Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: Those betting on AI storage will face a challenge on June 24. Micron will announce its quarterly performance after the market closes on that day. The stock price has risen from $103 a year ago to $1134, an approximately 11-fold increase, with a market value of $1.28 trillion. The market is betting that it will continue to rise, with Wall Street consensus expecting this quarter’s earnings per share to skyrocket approximately 932% year-on-year, and revenue to grow around 270%. The greater the increase, the higher the expectations that the financial report must meet. This financial report is the moment to verify this bet and represents the toughest challenge in the AI storage market this year.

If you hold Micron stock, or are looking into AI, chips, and storage, this financial report after market close on June 24 is worth watching.

Micron’s stock price has risen from $103 to $1134 in the past year, about 11 times. Its market value is $1.28 trillion, up around 297% this year. At this position, those buying more are surely thinking, "How much longer can this wave keep rising?" The financial report is the moment to verify this bet.

Currently, market consensus remains bullish.

According to Cryptobriefing reports, Wall Street expects Micron’s earnings per share for this fiscal quarter to be approximately $19.72, up from only $1.91 for the same period last year, marking an increase of about 932%; revenue is expected to be around $34.5 billion, approximately 270% year-on-year growth. Supporting this set of numbers is High Bandwidth Memory (HBM, a type of high-speed storage chip specifically designed for AI accelerators), and Micron’s entire HBM production capacity for 2026 has already been sold out, with orders extending to the end of the year.

Analysts have adjusted upward all year, and expectations are still climbing

This wave of increase did not come from nowhere. Over the past three months, Wall Street has been rapidly raising its earnings forecasts for Micron.

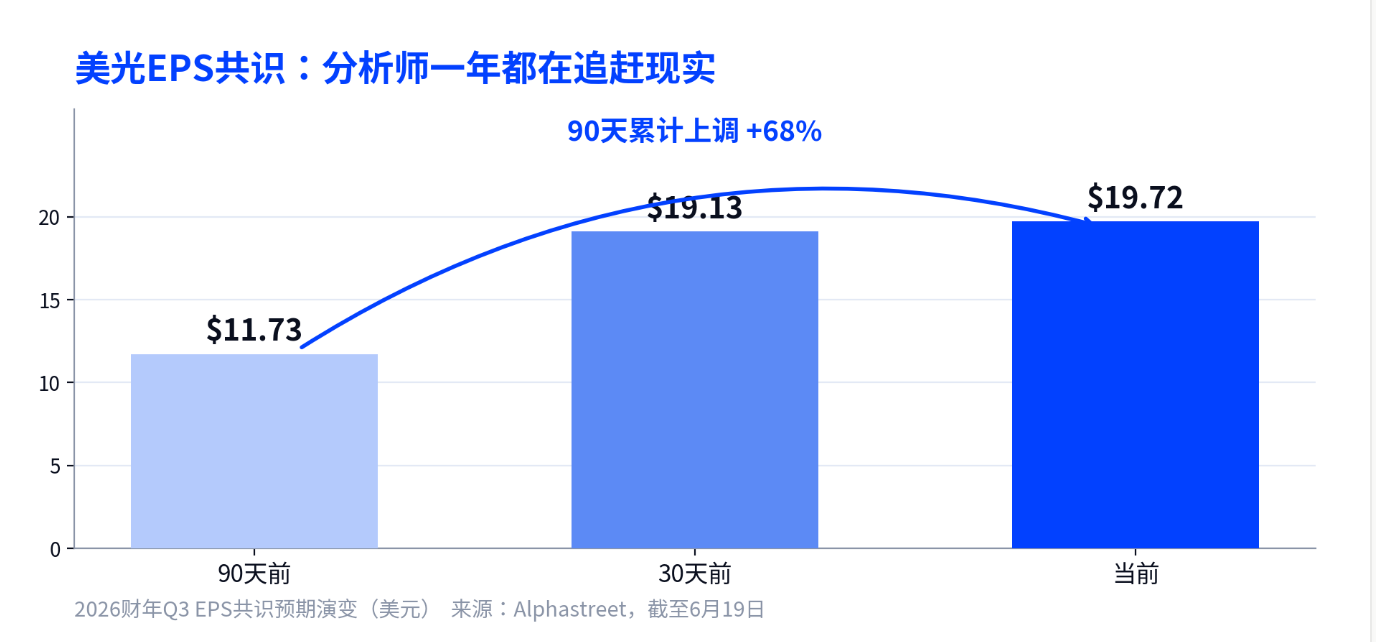

According to Alphastreet data, the consensus for Micron’s earnings per share for this fiscal quarter was $11.73 90 days ago, which rose to $19.13 30 days ago, and is now at $19.72, a cumulative upward adjustment of 68%. Three months ago, Wall Street's judgment of the company was nearly half lower than it is now.

The earnings forecast range given by 31 analysts varies widely from $7.53 to $24.08, and revenue estimates range from $19.7 billion to $40.1 billion, showcasing a large disparity. The steepness of this turning point is not fully understood even by the analysts themselves; they can only adjust upward based on actual data.

For ordinary investors, this sends a double-edged signal.

The repeated raising of expectations indicates that the fundamentals are indeed exceeding expectations; however, even if the performance on the day of the financial report is excellent, as long as it falls short of this raised consensus, the stock price may still drop.

Don’t believe that "Citigroup is too conservative," that is the most aggressive prediction in the room

There is a saying on social media that Citigroup's assumptions about storage prices are too conservative and that Micron's financial report will significantly exceed expectations. This judgment is misguided; making decisions based on it would lead to pitfalls.

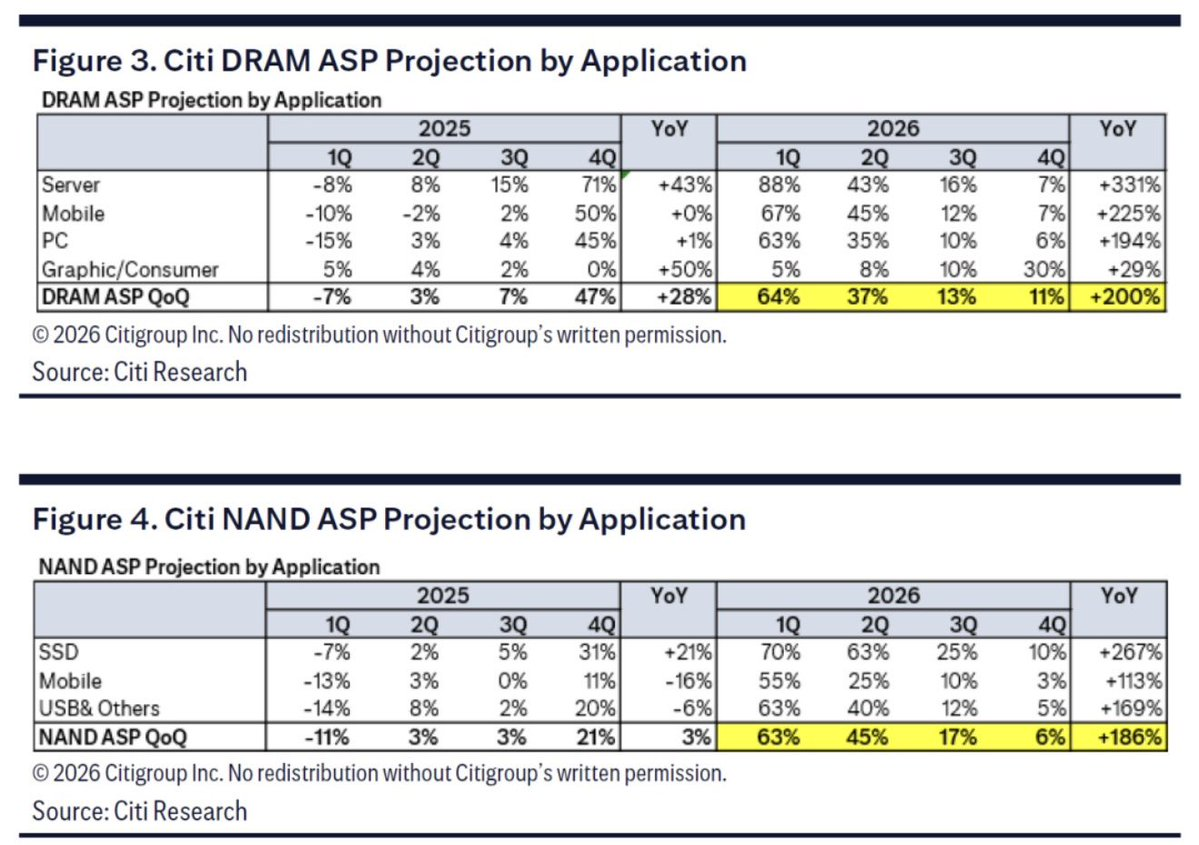

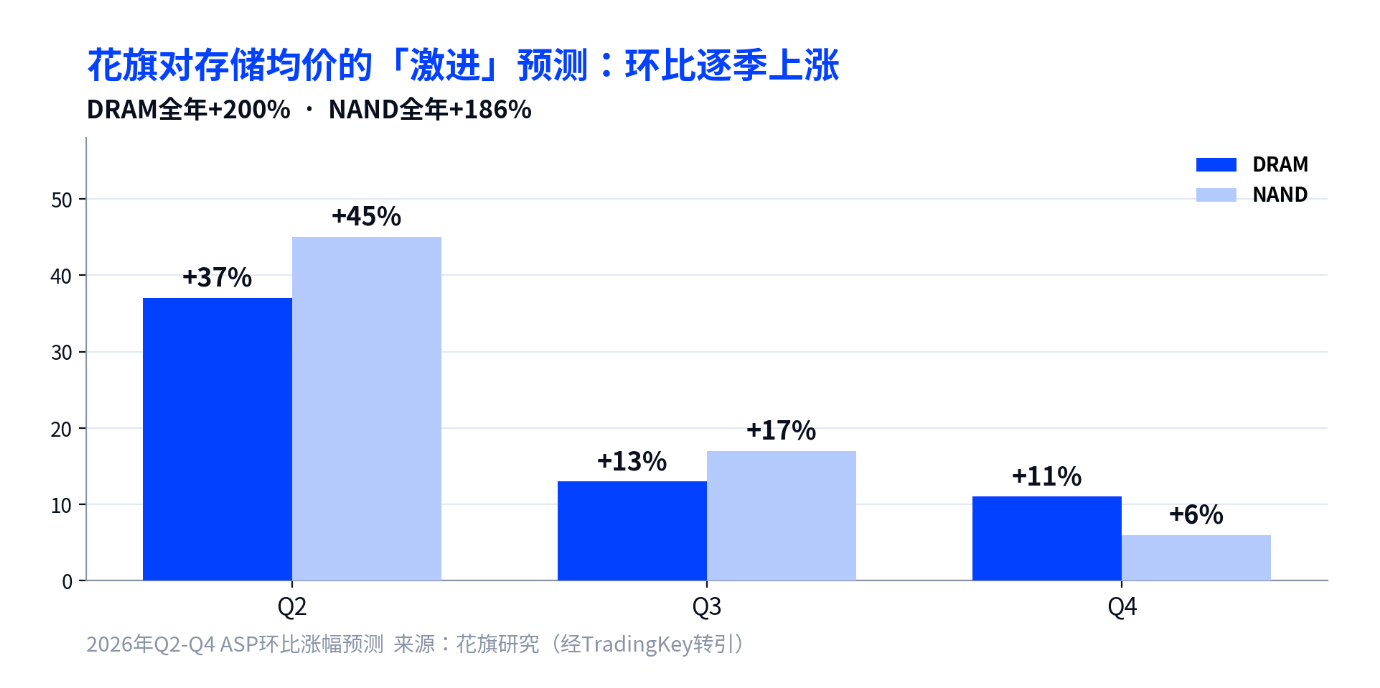

According to TradingKey reports, Citigroup expects the annual average price of DRAM to rise approximately 200% in 2026, with quarter-on-quarter increases of 37%, 13%, and 11% for the second to fourth quarters, respectively; NAND flash memory is expected to increase approximately 186% annually, with quarter-on-quarter increases of 45%, 17%, and 6%. A 200% annual increase is Wall Street's most aggressive forecast for storage prices, not conservative. Based on this, Citigroup raised its target price to $1200, with Deutsche Bank even raising it to $1500, both extending the forecast of storage shortages until 2028.

The risk point lies here: even the most aggressive institutions base their forecasts on a "200% increase," meaning the financial report needs to exceed expectations that have already been repeatedly raised. Relying on the assumption that "Citigroup underestimated" to achieve an outperformance in expectations is logically untenable.

Gross margin around 81%, the highest in history, and the biggest suspense of the day

The most important aspect to watch in the financial report is the gross margin.

According to TradingKey reports, Micron's own guidance is for revenue around $33.5 billion, fluctuating by $750 million, with earnings per share around $19.15 and gross margin around 81%. This is the company's highest gross margin in history, ranking among the top in the semiconductor industry. Last year, the net profit margin was 23.4%, and 58.8% in the previous fiscal quarter, more than doubling profitability in one year—a magnitude rarely seen in semiconductors.

The higher the gross margin, the more pronounced the sustainability issue becomes. Micron has historically been one of the most cyclical tech stocks, with everyone being aware of the boom and bust cycles in storage. On the day of the financial report, if there are signs of profit margins peaking or prices of bulk storage categories starting to ease, the stock price will feel pressure even with strong revenue figures.

According to TIKR reports, Micron's global operations executive vice president Manish Bhatia stated at the JPMorgan conference that the company's financial outlook is stronger than during the last earnings call, with the expectation of setting a new record for free cash flow this fiscal quarter; supply constraints for HBM, DRAM, and NAND will continue beyond 2026, and the ramp-up speed for HBM4's production capacity is twice that of last year's HBM3E. While these statements are optimistic, they represent the tone before the financial report, and their validity will depend on the data on that day.

The direction of the stock price is determined by the guidance, not this quarter's performance

This quarter's revenue and earnings are likely to be impressive, with the market already having expectations.

The direction of the stock price on that day will depend more on Micron’s guidance for the fourth fiscal quarter, such as whether it can continue to grow quarter-on-quarter, which is a watershed moment. Secondly, the volume ramp-up progress for HBM and the capacity allocation for 2027 will determine whether next year's story can still be told.

In the history of the storage industry, the times when investors are most easily ensnared are not when performance is at its worst, but when expectations are at their highest. Micron is currently positioned at peak expectations. If you plan to take action after the financial report, first look at the guidance and HBM, and then examine total revenue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。