Authors: Cosmo Jiang & Sam Lehman

Translation: Deep Tide TechFlow

Deep Tide Introduction: The partners at Pantera Capital present a clear argument in this article: AI Agents do not require blockchain in the initial stages of automation, but once it reaches the stage of fully autonomous transactions between Agents, traditional financial systems will completely fail.

This is not a general narrative but provides concrete arguments from the dimensions of identity, payment, and trust. For readers wanting to understand why the narrative of "AI + crypto" holds, this article is worth reading thoroughly.

The full text is as follows:

February 27, 2026 | Cosmo Jiang, Sam Lehman

The viral rise of OpenClaw (formerly Clawdbot) marks a generational leap in autonomy. When these AI Agents begin to interact with each other—negotiating and trading in some cases—the future of Agentification turns from science fiction into reality.

OpenClaw is just the starting point of an accelerated journey. Trillions of dollars are flowing into the AI field. In the United States alone, AI spending by major cloud providers is expected to exceed $650 billion by 2026, approximately ten times the inflation-adjusted cost of the Apollo program.

Starting from simple chatbots, AI systems are rapidly evolving into fully autonomous Agents. These AI Agents are not just content generators; they are becoming economic entities capable of reasoning, acting, trading, debating, coordinating, and doing so without real-time human supervision. The impact of this transformation will be ubiquitous, but the business sector may be the most profound.

Estimates suggest that by 2030, the global consumer commercial scale involving AI Agents will reach $3 to $5 trillion. Even if only 10% evolves into programmatic trading between Agents, the annual machine-native settlement volume will reach hundreds of billions of dollars.

This naturally raises a question: What kind of financial and coordination infrastructure is truly suitable for AI Agent-native commerce?

Today's commerce is designed for humans, involving identity verification, banking intermediaries, legal contracts, settlement cycles, and human oversight. Autonomous software cannot walk into a bank to open an account, cannot sign documents in a legal sense, and cannot wait several days for ACH transfers to arrive. The infrastructure needed by Agents must be programmable, always online, globally accessible, permissionless, and verifiable by machines by default.

Blockchain can meet these constraints, and we are already seeing this dynamic unfold.

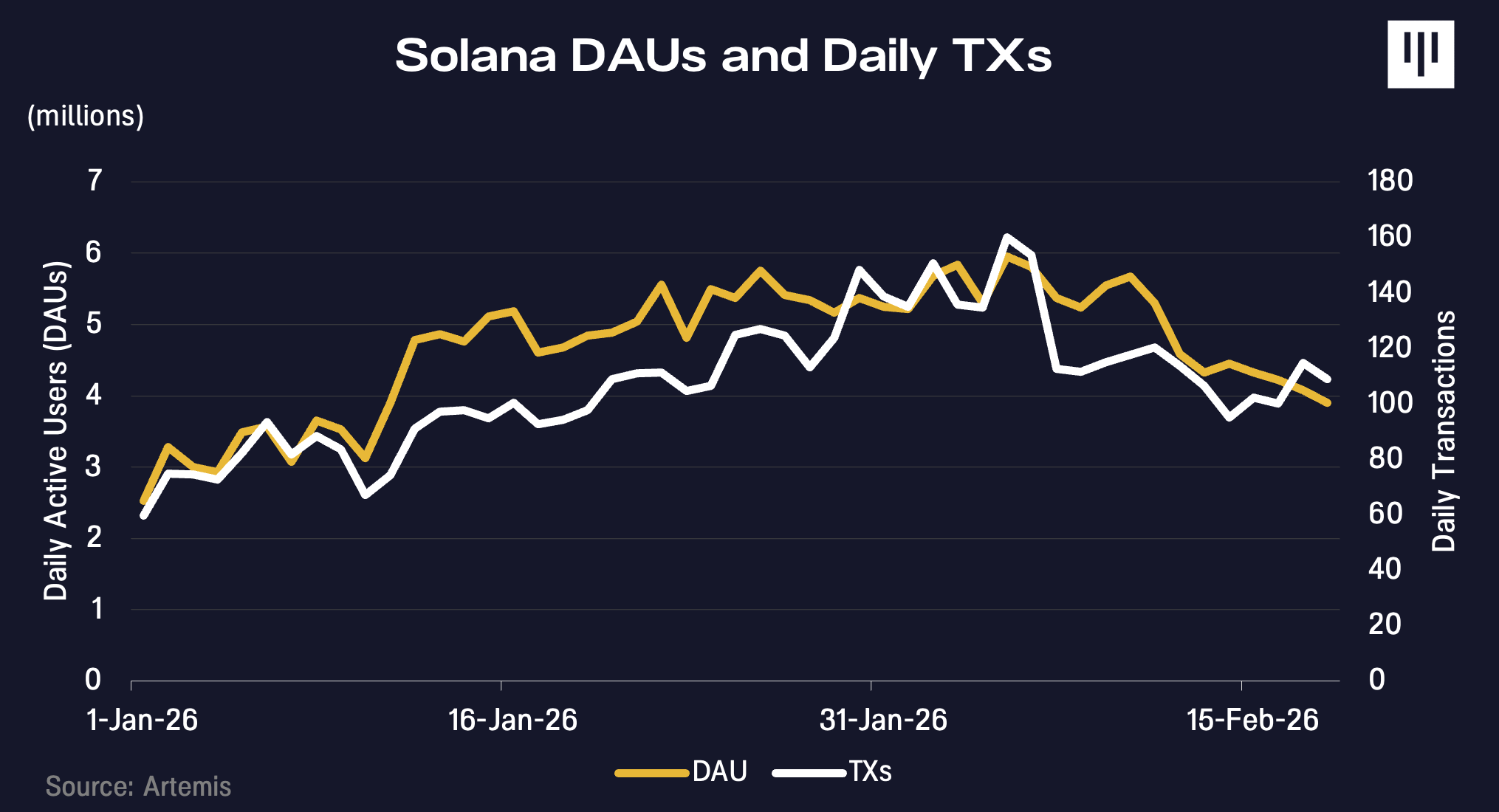

During the same period that OpenClaw went viral in January, Solana's transaction volume and active addresses also began to rise. Evidence from its AI Agent social network Moltbook indicates that Agent activity may be one of the contributing factors to this growth.

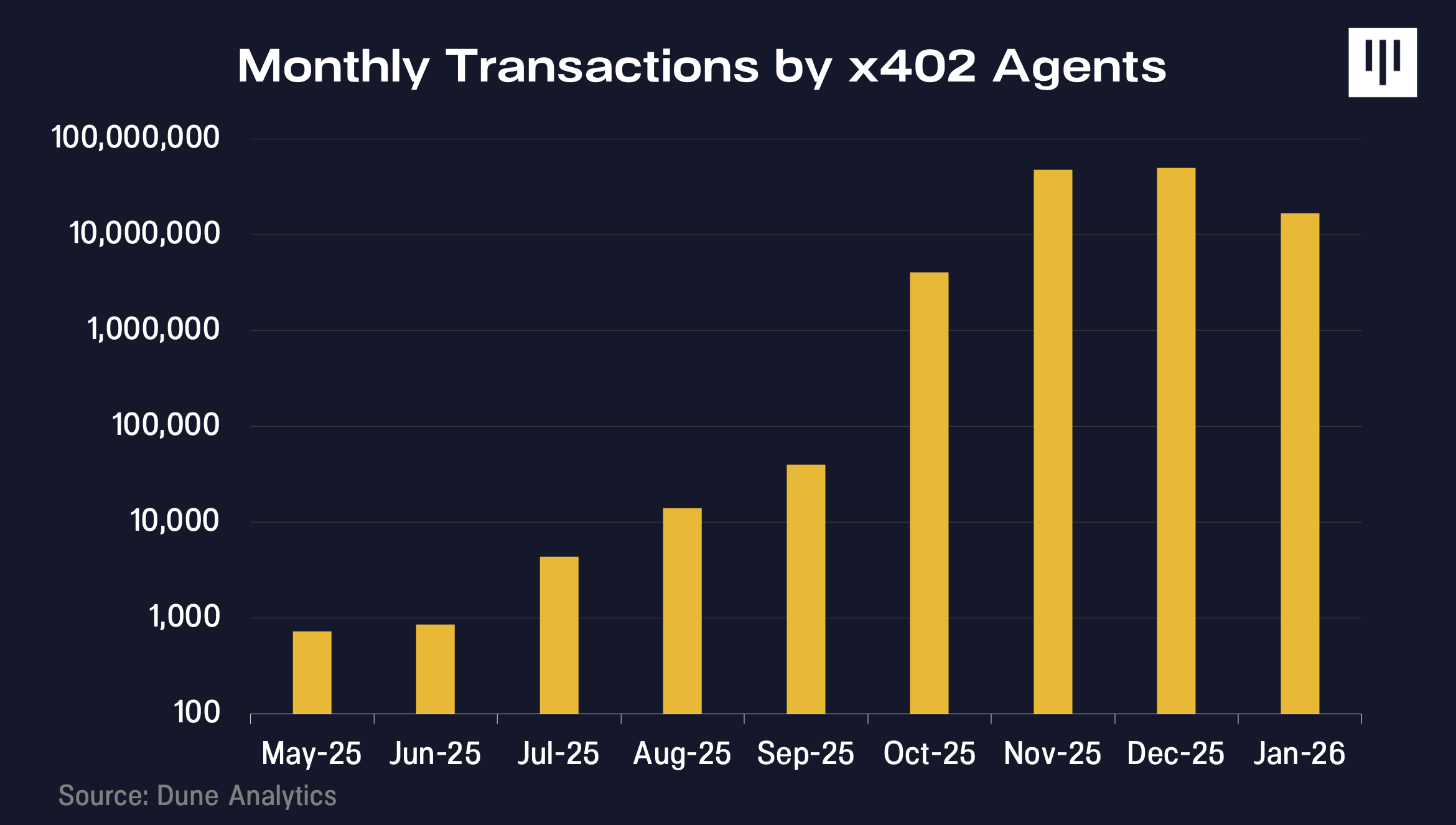

x402 is an internet-native payment protocol developed by Coinbase that allows AI Agents to make real-time payments for digital assets without needing accounts or complicated high-friction authentication processes. Since its launch in 2025, its transaction volume has continued to accelerate.

We are still in the early stages, and today's examples are more directional than definitive. But if investors are excited about the potential of AI innovations, they should not overlook why we believe that the blockchain infrastructure will be the foundation for unlocking a fully autonomous Agent world.

Many will rightly point out that today’s AI Agents do not need blockchain. This is indeed the case in the short term, but we believe this is a shortsighted view.

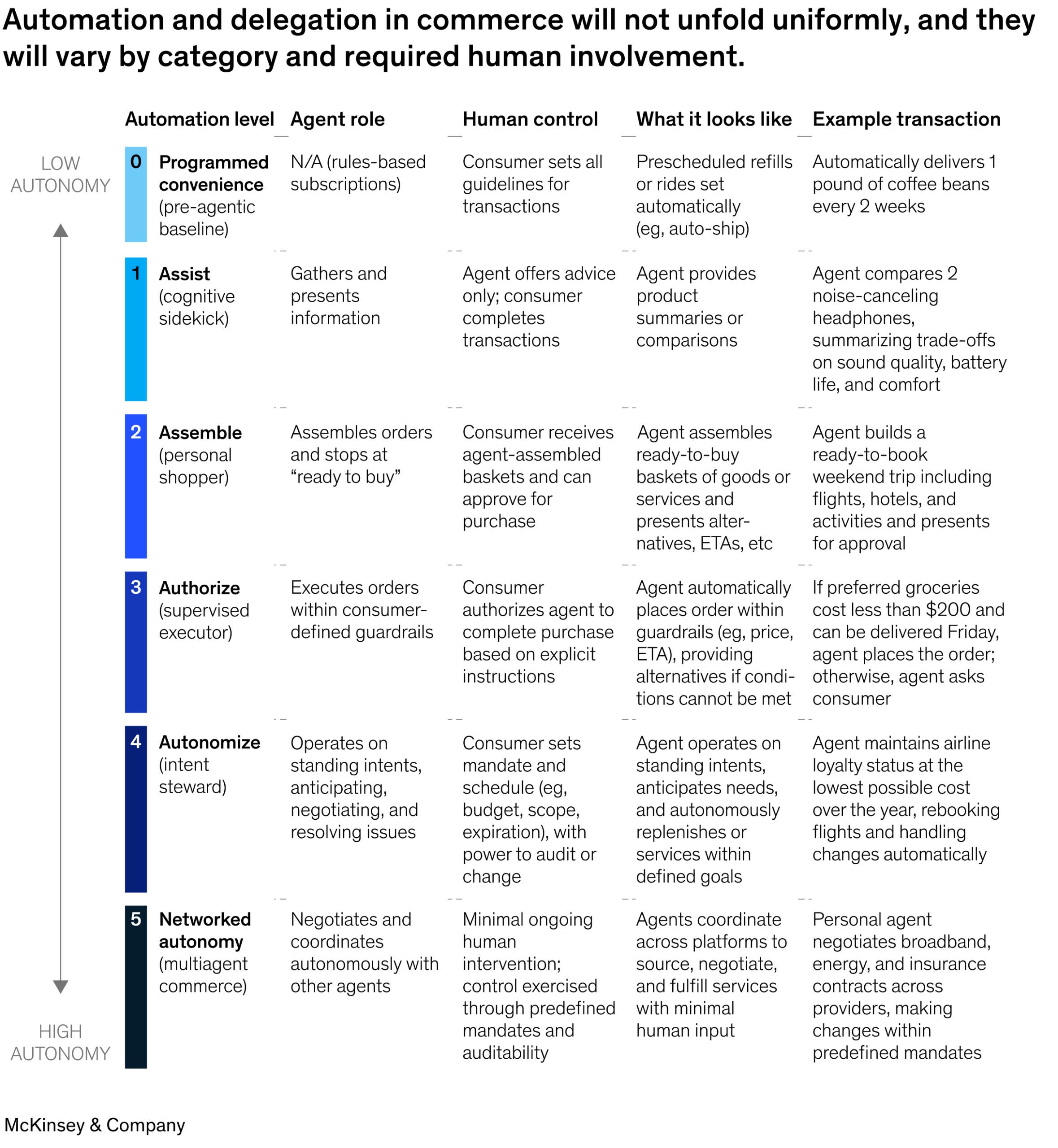

McKinsey recently released a framework that divides the degree of automation driven by AI in business into six levels: from basic subscription assistants (Level 0) to fully autonomous Agent-to-Agent commerce (Level 5). The core insight is that Levels 0 to 4 do not require new financial tracks. In every case, there is a human identity behind the transactions. Users have already been authenticated on ChatGPT, Amazon, or Perplexity, binding their credit cards. When Agents trade, they are acting on behalf of that human, inheriting their identity, payment credentials, and legal status.

The infrastructure for this type of business—shared payment tokens, chargeback systems, fraud detection infrastructure—already exists and operates quite well through Visa or Stripe.

The blockchain infrastructure becomes critical only at Level 5 and above: when Agents trade directly with other Agents without human instructions; when there is no human identity to inherit; when payments must be programmatic, conditional, and settled in milliseconds; and when Agents need cross-platform portable reputations.

As long as humans are still financially responsible, traditional tracks are sufficient. Once Agents become independent economic entities, the constraints will change completely.

To understand where value accumulates and why blockchain is important, we must envision the logical end state of Agent AI. We are moving towards a world where Agents are not just assistants to humans but independent economic entities. Some created by companies or individuals, others generated by Agents themselves, forming increasingly autonomous systems capable of reasoning, allocating capital, and trading without real-time human supervision.

Without human-specified trading channels (such as going to the bank, using Stripe, or opening a blockchain wallet), Agents will rationally choose those tracks that are the fastest, most reliable, globally accessible, and have the least friction and dependency. When the alternative is to open a bank account, wait for ACH settlements during limited banking hours, Agents will naturally choose permissionless, always-on blockchain tracks.

We believe there are three core constraints that will drive Agents towards blockchain tracks:

Identity and Access: How to track the unique identity of AI entities transacting with each other and registering services? What should a new reputation system look like when traditional credit scoring and fraud detection systems are built for humans with a physical footprint operating within a jurisdiction?

Currency and Payment: What form of currency is needed when Agents are executing countless micropayments, performing conditional payments, and significantly increasing cross-jurisdictional commercial demands? What form of accounts is needed when Agents cannot walk into a bank to open an account?

Minimizing Trust in Transactions: How do AI Agents avoid friction from disputes that require human arbitration or other forms of centralized trust—those systems they may be unable or unwilling to access?

Identity and Access

Before making payments, the counterpart must know who it is dealing with— or what it is dealing with.

Traditional identity systems are designed for humans. They rely on government IDs, physical signatures, and other credentials, defaulting to the notion that the other end is a legal person.

Autonomous AI Agents do not have these. They cannot walk into a bank to open an account or legally sign contracts. However, if we want Agents to conduct transactions autonomously, they need some way to prove they are legitimate and authorized to act.

If you connect an Agent to your bank account, the problems multiply. How do you conduct anti-money laundering checks on software? If the Agent acts autonomously, who bears the responsibility? What if it is manipulated?

In simple scenarios, Agents can inherit the credentials of their owners (such as ChatGPT Checkout). But this model does not scale. Multiple Agents require separable permissions and consumption limits. Issues must be isolatable without freezing all Agents. These scenarios require Agents to have their own verifiable identity instead of borrowing from human identities.

This is where blockchain-based identity comes into play. Through cryptographic techniques, Agents can prove they are authorized to act on behalf of specific individuals or companies without disclosing sensitive information about the parties involved. You can think of it as a digital power of attorney that anyone can instantly verify anywhere without contacting a lawyer or querying a database.

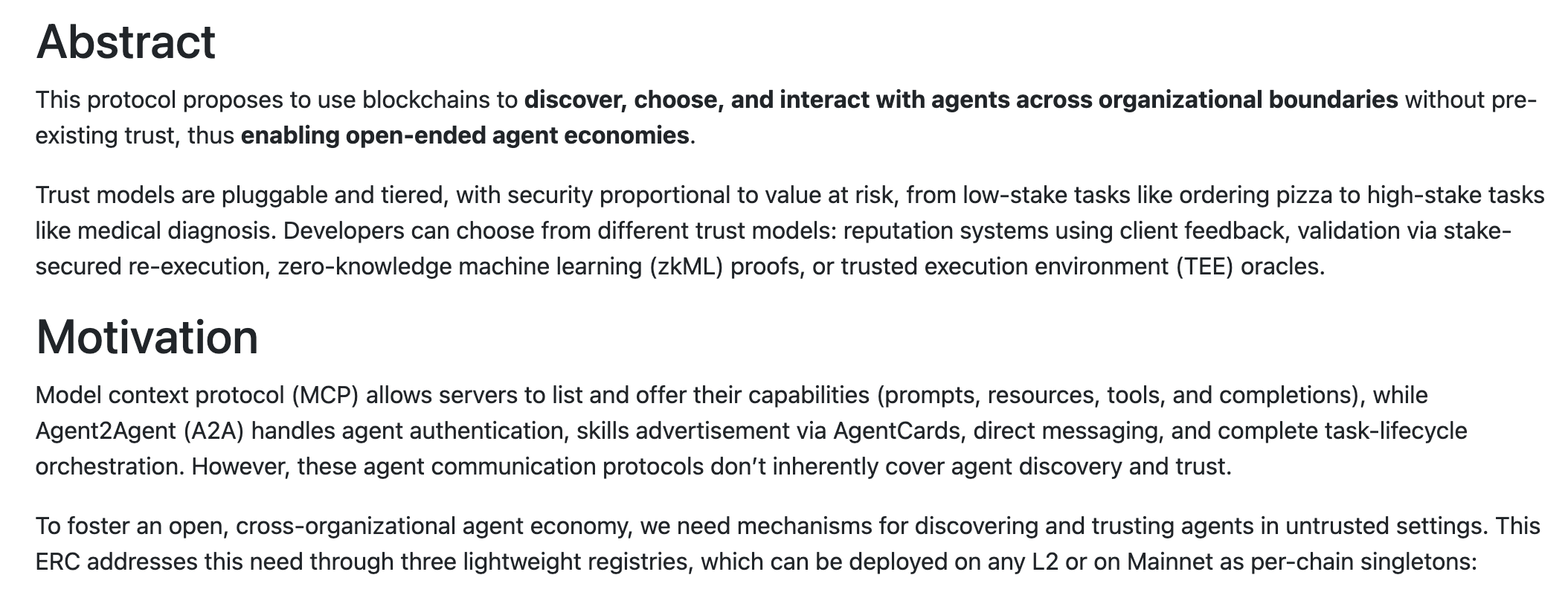

Emerging standards like Ethereum's ERC-8004 propose on-chain registries where Agents can establish verifiable credentials and accumulate transaction history and reputation over time. An Agent that has successfully completed thousands of undisputed transactions will form a meaningful difference from a brand new Agent with no history— and this reputation is cross-platform portable.

This is important because trust is the premise of business. Merchants have spent years establishing systems to shield against bots and crawlers. In an Agent-driven economy, they now need to figure out how to whitelist the right bots. Cryptographically secure and verifiable identities allow merchants to establish trust without human guarantees.

Programmable Currency and Micropayments

Traditional payment tracks are designed for human-scale transactions. When you pay for a cup of coffee or a pair of jeans, the credit card fees (usually 2-3% plus about 30 cents per transaction) are negligible.

But Agent-to-Agent commercial operations occur on a completely different scale. An Agent writing code might initiate 10,000 API calls within a single task. An Agent comparing prices may query hundreds of data providers. Payments need to be completed in milliseconds, repeatedly, with amounts counted in fractions of a cent.

Credit card networks are not optimized for this behavior. Minimum fees make micropayments economically unfeasible. Fraud systems will freeze accounts presenting high-frequency machine behavior. The speed of transactions is drastically lower compared to high-performance blockchain protocols.

Stablecoins and programmable currencies become truly useful here. On-chain transactions can be subdivided into extremely small units, with settlement costs approaching a fraction of a cent. More importantly, because payments are programmable, they can be conditional: pay X only when the API returns valid data; release funds only when the computation task is completed; pay in real-time as services are consumed rather than prepaying an amount you might not fully utilize.

Programmability also enhances capital efficiency. Today, you typically need to pre-fund Agents to access new services, need to estimate usage, and lock in capital upfront. With smart contracts and on-chain collateral, Agents can prove their creditworthiness before service delivery without transferring payments.

Blockchain provides financial infrastructure that aligns with how Agents operate: autonomous, high-frequency, conditional, and capital efficient.

Minimizing Trust in Transactions

Traditional businesses embed trust in intermediary institutions. Payment processors manage chargebacks. Banks provide settlement guarantees. Courts adjudicate disputes. Contracts ultimately rely on human legal systems for enforcement.

When billions of low-value transactions occur across multiple jurisdictions, this framework becomes inefficient. An AI Agent trading with another AI Agent may not have access to the legal systems of a specific jurisdiction and may not choose to rely on them. Cross-border enforcement can be slow, expensive, and uncertain in outcome.

Blockchain reduces reliance on these unreliable trust systems by using smart contracts to directly encode execution logic. For example, smart contracts allow funds to be programmatically escrowed and only released when preset conditions are met. Settlement is deterministic and unaffected by chargeback risks. The rules are transparent and verifiable in advance for both parties. There is no reliance on legal remedies.

For autonomously operating Agents at scale, reducing dependence on centralized intermediaries and human arbitration lowers friction, enhances predictability, and enables business to scale programmatically. This lower-friction infrastructure could expand the boundaries of economic activity that are uneconomical under traditional enforcement models. Agent commerce supported by blockchain tracks has the potential to accelerate global GDP growth.

The question is not whether Agent commerce will come, but on what infrastructure it will operate.

As AI Agents become independent economic entities, the number of economic entities in the global economy will grow exponentially. Agents will need digitally native financial tracks—a stack of technologies capable of handling programmatic settlements, high-frequency micropayments, permissionless coordination, and minimizing trust identity systems. These principles are the fundamental starting points for blockchain design.

We believe it is reasonable to say: The rapid proliferation of AI Agents is a powerful long-term tailwind for blockchain activities. Initial evidence already exists, and we believe that most investors have underestimated the value creation opportunities it entails.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。