Death spiral or sustainable capital engine? MSTR-STRC structure undergoes a six-month life and death test.

Written by: @100y_eth (Four Pillars)

Translated by: AididiaoJP, Foresight News

MicroStrategy (MSTR) recently sold 32 bitcoins (worth only 2.5 million dollars), which triggered a loss of over 100 billion dollars in bitcoin market value. STRC (its perpetual preferred stock) dropped from a reference price of 100 dollars to 94 dollars, and MSTR's stock price also fell from 150 dollars to 123 dollars.

MSTR, BTC, and STRC are deeply interconnected. In a bullish market, this structure acts as a powerful capital engine, allowing Strategy (MicroStrategy) to aggressively increase its holdings of bitcoin; but once the market deteriorates, as seen recently, the three will form a vicious feedback loop.

This recalls the LUNA-UST situation from back in the day. So, is the MSTR-STRC structure truly sustainable?

Key Points

UST and STRC superficially appear similar: both anchor their prices to specific reference values, offer high returns to holders, and carry the risk of a death spiral. However, there are fundamental differences between the two in price stabilization mechanisms, legal recourse, interest/dividend payment methods, and internal operational structures.

For Strategy to maintain sustainability, it must secure continued financing. This requires support from both market confidence and its own credit. In the worst-case scenario, even if it cannot continue financing, it would not face a direct "death spiral" like LUNA-UST.

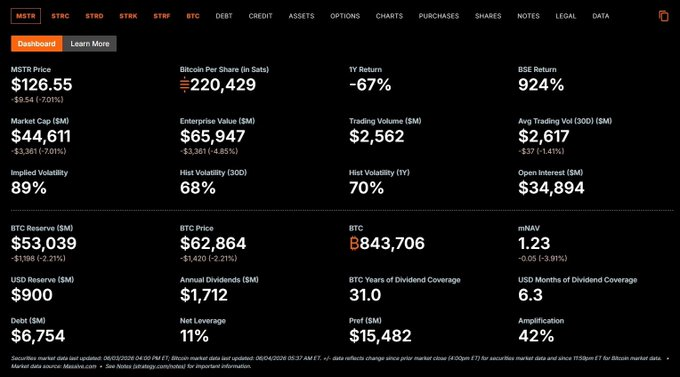

Strategy currently has a net leverage ratio of about 11%, with a magnification factor of around 42%. Even if MSTR and STRC enter a negative feedback loop, as long as the price of bitcoin remains above approximately 26,000 dollars, preferred shareholders still have a good chance of preserving their capital; and if bitcoin does not drop below around 8,000 dollars, the probability of bankruptcy due to debt is very low.

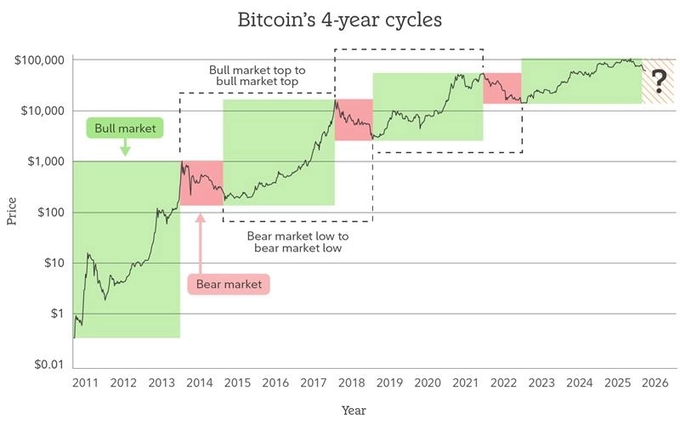

The next six months will be crucial. According to the four-year cycle theory of bitcoin, a bottom is expected in the second half of this year, while Strategy's dollar reserves will only last about six months. The core issue is: Can Strategy restart its capital engine through healthy deleveraging within these six months?

LUNA-UST Quick Review

The collapse of LUNA-UST occurred four years ago. Here’s a brief recap of its operational mechanism.

Price Stabilization Mechanism

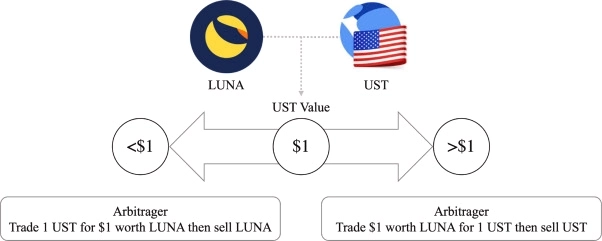

UST is an algorithmic stablecoin, without collateral, maintaining a 1 dollar peg through algorithms. The core rule is: 1 UST can always be exchanged for 1 dollar's worth of LUNA.

- When UST is 1 dollar: Users can burn UST worth less than 1 dollar to exchange for LUNA worth 1 dollar, and the arbitrage opportunity pushes the UST price back up while reducing the UST supply.

- When UST > 1 dollar: Users provide LUNA worth 1 dollar to exchange for a higher value of UST, and the arbitrage drives the UST price back down while increasing the UST supply.

Vicious Cycle Scenario

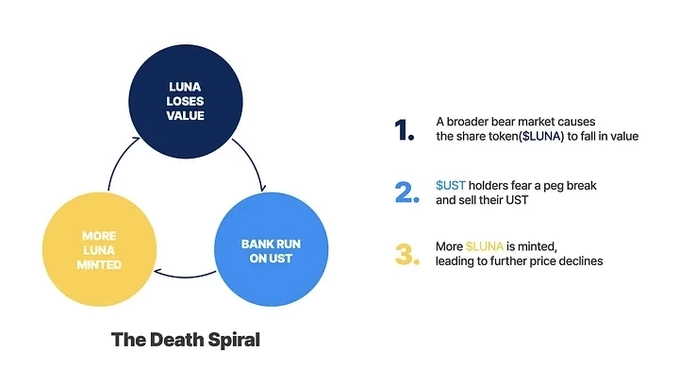

The more UST issued, the less LUNA supply there should be, which should drive up the price of LUNA. Terraform Labs indeed amplified this effect through aggressive expansion of UST usage scenarios.

However, once confidence collapses, the same mechanism can reverse into a death spiral:

LUNA price drops → UST confidence collapses → UST price drops → Massive issuance of LUNA → Further drop in LUNA price…

Collapse of LUNA-UST

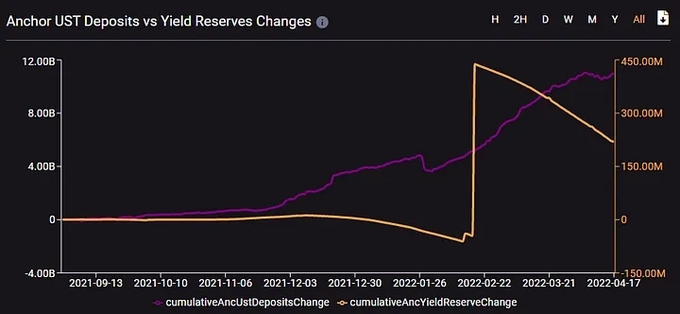

The immediate trigger for the collapse was the collapse of confidence. At that time, Terraform Labs was migrating UST liquidity from Curve's 3pool to 4pool, causing liquidity in the 3pool to thin. An attacker sold 85 million dollars of UST, breaking the peg and triggering panic.

A large amount of UST was withdrawn from the Anchor Protocol (which at the time offered about a 20% annual return), and the selling pressure flooded the market. Before the collapse, 71% of UST was in Anchor. Once the unsustainability of the 20% return was revealed, even an injection of 450 million dollars from the Luna Foundation Guard could not turn things around.

Ultimately, the supply of LUNA surged from around 350 million coins to 65 trillion coins (a 17,000-fold increase), with the price approaching zero.

MSTR-STRC Structure Analysis

The core goal of Strategy is to increase BPS (bitcoin per share). To achieve this, it finances through various financial engineering tools such as convertible bonds, perpetual preferred stock, and common stock ATM issuances, then uses the raised funds to buy more bitcoin.

Financing Methods

- Common stock ATM issuance: Issuing small amounts of MSTR Class A common stock and selling it on the market will cause ADSO (assuming fully diluted equity) dilution, but when mNAV > 1.22, it can actually enhance BPS.

- Convertible bonds: Low-interest borrowing, including equity conversion options, but there is pressure to repay principal.

- Perpetual preferred stock: Dividend and liquidation priority over common stock, but below creditors, with no principal repayment pressure, but a dividend burden close to 10%. There are currently several series, including STRF, STRC, STRE, STRK, STRD, among which only STRK is convertible preferred stock, the rest are non-convertible. Non-convertible preferred stock does not dilute ADSO, making it the financing method of choice for Strategy.

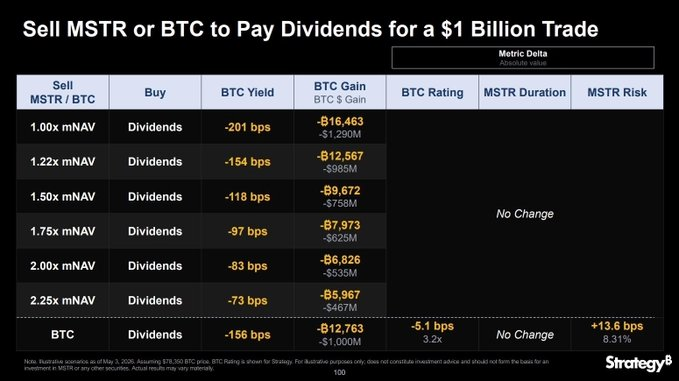

Strategy currently pays approximately 1.71 billion dollars in interest and dividends annually, primarily funded by dollar reserves, which are mostly supplemented through common stock ATM issuance. Recently, they also sold 32 bitcoins to pay dividends, attracting market attention.

STRC Price Stabilization Mechanism

STRC is designed with a reference price of 100 dollars.

- When STRC > 100 dollars: Strategy can lower the dividend rate to bring down the price, and can also issue more STRC to increase supply, while having the right to redeem at 101 dollars per share, effectively capping the upside potential of STRC.

- When STRC < 100 dollars: Strategy can raise the dividend rate to push the price up, while STRC has a liquidation priority of 100 dollars per share, providing price support.

The current annual dividend yield for STRC is 11.50% (based on a 100 dollar reference price).

Vicious Cycle Scenario

MSTR and STRC influence each other, forming a self-reinforcing feedback loop. When the market deteriorates, it may enter a vicious cycle:

MSTR price drops → mNAV declines → Difficulty in common stock ATM financing increases → Selling pressure on BTC rises → STRC confidence decreases → STRC price drops → MSTR price further declines…

But the key difference is: Strategy does not need to pay STRC dividends in cash every month. Cash payments require a board declaration and sufficient funds; otherwise, dividends can be accrued. In theory, Strategy can also lower the dividend rate to SOFR (the overnight lending rate for US Treasury collateral). In extreme cases, it can gradually reduce the dividend rate and defer payments until conditions improve.

LUNA-UST vs MSTR-STRC: Essential Differences

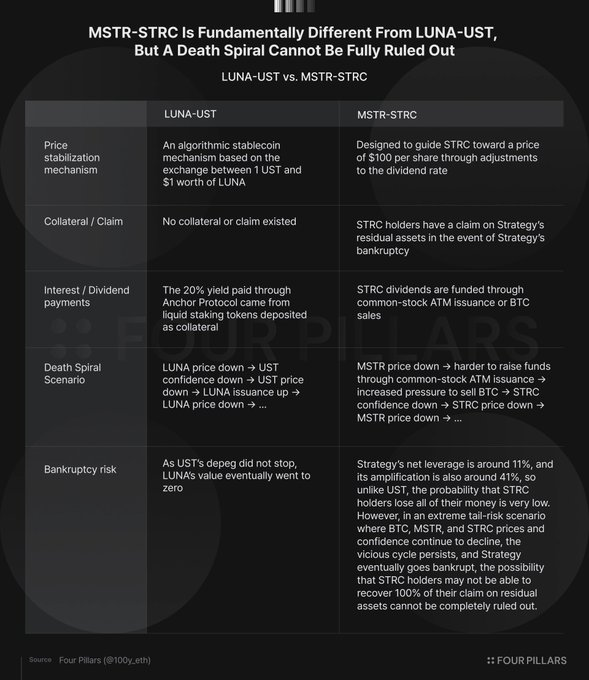

UST and STRC have three major similarities on the surface: price pegged to specific levels, holders can earn high returns, and both carry the risk of a death spiral. However, their internal operational mechanisms are completely different.

Price Stabilization Mechanism

UST achieves stability by adjusting LUNA supply; STRC relies on adjusting its own dividend rate. The pegging mechanism of UST directly affects LUNA's price and supply, while the STRC mechanism does not directly impact MSTR's price and supply.

However, as STRC dividends are mostly financed through MSTR ATM issuance, if MSTR's value decreases and causes mNAV to fall below 1.22, the ability of Strategy to maintain dividends will be questioned.

Collateral / Recourse

UST has no collateral at all, and its price can plummet to zero; STRC, although also without collateral as preferred stock, grants STRC holders a priority claim to remaining assets (with a liquidation priority of 100 dollars per share) in the event of company bankruptcy.

Interest / Dividend Sources

UST itself does not generate interest, with a 20% return coming from borrowing interest and staking income from the Anchor Protocol (natural market demand).

STRC dividends mainly rely on financing from common stock ATM issuances, and in extreme cases may also involve selling BTC. From a BPS perspective, issuing through the ATM is beneficial when mNAV > 1.22 but selling BTC is preferable when below 1.22. Overall, the "naturalness" of STRC's dividend sources is weaker than that of Anchor's borrowing + staking income.

Differences in Death Spiral

The death spiral of LUNA-UST is direct and automatic: UST drops → LUNA issuance increases → LUNA further drops.

The death spiral of MSTR-STRC is more complex and has two major brake mechanisms: Firstly, the direct linkage is weaker; MSTR will not automatically issue more to pay STRC dividends like a protocol; secondly, there is legal recourse; even in bankruptcy, STRC holders still retain rights to remaining assets, providing support for price declines.

The common catalyst for both is still "confidence." As long as investors maintain confidence in MSTR (or the original LUNA), the structure can function; once confidence collapses, real problems arise. Selling 32 BTC by MSTR may not seem significant rationally, but it could be the trigger for a collapse of confidence from an emotional standpoint.

Is MSTR-STRC Sustainable?

Continuous Financing Ability is Key

Strategy currently has 900 million dollars in dollar reserves, with an annual interest + dividend burden of 1.712 billion dollars. Without additional financing, relying solely on reserves can support about 6.3 months.

If reserves are depleted, financing can continue through issuing stocks/preferred stocks, or selling BTC (theoretically supporting up to 31 years). However, selling only 32 BTC recently has caused a sharp market reaction, and the side effects of selling BTC are much greater than anticipated.

Financing conditions are clear:

- MSTR ATM issuance requires mNAV > 1.22; otherwise, it actually lowers BPS.

- STRC issuance requires price to maintain around 99-100 dollars; otherwise, financing costs are too high.

Both are highly dependent on market confidence: investors need to believe that BTC will appreciate in the long term and that Strategy can create value beyond mere hoarding. In the current market environment, obtaining financing through stocks/preferred stocks in the short term is quite difficult. Strategy can only rely on existing dollar reserves, waiting for market and confidence recovery.

What Happens if Bankruptcy Occurs?

Strategy has a net leverage ratio of only 11% (debt - dollar reserves) / bitcoin reserves. Including preferred stocks, the magnification factor is about 42%.

As long as the price of bitcoin does not drop below about 26,300 dollars (the price corresponding to the total value of debt + preferred stock), preferred shareholders can preserve their capital through the recourse to remaining assets. This is the biggest difference from LUNA-UST.

Pressure from Convertible Bonds Maturity

Strategy has no obligation to repay perpetual preferred stock principal, but it must repay the principal on convertible bonds upon maturity (current total debt of 6.714 billion dollars). Maturities begin in 2028, and the current dollar reserves are only 900 million dollars; if it cannot finance, it may have to sell BTC to repay debt. However, the low net leverage ratio means the probability of bankruptcy due to debt is extremely low.

The Next Six Months Are the Critical Line

If the four-year cycle theory of bitcoin still holds, a bottom is expected in the second half of this year, while Strategy’s dollar reserves will just last about six months.

Within these six months, whether Strategy can restart its capital engine through healthy deleveraging will determine its future fate.

Although the title and accompanying images may seem sensational, MSTR-STRC is fundamentally different from LUNA-UST, and the probability of a similar catastrophic collapse is very low.

The real question is: Can Strategy endure the difficulties in the next six months, deleverage healthily, and restart its capital engine, or will it only become an interesting experiment in bitcoin history?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。