Author: CryptoSlate / Oluwapelumi Adejumo

Translation by: Shenchao TechFlow

Senchao Guide: The core narrative of the executive order by Trump establishing the strategic Bitcoin reserve is facing a legal loophole that has been little discussed: Approximately 30% of the Bitcoins in the reserve are related to the 2016 Bitfinex hack, and if the court rules to return them to the victims, the reserve size will immediately shrink. This article clarifies the essential differences between the reserve number and the available number from the perspective of legal property structure, as well as how the LEO token acts as a market agent in this legal game.

The full text is as follows:

The U.S. strategic Bitcoin reserve may lose nearly 30% of its holdings due to a legal ruling, even if the government does not sell a single coin.

Last year, President Trump signed an executive order establishing the strategic Bitcoin reserve. The order required the Treasury to consolidate the BTC held by the government into a reserve account and promised that the U.S. would not sell these Bitcoins.

However, the reserve's balance number may overestimate the amount of BTC that the government can actually consider as permanent strategic assets.

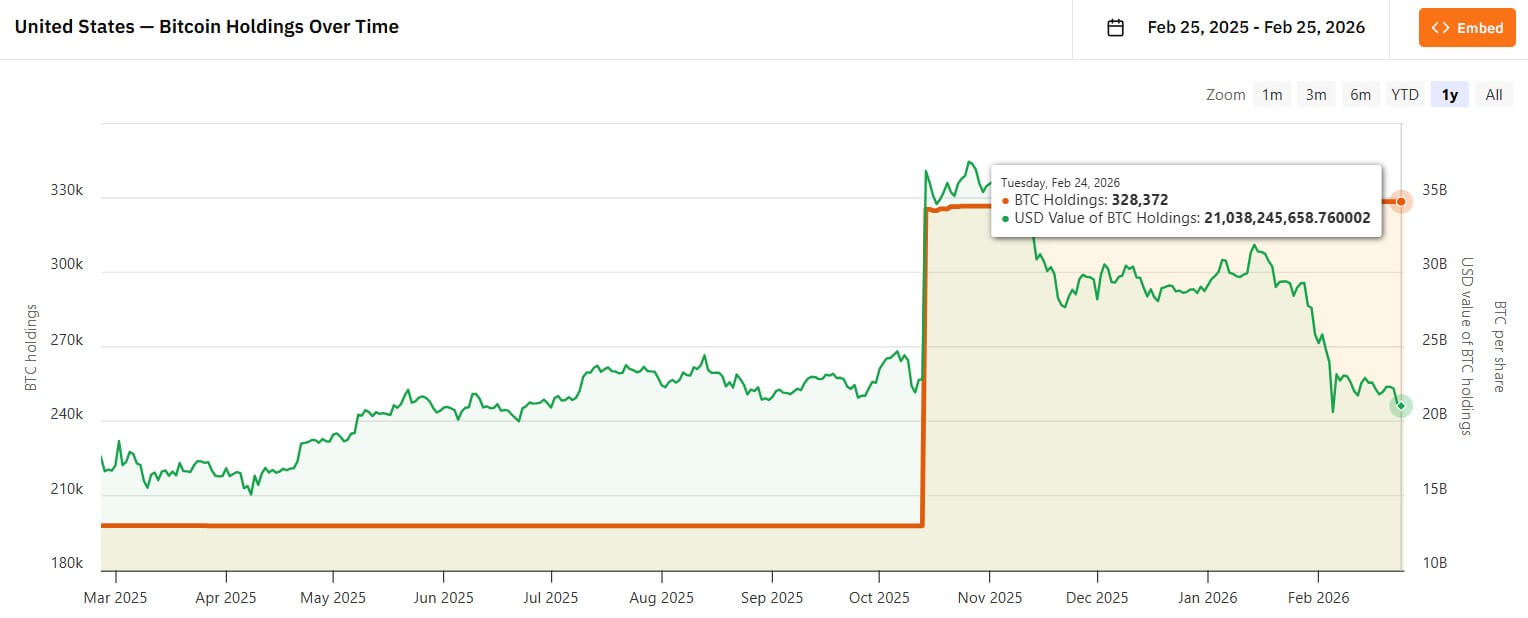

Bitcoin Treasuries data shows that the U.S. government controls approximately 328,372 BTC, making it the largest known national-level Bitcoin holder in the world. Based on the current Bitcoin price of about $65,842, this batch of assets is valued at approximately $21.6 billion.

However, the problem is that a large portion of this BTC, while held by the government, does not cleanly and strategically belong to the government.

The executive order explicitly allows for disposal of assets based on "court orders with jurisdiction" and sets an exemption for assets that "should be returned to identifiable and verifiable crime victims."

This exemption is crucial because about 94,643 BTC (around 30% of the government's holdings) are linked to the 2016 Bitfinex hacking incident.

If these Bitcoins are returned as compensation, the reserve number will mechanically drop to approximately 234,000 BTC.

The reserve number is real, but property rights issues remain unresolved

The strategic Bitcoin reserve is often discussed as if it were a clean sovereign asset balance sheet. In reality, it is a hybrid of legal and accounting levels.

Some BTC under the government's name have been completely confiscated and clearly belong to the U.S. But another part still involves criminal cases, compensation claims, or procedural steps that may take years to complete.

This gap has now become the core of the debate surrounding the U.S. reserves.

The 94,643 BTC related to Bitfinex is the most typical example. These coins appear in custodial accounts related to the government and are counted in market statistics.

But if the court rules that these coins should be returned to the victims, they were never considered as permanent strategic reserve assets from the start.

This is where the two voices of public opinion might miss the core issue.

The bullish version exaggerates the permanence of the reserves, as it sees all government-controlled Bitcoins as permanent strategic assets. The bearish version inflates market impact because it equates compensation transfers with sovereign sell-offs.

This legal distinction is of significant importance for prices, market sentiment, and how investors interpret the strategic Bitcoin reserves.

Why the Bitfinex-linked Bitcoins remain frozen

In August 2016, Bitfinex was hacked for 119,754 BTC, which remains one of the largest Bitcoin thefts in crypto history.

In February 2022, U.S. authorities recovered about 94,643 BTC linked to the hack, and this recovery garnered significant attention due to its scale and timing.

The next issue remains compensation.

In January 2025, prosecutors requested federal court approval to return the recovered assets to Bitfinex in the form of "physical compensation," meaning directly returning Bitcoins instead of selling them first for dollars.

This distinction is crucial for market structure.

The government's sale or auction would create a visible supply event, with timing and scale known in advance. Physical returns would instead shift the next decision-making to the recipient, which could be Bitfinex, its former users, or both depending on how the court rules on competitive claims.

The U.S. confiscation process is inherently designed to slow down this stage. Third parties claiming rights to confiscated property can file applications in ancillary proceedings. In the Bitfinex case, this process has become a core battle.

Some customers believe that the stolen assets individually belong to them. However, Bitfinex claims that the company ultimately bore the economic loss after socializing the losses and compensating users through internal mechanisms.

The significance of this ruling therefore extends far beyond the case itself, potentially influencing how compensation is handled in future exchange hacking incidents.

Until the court rules on these claims or the parties reach a settlement, these Bitcoins remain effectively frozen.

That is why the reserve numbers appear stable on-chain, but the legal aspects remain filled with uncertainties.

LEO is acting as a market agent for the court ruling outcome

The legal process is still slow, but traders are attempting to price the outcome using UNUS SED LEO (LEO) — the exchange token of Bitfinex and iFinex.

Bitfinex has stated that once the recovered BTC are returned, 80% of net funds will be used for repurchasing and destroying LEO tokens within 18 months.

The company noted that this process may include over-the-counter trades, such as directly exchanging BTC for LEO.

This policy effectively translates the federal court ruling into a huge repurchase pipeline, providing the market with a mechanism to speculate on the timeline before the legal ruling.

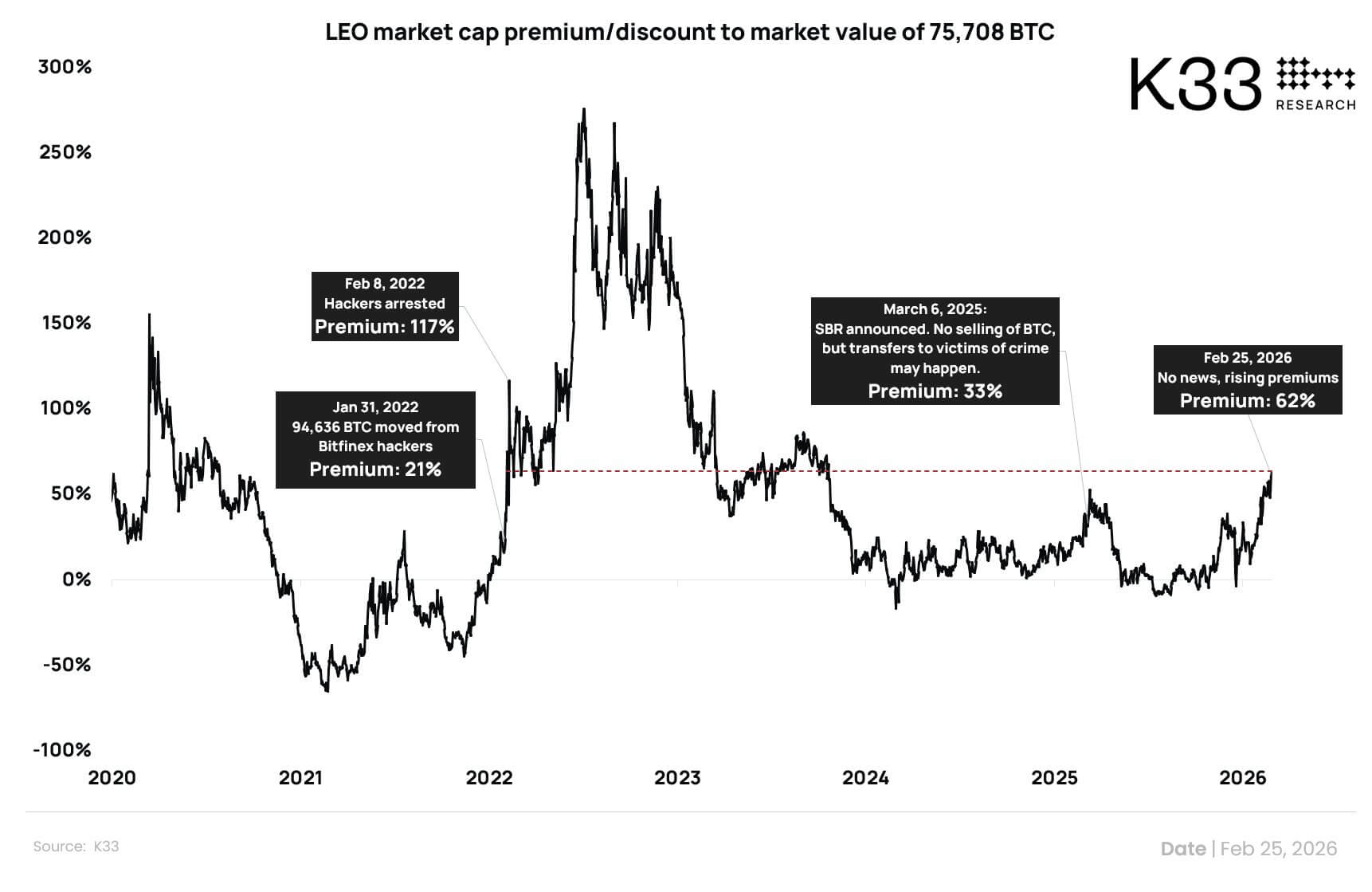

K33 Research director Vetle Lunde has modeled LEO based on two main value drivers: one is sustainable repurchases funded by Bitfinex trading income, and the other is expected future destruction linked to the reclaimed Bitcoins.

Using approximately 95,000 reclaimed BTC as a baseline, Lunde estimates that 80% of the allocation is approximately equal to 75,000 BTC. At current prices, this batch of funds is worth about $5 billion.

Meanwhile, he estimates that repurchases driven solely by trading income have a fair value of approximately $125 million.

However, trading this catalyst is highly volatile.

CoinMarketCap data shows that LEO has a market cap of about $8 billion, but the 24-hour trading volume is only $7.1 million. This low liquidity could severely amplify price volatility.

At the same time, a high market cap also means that LEO's current trading price has a premium of about 60% over its implied fair value.

This is the highest premium level since the prolonged high-premium phase following the first recovery announcement in 2022.

Lunde indicates that the current premium has a lot of noise because LEO's liquidity is extremely low and holdings are concentrated, allowing a few participants to significantly distort the market.

Therefore, traders may be preemptively positioning for a court transfer event or simply riding the wave in an environment where fair value takes a backseat.

Ultimately, LEO's low liquidity will amplify the final outcome. If the transfer is confirmed, valuations may be pushed higher in the short term. Conversely, if the scale of supply distribution is limited or delayed, premiums could be compressed quickly.

The shock from the headlines may far exceed the actual BTC liquidity impact

A broader market backdrop explains why this event may influence market sentiment even before the court ruling.

In early 2026, Bitcoin has been in a risk-off sell-off mode. The spot Bitcoin ETF has seen a net outflow of over $4.5 billion this year, with sustained outflows for 5 weeks.

In this environment, traders are highly sensitive to supply-related headlines, especially any news regarding the national holding of BTC.

As such, the headline "The U.S. transfers about 95,000 BTC" naturally has the energy to shake the market.

However, if this batch of coins leaves government custody, it is compensation, not a government sale.

If Bitfinex receives these Bitcoins and executes its stated repurchase and destruction plan, the corresponding BTC liquidity is likely to be processed in phases rather than dumped into the market all at once.

By rough calculations: about 75,000 BTC spread over 18 months amounts to approximately 139 per day.

This may impact LEO prices, but it does not constitute a significant supply shock compared to the larger-scale supply pressure from long-term holders and ETF outflows that Bitcoin has absorbed over the past five months.

Therefore, the real market impact may come from the narrative framework rather than the actual Bitcoin liquidity.

This is because the strategic Bitcoin reserve is not just a simple number of Bitcoin reserves; it is a political and market signal — traders can interpret it as bullish or bearish even when the legal status of these Bitcoins is still unclear.

This is why the framework of "The U.S. loses 30% of its Bitcoin reserves" is likely to trigger volatility: it is emotionally simple and powerful, suitable for headlines, but strips away the legal substance.

However, the legal substance is the real story.

The design of the strategic Bitcoin reserve is inherently aligned with compensation. If this portion of Bitcoins from Bitfinex leaves government custody, the tracked reserve number on the platform will decrease, and the market will react.

But the deeper reality will not change: the U.S. is not withdrawing from its reserve policy; it is acting in accordance with the law — and that is exactly what the reserve framework initially stated it would do.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。