Author: Deep Tide TechFlow

On June 1, the largest publicly traded Bitcoin holder, Strategy, submitted an 8-K filing to the U.S. Securities and Exchange Commission (SEC), disclosing that from May 26 to May 31, it sold 32 Bitcoins at an average price of approximately $77,135, realizing about $2.5 million. The document clearly states that the proceeds "are expected to be used to pay preferred stock dividends." This marks the first selling action by Strategy since December 2022, and analysts classify it as the company’s first separately disclosed net reduction in its history; the previous sale in 2022 involved selling 704 Bitcoins while net buying 2,395, leading to an overall net increase, which differs in nature from this instance.

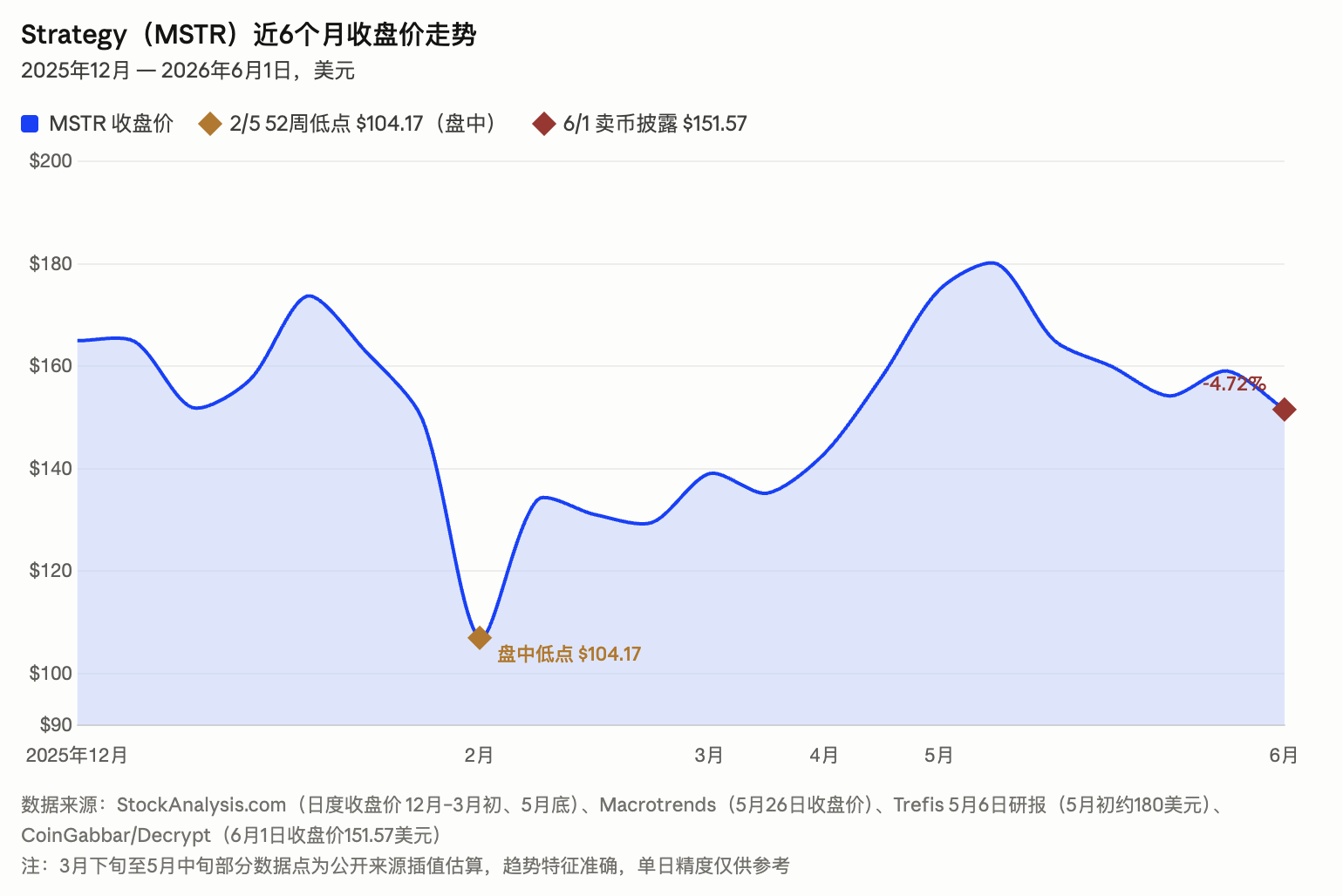

Executive Chairman Michael Saylor's only public response on the day was a tweet unrelated to the selling of coins: "Our goal is to make $STRC the best credit tool in the world." Market reaction was far more tense than this statement. MSTR's stock price fell 4.72% to $151.57, hitting a new low for 45 days and almost wiping out the cumulative gains for the year. The price of Bitcoin dropped below $72,000, decreasing by about 2.77% in a single day. Over $90 million in liquidations occurred in BTC futures within 24 hours, and the total scope of liquidations in the broader cryptocurrency futures exceeded $600 million.

32 Bitcoins sold above cost, with an additional 800,000 common shares issued

In the 8-K filing submitted on June 1, Strategy disclosed that it sold 32 Bitcoins in batches during the period from May 26 to May 31, at an average transaction price of approximately $77,135, recovering a total of about $2.5 million. As of May 31, the company still held 843,706 Bitcoins, with an average acquisition cost of about $75,699. This transaction price was still slightly above its holding cost but about 25% lower than the near $97,939 high of Bitcoin in early 2026.

During the same period, Strategy also sold 801,944 common shares, raising about $128.3 million. Part of this funding was used to address the cash gap following the discounted repurchase of $1.5 billion in convertible bonds. In the same week, Strategy completed three capital operations: "selling coins + issuing common stock + repurchasing convertible bonds," overall refining the cash buffer in its capital structure.

Analysts maintain target price: 32 Bitcoins are insignificant, but the market clearly does not agree

Saylor has repeatedly committed to "never selling coins" since starting the Bitcoin accumulation strategy in August 2020. On the night of the sale on May 31, he also posted the traditional "orange dot chart" on X, which has historically been interpreted by the market as a signal that "a new purchase of coins will be announced next week."

On June 1, the announcement of buying coins did not arrive; instead, the selling facts disclosed in the 8-K were awaited. Soon after the U.S. stock market opened, Saylor posted on X stating, "Our goal is to make $STRC the best credit tool in the world." This tweet did not mention the Bitcoin sale, nor did it provide any explanation for the first net reduction in four years. The official Strategy account also did not separately issue a statement on the coin sale; the entire incident was communicated solely through the SEC filing. This handling was interpreted by some investors as an attempt to "downplay" the situation.

Wall Street analysts have a highly consistent judgment on this coin sale: the quantity is insignificant. However, the market's actual response is obviously much more tense.

TD Cowen's Managing Director Lance Vitanza maintained an "Buy" rating on MSTR with a $400 target price. He bluntly stated that calling Strategy's substantial reduction of Bitcoin misleading, emphasizing that the 32 Bitcoins represent only 0.0038% of the company's total holdings of 843,700 Bitcoins, making it economically insignificant. Vitanza pointed out that TD Cowen's internal model already included expectations for small tactical sales and had not adjusted any core assumptions.

Benchmark's Managing Director Mark Palmer came to a similar conclusion: "We do not expect Strategy to use the sale of Bitcoin as a primary source of funding for paying STRC and other perpetual preferred stock dividends."

The volume of 32 Bitcoins has never been the problem. The issue is the cash flow pressure that it exposes.

The $100 face value red line of STRC: a fixed cash commitment of $100 million per month

Understanding this coin sale’s core is the Strategy’s STRC (Variable Rate Series A Perpetual Stretch Preferred Stock). This perpetual preferred stock is Strategy's flagship financing tool betting for nearly a year, with a scale of about $10.48 billion and a continuous 11.5% annual dividend rate for four consecutive months. Based on the current scale and interest rate, the monthly dividend expenditure is about $100 million, constituting a fixed cash flow obligation that the company must continuously meet.

The design mechanism of STRC directly links Bitcoin purchases to dividend payments. When the market price of STRC exceeds the $100 face value, the company can continuously issue new shares through an ATM tool to raise funds, partly for purchasing Bitcoin; when the market price falls below the $100 face value, the company loses the ability to raise new funds through share issuance and must use existing cash reserves to pay dividends.

In the last week of May, STRC was in a state below the $100 face value. Strategy currently has about $900 million in USD cash reserves, and after the discounted repurchase of $1.5 billion in convertible bonds in May, the cash buffer has significantly narrowed. In this context, the company chose to sell 32 Bitcoins to cover the effect of the STRC dividend for the month, which is essentially a passive fulfillment of its structural cash flow obligations.

Essential differences from 2022 and how much "buffer space" is left

The only publicly disclosed coin sale in Strategy's history occurred in December 2022 when the company sold 704 Bitcoins, realizing about $11.8 million, but it also net bought 2,395 Bitcoins during the same period, resulting in a net increase in holdings. At that time, the official characterization was "tax-loss harvesting," intended to offset capital gains from other assets and, in essence, did not constitute a reduction in holdings.

The core difference between this and 2022 is that this is Strategy's first instance of net reduction through a separately disclosed 8-K, specifically aimed at paying preferred stock dividends rather than for tax optimization purposes. Saylor himself indicated in an interview at the beginning of May that reducing some Bitcoin before the end of the year "is not impossible," which in hindsight seems quite suggestive.

Rajiv Sawhney, Head of International Portfolio Management at Wave Digital Assets, previously told Sherwood News that the sustainability of the STRC model depends on two factors: the intensity of demand from STRC investors and the health of Strategy's "debt/Bitcoin" ratio. He cited industry analysis pointing out that the company has about $10 billion to $15 billion of buffer space before this ratio reaches uncomfortable territory, but this space has "significantly diminished" over the past two months.

CoinDesk mentioned in its analysis that some market participants are comparing this coin sale to the sales in 2022, when Strategy's sale happened to be close to the bottom of the crypto bear market (when Bitcoin was around $16,800), leading to a long-term bull market afterward. Whether this coin sale will once again occur near the "bottom" will depend on Bitcoin's subsequent trend. Currently, Bitcoin's price has fallen about 25% from the early 2026 high of approximately $97,939 and still has nearly 20% space from the February low of $59,930.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。