Author: Dan Gray

Translated by: Deep Tide TechFlow

Deep Tide Introduction: This article starts from the historical roots of "financialization" and explains why the current economy increasingly resembles a casino. From meme stocks to cryptocurrencies, from sports betting to venture capital's "lottery ticket" mentality, author Dan Gray argues that when capital no longer flows to productive activities and instead circulates in financial engineering, the true health of the economy is being obscured. The article concludes with a call to return to "re-industrialization," betting on hard-tech companies that solve real problems.

The full text is as follows:

"Speculators as foam on the torrent of solid enterprises may not do much harm. But when the operation of enterprises themselves becomes foam on the vortex of speculation, things become serious. When the capital development of a country is reduced to a byproduct of casino activities, the work is mostly not done well."

--John Maynard Keynes, "The General Theory of Employment, Interest, and Money" (1936)

Meme stocks, cryptocurrencies, leveraged bets, prediction markets, VC's white-knuckle betting $2 billion in seed rounds.

The savings rate has hit a historic low, while debt has reached a historic high.

Capital has never been so anxious. Creating wealth has turned into a game of luck, betting big and hoping to hit it big.

Gambling has permeated every corner of the economy, from institutions to individuals, from top to bottom. It shapes the behavior of the younger generation and also influences the direction of tech investments.

Welcome to casino culture.

Caption: "Double or nothing" — from Shane Levine's Apple Pay design concept

The Roots of Financialization

To understand casino culture, we first need to clarify how we arrived at this point. The core concept is called "financialization," which refers to the gradual separation of capitalism from productive activities in the economy.

The actual performance is this: economic returns have shifted from producers to capital holders. This is the opposite of industrialization. During the industrialization period, investments in manufacturing and infrastructure increased, and economic returns flowed from capital owners to the production side.

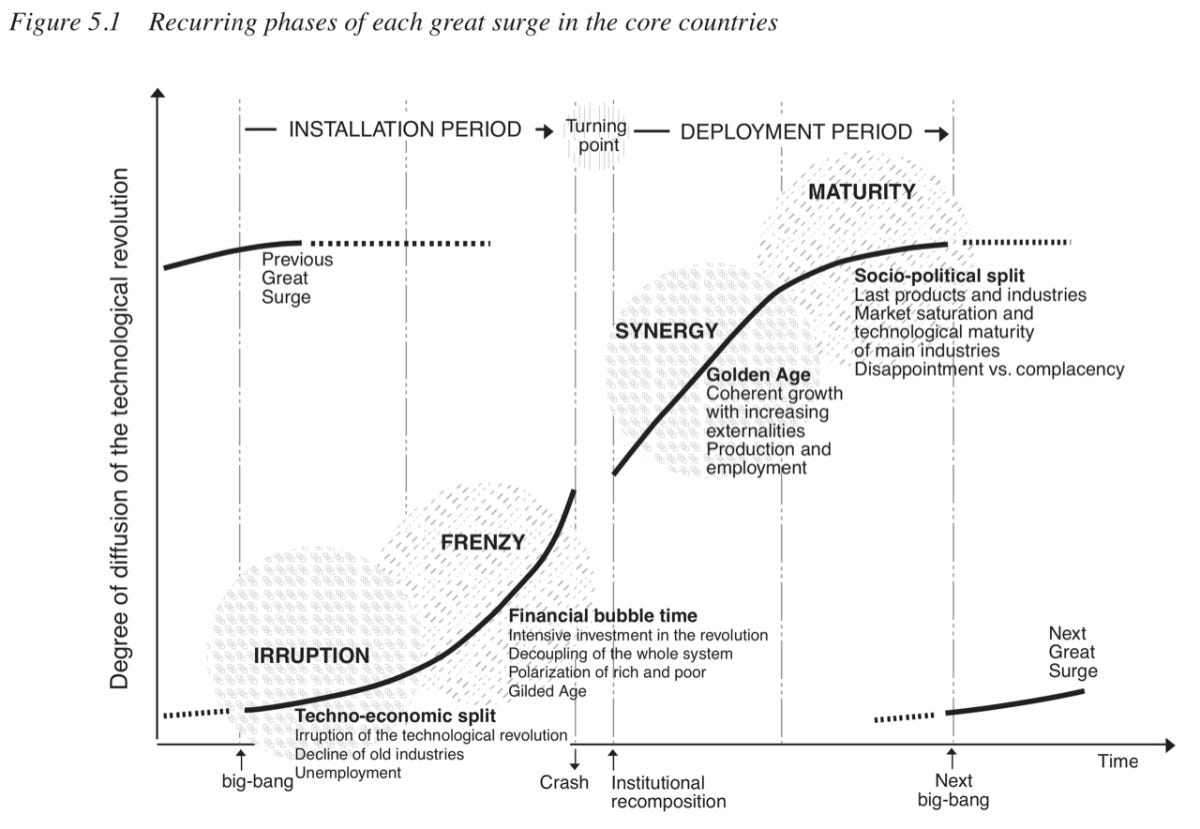

These two forces alternate with major technological revolutions, which is a core issue in Carlota Perez's book "Technological Revolutions and Financial Capital". In the early stages of market booms ("installation period"), large amounts of capital flow into meeting capital needs, overlapped by a layer of pure speculation. At some point, the market corrects (bubbles burst), leading to a new phase of production ("deployment period") where new technologies spread throughout the economy, driving widespread prosperity.

In a healthy economy, this complete cycle occurs roughly every 40 to 60 years, generally driving human progress. However, the West has experienced about 50 years of uninterrupted inflation in financial services and stagnation in industrialization.

Caption: Technological revolution and financial capital cycles, source Carlota Perez

From a policy perspective, financialization has been driven by the deregulation of financial markets (such as the American Nixon Shock, GLBA Act, and NSMIA Act), combined with money printing under the banner of "quantitative easing." As a result, companies are incentivized to pursue success through financial engineering. Shareholders focus on metrics that represent financial market performance, rather than actual economic production activities.

Consider the recent low interest rate era — which could have spurred unprecedented growth in manufacturing and infrastructure. Instead, financialization has spawned a whole generation of "asset-light" companies, efficiently turning abundant capital into inflated valuations and shareholder returns. Capital circulates in pools without flowing toward productive activities.

Historically, financialization began with mercantilism and the gold and silver standard in the 16th to 18th centuries. At that time, international trade was often settled in precious metals, and politics eventually leaned towards accumulating precious metals as a marker of success, rather than a more active and productive trade economy. This shift, along with the related "zero-sum game" thinking, is the underlying logic of many economic dilemmas today.

"We can always find the biggest thing is to get money... If we were to seriously prove that wealth is not measured by gold and silver currency, but by what money can buy — money has value only because it can buy — that would be absurd."

--Adam Smith, "The Wealth of Nations" (1776)

Profit does not bring prosperity

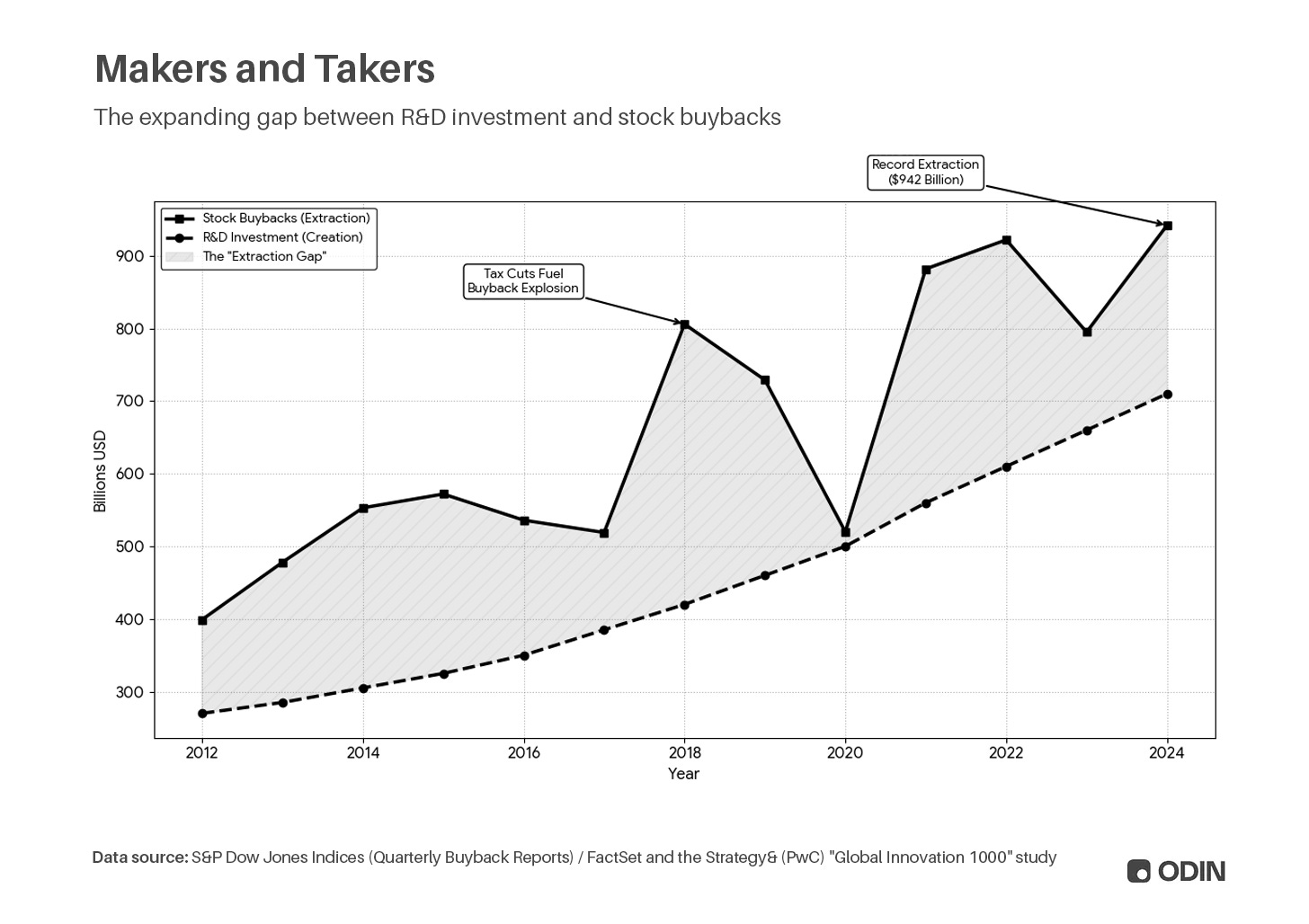

The preference for accumulation is reflected in publicly traded companies treating market value as the ultimate indicator of success. For example, more and more companies choose to distribute profits through dividends or share buybacks (buying back shares to reduce supply and raise earnings per share and stock price), rather than investing capital in R&D or capital expenditures. In plain terms, companies are not doing things that create more value but are manipulating metrics and ratios to make market value look good.

This behavior makes some sense to a certain extent, after all, it's about creating value for shareholders. But the risk is that it creates "hollow" companies with inflated valuations, ultimately eroding the productivity of the entire economy.

"For American manufacturers, the ratio of dividend payments to capital equipment investment rose from around 20% in the late 1970s and early 1980s to 40% to 50% in the early 1990s, and over 60% in the 2000s. In other words, market pressures force companies to maintain stock prices with higher dividends (or stock buybacks), rather than reinvesting funds in capital."

--"The Greater Stagnation," Luke A. Stewart and Robert D. Atkinson (2013)

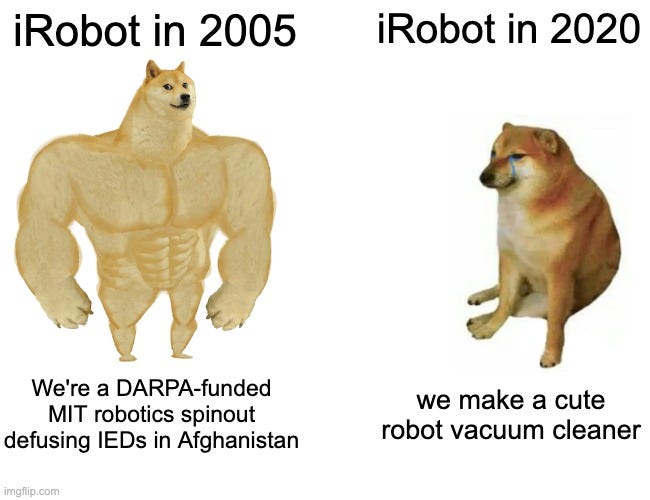

We once had robots

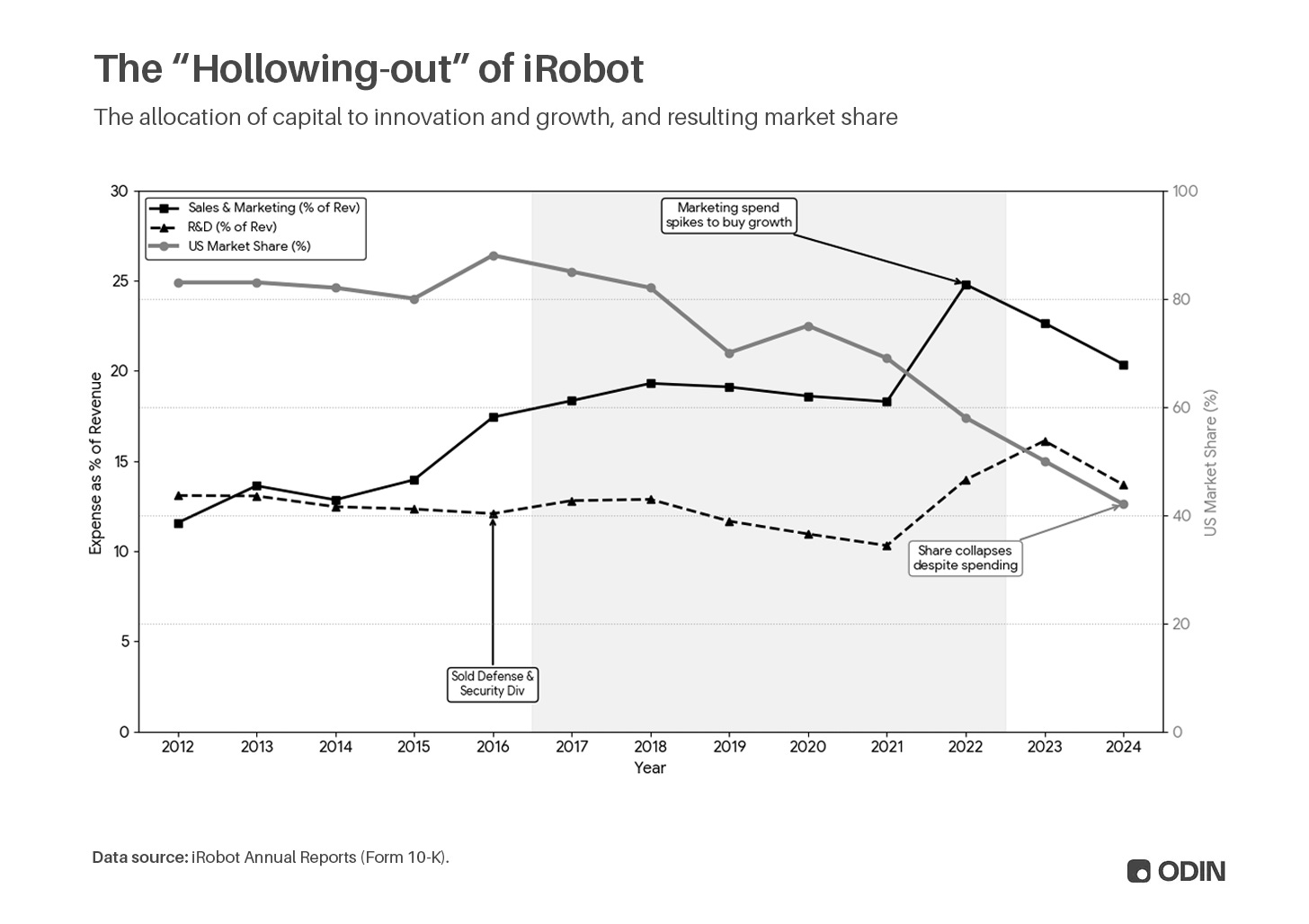

Throughout the 2010s, iRobot shed fixed assets (factories) and inventory risk by outsourcing production, reducing the capital denominator on its balance sheet, which boosted Return on Net Assets (RONA) and Return on Equity (ROE). At the same time, cutting R&D expenses increased free cash flow, which was used for stock buybacks rather than product innovation. Earnings Per Share (EPS) were artificially inflated, creating a positive feedback loop: stock prices rise → management compensation rises → continued buybacks.

In this process, iRobot rebranded itself as a "smart home" technology company to achieve more attractive valuation multiples (P/E, P/B, etc.), rather than being a less sexy "appliance" company. They hired large numbers of software developers while selling off their defense security business line and US manufacturing base. In the following years, maintaining competitiveness increasingly relied on sales and marketing expenses, rather than maintaining technological barriers.

This is the story of a cutting-edge robotics company funded by DARPA and incubated at MIT. It once disarmed IEDs in Afghanistan and participated in rescue operations after 9/11, only to transform into an overseas distribution business for robot vacuums. The outcome was unsurprising — when the company lost control over its products, its monopoly was eroded by more innovative competitors.

iRobot is just a microcosm of the systemic issues of financialization. Much of the economic growth of the past few decades looks beautiful on paper, but the reality is one of long-term stagnation and lackluster growth. The accomplishments in financial reports have been exaggerated (see Goodhart's Law), yet there has been no corresponding contribution to the actual prosperity and opportunities of ordinary people.

Debt leads to the center

"When a person is burdened with too much student debt or housing is too unaffordable, they will be in a long-term negative capital state, or find it difficult to start accumulating capital through property; and if a person has no chips in the capitalist system, they are likely to turn against it."

--Peter Thiel, Email to Mark Zuckerberg (2020)

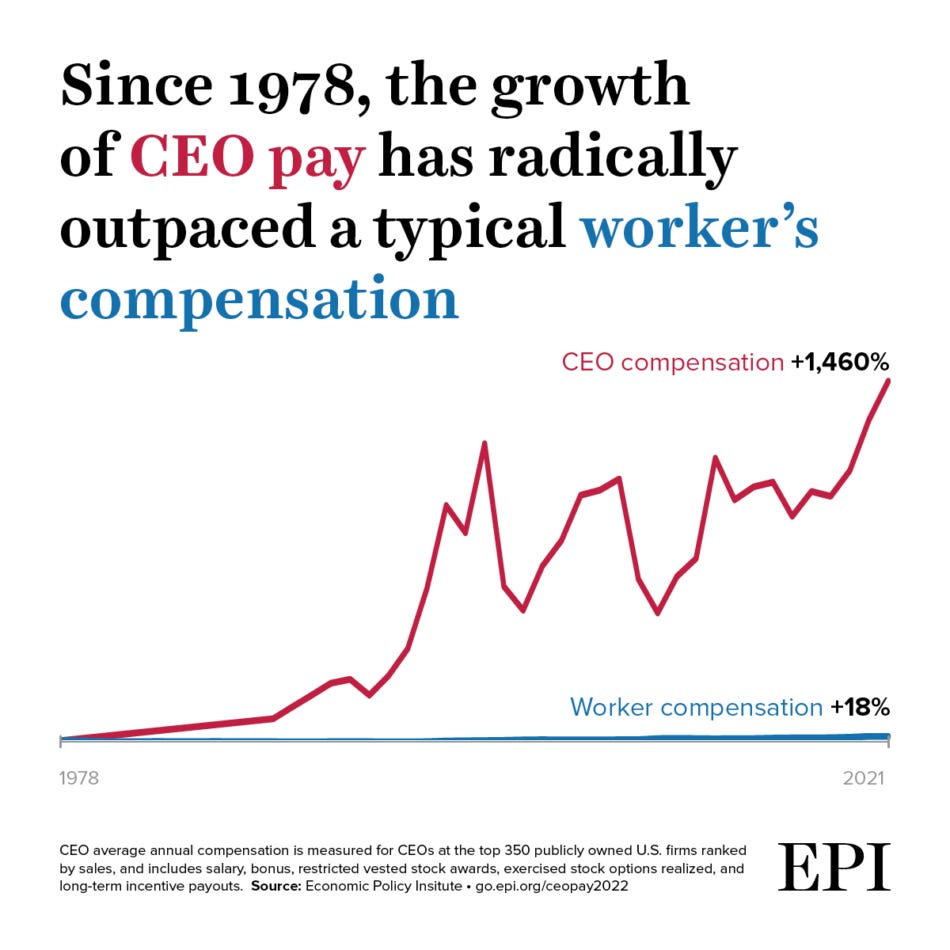

From an individual perspective, financialization limits opportunities for participating in wealth creation, as the economic upside is concentrated in the hands of capital holders. If companies are coerced to cut R&D, capital expenditures, and domestic jobs to optimize financial metrics, they become top-heavy. When this trend spreads throughout the economy, wages are depressed, and inequality increases.

Caption: Since 1978, CEO pay has soared 1460%, and in 2021, CEO pay was 399 times that of the average worker

Source:Economic Policy Institute

In an industrial economy, money is merely a liquidity unit that allows the system to operate more efficiently. It is a tool you can use to do important things, but it is not important in itself. Money has value because it can enable you to live in a good house, drive a nice car, and live comfortably. Your core economic role is to produce and consume goods and services, driving the "invisible hand" that Adam Smith described to create prosperity, from which you also benefit.

"The relationship between money and real wealth (i.e., actual goods and services) is like that between words and the physical world. Words are not the physical world itself; money is not wealth; it merely serves as a record of available economic energy."

--Alan Watts, writer and philosopher (1968)

In a financialized economy, the unequal distribution of opportunities is subsidized by financial products. You take out a loan to buy a house that you actually cannot afford, lease a car, and use credit cards for vacation spending. Trading stocks or buying cryptocurrencies makes everything seem fine — maybe you can turn your luck around through speculation and escape your permanent lower-class identity. Your core economic role transforms into a debt to the center, while the whole system is designed to keep you trapped there.

"Banks are using increasingly sophisticated models to predict which customers will borrow more money after their limits are raised. For many, this means an automatic increase that they never asked for and may not fully understand. These decisions are shaping nationwide household debt in ways most borrowers cannot see."

--Dr. Agnes Kovacs, Senior Lecturer in Economics at King's Business School

The Gambling Gene

"Buying a lottery ticket is the only time in our lives we can grasp a specific dream — to get those good things that you already have and take for granted."

--Morgan Housel, "The Psychology of Money" (2020)

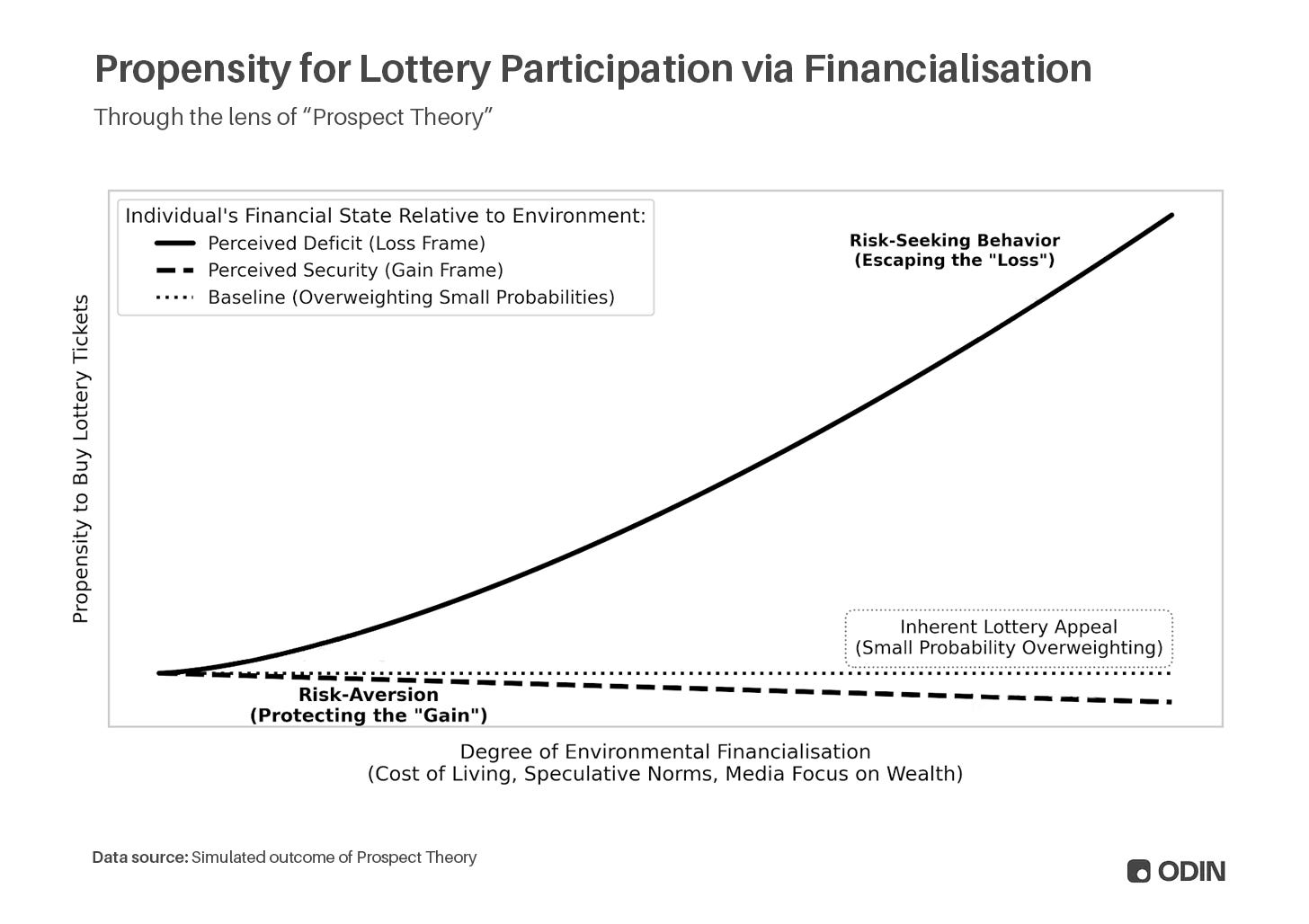

In times of economic pressure, financialization has evolved a set of means that exploit human cognitive biases. We tend to overestimate the low-probability of extreme returns, which economists Daniel Kahneman and Amos Tversky refer to as prospect theory:

"When people assess outcomes that are merely 'possible,' they underestimate their weighting, while over-weighting certain outcomes. This tendency is called the certainty effect and leads people to avoid risks when facing certain gains while seeking risk when facing certain losses."

For example, if you are chasing wealth, you are more likely to borrow money to buy lottery tickets because we cognitively assign higher weight to that extreme (and unlikely) return while underestimating that small (and certain) cost. Conversely, a wealthy person would prioritize loss avoidance and is therefore less likely to buy a ticket they can fully afford.

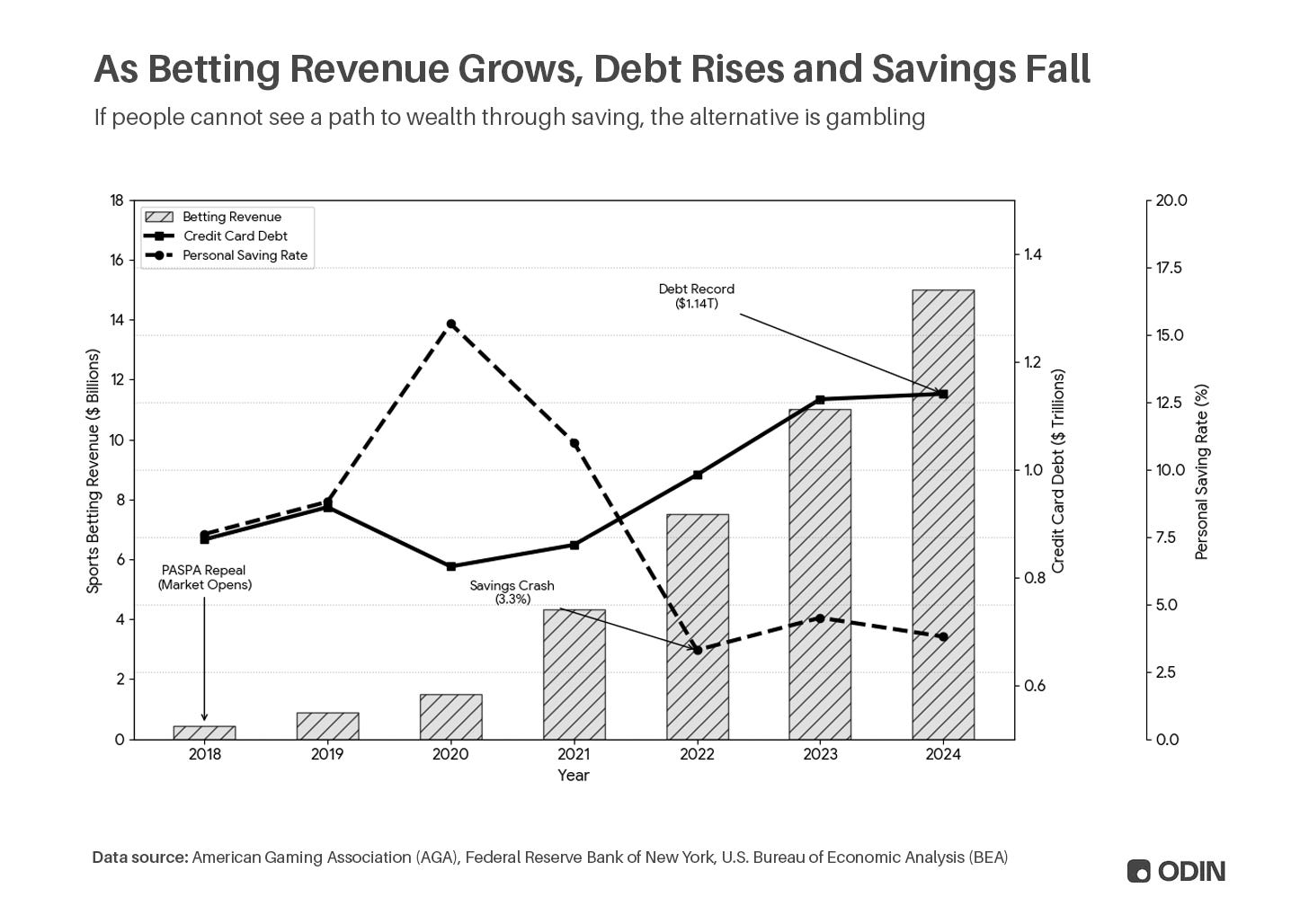

The result of deepening financialization over the past fifteen years is a behavioral shift from saving to debt and gambling. Sports betting revenue in the US skyrocketed from $400 million in 2018 to $13.8 billion in 2024, while credit card debt increased from $870 billion to $1.14 trillion during the same period.

This behavior obscures many ailments of the economy — goods purchased with debt still statistically count as consumption, while gambling shows up in statistics as service consumption.

When this mentality spreads in the economy, "gamblification" accelerates. Whether it’s sports betting, meme stocks, altcoins, gamified brokerage platforms, or the crazy拆游戏战利品箱 and Pokémon card packs, social media is filled with people rolling dice and taking chances to chase wealth.

Perhaps even more concerning is the audience scale that such content attracts — abstracted one layer further, where audiences experience vicarious thrill through performers. This content is pulling a new generation of young people into an environment where gambling is fully normalized and even glorified.

"Although loot box-related activities can predict the frequency of participation in monetary gambling (opening free boxes, paid openings, and selling loot), the influence of other activities is greater. More specifically, all tested monetary gambling indicators can be significantly predicted by watching gambling livestreams — or videos that include gambling behavior."

Of course, the house always wins. Whether it's harvesting order flow data, charging fees, or the negative expected values of gambling itself, existing capital holders always outperform individuals who must meet liquidity demands in shorter and more unpredictable timeframes.

Finance Devouring Innovation

Since 2011, the theme of Silicon Valley has been "software is eating the world." A more accurate statement might be "finance is eating the world." Despite its reputation for rebellion and independence, venture capital unfortunately exhibits all the flaws of financialization and similarly prefers accumulation.

In the low interest rate era, software provided VCs with a tool: to convert venture funds into inflated asset values and management fee income. Loss-making enterprises were massively scaled up by large losses, then justified for subsequent financing through multiple markings. Capital chasing capital creates an inflationary cycle, and the "best" deals become those most likely to attract more investment. Similar to stock buybacks, this creates fragile market leaders with inflated valuations.

This cycle of financial engineering died with the end of the low interest rate environment in 2022, while the subsequent corrections washed away massive "paper" accumulations. The market is still digesting the hangover, with liquidity collapses affecting subsequent funds' fundraising performance (mainly concentrated in marginal markets and "out-of-the-box" managers).

But the problem has not disappeared. Fund managers are also not immune to the impact of prospect theory; the metaphor of "buying a lottery ticket" corresponds very accurately to current investment behavior: When top firms dominate through accumulation, the general response is to significantly overpay for any project that might yield extreme returns. The "power law" now shapes entry logic more than exit explanations — investors are all rushing toward the endgame.

Even worse are investments that exploit the behavioral patterns solidified by long-term financialization. You can bet the bill, gamble against insiders in prediction markets, or try your luck in loosely regulated crypto casinos. Thus, the despair of late-stage financialization leads us into a "financialization squared" — where investors look for scalable business models and print paper gains by exploiting the economic stagnation caused by financialization.

Caption:Augustus Doricko, founder of Rainmaker, a true industrialist

Ultimately, investors must take responsibility for their choices. You can continue to glide along the inertia of financialization, investing in those products supporting financialization right to the end. Or, you can become part of the correction, supporting those companies that bring long-term prosperity through industrialization.

Obstacles are the Way

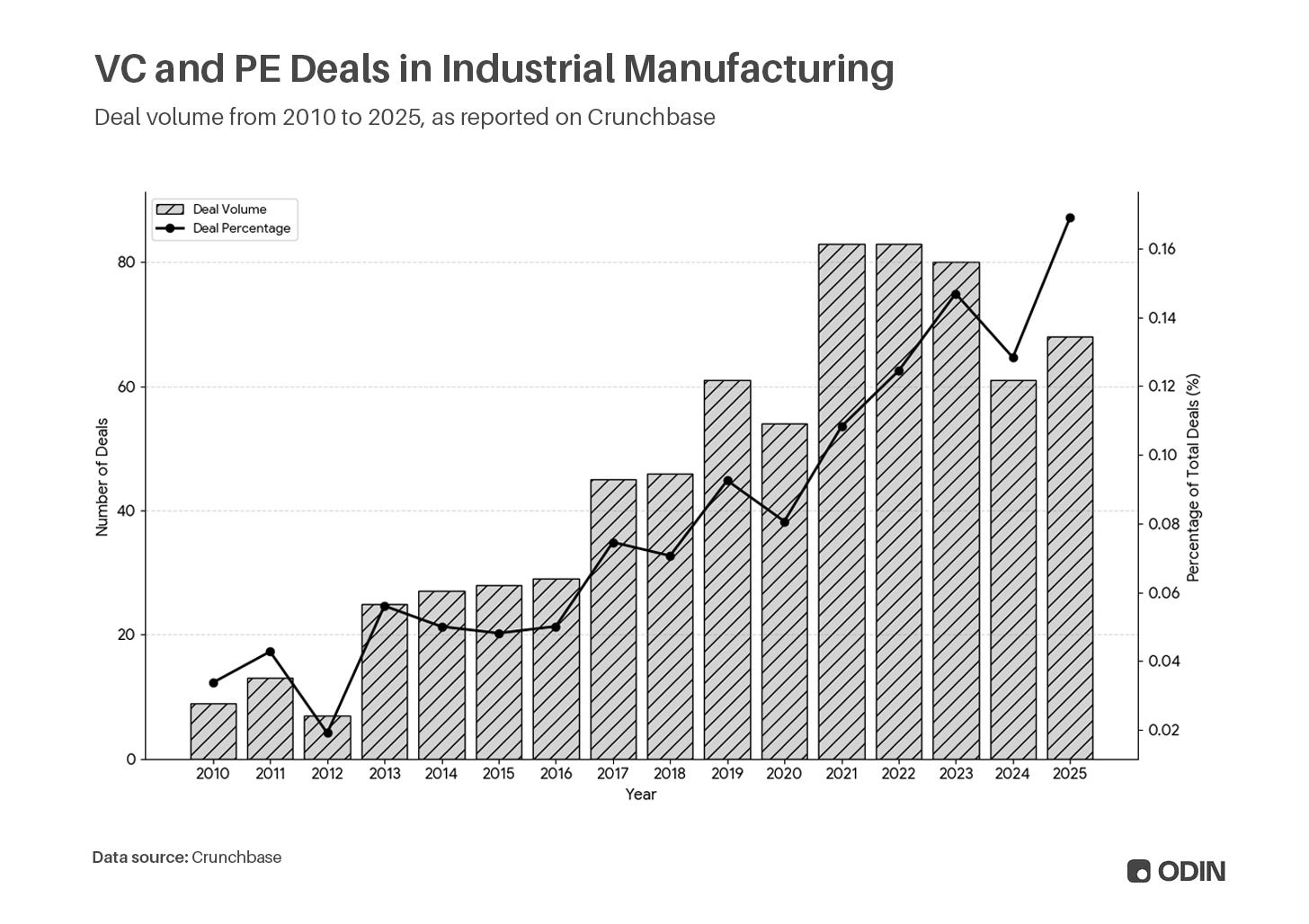

Despite disincentives (slower growth, lower valuation multiples), activity in fields like industrial manufacturing is still steadily rising.

Whether this signals a return of the industrial cycle or merely reflects an increasing awareness among people that the status quo is unsustainable — remains unclear. But one thing is certain: as more capital concentrates in fewer investors' hands, then flows into fewer companies, more investors and builders feel increasingly irrelevant within the current system.

Something will ultimately snap.

"But this time, things are different. In the current ICT revolution, we seem stuck in the installation period, or what I call the 'turning point' — an intermediate period of recession and uncertainty, rebellion and populism, exposing the pain caused by the initial 'creative destruction' process on society. It is precisely when the system is in danger, questioned, and attacked, that politicians finally understand they must establish a win-win game between business and society."

--Carlota Perez, "Why is the Installation Period of ICT So Long?”

As Perez describes, turning points are often driven by government action. Although the current US government has made some progress in industrial policy, trends in deregulation continue. Therefore, this may be the first time in history that the industrial economy quietly grows parallel to the financial economy, with both competing for capital and talent.

Don't get it twisted, industrialization is the harder path. Fund managers face skepticism from LP and less alluring short-term gains. But over the long term, these "hard tech" and "deep tech" companies possess lasting moats and compounding value, performing better than those in hotter spaces. More importantly, they directly and positively impact prosperity by solving real problems.

"Re-industrialization" is the shared call of technologists who recognize that the future has been betrayed.

It encompasses new uranium enrichment plants in the nuclear renaissance, ocean robotics startups addressing critical food supply chain issues, and specialized AI labs focused on drug discovery in the AlphaFold era.

None of these projects benefit from financialization. They do not easily fit into the metrics and ratios that achieve money printing in private markets. But they will restore genuine productivity to the economy.

The Age of Industrialists

"The creation of money and credit and the creation of wealth (actual goods and services) are often confused, but it is the greatest driver of economic cycles."

--Ray Dalio, founder of Bridgewater Associates

In the stability period after the post-prosperity era, financialization has become a lazy default — an extraction mechanism, as well as a driver of stagnation. Ultimately, it is self-serving, zero-sum, and increasingly liable to collapse under systemic shocks, washing away both hope of accumulation and turnaround.

Hope that capital is ready to re-embrace "hard problems." The hallmark of this phase of the cycle is the great industrialists, especially those pioneering in frontier fields. The key is that they are idealists, possessing visions that transcend shallow financial incentives. They will place enduring competitive strength ahead of fragile capital barriers and long-term legacy ahead of short-term position games. Finance will serve their needs, not the other way around.

Meanwhile, the return of Adam Smith’s "invisible hand" will show no mercy to those still dressing up distorted metrics in watered-down projects favored by investors.

(Thanks to Yifat Aran, Alex LaBossiere, Laurel Kilgour, and Aaron Slodov for their feedback during the draft phase.)

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。