This is not the ideal world that the cypherpunks originally yearned for, but it is still a great undertaking worthy of being recorded in history.

Written by: Connor Dempsey

Translated by: Chopper, Foresight News

On Monday, I will start my new job. Before starting my fifth career phase, I want to write this article to review the eight years I have spent in the cryptocurrency industry.

When I entered the cryptocurrency industry in 2017, I thought this technology would change everything.

Government fiat currencies would be replaced by decentralized tokens; blockchain would eliminate all intermediaries in the transaction chain that profit without providing value; power would return from large corporations to ordinary users.

Looking back now, almost none of the original visions have come to fruition, but the industry has taken a completely different path.

I have worked at four cryptocurrency companies for eight years, witnessing the industry's growth from less than $1 billion to over $40 trillion, surviving several rounds of speculative bubbles, and witnessing a systemic collapse. I gradually realized that what the industry is actually building is far more valuable than I initially envisioned.

Before starting my next job, I want to record what I have seen and heard, as well as my predictions for the future direction of the industry.

The Illusion of Wealth Creation: The ICO Frenzy of 2017—2018

At the beginning of 2017, I came across an introduction to Bitcoin in a book and was completely hooked. Not long after, I had read every Bitcoin-related book I could find and came up with the idea of moving to Singapore to blog and deeply explore this new technology.

At that time, I did not realize that I was at the tail end of the super speculative bubble of ICOs (Initial Coin Offerings). ICOs enabled anyone to raise funds globally; by selling cryptocurrency to investors, one could crowdfund money for creative projects.

And Ethereum was the protagonist of this carnival.

In November 2017, I published a popular beginner's guide to Ethereum that went viral on Reddit. That just happened to be the peak of this bubble, and just a month later, the market bubble completely burst.

Looking back at that article now, it seems more like a historical document: it captured the optimistic mood of the time and predicted a future that ultimately did not come to pass.

My main point was that blockchain networks like Ethereum could be used to create entirely new consumer applications.

Most of the value created by traditional internet platforms (like Facebook, Uber, etc.) went to large corporations and a few investors; the value generated by blockchain applications would be shared by early participants and ICO investors.

The article also envisioned the creation of a decentralized Uber. In this system, early users and drivers could earn tokens for each completed ride, thus owning the network and allowing early co-builders to receive more equitable returns.

The vision on paper seemed beautiful, but this decentralized revolution ultimately met with complete failure.

This was a repeat of the 2001 internet bubble in a cryptocurrency speculative feast.

Ethereum became the strongest fundraising platform in history, with over 3,000 ICO projects raising a total of $22 billion globally.

But just like the internet bubble of that year, the underlying technology was not mature enough to support the astronomical valuations set by the market.

More critically, ICOs completely distorted the interests between entrepreneurs and investors. Project teams could raise tens of millions of dollars overnight based solely on an idea; investors only held tokens and could only hope for the project to deliver value appreciation. Meanwhile, founding teams held large amounts of native tokens, which they could cash out as soon as they went live, completely losing the motivation to build solid products.

During a bull market, founders and early investors made a fortune; during a bear market, ordinary retail investors were left holding the bag. Despite the presence of well-intentioned builders, ICOs eventually became a breeding ground for greed, hype, and fraud.

Throughout hundreds of years of financial history, every speculative bubble has been like this.

Rebuilding from the Ruins: The Circle Dormancy Period of 2018—2019

As the market became increasingly bleak, I leveraged some fame I had gained on Reddit to join Circle in early 2018, taking on an entry-level marketing position.

At that time, Circle had been established for four years, and several consumer products (investing, payments, exchanges) had yet to turn a profit, but the over-the-counter trading desk quietly generated stable revenue, supporting the entire company's operations.

For the next two years, the entire industry was immersed in a recession following the collapse of the ICO bubble. Most ICO projects became abandoned, thousands of tokens lost their value, and industry sentiment hit rock bottom.

However, it was during this darkest period that the seeds for the next round of revival in the cryptocurrency industry were planted.

The focus of the industry shifted from consumer applications to reconstructing the traditional financial system based on the internet.

Stablecoins, pegged to the US dollar, were initially created to allow traders to quickly enter and exit cryptocurrency positions. With a 1:1 reserve of US dollars and US Treasury bonds, the token price remained anchored at $1.

Tether's USDT quickly rose to prominence during the ICO boom, with its US dollar reserves largely held in offshore bank accounts. Initially, stablecoins were used for trading, but soon they benefited another group of people: those who could not access the traditional banking system but wanted to hold USD assets.

For example, people attempting to bypass capital controls, Chinese billionaires allocating assets abroad, and citizens of Argentina and Turkey suffering from inflation.

In 2018, Circle partnered with Coinbase to launch the compliant US dollar stablecoin USDC. While initial usage was still primarily for trading, people began to envision that this internet currency could allow anyone with internet access to seamlessly access USD assets around the clock.

Meanwhile, high-quality projects left over from the ICO era mostly focused on the financial sector. Ethereum was not only suitable for fundraising but also capable of restructuring the financial market's underlying infrastructure: decentralized finance (DeFi) ecosystems were formed by projects like Uniswap in the exchange space and Aave and Compound in the lending space.

Stablecoins and DeFi subsequently became deeply integrated, and a once-in-a-century global pandemic propelled both to new heights.

Returning to the Wild West of the Internet: The Messari Period of 2019—2021

At the end of 2019, I joined the data research startup Messari, with only 13 employees, becoming the first full-time marketing staff member.

The company had only four analysts focusing on cutting-edge DeFi research, at a time when the total market value of DeFi was just $665 million.

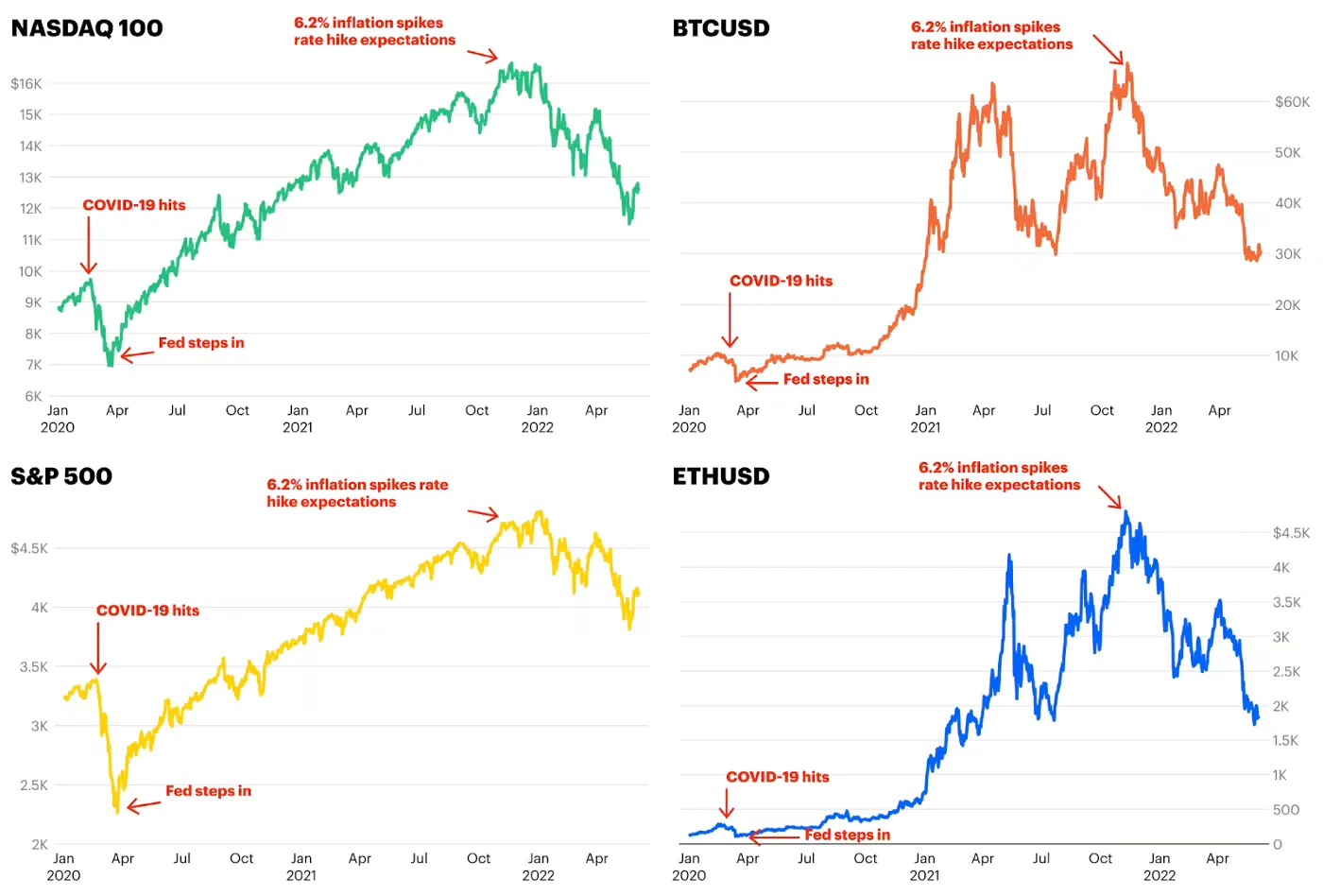

At the beginning of 2020, the COVID-19 pandemic broke out, the global economy was on the verge of a shutdown, and various assets plummeted.

To prevent economic collapse, global central banks began massive monetary easing, with a total of $9 trillion injected into the economy throughout 2020.

A large influx of hot money flowed into Bitcoin, Ethereum, DeFi, and various speculative assets due to the need for liquidity and widespread quarantines.

Bitcoin surged from under $4,000 to nearly $70,000, breaking the $1 trillion market cap with institutional backing, outperforming macro assets like gold.

The loose monetary environment also gave rise to the famous DeFi summer, where the market capitalization of DeFi protocols skyrocketed 250 times to $180 billion.

Initially, DeFi was expected to reconstruct traditional finance, but the DeFi summer resembled a massive online game dominated by profit-seeking traders, with billions of real funds entering the fray.

The core gameplay of the game was liquidity mining. Anonymous developers released new protocols one after another, with project names bizarrely clustered around various food themes: YAM Finance, Spaghetti Money, SushiSwap. Traders could deposit mainstream tokens like ETH, USDC, or USDT to claim new project tokens like YAM, SPAGHETTI, or SUSHI.

The scenes were absurd and chaotic: when a new project launched, concept tokens themed around food could hit a market cap of over $1 billion within just a few days. Early players cashed out at high levels and the tokens then plummeted.

This was truly the Wild West of the internet.

Like the previous ICO craze, the DeFi summer created a batch of new millionaires, but ultimately could not escape the fate of bubble burst. This wave also brought forth a new cryptocurrency billionaire, Sam Bankman-Fried, who would later become a key figure in the next disaster for the industry.

At the Peak of the Bubble: The Coinbase Period of 2021

In April 2021, just after Coinbase went public with a valuation of $100 billion, I was invited to join the company's corporate development and venture capital team.

My job involved participating in mergers and acquisitions, evaluating early-stage crypto projects, writing industry trend analyses, and even producing Coinbase's short-lived podcast. To this day, this remains one of the best team environments I have worked in.

It was also during this period that another round of speculative bubble quietly formed, marked by the rise of NFTs (non-fungible tokens) represented by digital art.

If DeFi was the arena for professional traders, NFTs completely broke through and entered the public eye. They provided artists with a new online monetization channel and laid the foundation for the rights management of internet digital assets.

However, like ICOs and the DeFi summer, NFT speculation quickly spiraled out of control. Digital collectibles like cartoon apes, punks, and penguins were selling for as much as $1 million; a collage piece by artist Beeple fetched a staggering $69 million at Christie’s auction.

The cryptocurrency concept thoroughly swept the mainstream: Larry David mocked cryptocurrency skeptics in a Super Bowl ad; Sam Bankman-Fried's exchange FTX spent $135 million to secure naming rights for the Miami Heat arena. Everyone became rich through tokens, NFTs, and concept stocks.

The madness of 2017 was replayed, coupled with unprecedented money printing, this round of bubble expanded fourfold.

Moment of Reckoning: The 2022 Industry Collapse

But soon, the glamour faded, and the industry collapsed.

The past benefits of raising all asset prices through interest rate cuts, monetary easing, and fiscal stimulus ultimately transmitted into consumer goods inflation. By the end of 2021, Bitcoin, Ethereum, the Nasdaq, and the S&P 500 all concurrently peaked; uncontrollable inflation became a foregone conclusion, and the central banks had to tighten policies, which were precisely the previous loose policies that had pushed the stock market and cryptocurrency assets to historical highs.

With the onset of the interest rate hike cycle and comprehensive tightening of fiscal policy, investors began to reassess their overvalued assets: Is a cartoon ape really worth $1 million? What justifies a sushi-themed token's valuation of $3 billion? How does Dogecoin support a valuation of $90 billion?

Pessimism spread, and a chain reaction of industry collapses officially began.

If the ICO bubble bursting was akin to the 2001 internet bubble bursting, the 2022 market resembled the 2008 global financial crisis: a few toxic assets piled up with high leverage nearly brought down the entire industry.

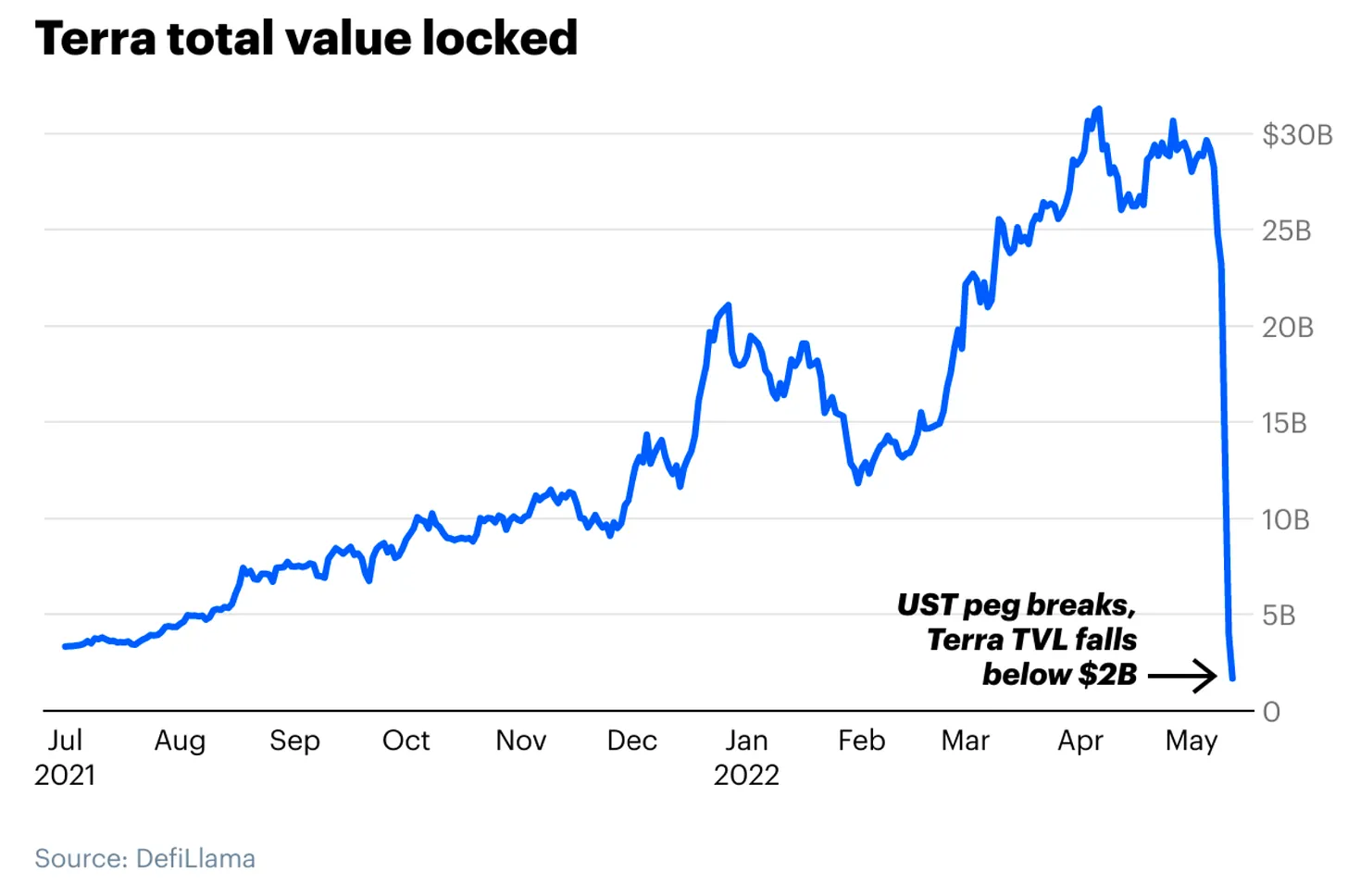

The first to blow up was the Terra algorithmic stablecoin, UST.

Mainstream stablecoins like USDC and USDT were backed fully by cash and US Treasury bonds, whereas UST depended on a complex algorithmic mechanism to maintain its $1 peg. The mechanism could function when the market was stable, but once a selling wave hit, it completely collapsed.

In just a few days, $32 billion in market capitalization evaporated, and countless holders saw their assets drop to zero.

Following that, the hedge fund Three Arrows Capital, with billions in assets under management, declared bankruptcy due to being heavily invested in Terra and its high leverage positions. Three Arrows Capital borrowed extensively from crypto lending platforms like Celsius and Voyager; these platforms misused users' cryptocurrency deposits in pursuit of seemingly stable 8% annual returns. After Three Arrows Capital collapsed, lending platforms collectively froze withdrawals and filed for bankruptcy, leaving ordinary users with substantial losses on their deposits.

During my time at Coinbase, we witnessed FTX and Sam Bankman-Fried stepping in to rescue several crypto lending institutions like BlockFi that were collapsing. He was once hailed as the "JPMorgan of the crypto world," and the industry's white knight.

But the truth eventually came to light: SBF and FTX were the ones taking on the most risk.

Do you remember FTX's extravagant spending on arena naming rights? This expenditure, and indeed the entire SBF business empire, depended on tokens FTT that the platform issued out of thin air. SBF used FTT as collateral to borrow heavily, and when the price of FTT plummeted, the loans were forcibly liquidated, and FTX declared bankruptcy.

Even worse, FTX misappropriated user funds for investments to cover financial gaps. This company, once valued at $32 billion, collapsed within a week, with $8 billion of user deposits vanishing.

SBF violated the ironclad rule in exchange operations: never touch user assets.

This is the cryptocurrency industry's "Lehman moment."

Games and Casinos: The Memecoin Craze of 2023—2025

After the collapse of FTX, SBF was thrown into prison. In just 12 months, the market capitalization of the cryptocurrency industry shrank from $3 trillion to less than $1 trillion.

Immediately after, the Biden administration began a comprehensive crackdown on the US cryptocurrency industry.

SEC Chair Gary Gensler filed lawsuits against the vast majority of compliant cryptocurrency companies, including Coinbase, Kraken, Uniswap, and Robinhood. Those companies, which had adhered to compliance for years, found themselves targeted by the SEC.

Meanwhile, Congresswoman Elizabeth Warren secretly pressured traditional banks to cut ties with crypto clients, isolating cryptocurrency companies from the banking system and forcing many teams to venture abroad.

This regulatory approach led to numerous unexpected consequences.

First, any cryptocurrency project with a business model (such as various DeFi protocols) was classified as securities violations and faced litigation risks at any time. Ironically, the safest legal choice became Memecoins—a type of purely narrative token with no actual application or clear vision.

The Pump.fun platform launched millions of Memecoins, with celebrities like Iggy Azalea, Caitlyn Jenner, and influencer Hawk Tuah Girl issuing personal Memecoins, all of which ultimately turned into farces.

The cryptocurrency industry once again devolved into a giant casino, larger than ever before. The number of Memecoins launched by platforms exceeded 6 million, with market capitalization peaking at $150 billion by the end of 2024, dwarfing the NFT boom.

Path to Institutionalization: The Crossmint Period of 2025—2026

Setting aside this industry farce, the gambling in the crypto circle betting on Trump's election came to fruition.

Once the expectations for Trump’s victory became clear, Bitcoin hit new highs. The market pricing logic was straightforward: the world’s largest economy switched from hostile regulation to supportive policies. Gary Gensler resigned, and the new SEC dismissed lawsuits against US crypto companies, while traditional banks reopened their cooperation with crypto businesses.

The most crucial development was the formal passage of the GENIUS Act in July 2025, the first federal cryptocurrency legislation in the United States, which established clear regulatory rules for stablecoins.

Washington sent a clear signal to Wall Street that the cryptocurrency industry, especially stablecoins, was about to become a major commercial sector. Companies like Bridge and BVNK were acquired by Stripe and Mastercard for over $1 billion valuations; Rain completed a nearly $2 billion Series C funding round; my former employer, Circle, the issuer of USDC, successfully went public, reaching a peak valuation of $60 billion in June 2025.

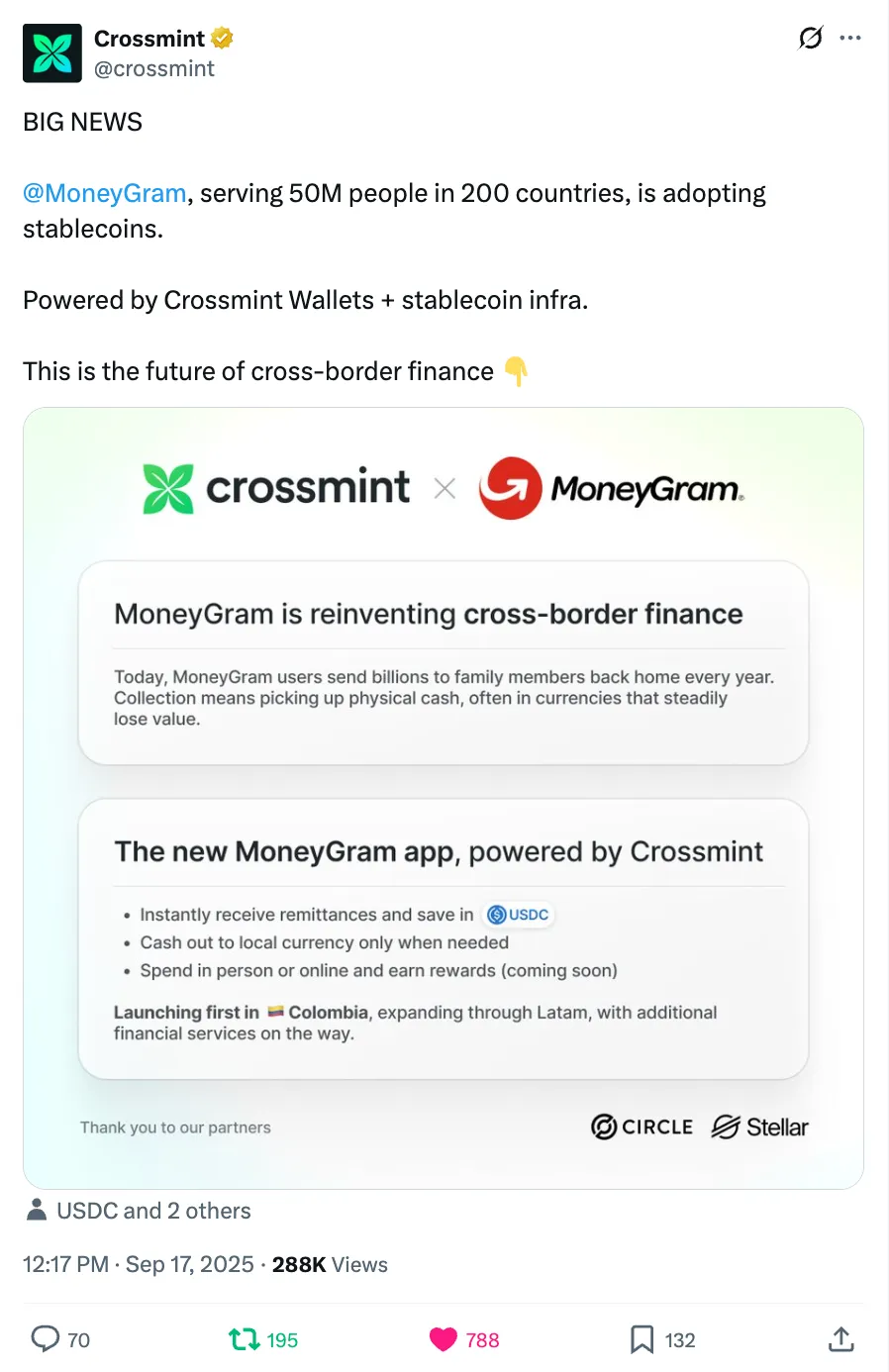

By then, I had taken on the role of marketing head at Crossmint, where the company partnered with MoneyGram to help the century-old cross-border remittance giant use stablecoins for global fund transfers.

With the value of dollar tokenization becoming increasingly apparent, Wall Street began serious plans for tokenizing other assets. Even Larry Fink, CEO of BlackRock, who once mocked Bitcoin as a "money laundering index," changed his stance, stating that tokenization is the next generation revolution for financial markets and that all asset classes, including stocks and bonds, will end up on the blockchain.

An Unforeseen Revolution: The Current State of the Industry

It has been eight years since I published that beginner's article on Reddit, and we still have not ushered in the decentralized Uber.

Blockchain has not eliminated all intermediaries, and decentralized tokens have not replaced national fiat currencies.

But I believe that looking back through history, these tumultuous years will ultimately be defined as the chaotic nascent phase of a new internet financial system. Each round of prosperity and collapse has solidified the underlying infrastructure, reshaped the global financial landscape, and allowed anyone with a smartphone to equally access financial services.

ICOs proved that companies can raise funds globally with no barriers; DeFi proved that services like trading and lending can be fully automated by code; NFTs established the underlying framework for rights management of internet digital assets; even the seemingly most valueless Memecoin cycle validated that the underlying infrastructure on this chain is capable of handling global traffic at scale.

The future simply requires the tokenization of traditional assets such as stocks, bonds, and real estate, combined with the implementation of regulatory rules, to facilitate the on-chain migration of the entire traditional financial industry.

Critics may still easily dismiss all of this, but the data regarding stablecoins is undeniable.

The total supply of stablecoins currently surpasses $300 billion, with settlement volumes expected to reach $33 trillion in all of 2025; this year, transaction volumes have already exceeded $40 trillion, with the whole year likely aiming for $100 trillion.

Skeptics will say that a significant portion of this comes from crypto trading and bots, which has some validity. But the large volume of transactions is already a given, and the US government's stance has already indicated the future direction of the industry.

A subtle yet critical logic is that stablecoins are backed by US Treasury bonds, which are the debts issued by the US government for fiscal expenditures. Every time a stablecoin is issued, it generates new demand for US Treasury bonds, which aligns perfectly with the current financing needs of the US Treasury. For this reason, the US Secretary of the Treasury has already prioritized the development of stablecoins as a national strategy.

This is not the ideal world that the cypherpunks originally yearned for. However, upgrading the dollar system for the internet era and allowing ordinary people worldwide to enjoy equal financial services is itself a great undertaking worthy of being recorded in history.

Future Directions for the Industry

Artificial intelligence is disrupting every industry, and the cryptocurrency sector is no exception.

The integration of cryptocurrency and AI has already begun, and millions of AI agents will soon participate in real commercial transactions: utilizing stablecoins tied to bank cards to connect with merchants in over 200 countries worldwide; leveraging crypto wallets and stablecoins for peer-to-peer automated transactions between agents.

In the future, AI agents will handle shopping for us, manage personal finances, and even represent large enterprises in completing transactions; this is a high-probability trend. Looking further ahead, pure AI-driven commercial entities will emerge: for instance, quantitative hedge funds that do not require analysts or fund managers, automatically reading financial reports, building models, and trading independently.

In the process of bringing this sci-fi level future to fruition, the cryptocurrency industry will not disrupt traditional finance; instead, it will integrate with it and fully move into the mainstream: backend infrastructure will be completely replaced with blockchain while the frontend user interface remains in traditional forms that the public is familiar with, so that most people may not even perceive the underlying cryptocurrency technology.

Traditional institutions will be eliminated as they rely on outdated financial systems that have been in use for decades; startups will create the next generation of financial giants. Ultimately, a financial system that operates continuously around the clock, providing fair global services without discrimination will be formed—Nigerian users and New York users will enjoy completely equal financial service privileges, leading to the emergence of millions of financial innovations.

Looking back eight years later, my current predictions may also be riddled with flaws, just like that Reddit article from years ago.

But in any case, next week I will embark on my fifth professional career in the cryptocurrency industry, immersed in this industry transformation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。