Author: Claude, Trend Research

The news of Meta building a cloud business has been absorbed by the market, and after CoreWeave's 14% drop, the real issues have surfaced.

Bernstein estimates that Meta currently has about 20GW of data center capacity, with an additional approximately 14GW expected to come online in the next few years, making its scale comparable to that of major cloud providers. However, the fact that Google has been limiting its Gemini usage since March raises doubts about the premise that "Meta has excess computing power."

Does Meta really have excess computing power to sell, and how much is CoreWeave's order book worth in a world where "customers become competitors"? Bernstein analyst Madison Rezaei's latest report has put these two accounts on the table.

20GW in stock, 14GW under construction, Meta's scale is sufficient to run a cloud provider

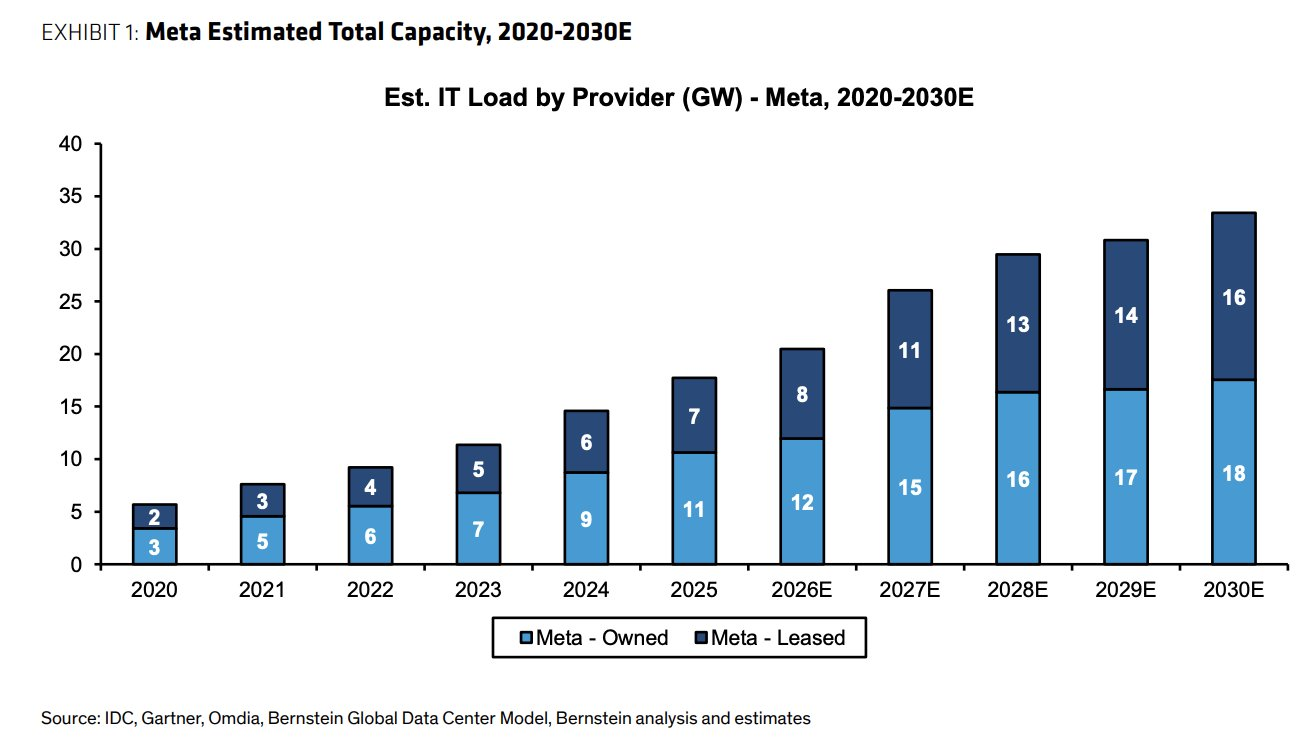

Rezaei estimates that Meta currently has a global data center footprint of about 20GW, with around 14GW expected to come online in the next few years, spanning both owned and leased assets. According to Bernstein's model, Meta's IT load has expanded from 5GW in 2020 to around 18GW by 2025, and it is estimated to reach 34GW by 2030, with owned capacity at 18GW and leased capacity at 16GW.

What does this number mean in the industry?

As of the end of the first quarter, CoreWeave's contracted power is about 3.5GW, with activated capacity just over 1GW and a target to reach 1.7GW by the end of the year. The new portion that Meta adds in the coming years is equivalent to the existing scale of ten CoreWeaves. Based on this, Rezaei judges that Meta's infrastructure "can now be directly compared to major cloud providers." Once it decides to open up this capacity, competing directly with AWS, Azure, and GCP would be structurally bad news for CoreWeave.

Capacity is the entry ticket, but having a ticket does not equate to chips on the table. The other side of this account is Meta's current situation regarding computing power.

On one hand, limited by Google, on the other, claiming to have surplus, these two matters are inconsistent

According to the Financial Times, Google has limited Meta's ability to purchase Gemini models due to its own lack of computing power since March, causing delays in some of Meta's internal AI projects, and the company has requested employees to conserve AI tokens.

Meta signed a six-year cloud agreement worth over $10 billion with Google in August 2025, but now it cannot even fulfill the capacity within the agreement. Furthermore, this June, Meta also locked in an additional 1.6GW of AI computing power with Crusoe, and its capital expenditure guidance for the first quarter was raised accordingly.

A company is engaging in three actions at once: aggressively buying computing power, being constrained by suppliers, and planning to sell computing power externally. Rezaei believes that this contradiction precisely constitutes a challenge to the notion of "excess capacity"; Meta may not actually have surplus at the moment.

The harmonizing explanation in the market is hierarchical scheduling. Meta reserves its latest generation clusters for cutting-edge model training while monetizing older GPUs and capacities freed up from non-core loads; what it buys from Google are ready-made model inference services like Gemini, and these three do not belong to the same pool. According to Morgan Stanley's logic, if Meta rents out 250MW at a price of $40 per watt, it could increase earnings per share by about $2.97 by 2028, corresponding to about an 8% upside.

The implications of these two readings for positions are completely different.

If Rezaei's suspicions hold true, Meta's cloud business may not get off the ground in the short term, making CoreWeave's sell-off an over-reaction; if hierarchical scheduling proves to be valid, Meta could earn new money with old computing power, keeping pressure on the valuation of the entire emerging cloud sector. The only way to distinguish these would be to look for two details when Meta officially announces: if the capacity opened is raw computing power or managed models, and whether pricing aligns closely with CoreWeave or is significantly higher.

CoreWeave Order Book Breakdown, nearly half the backlog is held by future competitors

More worthy of detailed observation than "whether Meta sells" is the structure of CoreWeave's order book itself.

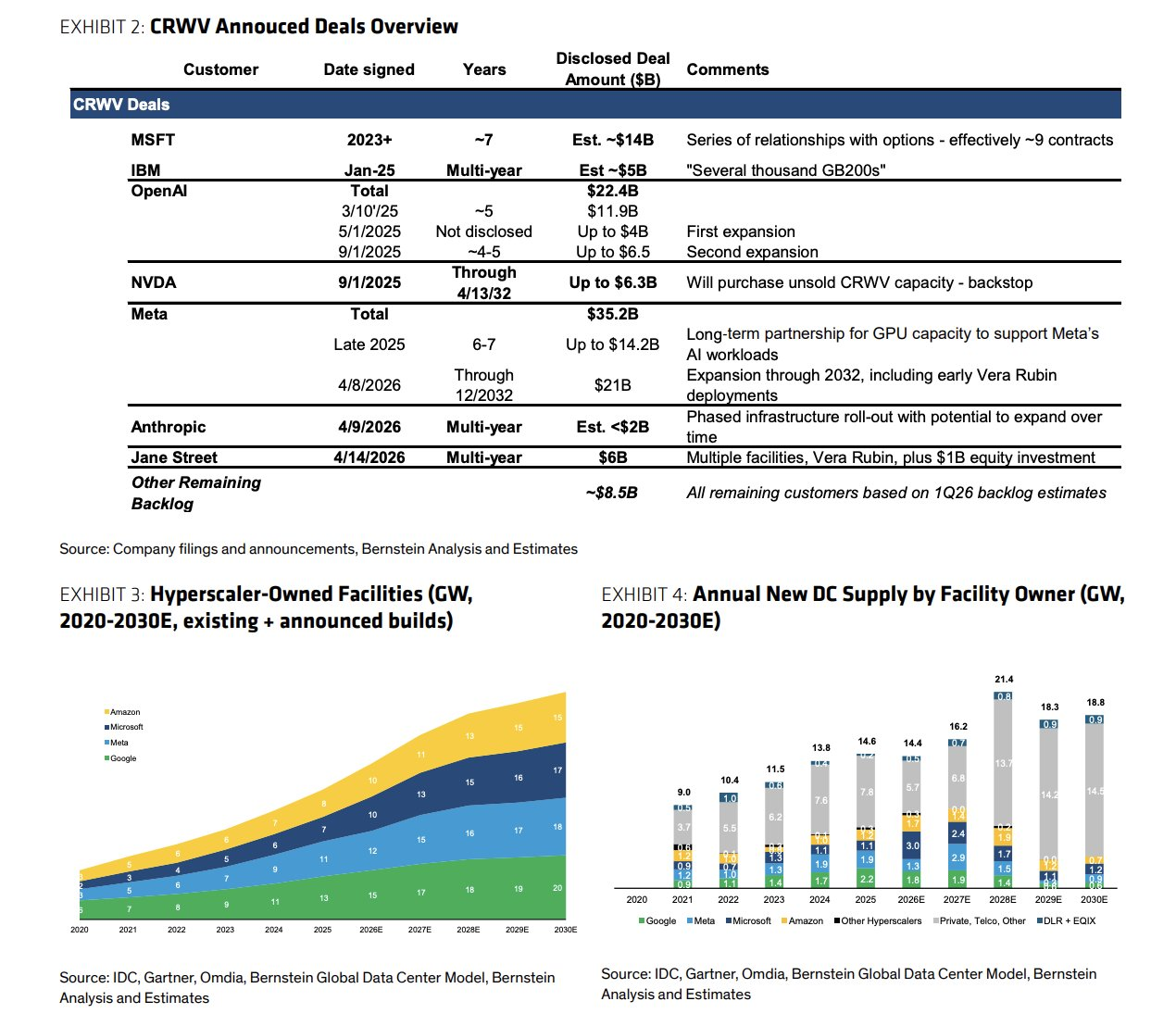

According to CoreWeave's disclosure, as of March 31, its backlog amounted to approximately $99.4 billion. Bernstein's breakdown shows that Meta accounts for about $35.2 billion of that (with $14.2 billion in September 2025 and $21 billion in April 2026, contracts locked until December 2032, including Nvidia's early deployment for Vera Rubin), making up over a third; Microsoft is around $14 billion, spread over approximately nine contracts. Combined, nearly half of the backlog comes from customers who are likely to be direct competitors when renewing contracts.

The remainder of the order book includes OpenAI's approximately $22.4 billion, Jane Street $6 billion (with another $1 billion in equity investment), Nvidia's $6.3 billion backstop agreement (receiving unsold capacity before 2032), and Anthropic has a long-term contract of an undisclosed amount, estimated by Wall Street to be between $4 billion and $7 billion.

Another analyst, McPeake, stated that Meta has no contractual right to resell capacity rented from CoreWeave before 2032. CoreWeave's cash flow cannot move before 2032.

The issue arises after 2032. Rezaei's deduction is that by then, both Meta and Microsoft will fully launch their self-built capacities, and across the renewal negotiation table will sit not customers eager to buy computing power, but competitors who are also selling computing power. CoreWeave faces not only customer loss but also pricing power for new orders being suppressed by more robust capital.

She summarized this as another testament to her consistent argument, "It is only a matter of time before better-capitalized major players enter the GPU leasing market, making CoreWeave's business model unsustainable in the long term." The bulls’ counter-argument is based on channel data, that GPU procurement behavior hasn't changed and the industry is still lacking cards, with McPeake giving a built-in rating of a $250 price target, claiming the sharp drop has provided a buying opportunity.

The risk period for valuation starts now

Putting the arguments of both bulls and bears on a timeline, the divergence is actually not at the factual level.

Before 2029, CoreWeave has no debt maturities, its contracts are locked, and its first-quarter revenue grew by 112% year-on-year, indicating limited short-term financial risks, an aspect the bears do not deny.

From 2031 to 2032, the first batch of major contracts will enter the renewal window, and by then Meta and Microsoft's self-built capacities will surpass 30GW and corresponding scales, respectively, with renewal prices and rates serving as true pressure tests. The market usually begins pricing renewal risks one to two years in advance, which means that around 2029, "the discount on order value" will start to be reflected in the valuation.

The current 14% drop can be understood as a rehearsal for this repricing. For holders of CoreWeave, the short-term tracking signals are:

1. The form and pricing of the announcement regarding Meta's cloud business,

2. The proportion of non-major customers in CoreWeave's subsequent new signed orders.

The latter will determine whether the narrative of "half the orders held by competitors" will be diluted or reinforced. For holders of Meta, the story of selling computing power has limited financial elasticity, as Morgan Stanley's estimated 8% upside is based on a 250MW rental scale, while the reality of being constrained by Google indicates that the capacity that can be freed up in the short term may not support larger imaginations.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。