Author: Claude, Deep Tide TechFlow

Deep Tide Briefing: Micron Technology's market value surpassed $1 trillion for the first time on May 26, becoming the fastest company in US stock market history to go from $500 billion to $1 trillion, taking only 48 trading days, while Nvidia took 490 days to reach the same milestone. UBS raised its price target from $535 to $1625, stating there is "no reason not to trade at Nvidia's valuation level." The supply and demand imbalance of AI-driven storage chips is reshaping the entire semiconductor valuation system.

Micron Technology (NASDAQ: MU) saw its stock price soar by 18-19% on May 26, with its market value surpassing $1 trillion for the first time.

The trigger was UBS analyst Timothy Arcuri raising the price target from $535 to $1625, the highest among all 46 analysts covering Micron on Wall Street. This target price implies that, based on last Friday's closing price of $751, Micron's stock has more than double the room to grow.

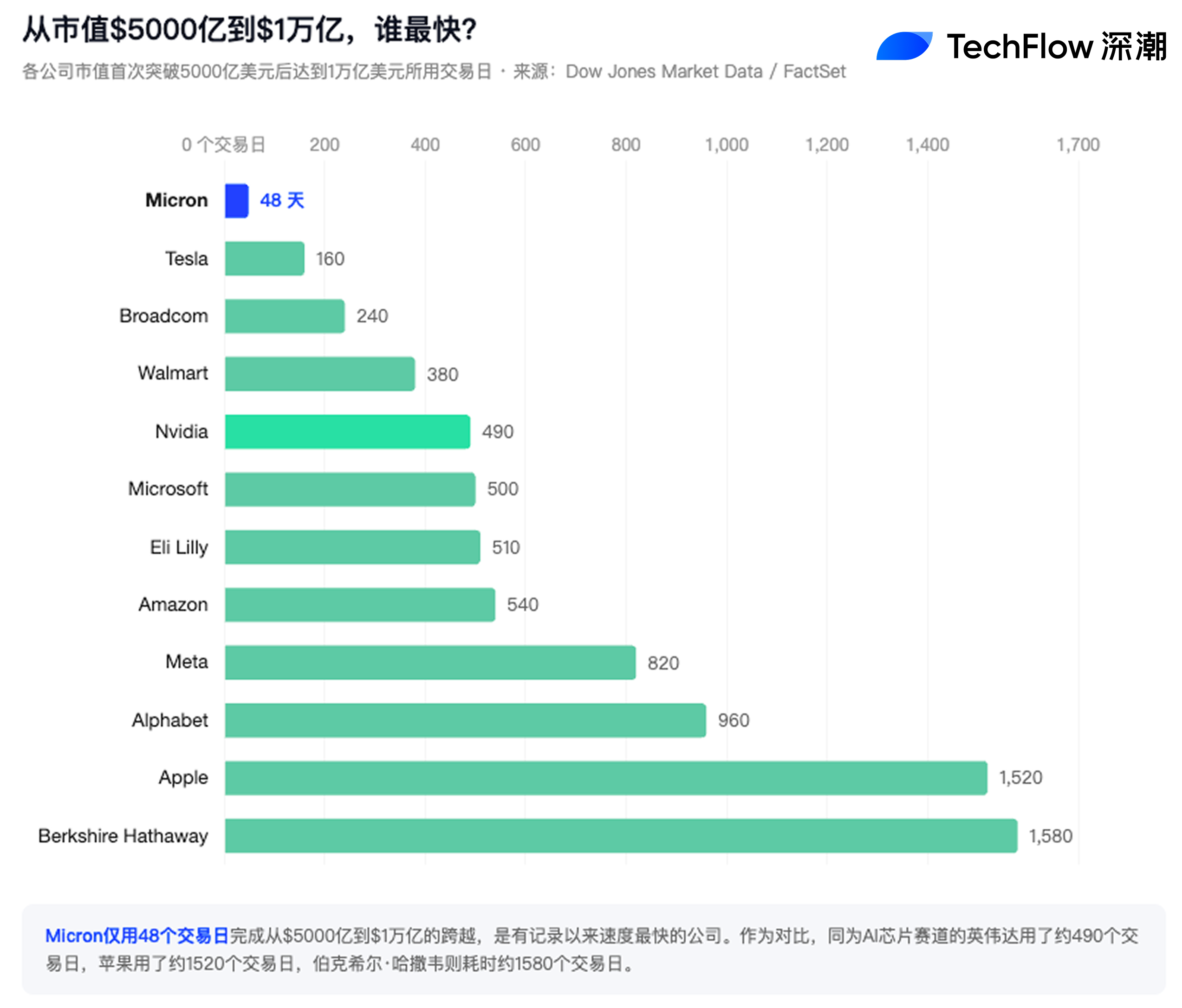

48 Days vs 490 Days: The Fastest Sprint to a Trillion

The record set by Micron is not just "another trillion-dollar company."

According to Dow Jones market data, it took Micron only 48 trading days to go from a market value of $500 billion to joining the trillion-dollar club. In comparison, Nvidia, another leader in the AI chip race, took about 490 trading days, Apple took about 1520 trading days, and Berkshire Hathaway took about 1580 trading days. Micron's speed is 10 times faster than Nvidia's.

This means that Micron is the 12th company in the US to reach a market value of $1 trillion and the first company headquartered in Boise, Idaho. In the past month, the stock has surged about 80%; since its low point at the end of March, the increase has reached 180%, with the market capitalization increase contributing nearly as much to the S&P 500 as Amazon during the same period.

Dan Russo, co-chief investment officer at Potomac, stated, "This seems unprecedented in every respect."

UBS: There is No Reason for Micron Not to Trade at Nvidia's Valuation

In its report, UBS provided a bold judgment framework: Micron is transitioning from a cyclical commodity stock to a structurally growth stock supported by long-term agreements, and its valuation method should change accordingly.

UBS pointed out that AI-driven demand is fundamentally reshaping the structure of the entire storage chip market. Long-term supply agreements (LTA) secure output and partially fix prices, which is expected to smooth Micron’s historically highly volatile profit curve. The report stated that Micron "has no reason not to trade at similar price-to-earnings levels as Nvidia."

According to UBS’s forecast, Micron's earnings per share will exceed $100 in the fiscal years 2027 to 2029. Even based on the current intraday high of about $891, the forward price-to-earnings ratio is only about 8.4 times, while the overall S&P 500 is about 21 times.

Michael Rosen, chief investment officer at Angeles Investments, had a more straightforward assessment: "For years, Micron has been seen as a commodity investment. They produce very basic things. And now, Micron has become the industry benchmark."

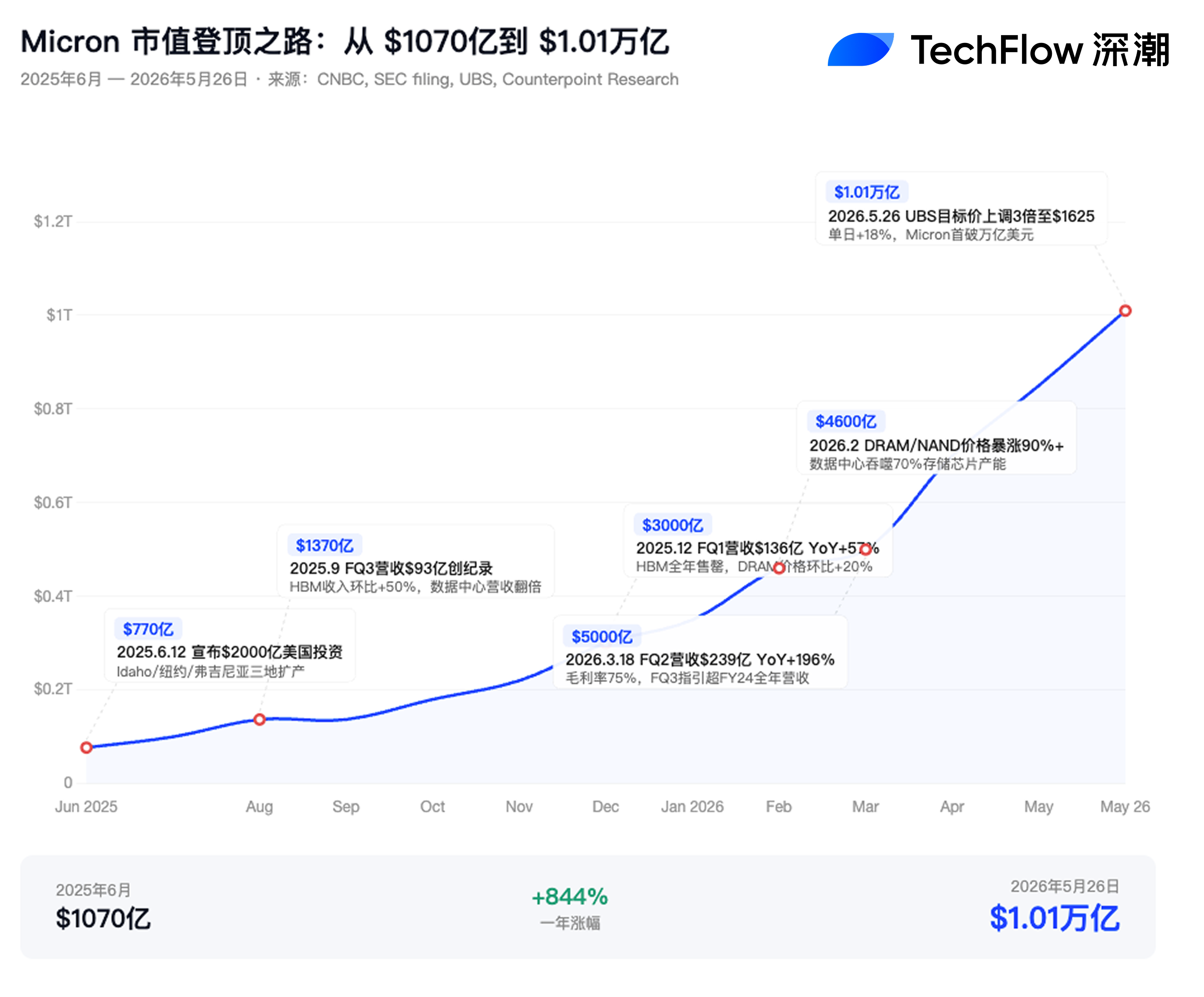

From $107 Billion a Year Ago to Over a Trillion Today: The Logic of the AI Storage Super Cycle

A year ago, in June 2025, Micron's market value was about $107 billion. Now it has multiplied nearly 10 times. Supporting this curve is a series of rapidly realized fundamental data.

In June 2025, Micron announced a $200 billion US investment plan in partnership with the Trump administration, expanding capacity in Idaho, New York, and Virginia, with the goal of relocating 40% of DRAM capacity back to the US. The FQ1 2026 financial report released in December 2025 confirmed that HBM (high-bandwidth memory, a key component for AI training chips) had sold out its annual capacity and prices were locked in, with DRAM contract prices jumping 20% quarter-on-quarter.

By March 18, 2026, when releasing the FQ2 financial report, the numbers had completely gone out of control: quarterly revenue reached $23.9 billion, a staggering increase of 196% year-on-year, exceeding Wall Street's expectation of $19.19 billion by nearly 22%. The gross margin soared to 75%, and non-GAAP earnings per share hit $12.20, 39% higher than the consensus expectation of $8.79. Even more astonishing was the FQ3 guidance: quarterly revenue of $33.5 billion, surpassing Micron's total revenue for the entire FY2024.

The underlying driver is the most severe supply and demand imbalance in storage chips in over 40 years. Data centers are expected to consume 70% of the global storage chip output by 2026. HBM capacity is sold out until 2027. DRAM and NAND prices surged over 90% in the first quarter of 2026. This is not a cyclical rebound but a structural reassessment of storage demand due to AI infrastructure development.

Micron CEO Sanjay Mehrotra stated in the FQ2 earnings call, "AI is not only increasing the demand for storage; it is fundamentally redefining storage as a key strategic asset of the AI era."

Storage Frenzy Obscures Nvidia's Absence, Philadelphia Semiconductor Index Diverges

Micron's single-day increase of 18% drove the Philadelphia Semiconductor Index up nearly 6%, but a notable phenomenon in this market trend is Nvidia's absence. The Philadelphia Semiconductor Index saw a rare and significant divergence from Nvidia's stock price, with storage and equipment stocks taking over the baton of the AI semiconductor market.

Micron currently accounts for only about 2% of the NASDAQ Composite Index and about 1.5% of the S&P 500, far below the respective weights of the "seven giants," each at over 6%. However, on May 26, Micron's contribution to both indices exceeded that of any single company among the seven giants.

Last Friday, President Trump also mentioned Micron at a rally in New York: "Oh my God, Micron is amazing."

On the prediction market platform Kalshi, the probability of whether the US government will take a stake in Micron in 2026 has reached 40%. Micron is the only US-based company among the three largest storage chip manufacturers globally (the other two being South Korea's SK Hynix and Samsung), and this identity holds additional strategic value in the current geopolitical environment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。