Curry, Deep Tide TechFlow

Deep Tide Introduction:

Holding 847,000 bitcoins, Strategy launched the "Digital Credit Capital Framework" on June 29, completely rewriting the script of only buying without selling over the past four years. The new framework authorizes the sale of bitcoins to raise up to $1.25 billion, sets a cash reserve of $2.55 billion, raises the STRC dividend yield to 12%, and authorizes a $1 billion buyback of its own securities. The background is that MSTR plummeted 36% in eight days, STRC's preferred stock fell below par by about 24%, and the annual dividend obligation quadrupled to $1.2 billion. For holders, this is a "stop-loss plan," but whether it can stop the bleeding depends on the price of bitcoin.

Strategy (formerly MicroStrategy) officially admits that the flywheel of infinitely buying coins through issuing preferred stock can no longer turn.

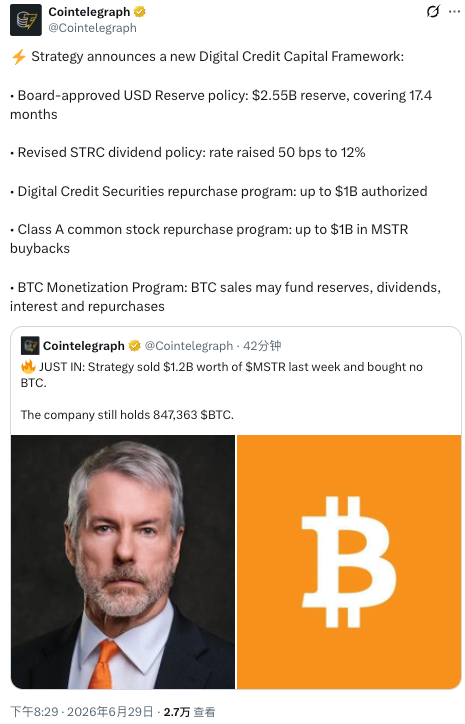

On June 29, this largest corporate bitcoin holder in the world announced the launch of the "Digital Credit Capital Framework," using a complete set of cash reserves, repurchase, and sell coin mechanisms to backstop its nearly out-of-control capital structure. The framework includes five components: USD reserve policy, revised STRC dividend policy, digital credit security repurchase plan, Class A common stock repurchase plan, and a bitcoin monetization plan.

The most impacted item is: the company's board authorized the sale of bitcoins to raise up to $1.25 billion to replenish cash reserves, pay preferred stock dividends and interest, or repurchase its own securities. For a company that wrote "never sell coins" into its creed, this is equivalent to officially paving the way for selling coins.

Founder Michael Saylor's wording in the statement has changed from the past. He said bitcoin remains the company's "primary financial reserve asset," but then acknowledged: "Digital credit requires liquidity, discipline, and active capital management."

Translated, it means that simply hoarding coins cannot sustain the $1.2 billion annual dividend bill.

STRC dividend yield soared to 12%, preferred stock falling below par is the trigger

To understand this framework, one must first see how passive Strategy is now.

The company simultaneously announced that it has raised the annual dividend yield of its variable rate Series A perpetual preferred stock STRC from the previous approximately 11.5% to 12.00%, effective for record dates on or after July 1. On the surface, it seems to enhance returns for investors, but in reality, it is market-driven — the STRC price has already fallen to about $75 to $76, at about a 24% discount to the $100 par value, hitting a historic low.

STRC falling below par has hit the fatal flaw of Strategy's financing model. This preferred stock was originally the company's "money printer": issuing continuously at prices close to or above par, with the raised funds going to buy bitcoins. Once the price is deeply discounted, new preferred stock cannot be issued at a good price, and the entire financing flywheel gets stuck. CryptoQuant's research director Julio Moreno calculated in a report on June 23: Strategy's annual dividend obligation has skyrocketed from about $300 million at the beginning of the year to about $1.2 billion, quadrupling in a year, while the dividend coverage period has dropped sharply from more than seven years to about 14 months. He directly suggested the company suspend buying coins and rebuild cash reserves to about $2.8 billion first.

For preferred stockholders, a 12% coupon sounds enticing, but the premise is that the company can afford to pay it. The new framework requires that the USD reserves must cover at least 12 months of preferred stock dividends and interest obligations, essentially writing "whether we can pay on time" into a hard constraint.

$2.55 billion cash reserve, shifting from "hoarding coins" to "hoarding cash"

Strategy's cash reserves are visibly expanding at a remarkable rate, with a direction completely opposite to the past.

According to the company's 8-K filing, as of June 28, the USD reserve balance was $2.55 billion, including expected cash income from the ATM issuance of Class A common stock that has not yet been settled. This number has notably jumped from $1.4 billion on June 21 and $1.44 billion when established in early December 2025. Where is the money coming from? The answer is selling its own stock, not buying coins.

The operations in the past three weeks have already shown signs of turning. In the week of June 22, the company only bought 520 bitcoins, spending about $34.9 million, which is one-third of the previous week; during the same period, it sold 2.71 million shares of MSTR common stock to raise $335.5 million, but only put less than 11% into bitcoins, with the rest all going into cash reserves.

Cointelegraph posted on June 29 that Strategy sold $1.2 billion worth of MSTR stock last week without buying any bitcoins. If this figure is true, it means the momentum of selling stocks to replenish cash is increasing (Note: The $1.2 billion one-week sell-off scale is significantly higher than previously disclosed weekly data, and must be checked against the company's latest filings before publication). The company currently still holds 847,363 bitcoins, with a weighted average cost of about $75,651 per coin.

The cost of shifting to "hoarding cash" is dilution. When the MSTR stock price falls below its net bitcoin value per share, issuing new shares will dilute the corresponding number of bitcoins per share. MSTR has already fallen to about $82 this week, nearing a two-year low of $81.81; the "premium" upon which the flywheel relies for operation no longer exists.

Each $1 billion repurchase, trying to buy back at a discount

The framework also hides two "knives" for repurchase: the digital credit security repurchase plan and the Class A common stock repurchase plan, each with an authorized limit of up to $1 billion.

The logic is not complicated. STRC and preferred stock as well as MSTR common stock are trading at deep discounts, and the company can use cash (or proceeds from selling coins) to repurchase at low prices, theoretically narrowing the discount and protecting the price. Bitcoin critic Peter Schiff has repeatedly called out on X recently, saying Saylor's best choice is to sell coins to buy back stock to reduce the discount.

Now Strategy has written this advice into the formal framework, but Schiff also warns that forcefully selling coins may conversely push down bitcoin prices, trapping the entire structure in a death spiral.

Whether the repurchase will be effective depends on how much cash the company has. For investors holding MSTR or preferred stock, the $1 billion authorization is just an upper limit, not necessarily indicating it will all be executed; the actual buying pace will depend on future disclosures.

Not just stopping the bleeding: legal investigations and debt pressure

This framework was hastily introduced under multiple pressures; merely looking at financial numbers is not enough.

On June 25, Rosen Law Firm disclosed that it is investigating Strategy and Saylor, indicating they may have issued "materially misleading information" to investors regarding their bitcoin holdings, covering all five securities: MSTR, STRF, STRC, STRK, STRD. This investigation is still in its early stages and has not yet formally filed a lawsuit, but the timing coincides with a continuous drop in stock prices.

The debt side is also tightening.

According to multiple media reports, Strategy's balance sheet has accumulated debt of about $8.2 billion, and since 2026, cash reserves have shrunk by about 38%; the company also conducted a debt buyback in May. With bitcoin's current price at about $60,000, it has fully fallen below the cost line of all purchase batches from 2024 to 2026 for Strategy, with a book loss ranging from $10.6 billion to $14 billion (different sources have varying figures).

For investors who are currently on the sidelines, the key indicator to watch is the discount of MSTR stock price relative to its net bitcoin value per share. Once the discount persists too deeply, the ATM issuance engine will stall. That is the real outcome this framework aims to avoid but may not be able to.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。