Author: Zuo Ye

The Clear Bill is progressing smoothly, with hopes to see multiple benefits for stablecoins, tokenization, and DeFi development at mid-year. However, the prohibition on passive interest for stablecoins will leave the on-chain outlook unclear.

It is not an overreaction. Efforts ranging from ETFs, DAT, to Wall Street RWA are constantly vying for pricing power in crypto. Compliance often means acknowledging established frameworks that erase the spark of grassroots innovation under the name of stability.

ETFs sacrifice BTCFi, DAT creates systemic crises, and RWA rejects existing public chains.

The Clear Bill compresses the arbitrage space for offshore dollar stablecoins like $USDT, but in reality, through the combination of payment and revenue segmentation, the U.S. is attempting a new model for dollar circulation beyond gold, oil, and credit.

The story of payment stablecoins is basically over, and the chapter of earning interest from stablecoins is about to begin.

Three Short, One Missing: Payment Stablecoins

Setting my heart on money learning pleasure more than Thee.

There has always been a doubt: how does the Genius Bill facilitate the realization of the "payment stablecoin" narrative?

As Wall Street giants lay out tokenization on the eve of the Clear Bill's passage, this doubt intensifies. Yes, I am not mistaken; they are positioning tokenization business for the interest of stablecoins.

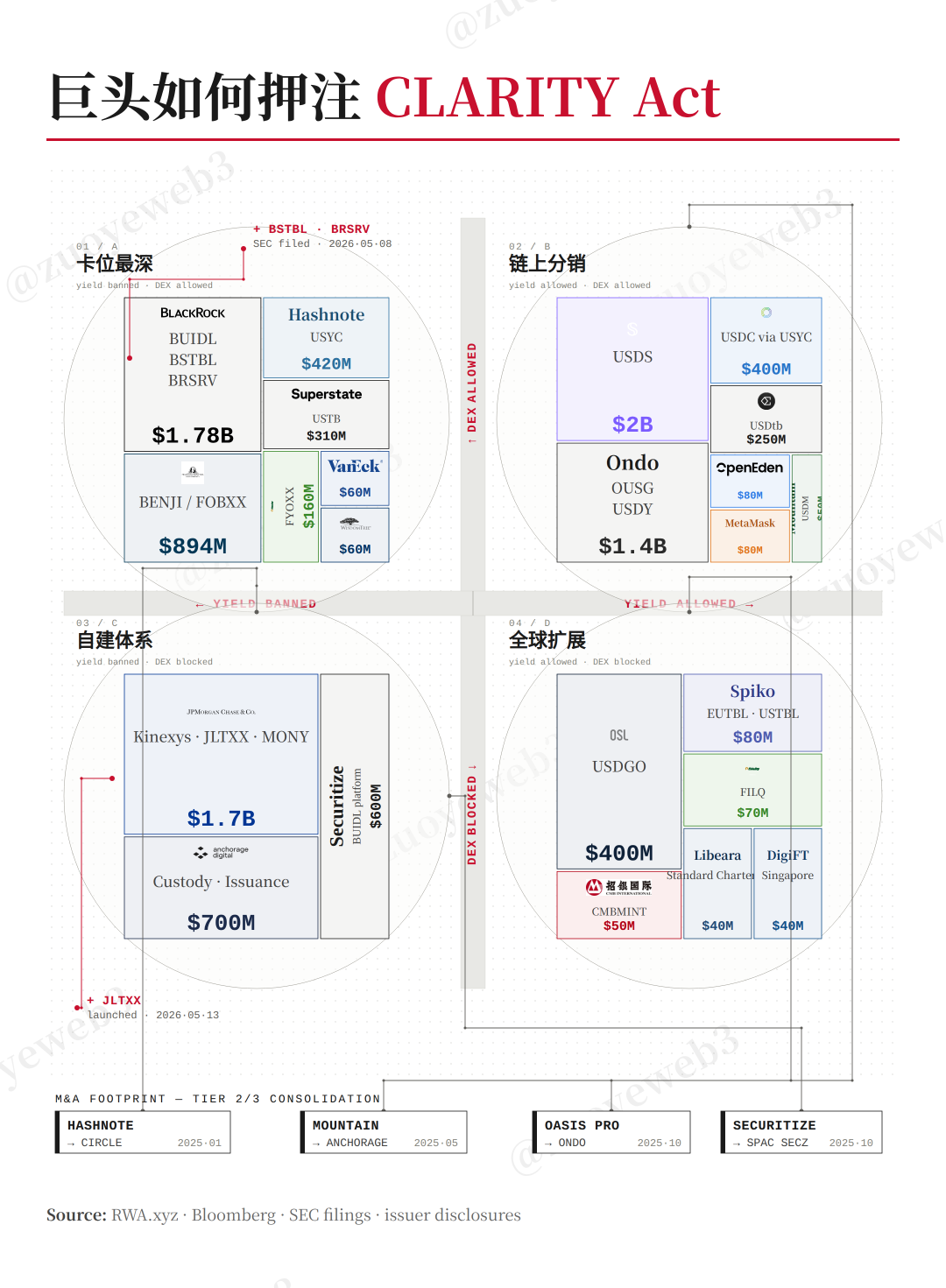

- On May 8, BlackRock plans to launch two new TMMFs (Tokenized Money Market Funds), BSTBL and BRSRV, beyond BUILD.

- On May 13, JPMorgan introduced a second TMMF, JLTXX, beyond MONY.

Not only that, BlackRock clearly stated that these new products are to meet the growing demand from stablecoin issuers, while JPMorgan also emphasized compliance with the Genius Bill's relevant qualification requirements.

Delving into the text, the Genius Bill indeed increases the descriptions of tokenization, allowing tokenized forms of U.S. Treasury and dollars to be reserves for stablecoin issuance.

This does not clarify what the relationship is between stablecoins, tokenization, and payments. We need to continue exploring.

Under the Genius Bill, the qualifications for stablecoin issuance are allocated to the federal chartered bank mechanism of the OCC. These banks cannot take deposits and must maintain adequate reserves, and cannot encroach on commercial banks' credit business.

In this context, policy creates market demand. Stablecoin issuers either build reserves themselves, like USDT and USDC, which buy up U.S. Treasury bonds beyond many sovereign nations.

Or, directly purchase TMMF and other RWA assets, which are crucial for stablecoins like USDS/sUSDS that rely on profit-sharing to attract users.

- Eliminating the complex process of purchasing and redeeming U.S. Treasury bonds;

- On-chain profit sharing and real-time earning interest align more with user habits.

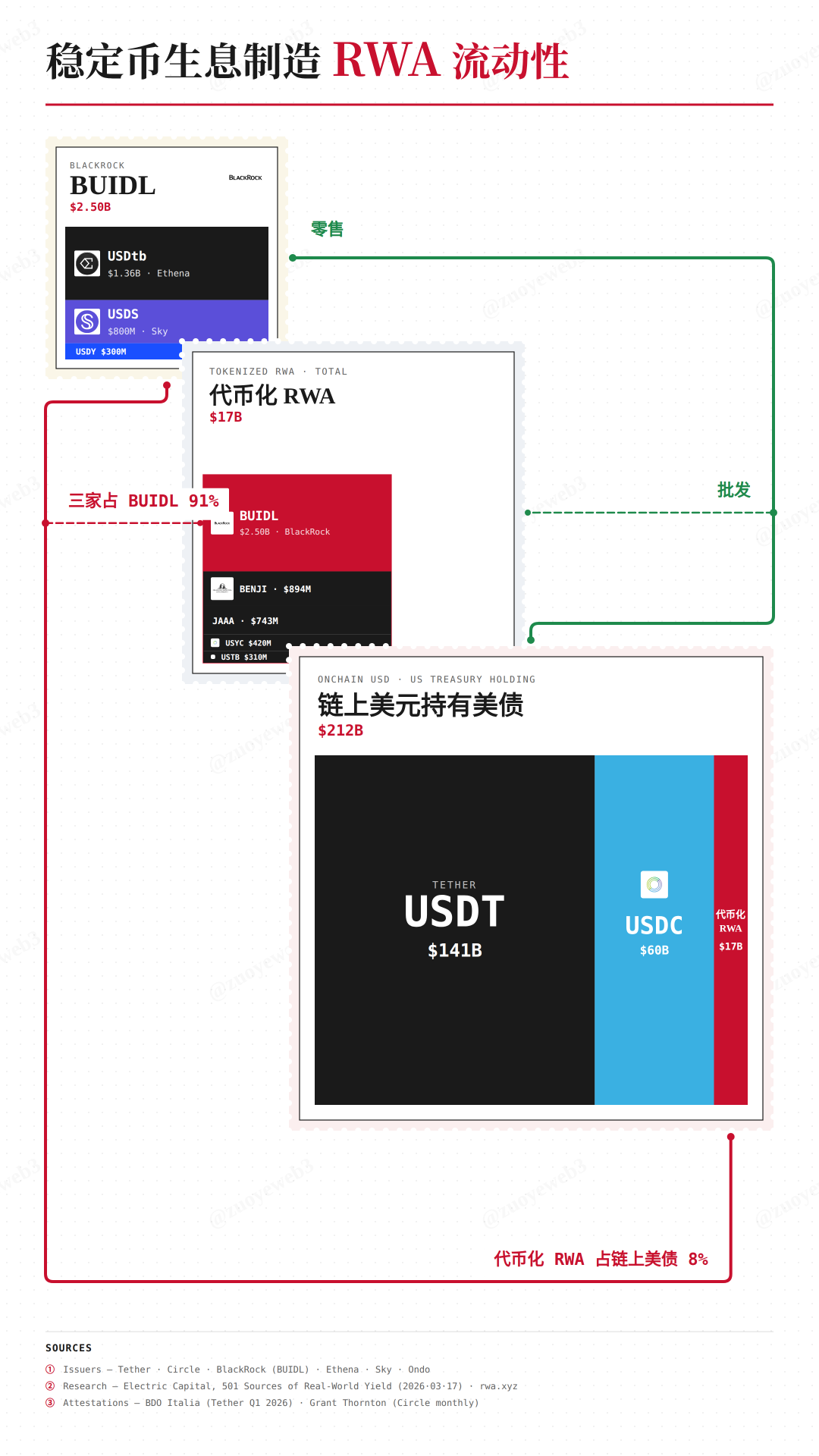

According to data from @ElectricCapital, 98% of BlackRock's BUIDL shares are subscribed by various interest-earning stablecoin issuers.

Moreover, the best part is that retail investors cannot directly purchase tokenized products; policy shapes market structure, which is the secret of how the Genius Bill can create "payment stablecoins."

A bill that relies entirely on coercive power cannot make market participants comply; otherwise, USDT wouldn’t have remained underground for so many years. Only by conforming to market trends can one achieve results.

Image Description: TMMF supports payment stablecoins

Data Source: @ElectricCapital

BlackRock's issued tokenized products, although circulating on-chain, cannot be purchased without "access," and still need to comply with KYC, qualified investor, and other scrutiny conditions, primarily targeting B-end sales.

You cannot monitor decentralized individual trades, just as the U.S. government cannot monitor the circulation of physical dollars, but monitoring a few giants is simple and straightforward.

By recognizing tokenized assets, the U.S. cleverly builds a feasible framework among stablecoin issuers, Wall Street giants, and regulators, where the stablecoins users obtain can only be used for payments, as they cannot earn interest.

A Genius Bill binds stablecoins and tokenization together, which also answers the previous doubt, making stablecoins a retail layer for U.S. Treasury bonds.

Previously, dollars relied on the credit mechanisms of commercial banks; in the future, dollars will rely on the intermediary role of tokenization companies.

Arbitrage Space: Stablecoins Earn Interest

Caring for worldly things more than God.

If the Genius Bill recognizes tokenization as creating payment stablecoins, then the Clear Bill restricts tokenization, pulling development for stablecoins earning interest into question.

The importance of earning interest does not stem from the banking sector's worries about deposit losses, nor from the difficulty of opening an account with JPMorgan or making profits with Coinbase.

Take a look: under the Clear Bill, if users choose to stake for interest, ideally, the interest source for stablecoin issuers can only be U.S. Treasury products.

But this also raises new questions. Issuers like Sky/Ethena that issue on-chain stablecoins, in a sense, do not need to first obtain an OCC bank license, so there is a need to make new arrangements for earning interest, especially DeFi earnings.

Regulatory costs are too high, which is the essence of Congress making "loose" arrangements for DeFi development. Besides, the dollar needs to be distributed in the form of stablecoins.

Image Description: Giants rushing to the Clear Bill

Image Source: @zuoyeweb3

This distribution can be divided into two major categories: one is the B-end customer acquisition paths among giants, and the other is the C-end arbitrage issuance on-chain and across regions.

Among the giants, the bet is on the strictness of the "prohibition of passive interest." The intermediary role also changes accordingly. If DeFi is limited, then the consortium chain model may be revived. If relatively loose, then closer cooperation with on-chain stablecoins is possible.

Moreover, the giants' intermediary models are hard to bypass. Ondo and others choose to be a retail distribution layer for the giants, while OSLs choose to enter the overseas compliance dollar stablecoin track.

Continuing to extend, Sky adds diverse "RWA" reserves for USDS, which is essentially leverage arbitrage, quietly switching adequate reserves into partial reserves.

A mainstream demand going forward is how to increase stablecoin yields based on U.S. Treasury bonds, requiring more complex financial engineering designs. This is where various yield strategies of DeFi can come into play.

It can be found that the earning mechanisms target offshore dollar stablecoins like $USDT, allowing BlackRock's TMMF to take over its position as a Treasury bond buyer.

For on-chain dollars and compliant offshore dollars, new arbitrage spaces will emerge. They cannot steadily earn scalable U.S. Treasury yields; they must continuously promote the growth of utilization, indirectly facilitating the circulation of dollars and stable purchasing of U.S. Treasuries.

In the ebb and flow, users will try their best to use stablecoins, as retention will devalue, while the interest generated from use will flow back into the U.S. financial system since the underlying is U.S. Treasury bonds.

This is the true purpose of the Clear Bill: to create individual demand for the dollar globally. Stablecoin issuance requires U.S. Treasuries, and stablecoins earning interest also requires U.S. Treasuries, ultimately completing the cycle.

Conclusion

To transcend the limitations of sovereign states, one must rely on the rigid demand of payments.

However, promoting the adoption of stablecoins must rely on the direct mechanism of earnings.

Both the Genius Bill and the Clear Bill focus on the intertwining of stablecoins and earning interest. Without controlling DeFi and cross-regional arbitrage, Wall Street needs to act as an intermediary to manage yields, which also gives us peace of mind that the arbitrage mechanism never sleeps, regardless of whether the Clear Bill passes on schedule.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。