On May 7, after the US stock market closed, Coinbase released its Q1 2026 financial report. The data shows that the company's total revenue was $1.41 billion, a year-on-year decline of 31%.

Due to the unrealized losses from holding cryptocurrency assets, the company recorded a net loss of $394 million, with a loss of $1.47 per share, whereas the company achieved a net profit of $66 million in the same period last year.

After the financial report was released, Coinbase's stock price fell about 4.7% in after-hours trading, with a cumulative decline of over 15% this year.

Trading revenue dropped by 40%, institutions and stablecoins were highlights

The loss Coinbase suffered this time was largely due to unrealized losses.

Behind the net loss of $394 million was an unrealized loss of $482 million from the company's held investment cryptocurrency assets. This part of the loss is accounted for based on price fluctuations and does not represent actual cash outflows.

Excluding this part, the company's adjusted net loss was only $45.6 million, with an adjusted EBITDA still positive at $303 million, and an operating loss ofabout$21.4 million.

The cryptocurrency market was generally sluggish this quarter. The price of Bitcoin dropped from over $97,000 at the beginning of January to around $63,000 at the beginning of February, and by the end of the period, it was still hovering below $70,000, with market sentiment plummeting and retail trading activity significantly shrinking. According to CoinGlass, the global cryptocurrency spot trading volume in Q1 was approximately $1.94 trillion, a year-on-year decrease of about 44%.

As a result, the companysaw overall trading revenue decline by 40% to $756 million,of which consumer trading revenue was $567 million, a year-on-year decline of 48%. Despite the trading volume being halved, Coinbase's global cryptocurrency spot market share increased to a historic high of 8.6%, ranking fourth among global spot exchanges.

On the institutional side, however, the trend was distinctly different. The company achieved institutional trading revenue of $136 million, a year-on-year increase of 37%. Even more impressive was the derivatives business,benefiting from the acquisition of Deribit completed in August 2025, the company's derivatives trading volume increased by 169% year-on-year, and the collateral size for derivatives clients surged from $27.4 million at the end of last year to $333 million at the end of this season, an increase of more than 10 times.

In terms of subscription and service revenue, the company recorded $584 million this quarter, a year-on-year decline of 14%, significantly less than the decline in trading business, accounting for 44% of total net revenue. Among them,stablecoin revenue was $305 million, a year-on-year increase of 11%, making it one of the few highlights of this quarter. By the end of the quarter, the company's platform asset scale was $294.4 billion.

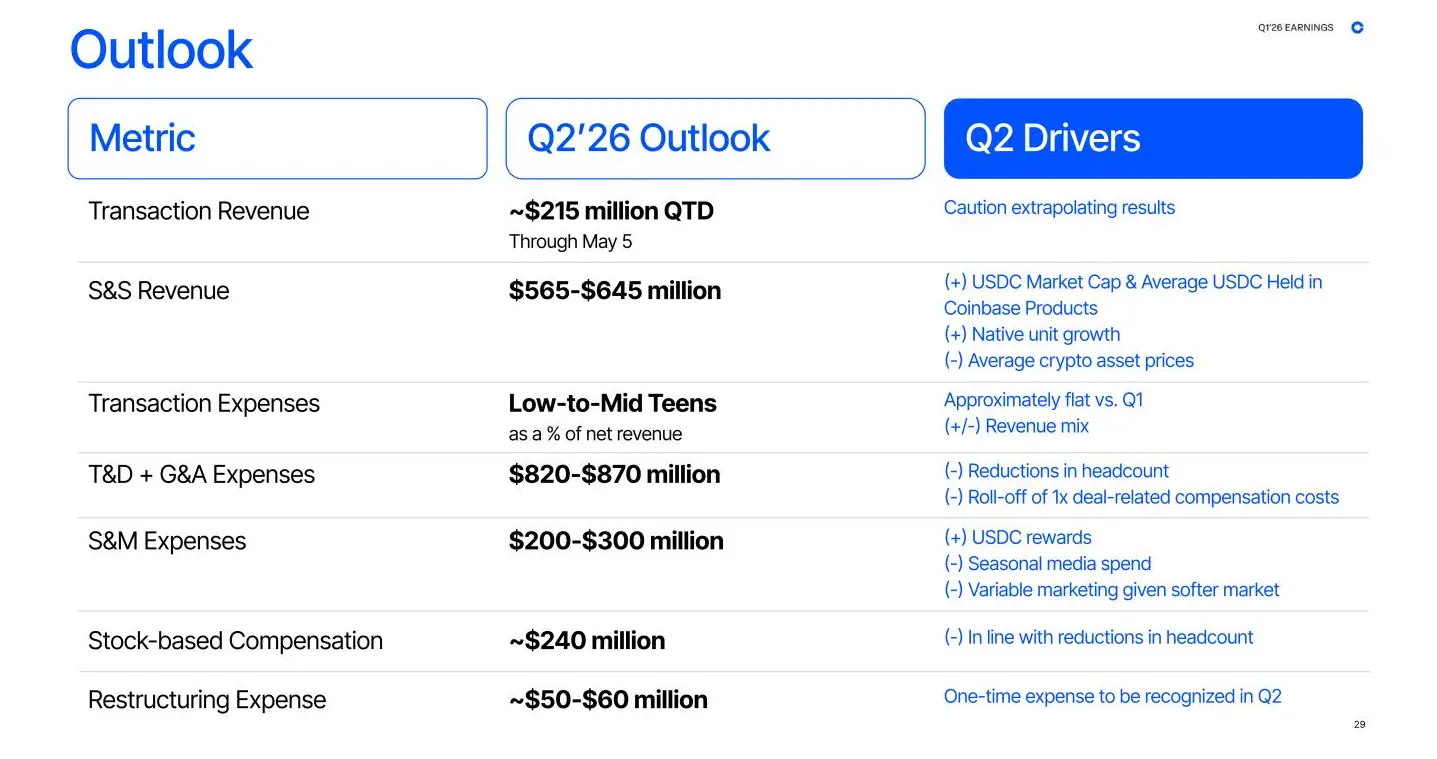

Looking ahead to Q2, the management's outlook is generally cautious. The company disclosed that trading revenue was approximately $215 million as of May 5, but management emphasized that the current market is highly volatile and this figure does not represent the performance for the entire quarter. The guidance range for subscription and service revenue is between $565 million and $645 million, with the midpoint slightly higher than Q1's $584 million, showing that management still holds confidence in this revenue line. The reorganization costs related to this round of layoffs, estimated at $50 to $60 million, will be recognized as a one-time expense in Q2, after which cost pressures will be significantly relieved.

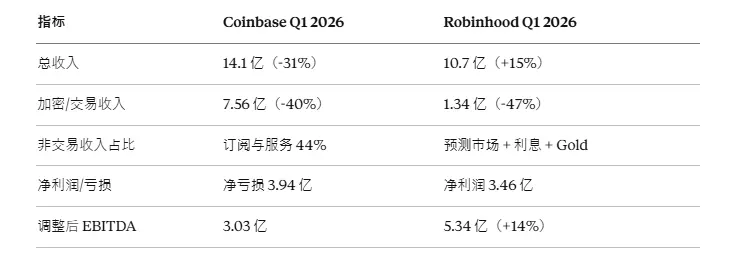

It is worth mentioning that Robinhood's Q1 financial report presents a different picture. Its total revenue increased by 15% year-on-year to $1.07 billion, with a net profit of $346 million and adjusted EBITDA reaching $534 million.

Looking closely at the structure, the quality of the growth is worth scrutinizing. Revenue from cryptocurrency-related activities also dropped by 47% to $134 million, while the company filled the gap primarily through three business segments: revenue from prediction market contracts surged 320%, becoming the largest increment source; net interest income grew by 24% to $359 million; Gold subscription service revenue increased by 32% to $50 million.

Additionally, Robinhood secured the exclusive initial trustee status for Donald Trump's accounts, investing about $100 million in additional construction costs for this.

In this quarter, Robinhood maintained its growth through prediction markets and the policy dividends from the Trump account, while Coinbase bet on a longer-term transformation under the pressure of halved trading volume.

Defense: Cutting 700 people, what is the company restructuring?

On May 5, just two days before the financial report was released, Coinbase announced the layoff of about 700 employees, accounting for 14% of its global workforce.

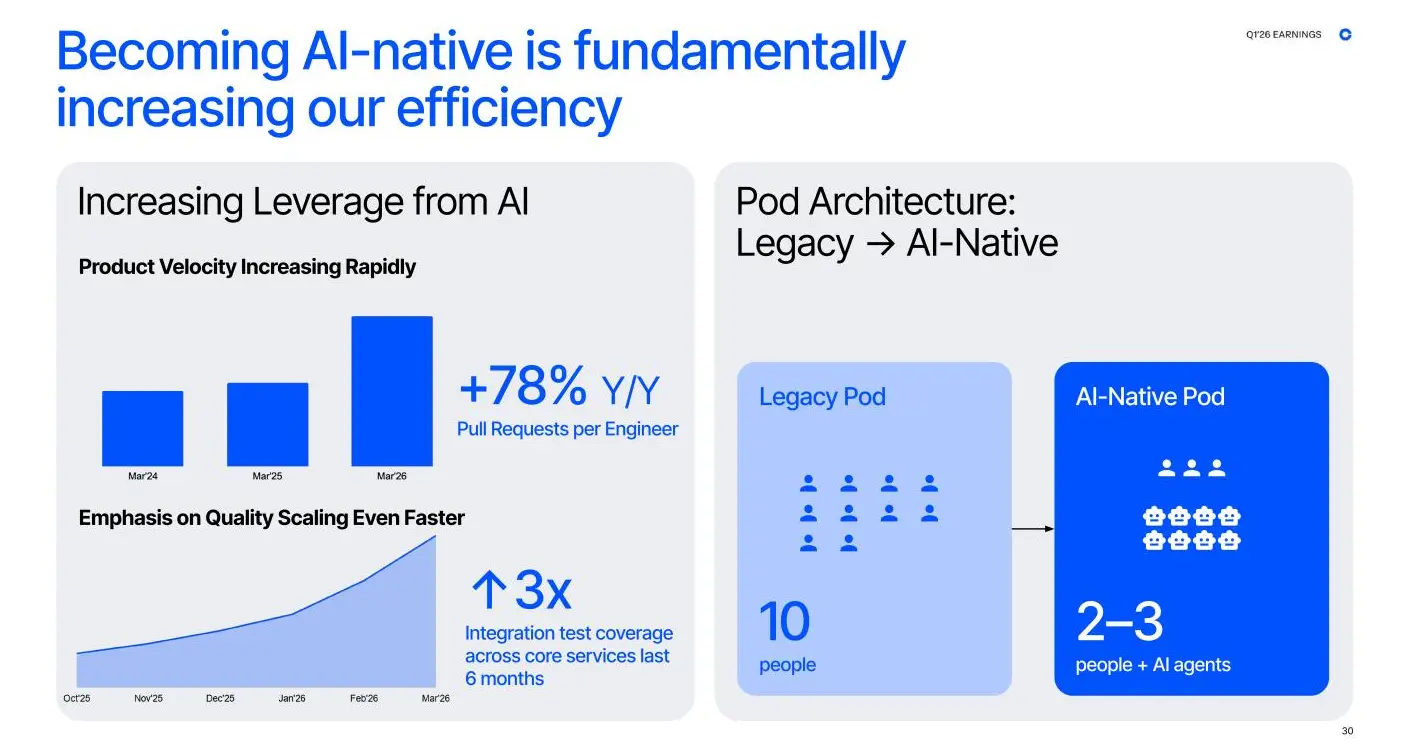

CEO Brian Armstrong stated that this restructuring aims to return the company to its entrepreneurial speed, accelerating the transformation to an AI-native organization, with the goal of reconstructing Coinbase into an organization centered on intelligence, collaboratively developed by humans at the edges.

Coinbase defines this approach as"AI-native"—not introducing AI tools within the existing organization, but redesigning the company's operational mode from the ground up.The data provided by the company shows that engineers' average Pull Request count increased by 78% year-on-year, team structures were reorganized from traditional 10-person Pods to AI-Native Pods with 2 to 3 persons plus AI agents, and core service integration testing coverage increased 3-fold over six months.

However, this accounting needs to be clarified. Dragonfly venture partner Omar estimates that this round of layoffs is expected to save the company about $225 million in annual salary costs. But the 2026 full-year expense guidance shows that, excluding the impact of the growth of USDC rewards, expenses will remain basically flat year-on-year, which means,the cost savings from the layoffs are largely offset by the investment in user incentive programs.

It is worth mentioning that over the past year, OpenAI has continuously poached at least 6 senior marketing executives from Coinbase, including former Chief Marketing Officer Kate Rouch, Sarah Russell, and Sarah Wolf, who was responsible for marketing for the Base chain, moved to Anthropic. Coinbase officially characterized these departures as normal personnel turnover, but interestingly, the company is reconstructing its organization and reducing personnel with AI, yet has delivered its most knowledgeable marketing talent about brand and growth to AI companies.

When asked whether there would be further layoffs in the future, CFO Alesia Haas stated, "We cannot predict the future, but as a public company, we will always do what is in the best interest of the company."

Offensive Side: Layout of on-chain financial infrastructure

Everything Exchange landscape

At the end of last year, Armstrong proposed the strategic goal of "Everything Exchange"—to transform Coinbase from a spot-focused cryptocurrency platform into a multi-asset comprehensive platform covering derivatives, commodities, futures, and prediction market contracts, allowing users to switch seamlessly between different platforms.

Q1 data shows that, derivatives, prediction markets, and decentralized trading have all shown strong growth, and transactions initiated by AI agents on the Base chain accounted for 90% of the chain's trading volume, with derivatives trading reaching an all-time high, and contract business first exceeded spot trading.

The effectiveness is beginning to show, and the company has recently been aggressively increasing its investments, including investing in Centrifuge to lock up RWA tokenization underlying assets, taking a stake in Kemet to integrate institutional derivatives channels, launching a stablecoin credit fund CUSHY, obtaining OCC national trust qualifications to overcome institutional custody compliance barriers, and partnering with AWS to integrate wallet infrastructure and the x402 protocol into Amazon Bedrock's AgentCore payment system, allowing AI agents to autonomously complete micropayments using USDC.

Stablecoin moat

Beyond the expansion of trading categories, the stablecoin business constitutes a more fundamental revenue moat for Coinbase.

According to the revenue-sharing agreement between Coinbase and Circle, 100% of the earnings generated by USDC within the platform belong to Coinbase, while earnings from USDC outside the platform are shared 50/50 between the two parties.

Currently, the market capitalization of USDC has reached about $80 billion, a historical high, with over 25% held by the Coinbase platform, and the platform's balance has grown nearly 10 times compared to three years ago. As the adoption of USDC continues to expand, the slice of the pie that Coinbase can claim is also growing.

However, this revenue stream is not without its concerns, with the average interest rate this quarter dropping by 67 basis points, resulting in about $57.5 million in negative impact on stablecoin revenue, and fluctuations in the interest rate environment could weaken the elasticity of this revenue line.

CFO Alesia Haas emphasized in the earnings call that, "Our USDC contract automatically renews every three years, and it is a perpetual renewal; this contract cannot be terminated." CLO Paul Grewal then added, "We expect to maintain the partnership with Circle under the same terms in the future."

This statement is clearly a response to market concerns regarding stablecoin regulatory legislation, with Coinbase engaging in a long-term strategic game around the CLARITY Act:

- In January, support was withdrawn due to unfavorable revenue terms, causing the Senate to postpone voting;

- In March, the new draft was again rejected, resulting in Circle's stock price plummeting 20% in a single day;

- At the beginning of May, a compromise text emerged, prohibiting "interest for holding" but retaining a reward system tied to actual activity. Armstrong replied "Mark it up" on X, and Grewal publicly expressed great confidence in the bill passing this summer.

The true value of this game lies in Coinbase not just complying with regulations but actively participating in the formulation of these regulations. The legal teams, compliance processes, and regulatory communication capabilities required to repackage yield products represent resource barriers that smaller exchanges cannot replicate in the short term.

In other words, once the CLARITY Act is enacted, the advantages of top platforms will be solidified by legislation, and regulatory clarity will benefit the entire industry, but the ones who benefit the most will always be those capable of sitting at the negotiation table.

However, it is worth noting that after the bill is passed, there will still be a 12-month rule-making phase, and the final boundaries have yet to be defined; uncertainties remain in place.

Conclusion

With trading volume halved by 50% and a net loss of $394 million, Coinbase's financial report serves as a reminder to the market that the company has not yet escaped the strong binding to the crypto cycle. There are plenty of skeptical voices in the market: is the AI narrative a genuine transformation or just a wrapper to cover business declines?

Brian Armstrong repeatedly emphasizes that "all finance will eventually move on-chain," as crypto increasingly resembles traditional finance, Coinbase is also striving to make itself more like a mature financial infrastructure company. This may just be the answer it provides during the current cycle.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。