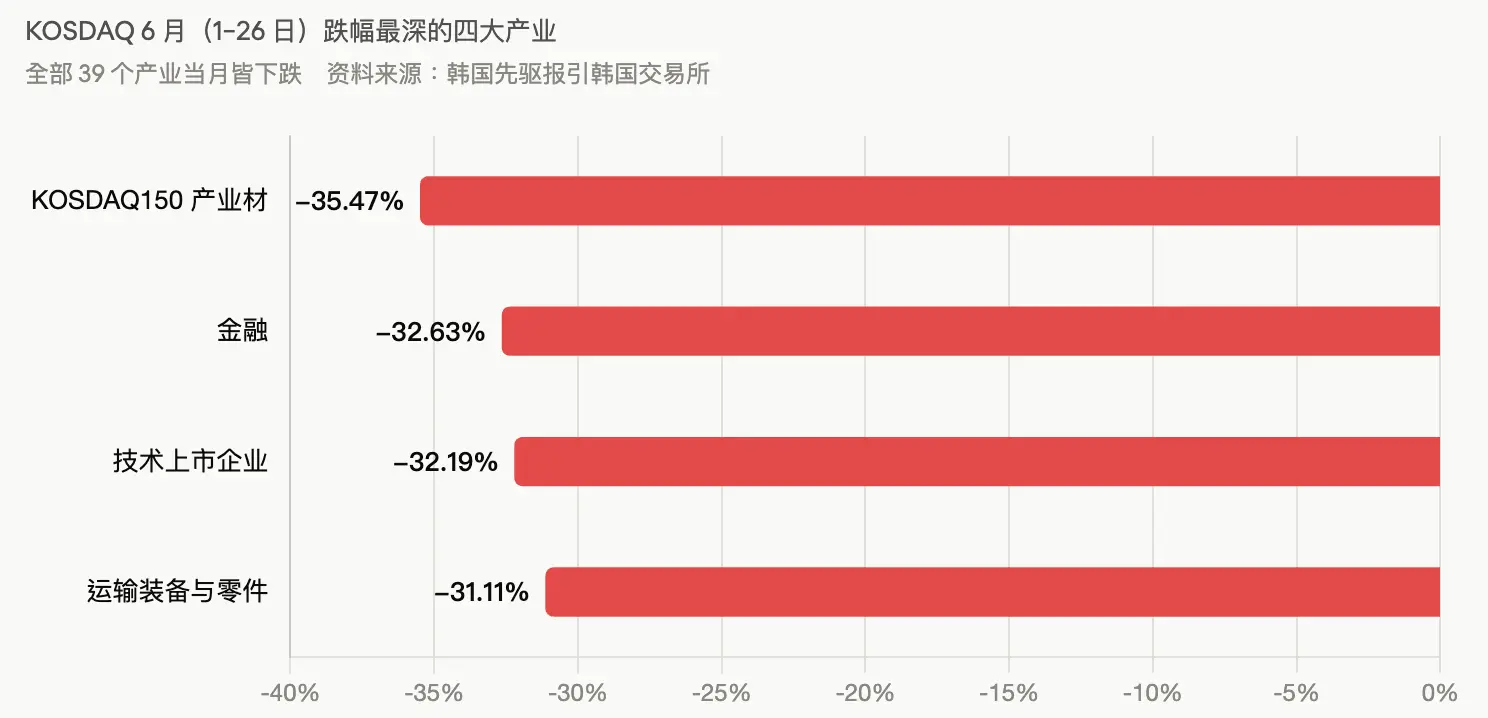

The Herald Business also cited data from the Korea Exchange, indicating that every one of the 39 sectors of KOSDAQ closed in the red in June (1 to 26), with the KOSDAQ150 sector leading the decline at -35.47%, and financial (-32.63%), technology listed companies (-32.19%), and transportation equipment and parts (-31.11%) also suffering declines exceeding thirty percent.

Conclusion

For these ultra-small companies, the room for self-rescue through financial engineering is being compressed. The Herald Business quotes industry views that the new "market capitalization requirement" will be harder to meet than the "stock price requirement"; a person from a KOSDAQ listed company candidly stated that penny stocks can still use non-compensatory capital reductions and stock consolidations to prop up their stock prices, but it is challenging to meet the market capitalization threshold without an actual increase in stock prices; attempting to solve this through mergers and acquisitions in a short time is not easy, and as long as the KOSDAQ remains sluggish, the number of companies failing to reach the market capitalization threshold will only increase.

A very representative example is Hyungji I&C (형지I&C), which conducted a 10 to 1 non-compensatory stock consolidation in March, raising its stock price to nearly 4,000 won, but its market capitalization still remained around 10.6 billion won, far below the new threshold, illustrating that even if the stock price temporarily meets the criteria, it still cannot pass the market capitalization hurdle. The Chosun Ilbo also emphasizes that the revised listing regulations contain provisions that limit reductions and consolidations after being designated as a managed stock, making it even more difficult for companies with no substantial stock price rebound to linger in the stock market.

Officials from the Korea Exchange downplay the impact, stating that a delisting wave will not occur immediately in July because companies on the management stock list still have a period for improvement before taking the next step. However, brokerage researchers are more pessimistic. Lee Jae-won, a researcher at Yuanta Securities (Korea), stated that in terms of capital supply and demand, profits, and interest rates, the current environment is all favorable for KOSPI; until personal fund inflows and profit rebound predictions receive confirmation, the relative weakness of KOSDAQ is likely to continue.

In other words, while the overall momentum of South Korean stocks is strong, this group of cryptocurrency concept stocks branded under “South Korean version of Strategy” is at a crossroads of survival amid the three-pronged assault of coin prices, market liquidity, and new regulatory rules.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。