Written by: Rita

Trend Guide

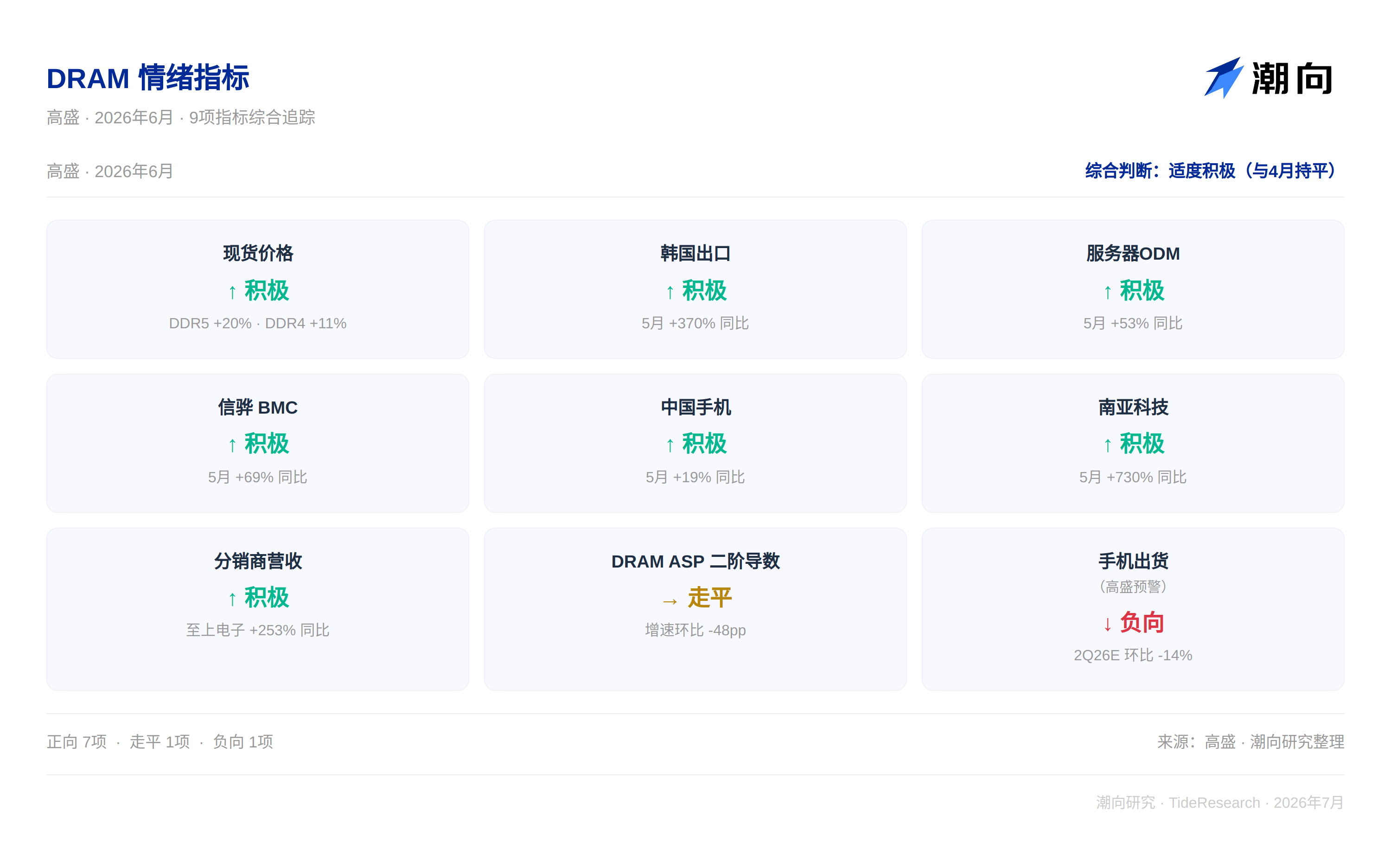

Goldman Sachs released the DRAM sentiment index monthly report on June 30, with 7 out of 9 indicators pointing positive, 1 flat, and 1 negative, giving a comprehensive judgment of "moderately positive," consistent with April. However, two things are particularly noteworthy: the price increase inertia of DDR5 is weakening, while the pricing expectations for HBM in 2027 are being quickly revised upward.

Since May, DDR5 spot prices have risen by 20%, while South Korean DRAM exports reached a historical high in May, growing 370% year-on-year. Nanya Technology has seen triple-digit growth in revenue for 10 consecutive months. However, the second derivative of Samsung's DRAM ASP has turned negative, decreasing by 48 percentage points, indicating that the acceleration of price increases is weakening. This time, Goldman Sachs raised its expectation for Samsung's HBM price growth in 2027 from +14% to +44%, clearly stating that "there may still be upward risks." The narrative around memory is shifting from "how much can it still rise" to "how to price after the rise."

DDR5 price increases are still running, but the acceleration is decreasing

Since May 1, DDR5 16Gb spot prices have risen by 20%, which is 25% higher than the May contract price. DDR4 8Gb increased by 11% during the same period, surpassing the contract price by 45%. The significant premium of spot prices over contract prices indicates a tight supply-demand situation in the short term, and buyers are willing to pay a premium to obtain inventory.

However, the second derivative of Samsung's DRAM ASP is worth noting. Goldman Sachs estimates that Samsung's DRAM ASP will rise about 46% quarter-on-quarter in the second quarter of 2026, following a 93% increase in the first quarter. The magnitude of price increases has shifted from a jump to a gradual rise. As the base for price increases gets higher, the increase will naturally narrow, and there are no issues on the demand side.

Servers and phones are supporting demand

The four major server ODMs in Taiwan (Inventec, Quanta, Wistron, and Pegatron) saw a year-on-year revenue increase of 53% in May, with rack-level AI servers and ASIC AI server shipments both climbing. The world's largest BMC supplier, Inspur, experienced a year-on-year revenue increase of 69% in May, continuing growth on a high base of 75% from the same period last year.

Mobile phone shipments in mainland China rose by 19% year-on-year in May, maintaining positive growth for two consecutive months. Goldman Sachs's China team expects shipments to fall by 14% quarter-on-quarter in the second quarter of 2026 due to storage price increases raising overall costs and suppressing end-demand. This judgment itself creates an interesting tension: while rising storage prices benefit storage manufacturers, excessive price increases may hurt downstream demand.

HBM expectations represent the biggest change this time

Goldman Sachs made a crucial adjustment to the 2027 HBM pricing forecast in its report, raising the expectation for Samsung's HBM price growth from +14% to +44%, more than tripling it. The logic is that the strong pricing trend of traditional DRAM will serve as a reference during annual HBM negotiations. The price difference between traditional DRAM and HBM is widening, allowing for price increases in HBM.

Goldman Sachs also clearly stated that "there may be further upward risks," as HBM supply and demand are tight, and the price gap between traditional DRAM and HBM continues to expand. If this judgment holds, it means that the peak storage prosperity in 2027 may be higher than the market currently anticipates.

South Korean export data can verify the heat

South Korea's DRAM export value reached a historical high in May, increasing by 21% month-on-month and 370% year-on-year, surpassing the previous high in March. Nanya Technology's May revenue increased by 730% year-on-year, marking the 10th consecutive month of triple-digit growth driven by robust DDR4 price increases. Taiwanese distributor Jie Shun Electronics experienced a year-on-year revenue increase of 253% in May, with a quarter-on-quarter increase of 54%, reflecting a strong willingness in the downstream to procure inventory.

Samsung remains the most direct target in this sector

Goldman Sachs maintains a buy rating on Samsung Electronics, with a target price of 480,000 won (currently about 323,000, with 49% upside), and a preferred stock target price of 360,000 won. The valuation method is based on the sum of the segment valuations of a 12-month forward EV/EBITDA. Downside risks include a significant deterioration in storage supply and demand, sharp contraction in mobile phone profits, and loss of market share in the mobile OLED segment.

Trend Perspective

The most noteworthy detail in Goldman Sachs's monthly report is the adjustment of the 2027 HBM pricing expectation from +14% to +44%. The market already knows that DDR5 is still rising, but the upward revision of HBM pricing is new. This means that the market is converting the shortage of traditional DRAM into the upward pricing space for annual HBM negotiations.

Another noteworthy piece of data is the negative turn of the second derivative of ASP. The cycle has not yet peaked, but the phase of "rising faster and faster" has already passed. We are now entering a phase of "still rising, but more slowly." Historically, during this phase, memory stocks primarily earn from realized profits, and there is limited room for further valuation expansion.

For Chinese investors focusing on storage concepts in US and A-shares, this report highlights two clues: in the short term, the spot premiums for DDR5 and DDR4 are still present, but the phase of accelerated increases is nearly over; in the long term, the upward revision of HBM pricing indicates that the high point in 2027 may be higher than previously imagined. The intersection of both determines how the current positions in memory stocks should be configured.

Disclaimer

This article is a summary and interpretation of third-party brokerage research reports by Trend Research. The ratings, target prices, earnings forecasts, and related judgments quoted in the text represent the views of the respective brokerage analysts and do not represent the views of Trend Research, nor do they constitute any investment advice.

The market is risky, and decisions should be made independently. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。