Author: Nikka / WolfDAO (X: @10xWolfdao)

In the context of a continued correction in the cryptocurrency market at the beginning of 2026 (with BTC hovering around $89,000-$90,000 and ETH around $3,200), enterprise-level accumulation strategies have become one of the most important narratives in the market. This article will analyze the accumulation behaviors of two representative companies, Strategy (formerly MicroStrategy) and Bitmine Immersion Technologies, revealing their strategic differences, financial models, and multidimensional impacts on the market.

Part One: In-Depth Interpretation of Accumulation Behavior

1.1 Strategy (MSTR): Leveraged Belief Injection

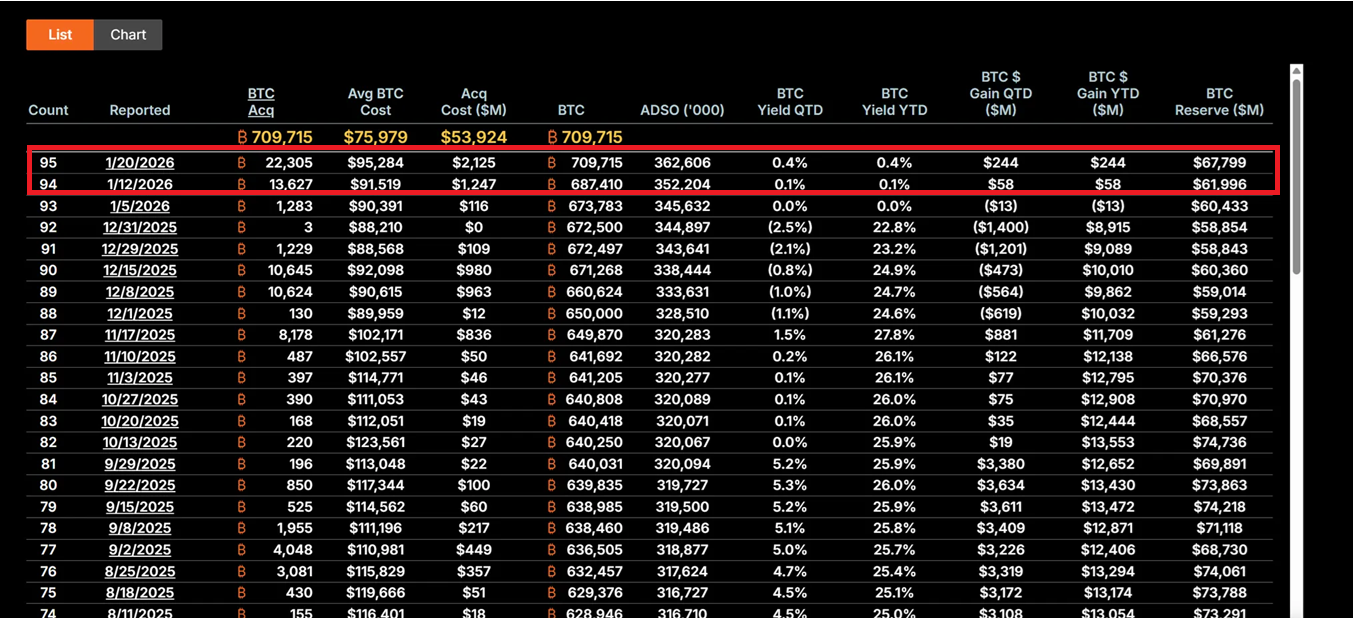

Under the leadership of CEO Michael Saylor, Strategy has completely transformed into a Bitcoin holding vehicle. Between January 12-19, 2026, the company purchased 22,305 BTC at an average price of approximately $95,500, totaling $2.13 billion, marking the largest single purchase in the past nine months. As of now, MSTR's total holdings have reached 709,715 Bitcoins, with an average cost of $75,979, amounting to nearly $53.92 billion in total investment.

Its core strategy is based on the "21/21 plan," which aims to raise $21 billion through equity financing and fixed-income instruments for continuous Bitcoin purchases. This model does not rely on operational cash flow but instead utilizes the "leverage effect" of capital markets—converting fiat debt into deflationary digital assets through the issuance of stocks, convertible bonds, and ATM (At-The-Market) tools. This strategy results in MSTR's stock price volatility typically being 2-3 times that of Bitcoin price fluctuations, making it the most aggressive "BTC proxy" tool in the market.

Saylor's investment philosophy is rooted in extreme confidence in Bitcoin's scarcity. He views BTC as "digital gold" and a hedge against inflation, and in the current environment of macro uncertainty (including Fed interest rate policy swings, tariff trade wars, and geopolitical risks), this contrarian bet demonstrates institutional-level long-termism. Even when the company's stock price has retreated 62% from its peak, MSTR is still seen by value investors as an "extreme discount" buying opportunity.

If Bitcoin's price rises to $150,000, the value of MSTR's holdings will exceed $106.4 billion, and the stock price could experience a 5-10 times elasticity due to the leverage amplification effect. However, the reverse risk is also significant: if BTC falls below $80,000, the debt cost (annual interest rate of 5-7%) could trigger liquidity pressure, forcing the company to adjust its strategy or even face liquidation risks.

1.2 Bitmine Immersion Technologies (BMNR): Staking-Driven Productivity Model

BMNR, under the leadership of Tom Lee, has taken a completely different path. The company positions itself as "the world's largest Ethereum Treasury company," holding 4.203 million ETH as of January 19, valued at approximately $13.45 billion. More critically, 1,838,003 ETH are staked, generating approximately $590 million in cash flow income annually at the current annual yield of 4-5%.

This "staking-first" strategy provides BMNR with an intrinsic value buffer. Unlike MSTR's pure price exposure, BMNR earns continuous income through network participation, similar to holding high-yield bonds but with the added benefit of Ethereum ecosystem growth dividends. The company added 581,920 ETH to its staking between Q4 2025 and Q1 2026, demonstrating a continued commitment to the network's long-term value.

BMNR's ecological expansion strategy is also noteworthy. The company plans to launch the MAVAN staking solution in Q1 2026, providing ETH management services for institutional investors and building an "ETH per share" growth model. Additionally, a $200 million investment in Beast Industries on January 15 and the shareholder-approved expansion of the share limit pave the way for potential acquisitions (such as acquiring small ETH holding companies). The company also holds 193 BTC and a $22 million stake in Eightco Holdings, with total crypto and cash assets reaching $14.5 billion.

From a risk management perspective, BMNR's staking income provides downside protection. Even if ETH prices fluctuate around $3,000, staking income can still cover some opportunity costs. However, if ETH network activity remains sluggish, leading to a decline in staking APY, or if prices fall below key support levels, the company's NAV discount may further widen (current stock price is approximately $28.85, down over 50% from its peak).

1.3 Strategy Comparison and Evolution

The two companies represent two typical paradigms of corporate accumulation. MSTR is an offensive, high-risk, high-reward leveraged model that entirely relies on Bitcoin price appreciation to realize shareholder value. Its success is based on the belief in BTC's long-term supply scarcity and the trend of macro monetary depreciation. BMNR, on the other hand, is a defensive, income-oriented ecological model that builds diversified income sources through staking and services, reducing dependence on single price fluctuations.

Notably, both have learned lessons from 2025 and shifted towards more sustainable financing models. MSTR avoids excessive equity dilution, while BMNR reduces reliance on external financing through staking income. This evolution reflects a transition of corporate accumulation from "experimental allocation" to "core financial strategy," marking the arrival of the 2026 era of "institutional dominance rather than retail FOMO."

Part Two: Multidimensional Impact on the Market

2.1 Short-Term Impact: Bottom Signal and Sentiment Recovery

MSTR's massive purchases are often interpreted by the market as confirmation signals for Bitcoin's bottom. The $2.13 billion purchase in mid-January drove Bitcoin ETF inflows to $8.44 billion in a single day, indicating that institutional funds are returning in line with corporate accumulation. This "corporate anchoring" effect is particularly important during periods of weak retail confidence—when the fear and greed index shows "extreme fear," MSTR's continued buying provides psychological support for the market.

BMNR's accumulation of Ethereum also acts as a catalyst. The company's strategy resonates with traditional financial giants like BlackRock, who are optimistic about Ethereum's dominant position in the tokenization of real-world assets (RWA). This could trigger a "second wave of ETH Treasury," with companies like SharpLink Gaming and Bit Digital already beginning to follow suit, accelerating trends in staking adoption and ecological mergers.

Investor sentiment is shifting from panic to cautious optimism. This sentiment recovery has a self-reinforcing characteristic in the crypto market, potentially sowing the seeds for the next upward cycle.

2.2 Mid-Term Impact: Amplified Volatility and Narrative Differentiation

However, the leveraged nature of corporate accumulation also amplifies market risks. MSTR's high-leverage model could trigger a chain reaction during further Bitcoin corrections. With its stock price beta coefficient being over twice that of BTC, any price decline will be magnified, potentially leading to forced selling or liquidity crises. This "leverage transmission" effect previously triggered a similar wave of liquidations in 2025, when many leveraged holders were forced to close positions during rapid declines.

While BMNR has a buffer from staking income, it also faces challenges. Sluggish Ethereum network activity could lead to a decline in staking APY, weakening its "productive asset" advantage. Additionally, if the ETH/BTC ratio remains weak, it could exacerbate BMNR's NAV discount, creating a negative feedback loop.

A deeper impact lies in narrative differentiation. MSTR reinforces Bitcoin's positioning as a "scarce safe-haven asset," attracting conservative investors seeking macro hedges. BMNR, on the other hand, promotes the narrative of Ethereum as a "productive platform," highlighting its application value in DeFi, staking, and tokenization. This differentiation could lead to BTC and ETH performing decoupled under different macro scenarios—e.g., in a liquidity-tightening environment, BTC may perform better due to its "digital gold" attributes, while in a technology innovation cycle, ETH may gain a premium due to ecological expansion.

2.3 Long-Term Impact: Reshaping Financial Paradigms and Regulatory Adaptation

From a long-term perspective, the behaviors of MSTR and BMNR may reshape corporate financial management paradigms. If the U.S. CLARITY Act is successfully implemented, clarifying the accounting treatment and regulatory classification of digital assets, it will significantly reduce the compliance costs for companies allocating crypto assets. This legislation could drive Fortune 500 companies to allocate over $1 trillion in digital assets, shifting corporate balance sheets from the traditional "cash + bonds" mix to "digital productive assets."

MSTR has become a textbook case of a "BTC proxy," with its market value and net asset value (NAV) premium mechanism referred to as the "reflection flywheel"—issuing stock at a premium to buy more Bitcoin, increasing the per-share BTC holding, thereby pushing up the stock price and creating a positive feedback loop. BMNR provides a replicable template for ETH Treasury, demonstrating how staking income can create sustained value for shareholders.

This could also trigger a wave of industry consolidation. BMNR has received shareholder approval for share expansion for acquisitions, potentially acquiring small ETH holding companies to form "Treasury giants." Weaker accumulation companies may be forced to sell or merge under macro pressure, leading to a "survival of the fittest" pattern in the market. This marks a structural shift in the crypto market from "retail dominance" to "institutional dominance."

However, this process is not without risks. If the regulatory environment worsens (e.g., the SEC takes a hard stance on digital asset classification) or if the macro economy unexpectedly deteriorates (e.g., the Fed raises interest rates due to inflation rebound), corporate accumulation could shift from a "paradigm shift" to a "leverage trap." Historically, similar financial innovations have often led to systemic crises when faced with regulatory crackdowns or market reversals.

Part Three: Core Issues Discussion

3.1 Corporate Accumulation: A New Golden Era or a Leverage Bubble?

The answer to this question depends on the perspective and time scale of observation. From the standpoint of institutional investors, corporate accumulation represents a rational evolution of capital allocation. In the context of global debt expansion and increasing concerns about currency depreciation, allocating part of the assets to scarce digital assets is strategically reasonable. MSTR's "smart leverage" is not gambling but rather utilizing capital market tools to convert equity premiums into digital asset accumulation, which is sustainable when the equity market fully recognizes its strategy.

BMNR's staking model further proves the "productive" attributes of digital assets. The annualized $590 million in staking income not only provides cash flow but also allows the company to maintain financial stability amid price fluctuations. This is akin to holding high-yield bonds but with the added benefit of network growth dividends, showcasing the potential of crypto assets to transcend "pure speculative tools."

However, critics' concerns are not unfounded. The current leverage ratio of corporate accumulation is indeed at a historical high, with $9.48 billion in debt and $3.35 billion in preferred stock financing potentially becoming burdens under macro headwinds. The lessons from the 2021 retail bubble are still fresh—many highly leveraged participants suffered severe losses during rapid deleveraging. If the current wave of corporate accumulation is merely shifting leverage from retail to corporate levels without fundamentally changing the risk structure, the ultimate outcome could be equally disastrous.

A more balanced view suggests that corporate accumulation is in a "institutional transition period." It is neither a simple bubble (as it has fundamental support and long-term logic) nor an immediate golden era (as regulatory, macro, and technological risks still exist). The key lies in execution—can sufficient market recognition be established before regulatory clarity? Can financial discipline be maintained under macro pressure? Can technological and ecological innovations prove the long-term value of digital assets?

Conclusion and Outlook

The accumulation behaviors of MSTR and BMNR mark a new phase in the cryptocurrency market. This is no longer a retail-driven speculative frenzy but a rational allocation based on long-term strategies by institutions. Although the two companies have taken completely different paths—MSTR's leveraged belief injection and BMNR's staking-driven productivity model—they both demonstrate a commitment to the long-term value of digital assets.

Corporate accumulation is essentially a gamble on "time." It bets that regulatory clarity will come faster than liquidity exhaustion, that price increases will occur before debt maturities, and that market faith will be stronger than macro headwinds. There is no middle ground in this game—either it proves that digital asset allocation is a paradigm revolution in 21st-century corporate finance, or it becomes another cautionary tale of excessive financialization.

The market stands at a crossroads. To the left is a mature market dominated by institutions; to the right is the abyss of leveraged collapse. The answer will soon be revealed in the next 12-24 months, and we are all witnesses to this experiment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。