JPMorgan believes that tonight's data will create a dilemma of "any outcome is wrong."

Written by: Zhang Yaqi

Source: Wall Street Insight

The non-farm payroll data for May, to be released tonight, will plunge the market into a rare "reverse Goldilocks" dilemma: regardless of whether the data is strong or weak, it is difficult to claim a net positive for the stock market. Investors are facing the most entangled directional choices on this historically low implied volatility non-farm night.

The market consensus expects an increase of about 88,000 non-farm jobs in May, slowing from 115,000 in April. However, there are significant divergences among institutions—Goldman Sachs predicts only 60,000 jobs, far below the consensus; Bank of America forecasts 95,000 and sees more pronounced upside risks. ADP data shows that May saw the addition of 122,000 private sector jobs, the strongest since January 2025, but analysts warn that the average deviation between ADP estimates and official Bureau of Labor Statistics (BLS) data can be as high as 83,000, limiting their reference value.

JPMorgan's market intelligence team points out that tonight's data will create a dilemma of "any outcome is wrong": if the data is weak, fears of stagflation will resurface, presenting a clear risk negative signal; if the data is strong, inflation expectations will drive bond yields and volatility upward, which is also detrimental to the stock market. According to JPMorgan's scenario analysis, the range covering potential downward risks accounts for about 60% of the probability distribution. Meanwhile, the money market currently prices the probability of a Federal Reserve rate hike this year at 56%, meaning that strong employment data could lead to more aggressive rate hike expectations, further constraining the stock market space.

The deeper background of this dilemma lies in the fact that the Fed's current policy balance clearly leans toward inflation, with increased tolerance for employment compared to previous periods; since the outbreak of the Iran war, the correlation between the dollar and employment data has significantly weakened, following oil price fluctuations more closely. Currently, the implied volatility of S&P 500 straddles is about 47 basis points, the lowest level since December 2024, indicating that the market's overall pricing for volatility tonight is relatively restrained.

Institution Predictions Diverge to Recent Extremes, Goldman Sachs and Bank of America Disagree

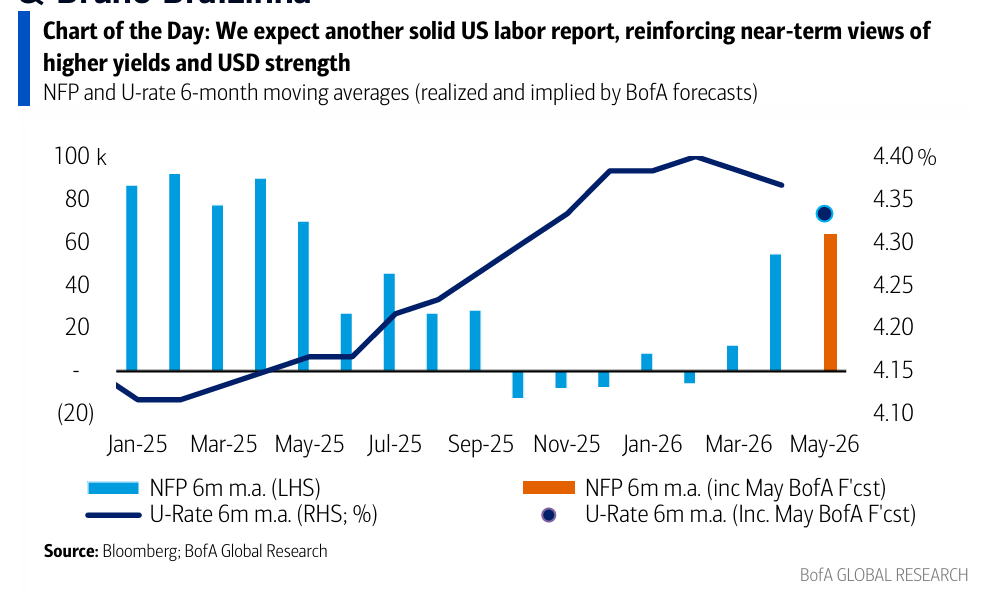

The market consensus expects the addition of 88,000 non-farm jobs in May, slightly above the average of 48,000 over the past three months and the twelve-month average of 21,000 jobs, with the unemployment rate expected to remain unchanged at 4.3% and average hourly wage growth year-on-year expected to slow from 3.6% to 3.4%.

Goldman Sachs economists Ronnie Walker and Jessica Rindels set their forecast at 60,000 jobs in their report, below the market consensus of 85,000, but slightly higher than the three-month average. The negative factors listed by Goldman Sachs include: their tracked big data alternative employment indicator shows an average addition of 69,000 jobs in May, down from 90,000 in April; the ongoing federal government hiring freeze is expected to lead to a net decrease of 5,000 jobs in government sectors (with federal jobs decreasing by 10,000 and state and local jobs increasing by 5,000); additionally, striking workers will drag down overall job additions by about 2,600. On the positive side, the average number of initial unemployment claims during the survey week stood at 203,000, a relatively low level over the past two years.

Bank of America economist Shruti Mishra, on the other hand, takes a more optimistic stance, predicting an increase of 95,000 jobs, above consensus, with upside risks including persistently low unemployment claims, better-than-expected ADP data, and additional support from hiring activities ahead of the World Cup. The bank points out that if the prediction is accurate, the average monthly employment increase in the private sector over the first five months of this year would reach 89,000, the strongest pace for five months since 2024.

The prediction market Polymarket data shows the most likely result range is 100,000 to 150,000 jobs, with a probability of 43%; followed by 50,000 to 100,000 jobs, with a probability of 38%.

Bullish and bearish signals contradict; unemployment claims and PMI surveys hold opposing views

The core basis for supporting a strong report centers on low layoff data. In the employment survey week of May, the average number of initial unemployment claims stood at 210,000, roughly flat compared to 215,000 in April, and well below historical alert levels; the layoff rate in April's JOLTS slightly decreased to 1.1%, remaining at a historically low level.

However, corporate survey data is sending clear warning signals. The ISM Manufacturing PMI employment sub-index, despite a month-on-month increase of 2.2 percentage points to 48.6, remains in the contraction zone, with survey results indicating that about half of the participating companies still consider controlling staff numbers as the norm; the ISM Services PMI employment sub-index has been in the contraction zone for the third consecutive month, dropping further to 47.9 in May, with surveyed companies frequently mentioning hiring freezes or not filling vacant positions. The Fed's latest Beige Book also shows that employment across its 11 districts has seen almost no change, with an overall "double low" scenario of low hiring and low layoffs, as employees become increasingly unwilling to switch jobs due to economic uncertainty.

It is worth noting that Pantheon Macroeconomics insists on maintaining a low forecast of 50,000 jobs, anticipating an increase in the unemployment rate to 4.4%. This judgment is based on corporate surveys performing better than big data indicators: the institution points out that over the past four years, the differences in the Conference Board employment availability index, the NFIB hiring intentions index, and the regional Fed employment intentions indices have been more reliable in predicting non-farm jobs, and all three indicators have shown significant downward signals, especially as the NFIB hiring intentions index has sharply fallen from its January peak to mid-2025 low levels.

Unemployment Rate Uncertainty: Will It Stay at 4.3% or Quietly Rise to 4.4%?

The direction of the unemployment rate also holds considerable uncertainty. The unrevised unemployment rate for April was 4.337%, just a step away from rounding up to 4.4%. The Chicago Fed's leading labor market indicators forecast a May unemployment rate of 4.32%, but simultaneously points out the probabilities of rounding up to 4.4%, maintaining 4.3%, and falling to 4.2% are 42%, 28%, and 30%, respectively.

JPMorgan believes that the overall risk of the unemployment rate leans downward, more likely to touch 4.2%. Reasons supporting this judgment include: the four-week average of ongoing unemployment claims is currently comparable to mid-2023 levels, during which the unemployment rate was still at a high range of 3%; additionally, the Conference Board employment market difference fell from 7.5% in April to 6.9% in May but remains close to historical low levels, while the NFIB hiring plans indicator is also at a cyclical low, both suggesting a cooling labor market. JPMorgan also predicts that the labor force participation rate will slightly drop from 61.8% to 61.7%.

Additionally, it should be noted that the May unemployment rate is influenced by positive seasonal residual factors—historically, the unemployment rate has had an average upward deviation of about 0.12 percentage points in May over the past three years, making the threshold for rounding the unemployment rate to 4.4% not high.

The Fed's Balance Tilts Toward Inflation, Strong Employment Becomes a Rate Hike Concern

The latest FOMC meeting minutes indicate that most members believe recent data suggest that the labor market has stabilized and anticipate that recent conditions will remain stable; some members argue that sluggish employment growth may merely reflect a slowdown in labor supply rather than market weakness, but a minority view it as a potential weakness signal. Overall, most members judge that employment risks lean downward.

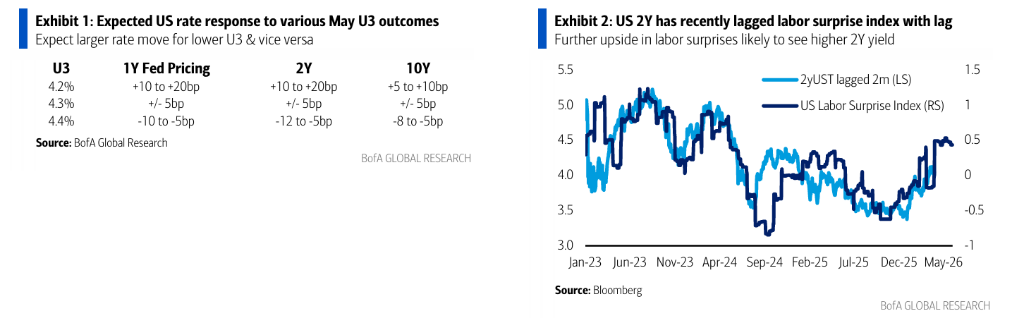

Nonetheless, against the backdrop of a stable labor market, officials' focus has clearly shifted towards price pressures. Some officials warn that persistently high energy prices and tariffs could trigger broader inflationary pressures, thereby shaking long-term inflation expectations and exacerbating the policy tradeoff between employment and inflation, leading to a conflict in the dual mandate. Currently, the money market prices the probability of a rate hike this year at 56%, with a probability of maintaining rates in the 3.50% to 3.75% range at 42%, and a rate cut probability of only 2%.

Bank of America rate strategist Mark Cabana points out that since last month's non-farm data release, market pricing for a Fed rate hike within a year has jumped from 5 to 6 basis points to about 35 basis points. The bank believes that if the unemployment rate drops to around 4.0%, even a largely dovish FOMC may be forced to take rate hike actions; and a strong employment report could push the dual mandate to move in the same direction, creating upward risk for U.S. Treasury yields.

Scenario Analysis: Stock Market Sweet Spot is Narrow, "Just Right" Probability is About 40%

According to analysis by Andrew Tyler, head of JPMorgan's market intelligence team, the overall importance of tonight's non-farm data to the market has somewhat diminished due to the additional uncertainty surrounding the Middle East situation, but this does not mean its impact can be ignored.

Based on JPMorgan's scenario analysis, the responses of the S&P 500 Index to different employment data ranges are as follows:

- More than 130,000 jobs added, the index is expected to range between a decline of 1% and an increase of 0.5%, with a probability of only 5%;

- In the range of 100,000 to 130,000 jobs, the index is expected to range between a decline of 0.25% and an increase of 0.75%, with a probability of 25%;

- In the "relatively comfortable range" of 70,000 to 100,000 jobs, the index is likely to rise by 0.5% to 1%, with a maximum probability of 40%;

- In the range of 40,000 to 70,000 jobs, the index is expected to decline by 0.75% to flat, with a probability of 25%;

- If below 40,000 jobs, the index could decline by 1% to 1.5%, with a probability of 5%;

- Overall, scenarios that could trigger different degrees of declines in the stock market comprise approximately 60% of the probability distribution.

Meanwhile, tonight's SPX straddle options are priced at about 47 basis points, the lowest since December 2024, reflecting the market's overall conservative pricing for the volatility of this "entangled non-farm night."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。