Written by: Rita

Trend Guide

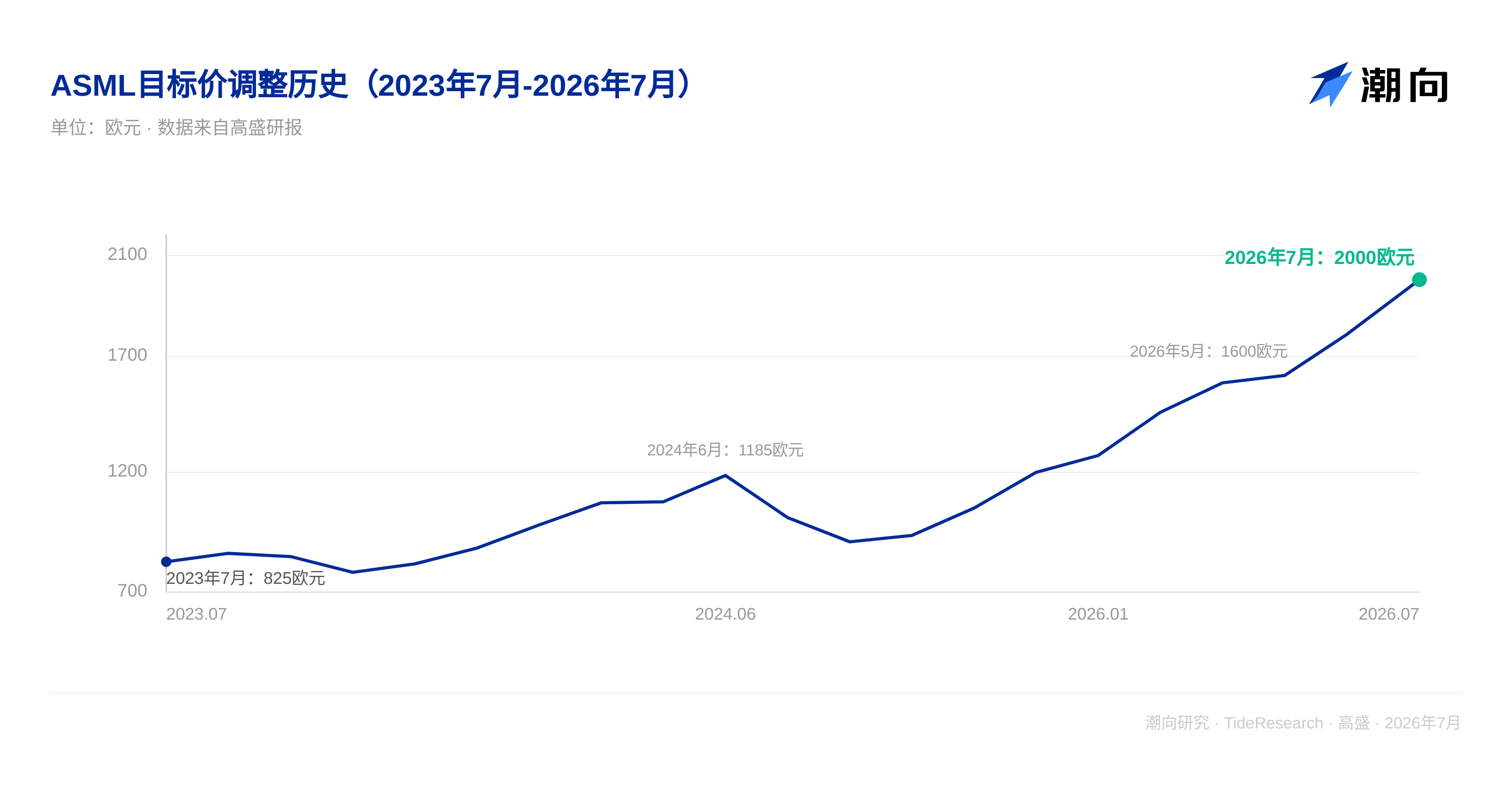

On July 1, Goldman Sachs raised the 12-month target price for ASML from 1770 euros to 2000 euros, maintaining a buy rating. This adjustment was made before the second quarter earnings report on July 15, directly triggered by the upward revision of capital expenditure expectations from storage chip manufacturers, with Micron and Samsung's latest capital expenditure plans factored into Goldman Sachs' forecasts for ASML's equipment orders in the coming years.

Goldman Sachs simultaneously raised the valuation multiple from 40 times to 43 times the expected price-to-earnings ratio for 2027, citing a more optimistic view on storage and advanced process demand. Based on the latest closing price of 1721.40 euros, the target price corresponds to approximately 16.2% upside potential.

Substantial Upward Revision of Storage Capital Expenditure

The core data point triggering this revision came from Micron. In its latest quarterly results, Micron provided a capital expenditure guidance of about $50 billion for the fiscal year 2027, which Goldman Sachs calculates is significantly higher than previous expectations, with about half of the increase coming from construction-related capital expenditure. Goldman Sachs believes that demand for storage will continue to outpace supply, and this upward revision in capital expenditure will drive a multi-year capacity expansion cycle, benefiting semiconductor equipment manufacturers. ASML, having a relatively higher exposure in the storage sector and a EUV equipment delivery cycle of over 12 months, stands to benefit more visibly. Samsung also announced an investment plan of about 245 trillion won over the next 15 years (from 2026 to 2040), with about 76% directed towards semiconductors; although Samsung did not disclose the specific breakdown of capital expenditure and research and development, Goldman Sachs believes this long-term investment constitutes a substantial benefit for ASML.

This Year’s Chinese Market Digesting, Expected Recovery Next Year

Goldman Sachs believes the company's outlook for this year’s Chinese market may be somewhat conservative, as demand in the region remains strong, and other semiconductor equipment peers are also optimistic. However, Goldman Sachs acknowledges that a portion of the capacity shipped to China last year needs time to be digested this year. Looking ahead, the tight supply-demand situation for traditional storage gives Chinese manufacturers room to capture shares in the overseas foundational storage market, which will further drive capacity expansion; once the digestion period concludes, extra expenditures in the Chinese market are expected by 2027, alongside local foundry construction plans bringing new rounds of equipment orders.

Customer Structure Improving, EUV Demand Rising

Goldman Sachs pointed out that advanced process customers outside of TSMC are accelerating their catch-up, which aligns with previous reports suggesting that ASML’s stock is undervalued. New players driven by AI may also bring additional demand increments, especially some large-scale infrastructure projects, where the implied scale of equipment procurement could be quite substantial. Additionally, as the advanced process completes its transition to Gate-All-Around (GAA) transistors, the layers of EUV will continue to increase, with Micron recently signing a multi-year EUV supply agreement with ASML for the 1-delta process node and subsequent generations, further corroborating the view of rising EUV demand.

Goldman Sachs listed four questions that investors will continue to monitor: First, the EUV and DUV capacity planning for 2027; historically, the company has prepared the supply chain for 90 units of equipment. If cycle time and delivery progress are further optimized, output may slightly exceed 90 units; second, whether there are new developments in orders for 2028; third, the latest situation in the Chinese market; and fourth, the pace of adoption of High NA equipment. Goldman Sachs believes that storage customers may adopt High NA faster than logic chip customers; seeing relevant order evidence would be a positive signal.

Earnings Forecast and Valuation

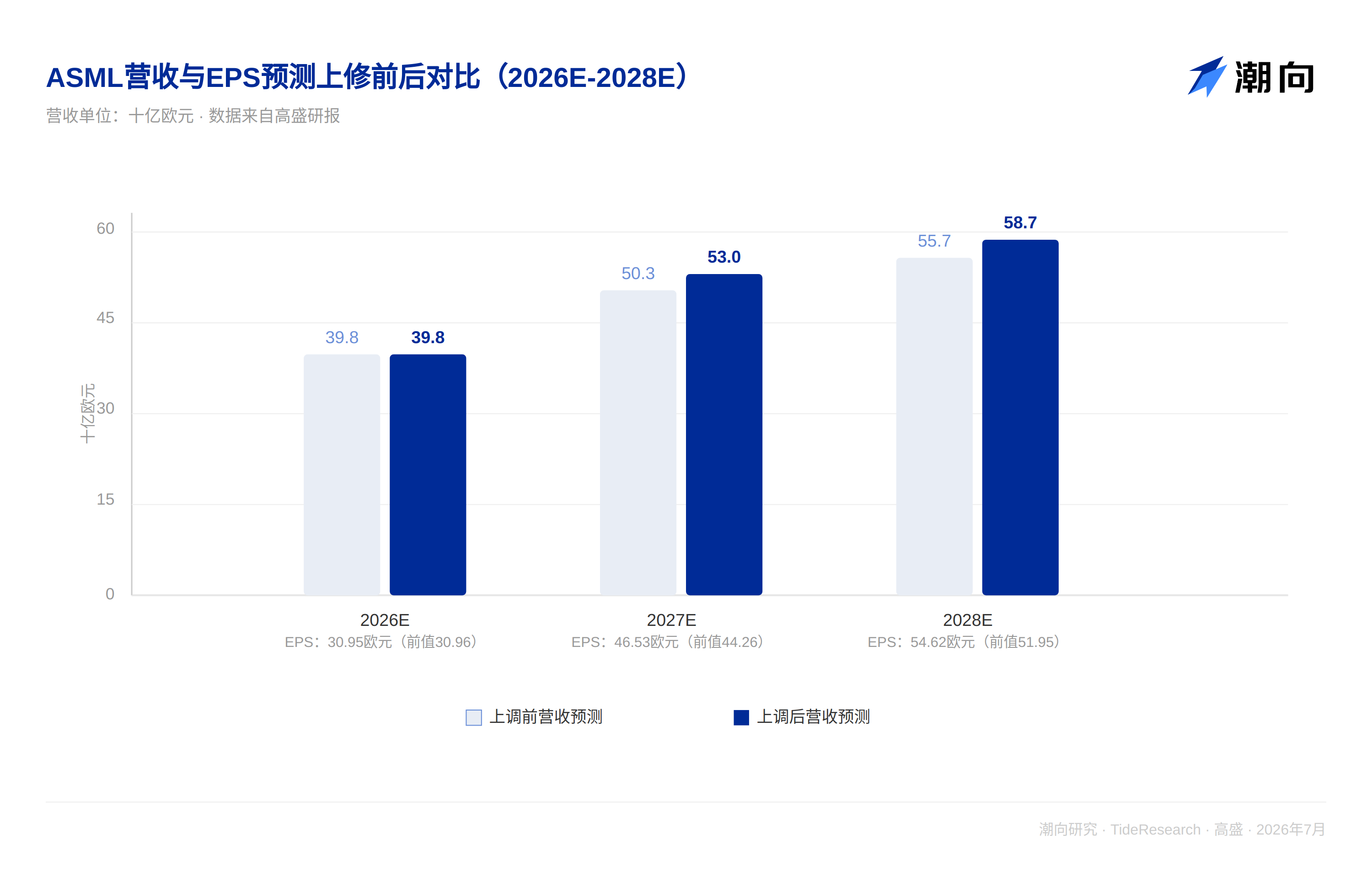

Goldman Sachs maintains its revenue forecast for the fiscal year 2026 unchanged but raises its revenue estimates for fiscal years 2027 to 2030 by 5% to 9%, reflecting a more positive view on advanced process demand (especially storage capital expenditure), while also being more optimistic about ASML's DUV business, based on the expectation of a recovery in the Chinese market in 2027. Accordingly, the forecast for earnings before interest and taxes for fiscal year 2026 remains unchanged, while forecasts for 2027 to 2030 are also raised by 5% to 9%; earnings per share estimates are raised by 5% to 8% for the period from 2027 to 2030.

Goldman Sachs set a target price of 2000 euros, up from 1770 euros, corresponding to 43 times the expected price-to-earnings ratio for 2027 (previously 40 times). The increase in valuation multiple reflects a more optimistic judgment of growth prospects in the coming years. Based on the latest forecasts, ASML's current stock price corresponds to about 32 times the expected price-to-earnings ratio two years from now, situated within the long-term historical range of 25 to 35 times. Main risks include delays in EUV equipment delivery, cyclical fluctuations in capital expenditure, and adverse changes in market share.

Trend Perspective

This revision is actually driven by two lines. One is that Goldman Sachs has incorporated Micron's and Samsung's capital expenditure expectations into its revenue model; such long-term capital expenditure commitments have significant elasticity, and whether Micron and Samsung's actual investment progress will meet the plans remains uncertain. The other line is that Goldman Sachs itself raised the valuation multiple from 40 times to 43 times, which is essentially paying a higher price for the same earnings forecast and is not solely supported by earnings upgrades. The second quarter earnings report will be released on July 15; this adjustment is essentially a preemptive incorporation of external industry signals into the model before actual performance disclosure, and real validation will have to await the order and outlook data in the earnings report.

Disclaimer

This article is a compilation and interpretation of research reports by third-party brokerage firms by Trend Research. The ratings, target prices, earnings forecasts, and related assessments quoted in the text are solely the views of the analysts of that brokerage firm and represent the stance of their respective institutions; they do not represent the views of Trend Research nor constitute any investment advice.

The market is risky, and decisions must be independent. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。