Original Author: Xu Chao

Original Source: Wall Street Journal

The market's concerns about the new Federal Reserve Chairman Kevin Warsh's aggressive reduction of the balance sheet may significantly overestimate what he can actually achieve.

Warsh was recently confirmed by the Senate as the Federal Reserve Chairman. Due to his long-standing critical stance on the Federal Reserve's massive balance sheet, the market generally fears he will quickly push for large-scale balance sheet reduction. However, Bank of America interest rate strategists Mark Cabana and Katie Craig bluntly stated in their latest research report released on May 18: From both the scale and structural perspective, the actual room for Warsh to make substantial changes is extremely limited, and the direct impact on the market is expected to be close to zero.

Bank of America’s core judgment is that: in terms of the size of the balance sheet, the Federal Reserve will complete the normalization of quantitative tightening by the fourth quarter of 2025; to further reduce the size requires cutting three major liabilities: currency, the Treasury General Account (TGA), or reserves, and Warsh can only effectively operate on reserves, with limited paths and slow pace.

Regarding asset composition, MBS reinvestment arrangements are ongoing and the market has fully priced them in, while the compression effect of the weighted average maturity (WAM) of Treasury securities approaches zero due to market mechanisms counteracting each other. Both do not constitute tightening of financial conditions, nor trigger a signal for interest rate cuts.

The report also presents a scenario that has yet to be highlighted by mainstream markets: if the bank’s standing repo rate (SRP) is set equal to the interest on reserves (IOR), along with reduced disclosure requirements to lessen the "stigmatization" effect, it is expected to more effectively compress bank reserve demand, thus creating truly actionable space for balance sheet reduction. Bank of America believes that the actual impact of this proposal may exceed traditional market expectations regarding Warsh's balance sheet reduction path.

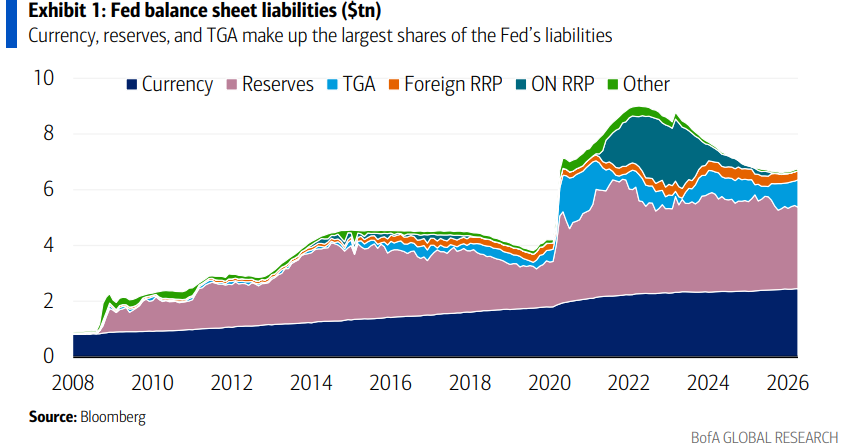

The Challenge of Scale: Three Major Liabilities, Only Reserves are Manageable

After the Federal Reserve completes the normalization of quantitative tightening, the total size is approximately $6.78 trillion, driven by liabilities. The three core liabilities are: reserves (approximately $3.12 trillion, accounting for 46%), currency (approximately $2.46 trillion, accounting for 36%), and TGA (approximately $807 billion, accounting for 12%).

Currency is considered an "exogenous" liability by central banks, outside the reach of policy tools. Bank of America points out that theoretically, it can be compressed by eliminating large denomination currency, but "this will not happen in the United States."

Regarding TGA, the Treasury has made it clear that it has no intention of compressing it, and it is expected that TGA will rise to $900 billion by the end of the second quarter of 2025, further increasing to $950 billion by the end of the third quarter.

Bank of America believes there is a possibility for marginal adjustments through repurchase investments in TGA, but the impact is minimal; adjustments through the Treasury Tax and Loan (TT&L) channel are considered "extremely unlikely."

Reserves are the most feasible option for Warsh to compress the balance sheet, but the paths each have their constraints.

The "bank-unfriendly" methods—such as setting reserve caps or tiered interest rates—would compress bank liquidity, weaken market making and lending willingness, thus dragging down the economy. Bank of America believes Warsh is unlikely to adopt such approaches.

The "bank-friendly" path is to relax regulations, allowing banks to pledge collateral to the discount window in advance to expand their high-quality liquid asset (HQLA), thus reducing reserve demand.

Bank of America estimates this path could ultimately lead to a reserve reduction of approximately $200 billion to $500 billion, but the process will be slow, and since it will not tighten financial conditions, it does not constitute a reason for interest rate cuts.

Constitutional Adjustment: The Impact of WAM Compression Approaches Zero Due to Mechanism Counteraction

At the asset composition level, Warsh's operational space is also constrained by mechanisms.

The Federal Reserve currently holds about $1.98 trillion in MBS, gradually compressing it at a pace of $10 billion to $20 billion per month by allowing maturing and early repaying MBS to be rolled out and reinvested in Treasury bills.

Bank of America believes the likelihood of selling MBS is extremely low (unless directly bought back by Fannie Mae or Freddie Mac, which is viewed as a low probability event), and the current approach has been fully priced by the market, not constituting new disturbances.

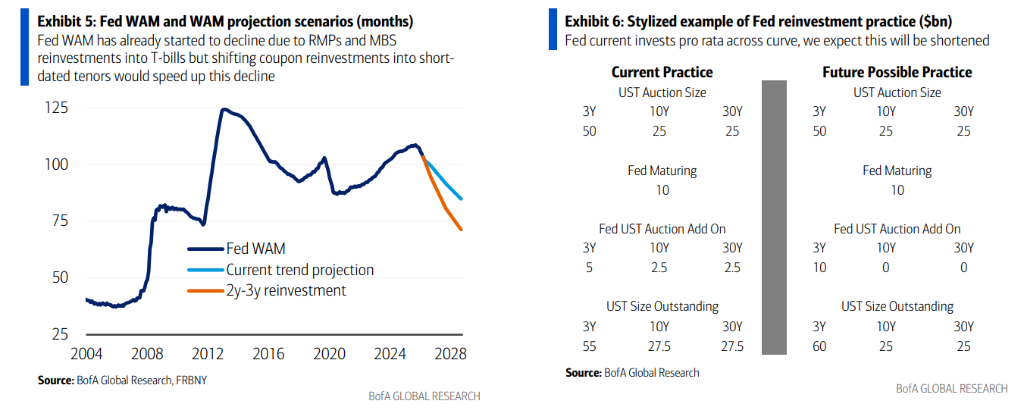

The shortening of the weighted average maturity (WAM) of Treasury securities is another focus.

Warsh may change the reinvestment of maturing Treasury securities from the current proportionally distributed method across maturities to concentrate investments in short-term offers (such as 2 to 3-year Treasury bonds) to accelerate WAM compression. However, the Fed's reinvestment adopts an auction "add-on subscription" model—this means participating in auctions in an additional manner to directly increase the short-term Treasury stock, rather than replacing long-term offerings.

This leads to a key question: will the Treasury adjust its debt issuance structure to offset the Federal Reserve's shortening of WAM's effects? Bank of America's answer is negative. If this judgment is correct, the Fed's WAM compression will have no actual impact on the overall Treasury market and financial conditions, and Warsh has no rationale to push for interest rate cuts based on this.

Abundant Reserves: Warsh has neither the willingness nor the ability to change

In Bank of America’s view, the most critical question regarding Warsh is: will he support an "ample" or "scarce" reserve system? Bank of America’s answer is: ample, with very high certainty.

The advantage of an ample reserve system lies in its ease of operation, ensuring sufficient funding for the banking system, suppressing money market fluctuations, and supporting relatively loose financial conditions, with the only cost being a slightly larger balance sheet size. In contrast, a scarce system may further compress on-balance sheet size but could lead to increased monetary market volatility and liquidity pressures, posing substantial risks.

Bank of America provides twofold support. First, Trump's emphasis on loose financial conditions far exceeds his concern regarding the size of the Federal Reserve's balance sheet, and Warsh is expected to maintain an open attitude towards his policy preferences.

Second, the Federal Reserve formally adopted the ample reserve system in 2019, and the current leadership fully supports it, with some officials' positions being quite clear—Bank of America quotes Fed Governor Waller's statements during a February 2026 speech: "You don't want banks looking for money under couch cushions every night… that is extremely inefficient and extremely foolish." Bank of America particularly pointed out the last word in its report.

Bank of America believes that Warsh is not only subjectively inclined towards an ample system but also objectively constrained by a consensus within the Federal Reserve.

SRP=IOR Mechanism May Be the True Path to Breakthrough

Bank of America proposes a reform mechanism that goes beyond the traditional framework in the report, stemming from previous statements by Dallas Fed President Logan: setting the bank's standing repo rate (SRP) equal to the interest on reserves (IOR).

The specific design allows banks to pledge Treasury or agency bonds to the Federal Reserve for cash at any time at a rate equal to their deposit rate, operating similarly to a discount window, but open all day, with no discrete operation time points.

Since the rate is competitive and without a premium, banks are more willing to use it, and the demand for holding precautionary reserve buffers decreases, thus creating actionable space for the Federal Reserve to compress the balance sheet. The Bank of England currently employs a similar mechanism.

To further enhance the effect, Bank of America suggests reforming the information disclosure system, specifically including the cancellation of the current weekly reports that disclose reserve distribution by region. This report is currently used by market participants to track institutions that may face liquidity pressures, and its cancellation could effectively reduce the "stigmatization" effect of using the SRP tool, making banks more willing to utilize the tool when needed, rather than hoarding excessive reserves.

The report also notes that the bank SRP and dealer SRP should be distinguished: the dealer SRP rate should be set about 5 to 10 basis points higher than the bank SRP, to ensure that banks are willing to lend money in the repo market while retaining pricing space for free market transactions.

Bank of America concludes that the "bank SRP=IOR" combined with the reform of the reporting system is expected to substantially reduce bank reserve demand, thus providing a truly feasible path for Warsh to compress the balance sheet. This proposal has not yet entered mainstream market discussions, but Bank of America expects it will eventually attract broad attention—its influence may far exceed the market's current traditional estimates of Warsh's balance sheet reduction capabilities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。