Author: @zuoyeweb3

AI is the opportunity for Nerds, Agents are the opportunity for Money

Venture capital, MegaFunds like A16Z have always told us it’s a story about cycles and exits, but for Solo GPs, it feels more like a harmonic vibration of signals and structures; you need to find the real patterns they haven’t articulated.

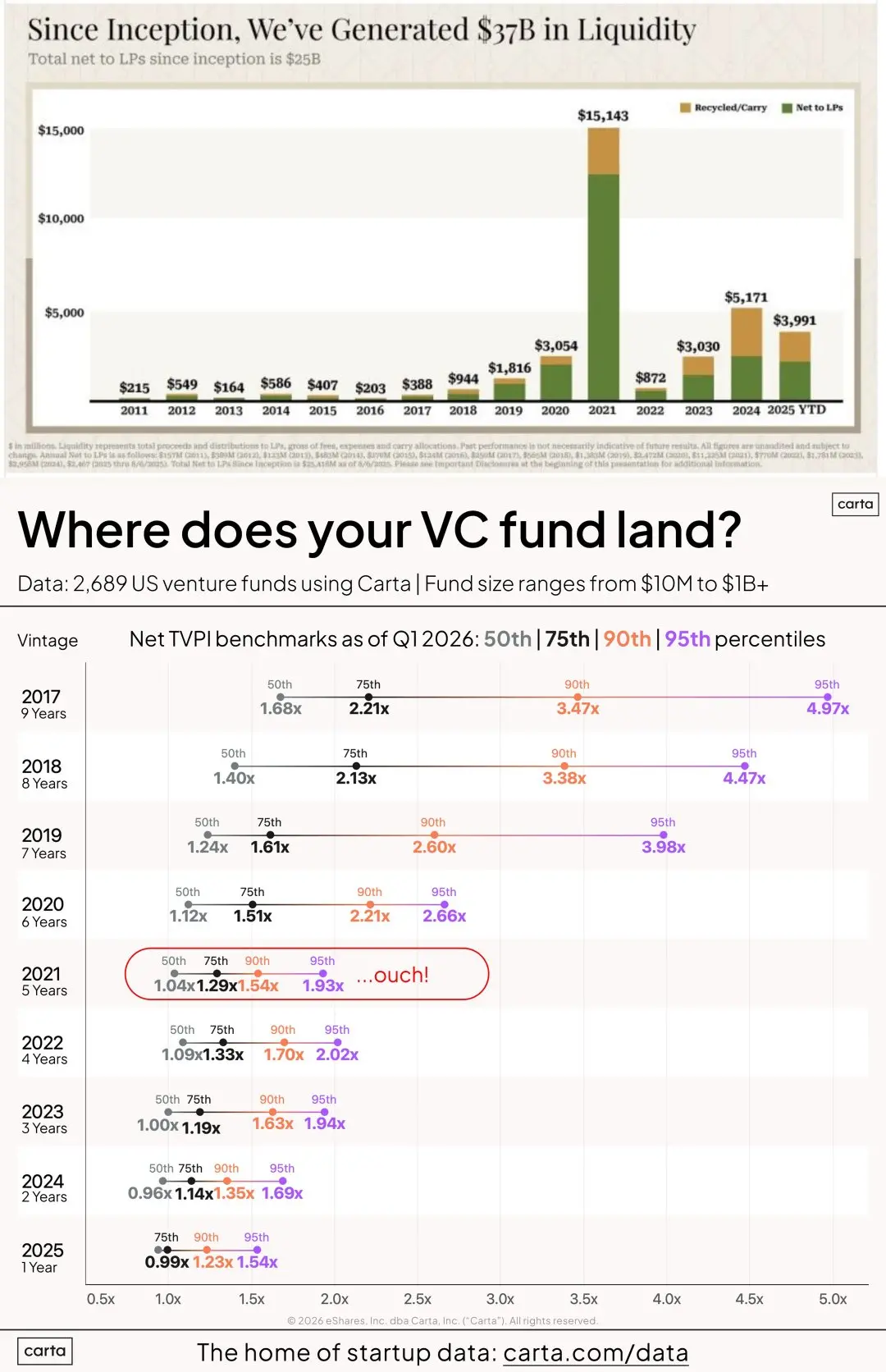

In 2021, a16z returned $12.5B to LPs, with DPI exceeding the total of the previous decade, meanwhile, 2021 also marked the beginning of the catastrophe for the US VC industry; discounting the real DPI, it was just unrealized gains.

In other words, 2021 was a golden period for exits; LPs could receive real money, but if LPs reinvest, they have to go through the ongoing pain.

Image description: Only by releasing capital can there be a true exit

Image source: @jasonlk @PeterJ_Walker

This all tells a contrary narrative, the fluctuations in the crypto market are in sync with this; in 2022, the concept of the Metaverse fed the flames of Web3, even forcing a continuation of the bull market until early 2025, when Binance ended the VC token with the “girlfriend token” farce.

Today, most VCs have fallen into a silence mode, economies of scale dragged into a heavy capital mode of computing power and data, unable to break even for a long time, network effects cannot be discussed on-chain, instead drifting toward institutionalization and surviving through SaaS channel fees.

However, looking at the history of venture capital, each round of interest rate hikes and cuts creates different VC models as liquidity is provided; we will repeatedly invent valuation logic for risks, while the relative freedom of the crypto market allows those with vision to uncover the most profitable signal mechanisms.

When VCs No Longer Take Risks

“Every passion begins with an external thing impacting the senses, causing the animals’ spirits to move through the nerves.

If you recall, in March and April 2021, Roblox and @coinbase chose the Direct Listing mode for their IPO; unlike a conventional IPO, direct listing only sells existing shares, requires no underwriters, and does not have a lockup period.

Interestingly, both were led by A16Z, under the brilliant DPI data, in June 2021, A16Z raised $2.2 billion for their third crypto fund, and in January 2022, A16Z raised an astounding $9 billion for a new fund.

So what is the cost?

The cost is that Coinbase’s stock price fell 90% from its peak in 2023. It’s quite clear that A16Z’s role in the US stock market is no different from crypto VC, but the problem is, A16Z can still raise $7.2 billion in 2024 and $15.1 billion in 2026.

Even in May 2026, their fifth crypto fund raised over $2.2 billion, with their history of crypto fund amounts nearing $10 billion.

The market presents a choice: become LPs of @a16z and wait for the astonishing DPI at the moment of liquidity, or bear the cost of being A16Z's source of astonishing DPI.

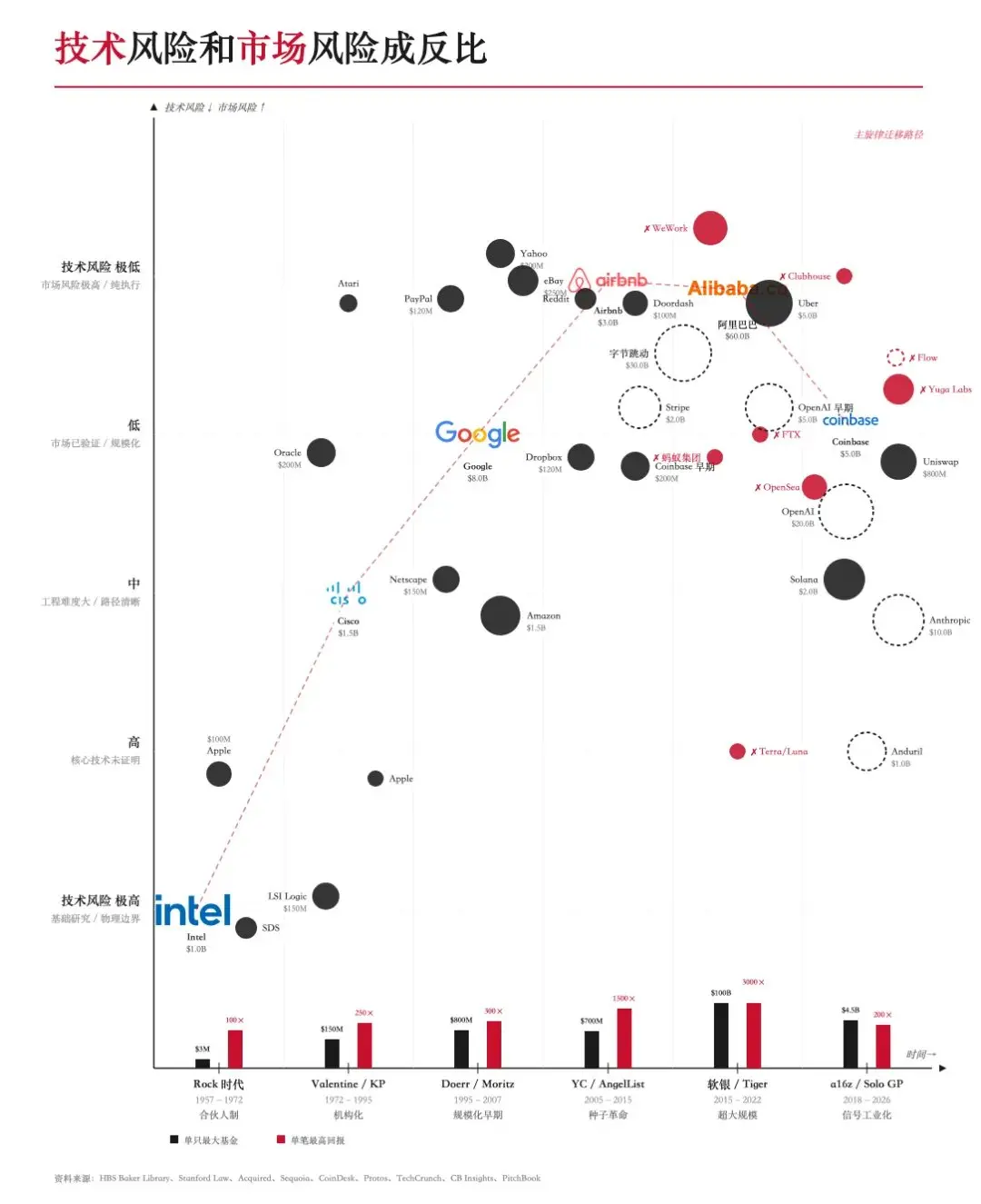

Yet problems arise; A16Z’s sensitivity to market signals is not sharp. In other words, every VC king in cyclical periods faces the curse of scale; too large a scale leads them to lack sufficient motivation to discover extremely early paradigms, especially those that are revolutionary rather than merely improvements.

- The father of modern venture capital, Arthur Rock, reached his peak at the outset, with Fairchild and Intel initiating the venture capital model in Silicon Valley;

- KP and Sequoia formally introduced venture capital institutionalization, but led in the transition between PC and mobile internet;

- YC turned venture capital into a probability mechanism under big numbers, mass-producing sub-gigantic unicorns under power laws;

- Masayoshi Son transformed venture capital into an ultra-large-scale game akin to a Ponzi scheme via Alibaba’s Sino-US myth;

Thus, while the old giants indulge in past glories, emerging aspirants will showcase their unique insights through innovative mechanisms, thereby securing cheap funding and ushering in a new era of adventure.

Image description: The fluctuations of the VC cycle

Image source: @zuoyeweb3

Moreover, reputation itself can be converted back to money; Paradigm founder Matt Huang invested in ByteDance, even though it cannot be publicly listed, Paradigm chose to leap into crypto, and according to the latest news, they have now pivoted to AI and robotics.

Let us adjust the answer; if you cannot become an LP of A16Z and do not wish to bear the cost of being stepped on, then you need to discover the new signals that haven’t been amplified and create new mechanisms to surpass the old predecessors.

Cracks have emerged; in 2021 A16Z was not “permitted” to participate in Anthropic’s financing, but more individual investors jumped in early, such as Skype co-founder Jaan Tallinn and former Google CEO Eric Schmidt leading the A round, with FTX’s SBF entering in 2022, giving us an enduring imagination of another Crypto X AI.

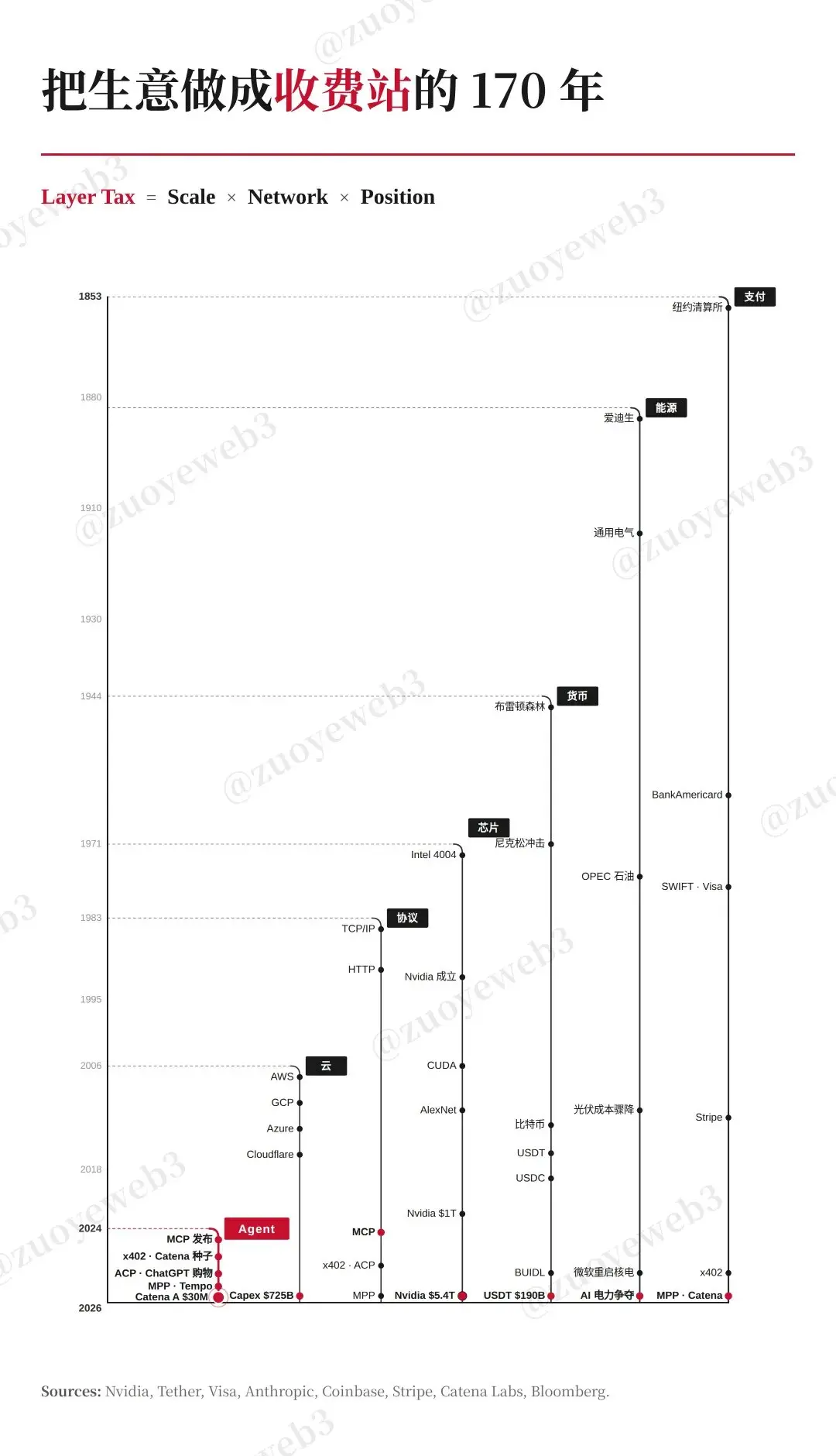

Image description: The positioning race has just begun

Image source: @zuoyeweb3

A16Z does not need to take risks; SBF collects retail money “effectively earning A” while if we need a reasonable starting point for Solo GPs, the entrepreneurial history of Claude is the most typical.

Different from individual angels, Solo GPs operate their entire VC through self-research abilities; the Agent era is easy to understand, but it is precisely humanity that first puts this into practice. Unlike YC’s broad net strategy, Solo GPs still need to deeply invest in each project; every investment is crucial for DPI.

A16Z becomes an indicator of the market itself; as new technological trends emerge, newer participants try to get a slight edge over A16Z. Beyond the large AI models, they are focusing on Agents.

There exists a dangerous leap here, that economies of scale cannot exist within the large AI models. For every additional human user, server costs will rise, and unlike software, costs cannot be diluted; thus, the anticipated network effects have not manifested within Agents, and the invocation between Agents remains an ideal state.

Non-Human Network Effects

“In 1784, Watt improved the rotary steam engine, and in 1824, the complete theory of the steam engine was expounded by the Frenchman Carnot.

Everything in AI is a black box; Scaling Law was observed by Adi Wang at Baidu, the math required for Transformer does not exceed graduate school level, but the reason why it can surpass that level of mathematical understanding is unknown.

AI is the opportunity for Nerds; you just need to fund the forefront of people, then patiently await miracles, and the talent acquisitions popular in Silicon Valley serve as the best proof: Researcher > Data > Model.

However, large models themselves face significant cost recovery challenges; reiterating the contradiction regarding scale effects, even if transitioning from training to inference, or from conversations to tasks, this process cannot be halted.

The sole escape route for large AI models is to become traffic centers like AWS and CloudFlare; if production-side costs cannot be lowered, then consumption-side growth must be infinite.

Agents represent the opportunity for Money; Agents must become the primary subjects of consumption, where subjects x consumption is infinite, which is the root of Agents calling upon each other becoming a mainstream topic.

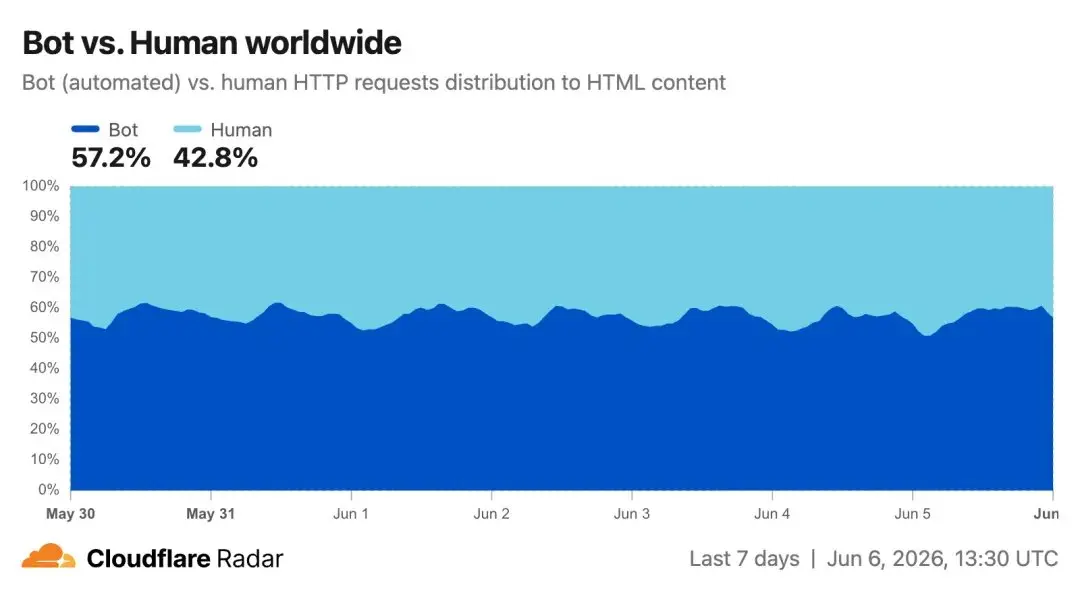

Yet to a considerable extent, differentiating Agents from Bots is challenging; it’s unclear what exactly defines an Agent, seemingly Bots have long existed.

Image description: Bots are not Agents

Image source: @Cloudflare

If we must define Agents, the “evaluative agents” in reinforcement learning is the origin of this technological wave; in DeepMind’s perspective, letting agents automatically evaluate the success of training is key to the next step of intelligence upgrade.

This vastly differs from Claude’s role delineation from Coding; the programming perspective of Agents essentially translates to a human programmer’s role, whereas when we speak of Agentic Coding, it diverges significantly from AlphaZero's Agents.

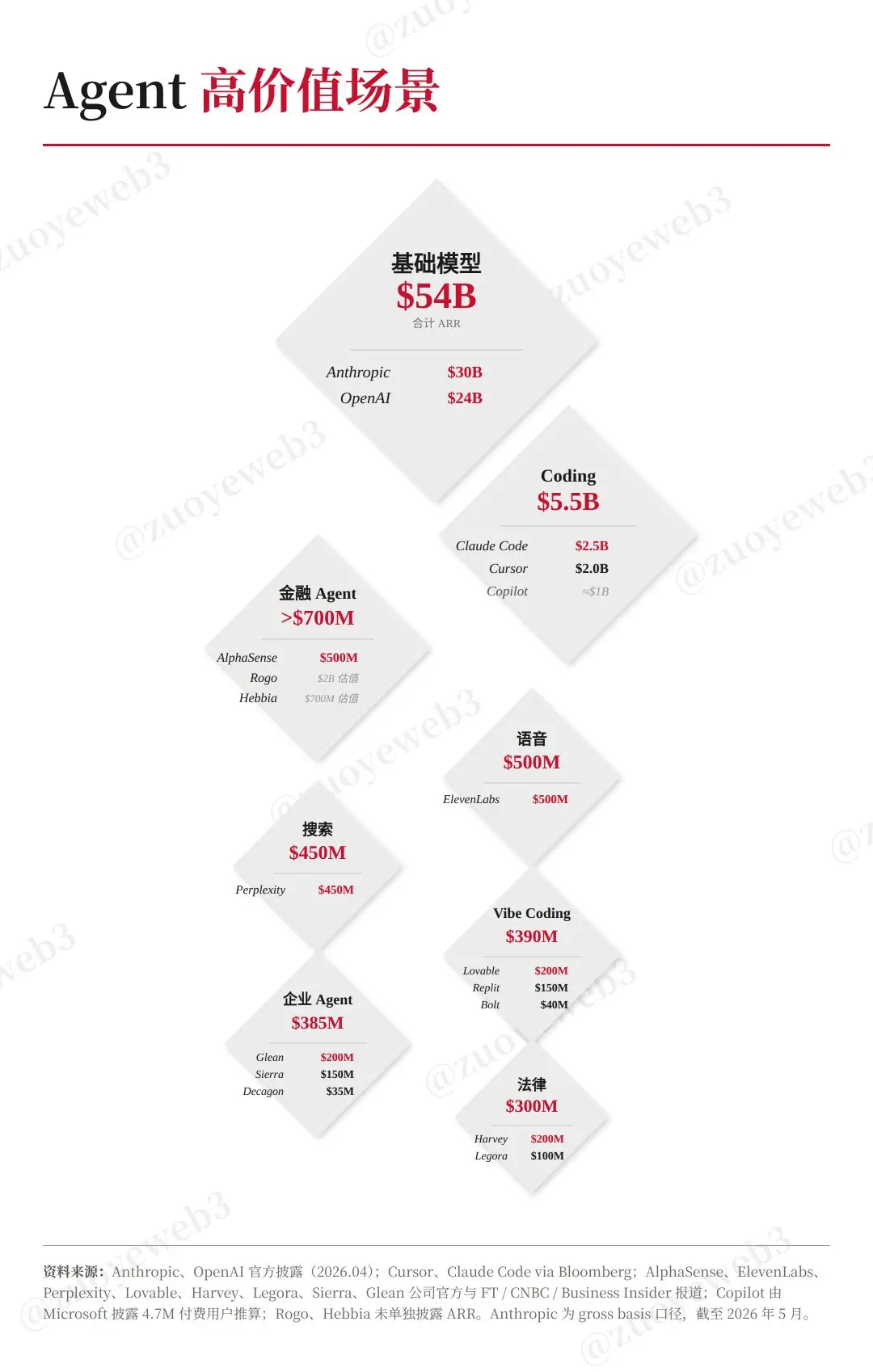

Image description: High-value scenarios for Agents

Image source: @zuoyeweb3

Only from this angle, when Agents take on tasks, Claude's impact on SaaS becomes tenable, merely being a continuation of the human outsourcing mechanism:

- Advancing towards high-value scenarios; after programmers, come accountants and analysts;

- Moving towards fewer full-time employees; after outsourcing comes the cost of invoking multiple Agents.

However, a problem remains; Agents do not exhibit human social relationships; genuine business relationships will not become smoother through Agents; humans still prefer to interact with other humans.

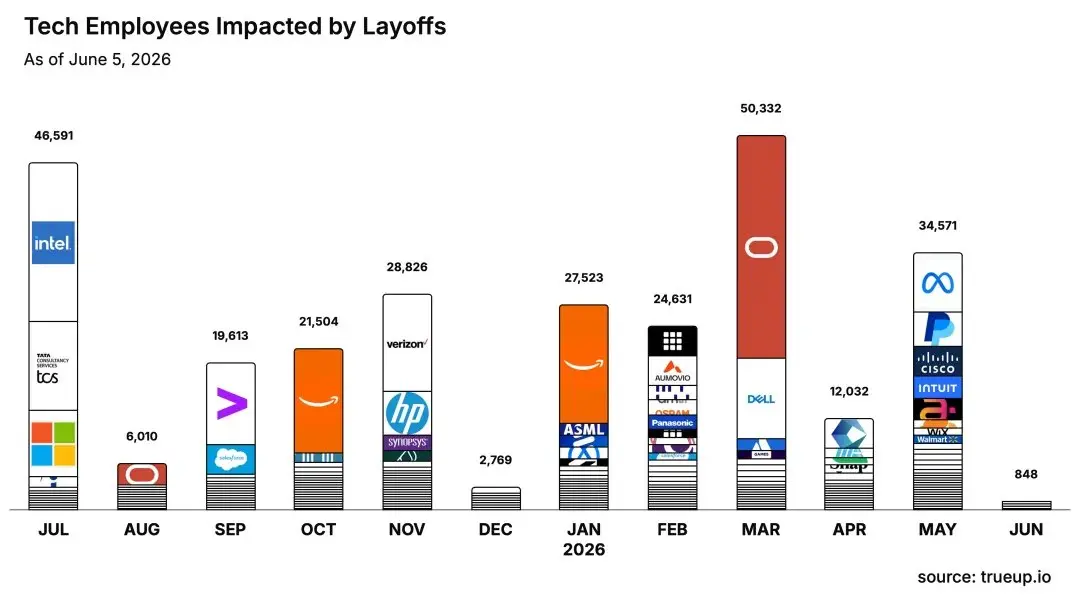

We indeed create more Agent scenarios; internally, they perform well, such as large companies substituting GPUs effectively.

Image description: High-value scenarios do not require humans

Image source: @trueupio

But in “external” cooperation, it must be noted, as yet unproven; in May 2026, the US experienced robust job growth, with non-farm employment increasing by 172,000, primarily in blue-collar fields like leisure and hospitality and healthcare, while the finance sector saw a decrease of 22,000 jobs.

The societal anxiety about Agents is real but significantly overestimated.

Of course, just like whether the Sahara needs shoes, this could also signal a continued enhancement of model intelligence, an increase of Agent capabilities, and an investment in Robotics.

In other words, Agent economics only holds theoretically; the infinite growth on the consumption side has not materialized, continuing to bet, how can we allow Agents to invoke each other and birth network effects?

Crypto Positioning in the Agent Era

“Evolution does not always lead to increased complexity; evolution does not always follow an upward trend.

Let’s summarize our knowns to provide a warning for the dangers ahead.

Venture capital cannot represent effective discovery of technological signals; this has become a game for the brave few;

Agents are forcibly produced in large numbers, aiming to reduce the production costs of large models, yet a natural invocation relationship does not occur in between.

These two seemingly contradictory discourse systems embody a clever coordination - an exploration of the signal mechanisms that stimulate Agent invocation.

Simply issuing Agent assets, or turning DeFi protocols into Agents is meaningless; on-chain, there are already relatively few humans and many Bots, increasing smart contract invocations would only add technical risks; this path is not a smooth one.

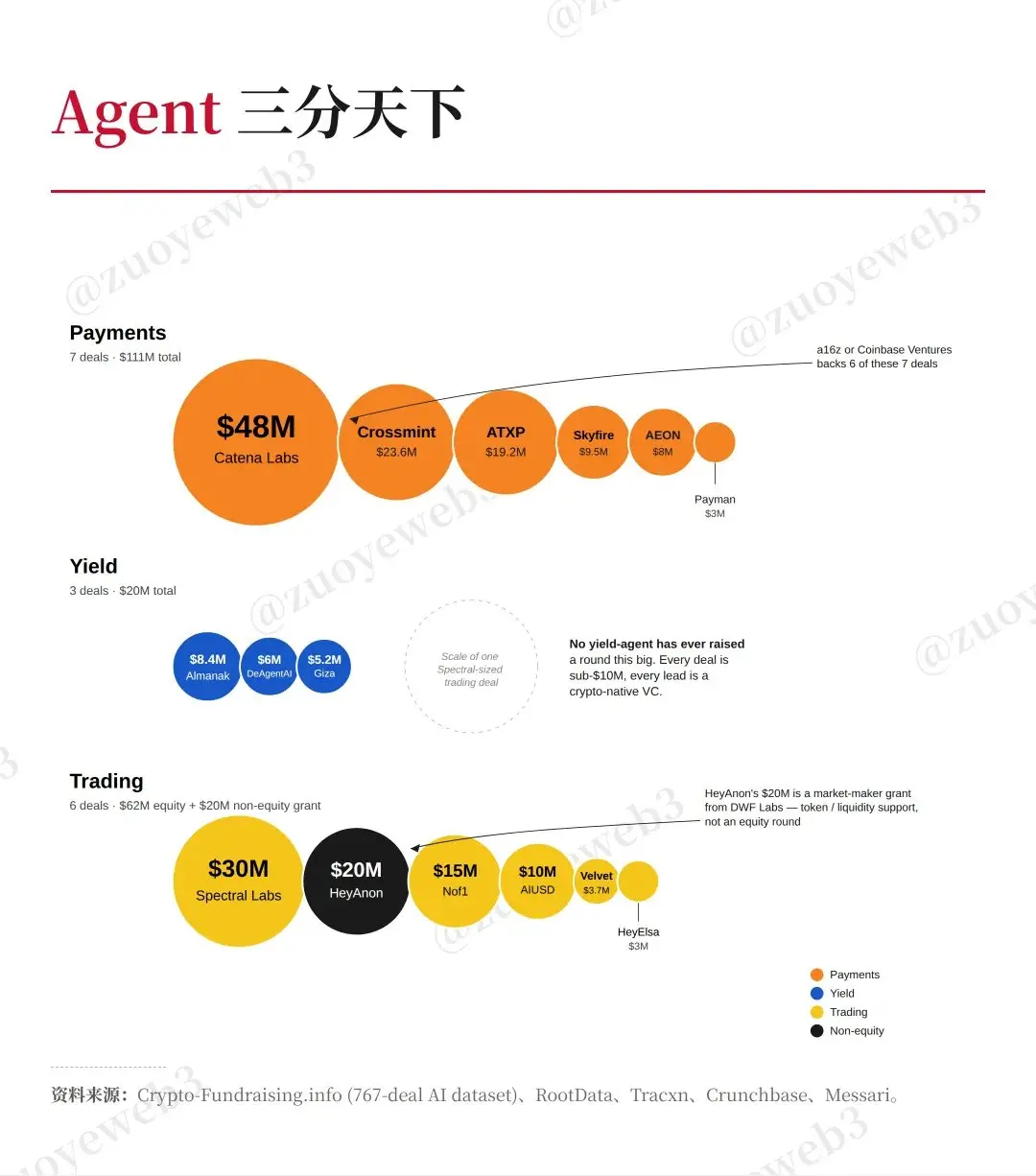

Image description: The positioning race in Agent economics

Image source: @zuoyeweb3

Exa aims at the demand for real-time + high-quality data for Agents, cleaning once and invoking multiple times, this is real scale economics but is difficult to trigger invocations between Claude and Codex.

Catena satisfies the compliance financial needs between B-end Agents and even needs to apply for an OCC license to facilitate B2B compliance; this is a specialized version of network effects but is hard to reduce usage costs.

Meanwhile, payment protocols represented by stablecoins aim to tap into consumer side entry + settlement exit needs, lightweight protocols lower usage costs, and micropayments reduce collaboration costs.

But this is still insufficient; to achieve daily communication among A2A, we must enable humans to willingly contribute their souls, similar to a three-step process like TrueNorth:

- Allow people to use Agents to assist in transactions;

- Let Agents learn from human participation in transactions;

- Enable Agents to lead on-chain transactions.

Relative to Claude’s legal and policy limitations in accessing IBKR, it can only serve as a somewhat CoPilot, while TrueNorth's actual trading with Hyperliquid is not particularly challenging.

However, getting humans to willingly accept guidance from Agents remains a far-off goal, at least further from VCs’ imaginations.

Image description: Payment + transactions > revenue

Image source: @zuoyeweb3

In attempts concerning Agent + finance, “primarily investing in payments, secondarily in transactions” occupies an absolutely mainstream structure.

Payments are very certain; the market shares of PayPal and Stripe will be monetized with stablecoins, and stablecoins will be converted into Agents.

The transaction prospects are vast, from Simmons to Jane Street, and the unpayable debts of Steven Liang evoke infinite imagination from VCs.

Yet all of this does not equate with our imagined Agents taking over transactions and payments.

Quantifying establishes “computational power hegemony,” which remains a speed advantage relative to humans; trading establishes “channel advantages,” still a fee discount relative to banks.

A gap thus arises; VCs must facilitate a condition where humans willingly get replaced by Agents; A16Z is powerless in this regard; throwing money cannot lead to the success of new social platforms like Clubhouse and Towns Protocol, thus they can only lay flat concerning more complex financial Agent scenarios.

If we refer to the successful experiences of DeFi, let Agents touch on funds, low-frequency, small-amount verifications of feasibility, then high-frequency, large-amount daily use can follow.

Imagine if all the roads were filled with FSD Tesla Robotaxis, it would arguably be safer than mixed human/AI driving, but to facilitate this, humans need to serve as test subjects:

- A few individuals use AI-assisted driving, establishing tech equity with human drivers;

- Reducing the casualty rate of those using AI-assisted driving, establishing a compensation mechanism.

In other words, establishing a mechanism where Agents engage with money would convert users more easily than getting Agents to make money; only when Agents gather enough experience with money will it allow humans not to think, but merely click to confirm.

Only when Agents actively participate in the market can market efficiency and safety increase; one can understand this as the process through which Agents seek profit is the process of market efficiency enhancement, progressively bootstrapping, with C++ writing C++, optimizing Agents with Agents.

Trading is the endpoint for Agents, but before that, you must traverse a long elliptical track.

In the high-value scenario of finance, blockchain is the open testing ground for finance, stablecoins are the proof of the process of Agent optimizing the market; this is unrelated to scale and resource investment, but pertains to the establishment and expansion of mechanisms.

Conclusion

“In life, where is there no cycle; without cycles, there is no generational dividend, there is always a new generation surpassing the old one.

VCs are becoming smaller and more personalized; whether Solo GP or OPC, we have yet to observe Solo GP investments in OPC becoming mainstream; amidst the uncertainties of technological waves, we do not know which paradigms will emerge as dominant.

“Software eats the world” came after the internet bubble of the early 2000s, ushering in over 20 years of long-term dividends; now we are entering a new era where “Agents consume software.”

Agents themselves are development tools; they signal the evolution of productivity, but no new software developed by Agents has yet become a universal application; this is also a fact. After the IPOs of @SpaceX, OpenAI, and @AnthropicAI, the positioning of large foundational models has come to an end.

If this is a new round of long-term dividends, then new fundraising crypto VCs like @dragonfly_xyz, ParaFi, Haun, and @paradigm, a16z will continue to scale up, or run specific fund projections like 5cc in the new deployment frenzy.

Even the entire DeFi industry will experience paradigm updates; during the last two Kondratieff cycles, financial system innovations have continuously changed, and this time, Agents will become a new starting point for dual revolutions alongside stablecoins.

Crypto is small, the world is vast; let’s witness together!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。