Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: In February of this year, U.S. money market funds surged to a historical peak of about $8.25 trillion, and before retiring, Buffett left behind $381.7 billion in cash, with rumors swirling that super-rich individuals were exiting the stock market.

But now in June, the story has reversed: the S&P 500 has set new highs, breaking 7600 points for the first time on June 2, while the size of money market funds has fallen back to $7.87 trillion as of June 10, with money flowing back from cash into the stock market. The wealthiest group of people who bet on safety have now been slapped in the face by the market.

The Story of February: Cash Piling Up to a Historical High in the Hands of the Rich

Let's turn back time to the beginning of this year.

According to a Goldman Sachs survey from October 2025, high-net-worth individuals with over $1 million in investable assets, on average, held about 20% of their net worth in cash and cash equivalents, a relatively high proportion for traditional allocations.

The most iconic example is Buffett.

According to Bloomberg, this former CEO of Berkshire Hathaway, who retired on December 31, 2025, had stacked the company's cash reserves to about $381.7 billion by the end of the third quarter of 2025. This cash even made money—despite market turbulence, Buffett's personal net worth still grew by about $21 billion last year.

He was not the only one reducing positions. According to holdings documents revealed by Reuters, PayPal co-founder Peter Thiel sold about $100 million worth of Nvidia stock through his hedge fund Thiel Macro in the third quarter of 2025. Nvidia rose nearly 35% in 2025, and Thiel exited at a high point, adding fuel to concerns about the “AI bubble.”

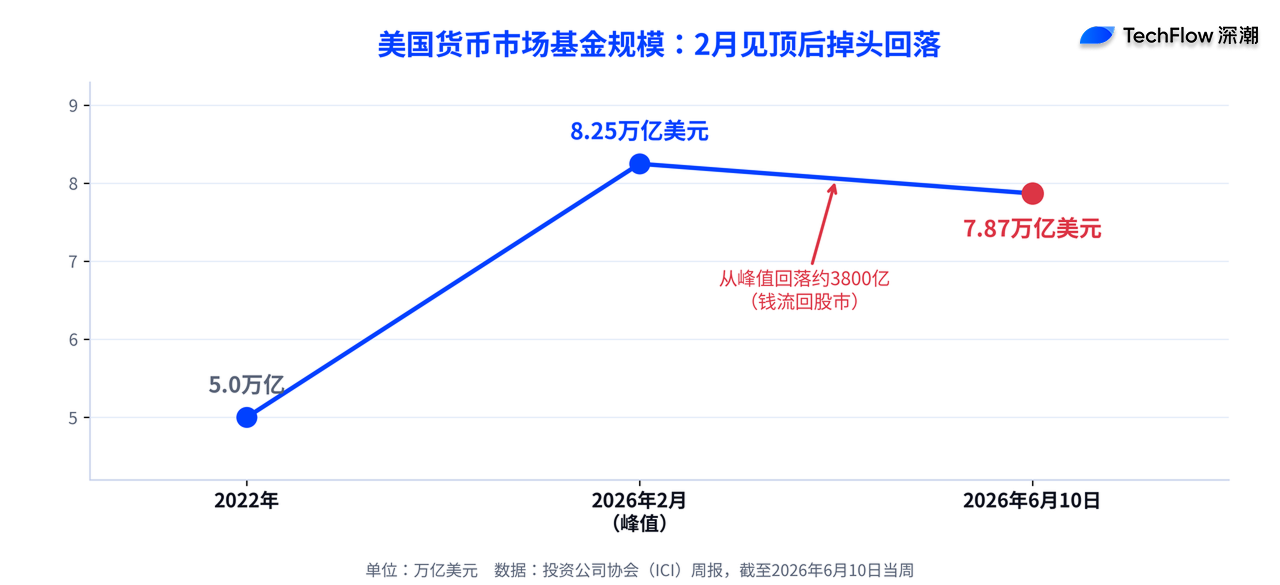

On the market level, the same trend is evident. According to data from the Investment Company Institute (ICI), the size of U.S. money market funds surged to about $8.25 trillion at the end of February, a 65% increase from about $5 trillion in 2022. The narrative at the time was clear: smart money was hiding in cash.

June's Reversal, Money Flowing Back from Cash to the Stock Market

The problem is, it’s now June, and this story has flipped.

According to official ICI data, as of the week ending June 10, the size of money market funds has fallen to $7.87 trillion, with a weekly outflow of $21.48 billion; further back on June 4, it was $7.89 trillion. From February's peak of $8.25 trillion, it has shrunk by about $380 billion. Money is coming out of cash, not going in.

Where is it going? The stock market. According to CNBC, the S&P 500 closed at 7609.78 points on June 2, marking the first time it has crossed 7600 points, rising for the ninth consecutive day; the Nasdaq also set new highs. Nvidia’s release of a new generation of PC chips led to a single-day increase of over 6%, driving Dell and HP up as well. In short, the funds that hid in cash back in February are now watching the market set new highs without them.

There is a signal that has long been pointed out. According to investingLive, Bank of America (BofA) warned as early as the end of May that with the market reaching new highs and bullish sentiment peaking, cash levels were actually declining. The $8.25 trillion record is old news from February; by June, the market situation is completely different.

The Cost of Holding Cash: Underperforming Stocks by More than Double

Why do we say the wealthy's recent attempts at safety have backfired? The return gap makes it clear.

According to calculations from The Motley Fool, if one held cash in money market funds since the beginning of the bear market in early 2022 until now, the total return for the S&P 500 is about 42%, while the Vanguard federal money market fund only had 18% over the same period—a difference of more than double. Hiding in cash may seem stable, but the cost is missing out on a significant market rally.

This is also why many analysts remain cautious about “hoarding cash at the first sign of volatility.”

Historically, events like geopolitical conflicts are often short-term, and may even present buying opportunities at lower levels rather than reasons to liquidate.

The Money Released from the Stock Market has Flowed into Real Estate and Artwork

Those wealthy individuals who indeed reduced their stock holdings did not let the money sit idle. Goldman Sachs' survey shows that nearly 40% of people with investable assets between $1 million and $5 million held alternative investments; among those with assets exceeding $10 million, this ratio reaches up to 80%. The more assets one has, the more they venture beyond traditional stocks.

Artwork is one such destination. According to UBS's 2025 art market report, high-net-worth collectors allocated on average about 20% of their wealth to art in 2025. Real estate, private credit, and hedge funds are also absorbing funds flowing out of the stock market. The logic is that in an environment where inflation is sticky, interest rates are high, and tariff prospects are unclear, these categories resemble safe havens. However, safe havens also come at a cost, as the earlier figures on returns already highlight.

Large Banks are Doubling Down: Goldman Sachs and Morgan Stanley Raising Target Prices

If the wealthy's actions in February were defensive, the posture of Wall Street's big banks in June is quite the opposite.

According to Bloomberg, Goldman Sachs' strategist team, led by Ben Snider, raised its year-end target for the S&P 500 from 7600 to 8000 points at the end of May, citing profit growth driven by AI. Goldman Sachs raised its 2026 EPS forecast for the S&P 500 to $340, corresponding to a year-on-year growth of 24%, and believes that beneficiaries of AI infrastructure will contribute about half of this year's index profit growth. However, Goldman Sachs also cautioned: “AI sentiment and interest rates pose risks in both directions.”

Morgan Stanley is even more bullish. Lisa Shalett, Chief Investment Officer of Wealth Management, set a one-year target of 8300 points for the S&P 500 in her outlook on May 20, suggesting an upside of about 11% to 12%. However, she also outlined five risks: excessive concentration of gains in a few large-cap AI stocks, deterioration of U.S. consumer finances, corporate profits relying on price increases rather than productivity, pressure on long-term interest rates, and better performance outside U.S. stocks (in Japan and some emerging markets). Shalett's core judgment is that the market appears stronger on the surface than the underlying economy.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。