For the global fintech community, the question is not whether stablecoins will become mainstream. The question is, what can we learn from the places where stablecoins have already become popular—Africa.

Author: Oui Capital

Translated by: Will A-Wang

In previous articles, such as “The Crypto Narrative of Stablecoins is Reshaping Africa's Economic Landscape” and “Web3 Payment Research Report: In 2025, Stablecoins in Africa,” we have looked at the financial transformation in the African continent from the perspective of stablecoins, a bottom-up view that resonates deeply.

From everyday tools: savings, consumption, and credit, to B2B trade and cross-border payments, and access to credit, stablecoins are addressing issues such as Dollar Access, Instant Settlement, and FX Inefficiencies in Africa, which are particularly pronounced in markets with insufficient traditional payment channels.

Stablecoins have already become a reality in Africa's cross-border payments… the rest of the world is just catching up. — Zekarias Amsalu, Co-Founder of Africa Fintech Summit

Stablecoins are like the communication signals I received from space through Starlink while in the vast Serengeti. However, this is not comprehensive; the vast majority of the African population still relies on traditional telecom pathways. This mirrors the financial reality in Africa. The fragmented nature of various regions and the lack of financial infrastructure actually require an overall enhancement of the fintech transformation, of which blockchain stablecoins are just one optimal path.

Therefore, we have compiled an article from Oui Capital: Africa's Cross-border Payment Landscape, aiming to explore the butterfly effect that financial transformation will have from a comprehensive perspective of Africa's cross-border payment landscape. This report provides a thorough insight into the African cross-border payment market, outlining market conditions and key trends, regional differences, payment path choices, and potential investment trends.

Through this report, we also see the missing aspect of bottom-up transformation with stablecoins: the impacts that regulatory collaboration will bring, the value released by interoperability between fintech companies and banks, and solutions to the pain points of essential scenarios (which is also a reflection on Airwallex CEO Jack's comments on stablecoins).

Although some regional financial innovations can accelerate the flow of funds, the financial tracks supporting Africa have not synchronized. The traditional financial system has failed to provide stability, accessibility, and efficiency, leading people to face risks of inflation and financial uncertainty, with limited control over savings and difficulty entering global markets. But just as the region skipped the desktop era and went straight into mobile, now, the African continent is ready to move beyond outdated banking infrastructure and actively embrace the next generation of fintech transformation.

For the global fintech community, the question is not whether stablecoins will become mainstream. The question is, what can we learn from the places where stablecoins have already become popular—Africa.

Executive Summary

The current value of the African cross-border payment market is expected to reach $329 billion by 2025, with a projected compound annual growth rate (CAGR) of 12%, reaching $1 trillion by 2035. However, the market faces inefficiencies that cost businesses and consumers billions of dollars each year. Factors such as trade growth in Africa, increased migration, rising mobile payment adoption, and fintech innovation are reshaping this landscape. Despite progress, challenges such as high transaction fees, currency volatility, and regulatory fragmentation continue to hinder seamless transactions.

In 2022, the number of registered mobile payment accounts in Africa reached 781 million, a year-on-year increase of 17%, with transaction volumes reaching $837 billion, accounting for 66% of global mobile payment transaction volumes. Fintech solutions have significantly reduced remittance costs, averaging only 3.5%, allowing remittances to be completed in minutes, while traditional bank fees can be as high as 8-12%. Additionally, intra-African trade is also growing, with small and medium-sized enterprises increasingly utilizing digital payments to efficiently handle cross-border transactions. However, the market still faces numerous obstacles.

Despite this, Africa remains the region with the highest remittance costs globally, averaging 7.4%-8.3%, primarily due to regulatory fragmentation and limited digital interoperability. Only 55% of African countries allow electronic KYC, leading to redundant compliance processes, while inconsistent foreign exchange policies in countries like Nigeria further exacerbate transaction uncertainty and costs. Additionally, foreign exchange liquidity challenges necessitate costly offshore USD/EUR settlements, resulting in an extra $5 billion in costs annually due to insufficient liquidity and currency double conversion.

Investment and innovation opportunities abound, especially in enhancing the interoperability of digital payments and building robust APIs and infrastructure layers. Connecting mobile payment networks can save up to $5 billion annually by addressing transaction inefficiencies. Furthermore, the expansion of cryptocurrency and stablecoin payments presents significant opportunities, with remittance costs potentially reduced by up to 60% compared to traditional banks, and faster settlements achievable at minimal foreign exchange costs. Finally, establishing decentralized foreign exchange exchanges in Africa could significantly lower foreign exchange conversion costs, stabilize exchange rates, and promote intra-African trade and remittances.

1. Market Overview and Key Trends

The African payment market is at a critical juncture. The increasing adoption of digital payment channels and the shift in migration patterns are seeking to formalize informal transactions by providing faster and cheaper alternatives to traditional bank transfers. Mobile payments, fintech solutions, and regulatory reforms are driving this shift, making digital payment channels more competitive.

This shift is expected to achieve a 12% CAGR and could drive the entire cross-border remittance market (including formal and informal) to reach $329 billion by 2025 and $1 trillion by 2035. However, despite increasing digital penetration, informal channels and traditional bank transfers remain entrenched due to costs, accessibility, and regulatory gaps.

Even as digital solutions continue to evolve, some users still rely on old methods due to trust issues, regulatory inconsistencies, or limited infrastructure. Can digital innovation truly absorb informal capital flows on a large scale? Or will structural inefficiencies continue to drive the development of other transfer methods? The answer will determine whether the African payment market can achieve its expected formalization or whether the informal market can continue to thrive.

1.1 Formal Cross-border Remittance Channels and Market Growth (2020 - 2035)

A. Current Market Value (2025)

By 2025, the formal cross-border payment market in Africa is expected to reach $140.9 billion, with a CAGR of 12%. In 2023 alone, remittances flowing into Africa reached $90.2 billion (accounting for 5.2% of the continent's GDP), nearly double the amount of foreign aid received by Africa.

B. Historical CAGR (2020 - 2025)

Over the past five years, formal remittance inflows have continued to grow, with a CAGR between 10% and 15%, averaging 12%. Specifically, from 2020 to 2023, remittance inflows grew significantly by 14.8%, primarily due to increased remittances from expatriates.

1.2 Total Cross-border Remittance Channels and Market Size Estimates

A. Share of Informal Capital Flows

In 2022, the total formal remittance amount to Sub-Saharan Africa was between $53 billion and $54 billion, but informal channels accounted for a significant portion of total remittances, indicating an underestimation of market size. Informal remittances account for 35% to 75% of total remittance amounts, meaning that the actual remittance amount, including informal transactions, could exceed $329 billion by 2025.

B. Cost Impact

The average fee for formal remittances is 7.4%, which encourages continued reliance on informal transfers. Digital solutions have reduced fees to between 1.5% and 3%, making formal channels more attractive and potentially capturing a larger share of informal capital flows.

C. Market Growth Forecast

With the increasing adoption of digital applications, it is expected that a 12% CAGR will drive the total remittance market to reach $1 trillion by 2035. This also highlights the significant opportunities presented by digital solutions, which can formalize more transactions, shift informal capital flows to traceable online channels, and drive future market growth.

1.3 Key Growth Drivers for Cross-border Payments

A. Regulatory Reforms (Pan-African Payment and Settlement System (PAPSS) and African Continental Free Trade Area (AfCFTA))

The Pan-African Payment and Settlement System (PAPSS) launched in 2022, enabling instant cross-border payments in local currencies, with an expected annual savings of $5 billion. Additionally, the African Continental Free Trade Area (AfCFTA) is coordinating financial systems to reduce reliance on SWIFT and external banking intermediaries.

B. Regional Migration, Trade, and Urbanization

In 2022, intra-African remittance amounts reached $20 billion, reflecting strong regional migration trends. Urbanization and intra-African trade are driving the development of South-South remittance corridors, enhancing regional financial integration.

C. Mobile Payment Penetration

Currently, 30% of cross-border remittances in Sub-Saharan Africa are processed through mobile payments, with transaction amounts reaching $16 billion in 2022, a year-on-year increase of 22%. The annual growth rate for mobile payment remittances is 48%, with fees (1.5% - 3%) lower than bank remittances (over 7%).

1.4 The Impact of Fintech Innovation on Cross-border Payments

A. Remittance Volume through Fintech Channels

Since 2020, the usage of digital remittances has doubled, with 71% of mobile remittances originating from Africa. By 2024, mobile payments are expected to process over 30% of remittance volumes in Sub-Saharan Africa, with fintech companies handling hundreds of billions of dollars in remittances annually.

B. The Rise of Fintech Solutions (Blockchain, API, Digital Wallets)

Africa is one of the regions with the highest cryptocurrency adoption rates globally, with on-chain cryptocurrency transaction volumes reaching $125 billion, highlighting the increasing shift towards cheaper and faster remittance solutions.

Fintech APIs are enhancing direct wallet-to-wallet remittances and interoperability, reducing reliance on high-cost intermediaries.

Emerging banks and digital wallets are providing seamless cross-border transfer services through mobile and online platforms, making remittances faster, more convenient, and cost-effective.

According to Chainalysis data, Africa is the fastest-growing region for cryptocurrency adoption, with a year-on-year growth rate of 45% from 2022-2023 to 2023-2024, surpassing other emerging markets like Latin America at 42.5%. This rapid growth underscores the immense potential for stablecoin applications, especially in Africa, where bank penetration remains among the lowest globally.

C. Expected Cost Savings from Digital Innovation

Digital transfers have significantly reduced remittance costs from 7.4% to 3% or lower, saving migrants $4 to $5 billion annually while making cross-border payments more affordable. Additionally, PAPSS and fintech APIs are expected to eliminate $5 billion in correspondent bank fees, further accelerating transaction speeds and reducing costs. For every 1% reduction in remittance fees, African households can save approximately $6 billion annually, highlighting the substantial financial impact of digital innovation on the remittance industry.

## Overview of Fund Flows in Different Regions of Africa

While mobile payment adoption is increasing in some areas, it remains relatively low in others compared to East and West Africa. Central Africa's financial system is more fragmented, heavily reliant on informal networks, and has limited interoperability between banks and mobile payment platforms.

Here’s an insight into the inflows and outflows of funds by region:

2.1 West Africa

West Africa is one of the largest remittance-receiving regions in Africa, with remittance inflows reaching approximately $48 billion in 2022 (World Bank 2023 data). Nigeria alone received $20 billion, primarily from the United States, the United Kingdom, and Canada. Ghana, Senegal, and Côte d'Ivoire also received significant remittances, thanks to their close migration ties with France and other European countries.

Remittances between regions are also relatively substantial, such as Côte d'Ivoire - Burkina Faso ($1.5 billion), Ghana - Nigeria ($900 million), and Mali - Senegal ($750 million) (African Development Bank 2023 data).

These fund flows are primarily driven by trade, facilitated by high remittance costs averaging 8-10% (IMF 2023 data), with informal networks playing a significant role. Despite advancements in financial infrastructure, interoperability between mobile payments and bank-dominated systems remains a challenge in some areas. While Nigeria and Ghana have stronger bank-dominated systems that can promote broader integration, seamless transactions between mobile payments and traditional bank channels are still evolving.

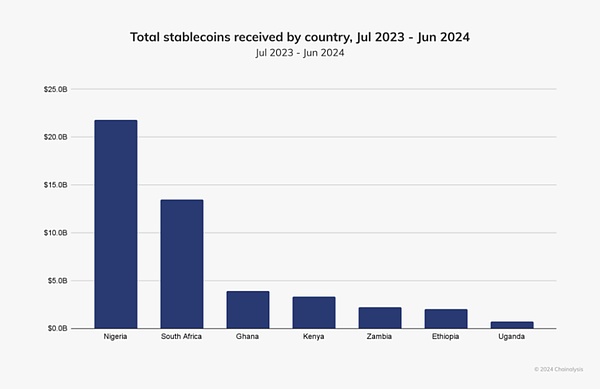

In Chainalysis's Global Crypto Adoption Index, Nigeria ranks second overall. Between July 2023 and June 2024, the country received approximately $59 billion in cryptocurrency. Nigeria is also one of the leading markets for mobile crypto wallet adoption, second only to the United States. The country is actively working towards regulatory clarity, including through incubation programs, and the use of stablecoins in everyday transactions (such as bill payments and retail purchases) has significantly increased.

(Sub-Saharan Africa: Nigeria Takes #2 Spot in Global Adoption, South Africa Grows Crypto-TradFi Nexus, Chainalysis)

Like Ethiopia, Ghana, and South Africa, stablecoins are also a crucial component of Nigeria's crypto economy, accounting for about 40% of all stablecoin inflows in the region—the highest in Sub-Saharan Africa. Nigerian users report higher transaction frequencies and a deeper understanding of stablecoins as a financial tool rather than just an asset class.

Cryptocurrency activity in Nigeria is primarily driven by small retail and professional-scale transactions, with about 85% of transfer values below $1 million. Due to the inefficiencies and high costs of traditional remittance channels, many Nigerians rely on stablecoins for cross-border remittances. Cross-border remittances are the primary use case for stablecoins in Nigeria, as they are faster and more affordable.

2.2 East Africa

East Africa is leading in mobile payment adoption, with over 60% of remittance transactions conducted digitally (GSMA 2023 data). Kenya, Uganda, and Tanzania rely on M-Pesa, MTN, MoMo, and Airtel Money, reducing remittance costs to 3%.

The region's outward remittances primarily flow to the Middle East, especially to Ethiopia ($5.3 billion), Somalia ($2.1 billion), and Kenya ($3.5 billion) (World Bank 2023 data). These funds support household livelihoods and small businesses. However, cross-border payments within East Africa are still constrained by regulatory differences and a lack of seamless interoperability, limiting financial inclusion.

One of Kenya's greatest advantages is its deeply rooted mobile money culture. M-Pesa, launched by Safaricom in 2007, has become a pillar of Kenya's financial system, processing about 60% of the country's GDP and covering over 90% of the adult population. Its success lies in providing banking services without the need for physical banks, enabling millions of Kenyans to deposit, withdraw, transfer, and even access credit via mobile devices. Stablecoins complement this ecosystem by allowing users to hold value in stable currency and conduct frictionless transactions globally.

In addition to mobile money, Kenya's regulatory environment has been a significant driver of fintech and Web3 development. Unlike many countries that take a restrictive stance on digital assets, the Capital Markets Authority (CMA) in Kenya actively promotes innovation through regulatory sandboxes, allowing blockchain-based companies to test and refine their products.

2.3 Southern Africa

Southern Africa has substantial remittance flows, particularly from South Africa. In 2022, South Africa remitted $17 billion to neighboring countries (Statista 2023 data), with Zimbabwe receiving $1.9 billion, followed by Mozambique ($1.2 billion) and Malawi ($800 million). Labor migration is a major driver, with workers in mining, construction, and domestic services regularly sending money back home. However, remittance costs remain the highest in Africa, with average fees for formal channels ranging from 12% to 15% (World Bank 2023 data), leading to reliance on informal networks, which account for nearly 40% of total remittances.

The remittance landscape in Southern Africa is primarily bank-dominated, with traditional financial institutions playing a leading role in cross-border transactions. Unlike East Africa, where mobile payments are widely adopted, the penetration of mobile payments in Southern Africa is relatively low. For example, South Africa has a well-established banking system that handles most remittance business. However, high fees and slow processing times lead many migrants to prefer informal channels. Efforts to integrate mobile payments into a broader financial ecosystem are ongoing, but interoperability between mobile wallets and banks remains limited.

2.4 Central & North Africa

North Africa, led by Egypt ($32 billion), Morocco ($11 billion), and Algeria ($5.1 billion), remains one of the largest remittance-receiving regions, benefiting from a large diaspora in Europe (World Bank 2023 data). Over 65% of remittance inflows come from France, Spain, and Italy.

The Middle East is also a significant source of remittances, especially for Egypt, where Saudi Arabia, the UAE, and Kuwait account for over 50% of total remittance inflows (World Bank 2023 data). Moroccan and Tunisian migrants working in Gulf countries also contribute substantial remittances, but inflows from Europe still dominate.

In Central Africa, the construction of remittance channels is primarily driven by internal migration within Africa, with Cameroon receiving $2.8 billion in remittances from Chad and the Central African Republic (African Development Bank 2023 data). Due to limited financial infrastructure and high fees exceeding 10% for formal channels, over 70% of transactions remain informal. The financial landscape in North Africa is primarily bank-dominated, with most remittances processed by formal financial institutions.

2.5 Populations Driving Cross-border Payments

A. Workers and Migrants

Labor migrants send funds back home primarily for household expenses, education, and healthcare.

The strongest migration patterns are from rural to urban areas and from low-income African countries to high-income African countries, such as South Africa and Nigeria. Other examples include Egypt in North Africa and Kenya in East Africa, which attract a large number of labor migrants due to economic strength and job opportunities.

Typically, remittances range from $200 to $500 per month, primarily for family support.

B. Traders and Small Enterprises

Informal traders and small enterprises rely on remittances for inventory purchases, supplier payments, and cross-border trade expansion.

Mobile payment and fintech platforms are the primary transaction channels, providing fast and convenient payment solutions.

Payment amounts range from $1,000 to $10,000, depending on trade volume and industry.

C. Corporate Transactions

Businesses process payroll for foreign employees and gig workers through remittance processes.

Large supply chain transactions increasingly utilize fintech-supported instant payments, reducing reliance on cash.

Transaction amounts can exceed $50,000, especially in logistics, payroll, and supply chain settlements.

## Global Cross-border Payment Pathways

Global cross-border payments operate through a complex multi-layered infrastructure, facilitating the flow of funds between different countries, currencies, and financial institutions. This system is built on traditional banking networks, fintech disruptors, foreign exchange (FX) settlement systems, and emerging digital payment alternatives.

To understand how cross-border payments currently operate in Africa, it is essential to grasp how funds flow in the global market. This section explores the key components of existing transaction methods, major participants, and the cost structure that defines today's cross-border payments.

3.1 Traditional Finance (TradFi) — Bank-Dominated Infrastructure

TradFi underpins most high-value international transactions, with transaction amounts typically ranging from $100,000 to several billion dollars. These payments are processed through secure, regulated banking channels that rely on interbank messaging, correspondent banking, and large-scale settlement systems.

Information transmission and instructions: The communication infrastructure that financial institutions use to securely send transaction details. They do not transfer funds but enable banks, payment service providers, and financial institutions to exchange payment instructions in a standardized format. Without these systems, banks would struggle to achieve interoperability, leading to slow transfer speeds, high costs, and a higher likelihood of errors.

Forex execution and trading: The currency exchange layer facilitates and ensures that funds are exchanged at market rates. Banks, hedge funds, and corporations utilize the forex market to ensure liquidity, hedge currency risks, and settle international invoices. Without this layer, businesses would find it difficult to conduct cross-currency transactions, resulting in inefficiencies in global trade.

Forex settlement and clearing: The forex settlement layer ensures that transactions are properly settled, thereby avoiding the risk of default by either party. They employ a payment versus payment (PvP) model, ensuring that both sides of the currency exchange occur simultaneously, thus eliminating counterparty risk. Without such systems, transactions could fail, meaning one party delivers currency but does not receive the expected funds.

Correspondent bank network: Large global banks handle payments between financial institutions that lack direct connections, enabling them to process cross-border payments. These banks hold accounts on behalf of foreign banks, ensuring the correct flow of funds.

USE CASE: An American company pays $5 million to a German supplier via traditional bank wire transfer.

A. Payment Initiation

An American company pays $5 million to a German supplier via traditional bank wire transfer.

Involved parties: For example, JPMorgan (U.S. bank), Deutsche Bank (German bank).

Cost and time impact: SWIFT fees range from $10 to $50. Payment initiation is instantaneous, but processing may take several hours.

B. Currency Exchange (USD to EUR)

JPMorgan uses its forex trading platform to convert USD to EUR.

Involved parties: For example, EBS, Refinitiv FX Matching, CME FX.

Cost and time impact: Forex spread is 0.1% - 2% (cost impact of $100 - $1,000), settlement time is seconds to minutes.

C. Forex Settlement and Clearing

Payments are settled through CLS Group to ensure both currencies are transferred simultaneously.

Involved parties: For example, CLS Group (PvP settlement).

Cost and time impact: Ensures secure forex settlement, but incurs a small CLS fee (approximately $5 per $1 million settled).

Time: 1 business day.

D. Correspondent Bank and Final Settlement

If there is no direct connection between JPMorgan and Deutsche Bank, a correspondent bank handles the payment. Deutsche Bank deposits the funds to the supplier and sends final confirmation.

Involved parties: Correspondent bank (e.g., HSBC).

Cost and time impact: Additional fees range from $20 to $100. Complete transaction settlement takes 1 to 3 days.

Estimated total cost: $20,000 to $150,000, including SWIFT fees, forex spreads, and correspondent bank fees. Settlement time: 1 to 3 days.

Reasons for high costs: Multiple intermediaries charge fees at each step, forex spreads can be significant, and settlement times are lengthy.

In Africa, due to the lack of traditional financial infrastructure, even cross-border remittances to neighboring countries sometimes require routing through correspondent banks in the U.S.

3.2 Fintech Disruptors — Faster Payment Alternatives

While traditional finance (TradFi) dominates high-value transactions, small businesses, freelancers, and digital-first companies require cheaper and faster alternatives. This has led to the rise of fintech disruptors that bypass (optimize) the correspondent bank network, opting for local partnerships, centralized liquidity, and real-time settlement networks.

Fintech companies are circumventing traditional banking channels, transforming cross-border payments by providing faster, cheaper, and more transparent transactions for amounts typically ranging from $100 to $50 million.

Estimated total cost: Fees of $12 to $30, saving up to $100 compared to banks.

Settlement time: Same day (hours instead of days).

Reasons for being cheaper and faster: Wise matches transactions locally without needing correspondent banks, eliminating forex markups and SWIFT fees.

This settlement method, which achieves cross-border funding pools through local bank accounts, inherently allows for higher efficiency in fund delivery. This is what Airwallex CEO Jack refers to when he says he sees no advantages of stablecoins. However, it also tests fintech companies' capabilities in managing banking channels and liquidity positions across various regions.

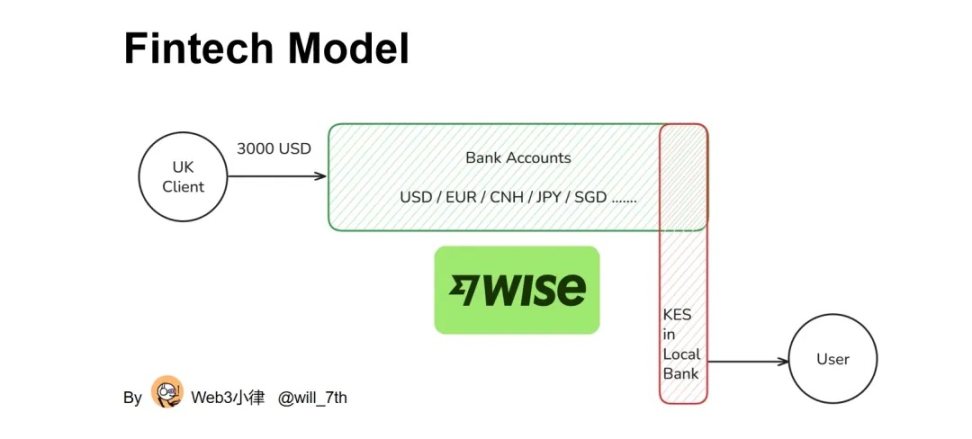

USE CASE: A freelancer in Kenya receives $3,000 from a British client via Wise.

A. Payment Initiation

A British client remits $3,000 via Wise instead of a traditional bank wire transfer.

Involved parties: For example, Wise (fintech alternative).

Cost and time impact: Transfer starts immediately, fees: 0.4% - 1% ($12 - $30).

B. Liquidity Pool and Local Settlement

Wise matches this transaction with individuals sending KES to the UK, avoiding direct forex transfers.

Involved parties: For example, Wise local settlement network.

Cost and time impact: Close to market mid-rate, 0.5% - 1% spread (savings of $60 - $100).

C. Local Bank Payment

Wise pays the freelancer in KES from its local bank account in Kenya.

Involved parties: For example, Kenyan cooperative bank.

Cost and time impact: Settlement time is within minutes to hours, with no SWIFT fees.

3.3 Cryptocurrency and Blockchain-Based Settlement

Blockchain and stablecoins completely replace banks, enabling instant, low-cost transactions ranging from $1 to $10 million. Cryptocurrency rails utilize decentralized ledgers, entirely bypassing SWIFT and correspondent banks, reducing settlement times from days to seconds.

Estimated total cost: On-chain fees are negligible. The main costs are for currency acceptance for deposits and withdrawals, ranging from 0.4% to 1%.

Settlement time: Instant.

Reasons for being cheaper and faster: Eliminates intermediaries, reducing fees by up to 99% compared to banks, and shortening settlement times from days to seconds.

While there are costs associated with currency acceptance for deposits and withdrawals, they are indeed present relative to the costs of cross-border funding pools. However, for countries with foreign exchange controls, holding USD instead of a domestic currency that is subject to inflation is a significant advantage.

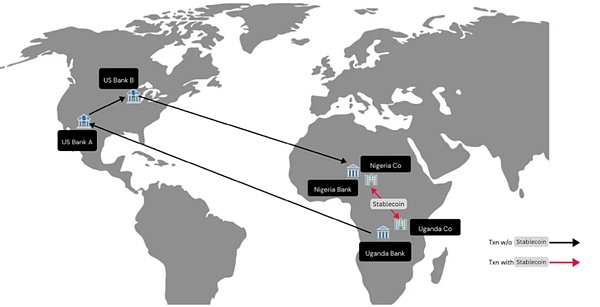

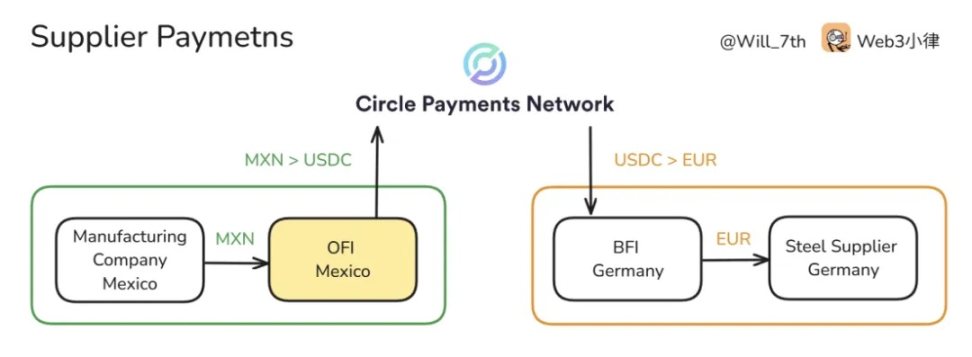

USE CASE: A textile factory in Mexico sends $1 million USDC to a supplier in Germany.

A. Blockchain Transfer

The sender converts local currency into $1 million USDC and transfers it via blockchain.

Involved parties: For example, Ethereum, Solana, USDC issuer (Circle) 0.4% - 1% ($4,000 - $10,000).

Cost and time impact: Network fee: $1.

Time: Seconds.

B. Cross-Border Settlement

The recipient immediately receives $1 million USDC in their digital wallet.

Involved parties: For example, cryptocurrency exchanges (Binance, Coinbase, Circle API).

Cost and time impact: No intermediaries, completed instantly.

C. Local Exchange and Payment

The recipient exchanges USDC for euros through an exchange.

Involved parties: For example, Binance, local fintech company.

Cost and time impact: USDC issuer (Circle) 0.4% - 1% ($4,000 - $10,000), settlement completed within minutes.

3.4 Cross-Border Payment Channels in Africa

Traditional finance (TradFi) dominates large payments, but costs remain prohibitively high, with transactions reaching $20,000 to $150,000. In contrast, fintech solutions offer a cost-effective alternative, reducing fees for SMEs and freelancers by up to 90%. More transformationally, blockchain-based settlements bypass traditional banks, bringing costs close to zero.

Despite these advancements, remittances remain expensive under the operations of traditional service providers like Western Union. However, fintech disruption is reshaping this landscape, providing faster and cheaper alternatives.

This shift is particularly urgent in Africa, where cross-border payments are fragmented, costly, and heavily reliant on correspondent banks and cash remittances. While global markets embrace real-time settlement and fintech-driven efficiencies, Africa still depends on traditional infrastructure, leading to delays and high costs. However, innovation is on the rise.

The unique financial landscape of the African continent, dominated by mobile payments, regional payment systems, and blockchain-based solutions, is beginning to address long-standing inefficiencies and pave the way for a more inclusive and affordable future.

Key characteristics of cross-border payments in Africa:

A. Low-Value, High-Frequency Transactions Dominate

Remittances, SME trade, and informal payments are the primary use cases. The average remittance transaction in Africa is $200 to $400, with an estimated monthly transaction volume of 60 to 80 million (World Bank 2023 data). Informal cross-border traders typically handle payments of $200 to $1,000 per transaction, often trading multiple times a week (UNCTAD 2021 data).

B. Fintech and Blockchain

Companies like Chipper Cash, Flutterwave, and BitPesa are bypassing banks to achieve faster and cheaper transfers.

C. Currency Fragmentation

Africa has over 40 currencies, leading to high forex costs and reliance on USD/EUR settlements.

D. Heavy Reliance on Cash

Digital applications are growing, but over 80% of transactions are still cash-based (World Bank, 2023). Cash remains dominant.

E. Strong Mobile Payment Networks

Africa leads in mobile payment adoption, with platforms like M-Pesa, MTN MoMo, and Airtel Money dominating.

F. Reliance on Correspondent Banks

Many African banks lack direct cross-border business relationships, which increases transaction costs and processing times.

### IV. How Are Cross-Border Payments Conducted on the African Continent?

Remittance transactions typically require multiple steps, from the remitter to the recipient, involving different financial entities and regulatory frameworks.

4.1 Remitter Initiates Transaction

The remitter selects a payment channel based on cost, speed, accessibility, and convenience. Preferences vary by location, digital literacy, and financial infrastructure:

Mobile Payments (e.g., M-Pesa, MTN MoMo)

Due to their low fees (typically 1-3% per transaction) and high accessibility, individuals in countries/regions with developed mobile payment ecosystems prefer mobile payments. Transactions are usually completed instantly, making them ideal for everyday remittances under $500.

Fintech Apps (e.g., Chipper Cash, Grey)

These attract digital finance users who need faster transfers and better exchange rates. The fees charged by these services are lower than banks (averaging 0-2%), and transaction processing times range from a few minutes to a few hours.

Bank Transfers (e.g., UBA, Ecobank)

Typically used by businesses and individuals with formal banking services for large transactions. However, these services have higher fees (2-5%) and slower processing times (1-3 days), making them less suitable for urgent remittances.

Cash Withdrawals (e.g., Western Union, MoneyGram)

These remain crucial for recipients in rural areas with limited digital payment infrastructure. These services charge 5-10% per transaction and require recipients to visit physical locations, but they are reliable and widely available.

Cryptocurrency Transfers (e.g., Bitnob, Afriex)

Favored by users seeking low-cost (0-1%) and borderless transactions, especially where forex trading is restricted. Settlement times can be instant or take several hours, depending on blockchain congestion and the availability of fiat currency entry and exit options.

4.2 Transaction Processing and Routing

Transactions are processed by payment aggregators, money transfer operators (MTOs), or routed through blockchain-based networks, each serving different market needs and operational models:

Mobile Payment Aggregators

These companies connect telecom operators, banks, and international money transfer operators (IMTOs) to enable seamless transaction routing. As aggregators, they do not directly own customer relationships but facilitate interoperability. They focus on the entire African continent, especially in regions with high mobile payment penetration (East Africa, West Africa, and parts of Central Africa). They typically generate revenue by charging transaction fees to international money transfer operators, telecom operators, and banks.

At the same time, they often have payment channels that allow them to conduct direct-to-consumer (D2C) transactions for individuals and SMEs wishing to engage in cross-border transactions. Examples include Onafriq (formerly MFS Africa), Cauridor, and Thunes.

Fintech Aggregators

These are digital payment infrastructure providers that offer businesses (merchants, fintech companies, SMEs) a single API to accept various payment methods, including mobile payments, bank transfers, and card payments. Companies like Flutterwave, Paystack, and Fincra enable merchants to process digital payments from multiple sources through a single integration. They focus on countries where the digital economy is thriving and banking is formalized, such as Nigeria, South Africa, Egypt, and Kenya. Their revenue model is based on merchant transaction fees (1-4%), API subscription fees, and value-added services like fraud detection and instant settlement. These aggregators meet the needs of businesses, merchants, and digital platforms requiring seamless payment processing.

Traditional Banks and Correspondent Bank Networks

Transactions conducted through banks are processed via the SWIFT network and correspondent bank relationships, which remain the primary processing method for high-value transactions. Most African banks lack direct connections with foreign banks, necessitating the use of intermediary correspondent banks (e.g., Citibank, JPMorgan) to settle cross-border payments. This reliance on multiple intermediaries increases costs and delays, with settlement times ranging from 1 to 5 days.

SWIFT processes over $80 billion in cross-border transactions involving African banks monthly (SWIFT 2023 data), and due to its global acceptance and regulatory compliance, SWIFT is deeply entrenched in the financial system. However, this also makes it one of the most expensive solutions, with fees ranging from 0.5% to 3% of the transaction amount, plus forex spreads and intermediary fees. Disrupting this system has proven challenging, although emerging alternatives like PAPSS and blockchain-based networks are striving to reduce costs and shorten settlement times.

Cash Withdrawal and Remittance Networks

Transactions from Western Union and MoneyGram typically go through correspondent banks (e.g., Citibank and JPMorgan) before reaching the recipient, adding multiple layers of fees and delays. Due to the lack of direct international clearing capabilities among most African banks, these remittance providers must transfer funds through the SWIFT system, leading to high transaction costs (5-10% per transfer) and extended processing times (from hours to days). Additionally, many banks serve as cash withdrawal points for Western Union and MoneyGram, further reinforcing their reliance on banking infrastructure for physical payments and compliance checks.

Despite these inefficiencies, Western Union and MoneyGram maintain a strong market position due to their extensive agent networks, compliance, and consumer trust built over decades. They can offer cash withdrawals, bank deposits, and forex services, ensuring their continued dominance in the African remittance space.

To address these inefficiencies, emerging companies like BnB Transfer have expanded payment options beyond traditional cash withdrawals. They now offer bank deposits, mobile payments, and agent network services, providing individuals and SMEs with more flexible funding access while reducing reliance on expensive correspondent banking systems.

Blockchain Networks and Cryptocurrency-Based Remittances

Platforms like Afriex, Bitnob, and Stellar process transfers based on blockchain networks. This provides instant transaction verification and reduces intermediaries, shortening transaction times to minutes and lowering costs to 0-1% per transaction. Users typically fund their cryptocurrency wallets through bank transfers, mobile payments, or any other available access method.

While blockchain-based remittance solutions offer faster settlement speeds and higher accessibility for users in countries/regions with forex controls or limited banking infrastructure, these companies struggle to scale due to regulatory uncertainty, limited fiat access and exit options, and compliance restrictions. The inability to effectively convert cryptocurrency into local currency makes it difficult for these providers to establish partnerships with major financial institutions, limiting their ability to process transactions at scale and compete with traditional remittance providers.

4.3 Currency Exchange

If the remittance involves different currencies, currency exchange is required before payment. Currency exchange is facilitated by multiple entities, including banks, forex brokers, fintech platforms, and blockchain-based liquidity providers.

Banks and Correspondent Banks

Traditional banks rely on correspondent bank networks to obtain foreign currency, which increases fees (typically charging 0.5% - 3% per transaction) and extends settlement times (1 - 3 days).

Forex Brokers and Fintech Platforms

Companies like AZA Finance, VertoFX, and Thunes provide alternative currency exchange services, often offering better rates and faster settlement speeds than banks. They aggregate liquidity from multiple sources to facilitate cross-border trade and remittances.

Blockchain-Based Liquidity Providers

Platforms like Stellar, Bitnob, and Afriex use decentralized networks to provide real-time currency exchange at minimal costs (0 - 1% per transaction), but their scalability is limited due to regulatory barriers and low institutional adoption rates.

4.4 Last Mile Delivery

This involves depositing funds into the recipient's mobile wallet, bank account, or withdrawing cash through partner agents, banks, or mobile payment operators.

Banks and Financial Institutions

For recipients opting for bank deposits, financial institutions will process the transfer. Settlement times range from instant to 3 days, depending on the bank's infrastructure and interbank relationships.

Mobile Payment Operators

Platforms like M-Pesa, MTN MoMo, and Airtel Money support direct wallet deposits, typically processing in real-time or within a few hours.

Cash Withdrawal Networks

Providers like Western Union, MoneyGram, and BnB Transfer offer on-site cash withdrawal services at designated agent points or partner banks. These transactions require additional KYC verification and fees.

### V. The Landscape of Payments in Africa and Key Players

Traditional institutions like banks and money transfer operators (MTOs) rely on correspondent banks and the SWIFT network, which drives up costs and slows down settlement speeds. As fintech companies provide users with faster, cheaper, and more convenient solutions, the landscape of cross-border payments in Africa is rapidly evolving.

In contrast, fintech disruptors are changing the payment ecosystem by offering direct-to-consumer services and developing infrastructure that empowers traditional institutions. This wave of innovation is reshaping the cross-border payment industry in Africa and intensifying competition.

5.1 Market Opportunities and Real Challenges

Challenges:

Lack of a true intra-African clearing and settlement system. Payments require USD settlement, increasing costs and reducing efficiency.

Absence of a unified African forex market. Insufficient liquidity in local currencies leads to high currency exchange costs.

Limited interoperability between banks and fintech companies. Financial institutions operate in silos, leading to inefficiencies.

Slow adoption of PAPSS. Regulatory hesitance and liquidity constraints are slowing the progress of regional payment initiatives.

Over-reliance on SWIFT for cross-border transactions. African banks depend on expensive international payment networks.

Opportunities:

Real-time gross settlement (RTGS) systems capable of enabling instant transactions within Africa without relying on USD.

Decentralized forex liquidity pools that facilitate African currency trading without correspondent banks.

Standardized API layers aimed at improving interoperability between banks and fintech companies.

Pan-African instant payment channels (similar to SEPA in Europe) aimed at unifying fragmented payment systems.

Alternatives to SWIFT for African banks to reduce reliance on expensive international networks.

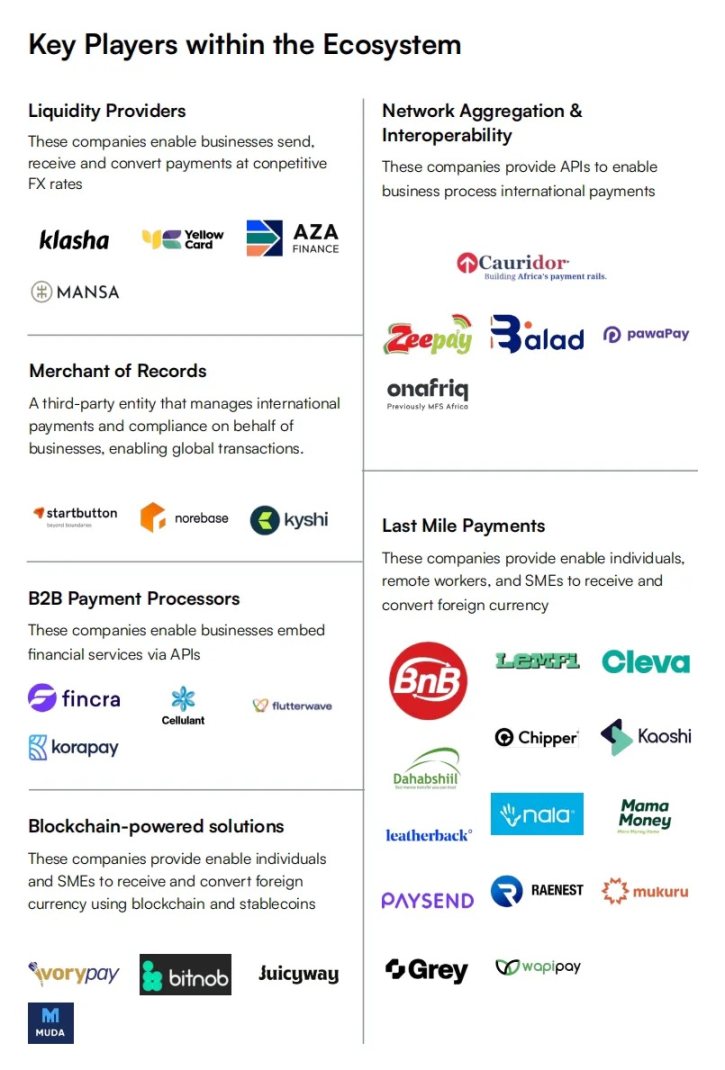

5.2 The Landscape of Fintech Disruptors

In response to the aforementioned opportunities and challenges, we can see the power of financial disruptors:

The emergence of B2B Payment Processors (these companies enable businesses to embed financial services through APIs) and Last Mile Payments providers (these companies allow individuals, remote workers, and SMEs to receive and exchange foreign currency) has significantly reduced transaction costs, often by 50% to 80% compared to traditional channels. Fintech platforms can now provide near-instant settlements within hours, significantly shortening the processing time that banks typically require, which is 2 to 5 days. Nevertheless, the entry barriers in this segment are relatively low, leading to intense competition and declining fees. Companies like Chipper Cash and LemFi have eliminated transaction fees for specific channels, forcing traditional providers to reconsider their pricing strategies.

Liquidity Providers (these companies enable businesses to send, receive, and exchange payments at competitive prices) now offer competitive foreign exchange (FX) pricing and multi-currency settlement services, filling the gaps left by traditional banks in capital controls and dollar shortages. However, due to high capital requirements, limited competition, and rapid market entry, this sector still faces challenges in scaling.

Network Aggregation & Interoperability providers (these companies offer APIs for international payments in business processes) address the fragmented mobile payment ecosystem in Africa by enabling seamless cross-border payments. However, regulatory barriers and the dominance of telecom operators hinder the development of this field, necessitating deep market integration and strategic partnerships.

As fintech companies steadily increase their market share, banks and traditional providers are responding to the changing landscape of cross-border payments in Africa. Established companies like Western Union and MoneyGram have taken measures to reduce fees and integrate mobile payment platforms, while banks are increasingly collaborating with fintech companies to innovate and enhance customer experience. Although traditional SWIFT-based transactions still hold significant importance, fintech solutions are gradually attracting users by offering faster and more cost-effective alternatives, fostering broader innovation across the industry.

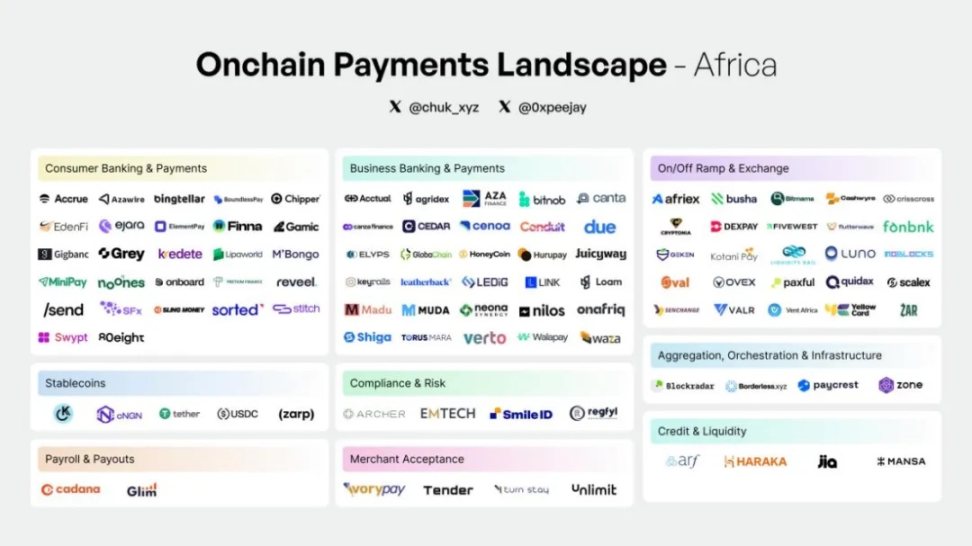

In addition to the fintech-focused perspective presented by Oui Capital, Chuk from Paxos has also drawn an ecosystem map covering African payment channels, use cases, and companies to showcase the depth of the impact that Africa's stablecoin revolution has had, focusing on Africa's role in shaping its financial future.

(Mobile Money to Global Money: Africa's Stablecoin Revolution, Chuk @ Paxos)

Looking ahead, Africa's cross-border payment industry is expected to experience further price declines, increased adoption of stablecoins, enhanced interoperability between financial institutions, and deeper collaboration between banks and fintechs. The most successful companies will expand efficiently, adeptly navigate regulatory frameworks, and provide seamless and reasonably priced transaction services. As competition intensifies, traditional institutions must innovate rapidly, or they risk being marginalized in Africa's rapidly digitizing financial ecosystem.

### VI. Risks and Challenges in Fintech Development

Fintech companies in the cross-border payment sector face multiple challenges that affect their scalability, profitability, and long-term sustainability. These challenges stem from the regulatory environment, financial risks, and intense competition. The following are the main risks and constraints limiting fintech development:

6.1 Regulatory Uncertainty

Navigating a complex and ever-changing regulatory environment remains one of the biggest obstacles fintech companies face in operating in the cross-border payment space.

Diverse Compliance Requirements: Each country/region has its own financial regulations, anti-money laundering (AML) rules, and capital controls, making cross-border operations cumbersome.

Licensing and Approval: Obtaining the necessary remittance licenses across jurisdictions can be costly and time-consuming, with regulatory approvals potentially taking months or even years.

Data Protection and Privacy Laws: Compliance with regulations such as the General Data Protection Regulation (GDPR) in Europe, the Data Protection Act in Nigeria, and the Protection of Personal Information Act in South Africa adds additional complexity, especially regarding data localization requirements.

Sanctions and Fraud Prevention: Cross-border transactions are subject to strict scrutiny from global financial regulations like the Financial Action Task Force (FATF), making compliance an ongoing challenge.

Example: The closure of cryptocurrency remittance services in Nigeria due to stringent regulatory crackdowns highlights the unpredictability of fintech operations in emerging markets.

6.2 Credit, Forex Lending, and Funding Risks

Many fintech companies, especially those involved in forex trading, provide credit to customers through forex position loans or liquidity support. However, this introduces risks related to counterparty defaults, currency fluctuations, and poor fund management.

Forex Liquidity Provision and Position Loans:

When businesses and fintech companies need to settle cross-border payments but lack immediate forex channels, forex providers can act as a source of liquidity. They extend credit in the required currency, allowing transactions to be executed before full settlement. If clients fail to repay or encounter delays, forex providers face risks.

Forex Volatility Risk: Exchange rates fluctuate continuously, and sudden currency devaluations can lead fintech companies to default on forex position loans. Forex providers facing significant exchange rate volatility may struggle to maintain liquidity, especially in deteriorating local market conditions.

Chain Reactions in the Ecosystem: If multiple fintech companies default, liquidity shortages can arise, widening spreads and transaction costs across the market. Banks and liquidity providers may respond by tightening credit limits, increasing collateral requirements, or raising fees, further pressuring fintech companies financially.

Funding Management Risks: Most forex companies generate income through bid-ask spreads.

However, without sound funding management practices, such as accurate forex spread pricing, reasonable balance sheet allocation, and effective currency hedging, they face the risk of substantial losses. Poor cash flow management can quickly deteriorate, putting the company at risk of bankruptcy.

6.3 Market Competition and Profitability Pressure

Competition in the fintech space is intensifying, making differentiation and long-term profitability increasingly difficult.

Established Competitors: Traditional banks, global remittance giants (Western Union, MoneyGram), and large fintech companies (Wise, Revolut) dominate key markets. However, African fintech companies like LemFi, Geegpay, and Chipper Cash have made significant strides, offering more localized and cost-effective solutions for cross-border payments.

These companies leverage digital wallets, multi-currency accounts, and direct integration with mobile payment platforms to streamline transaction processes, reduce costs, and shorten settlement times. Their rise highlights the intensifying competition in Africa and the shift towards fintech-driven remittance solutions.

Price Wars and Thin Margins: Many fintech companies are competing to lower transaction fees, which reduces profitability and makes scaling more challenging. The average transaction fee for African fintech companies ranges from 0.5% to 2% per transfer, significantly lower than the 5% to 10% fees charged by traditional remittance service providers like Western Union and MoneyGram. Some companies, such as LemFi and Geegpay, offer zero or near-zero fee transactions to attract users, further squeezing their profit margins. While this pricing strategy helps gain market share, it may lead to sustainability challenges, requiring fintech companies to diversify revenue sources through forex spreads, subscription models, and embedded financial services.

Customer Acquisition Costs (CAC): High costs associated with acquiring and retaining users increase expenses, especially in emerging markets where fintech adoption is growing, but customer education remains a challenge. The customer acquisition cost (CAC) for fintech companies typically ranges from $5 to $30 per user, while lifetime value (LTV) largely depends on transaction frequency and additional financial services. In a competitive market, marketing expenses and new user incentives further erode profitability, making long-term sustainability a challenge.

6.4 Infrastructure and Liquidity Constraints

Fintech companies often struggle to access banking infrastructure and liquidity, impacting their ability to scale effectively.

Dependence on Partner Banks: Many fintech companies rely on traditional banks for cash deposit and withdrawal services, limiting their independence and increasing costs.

Slow Settlement Times: The lack of real-time settlement solutions for cross-border transactions increases delays and affects user experience.

Liquidity Risks in Emerging Markets: Managing liquidity across multiple currencies without strong banking support remains a major bottleneck. Forex fintech companies typically rely on a network of liquidity providers, correspondent banks, and market makers to access currency on demand. This dependency introduces significant risks, including currency mismatches, high transaction fees (ranging from 0.5% to 3% per transaction), and exchange rate volatility risks. Without robust funding management practices, fintech companies may struggle to maintain adequate liquidity buffers, leading to potential settlement failures, rising borrowing costs, and decreased transaction efficiency. Real-time forex settlement solutions and partnerships with stablecoin issuers are emerging strategies to mitigate these risks and improve liquidity management in the industry.

### VII. Conclusion and Recommendations

Driven by the increasing prevalence of digital applications, rising mobile money penetration, and the dominance of fintech, Africa's cross-border payment market is poised for significant growth. As more individuals and businesses seek cost-effective, faster, and more convenient payment solutions, remittance volumes within Africa are expected to continue rising.

With the emergence of regional payment networks like PAPSS, reliance on SWIFT-based correspondent banking may decline, reducing transaction costs and improving settlement efficiency. Additionally, crypto remittances and stablecoins are increasingly favored as alternatives to traditional forex and banking systems, providing seamless, low-cost cross-border payment services. However, regulatory challenges and liquidity constraints remain key barriers to widespread adoption.

For fintech founders:

Addressing the payment and trade financing issues of SMEs (high costs and inefficiencies in B2B transactions) presents significant opportunities. Additionally, collaborating with mobile payment providers to build interoperability in the financial system will lead to exponential market growth. In terms of scenario segments, expanding beyond P2P remittances into areas such as embedded financial services (loans, insurance, working capital solutions) will enhance profit margins.

For investors:

Prioritize infrastructure investments, as the largest gaps (PAPSS adoption rates, forex liquidity solutions, API interoperability) present opportunities exceeding $10 billion. Secondly, keep an eye on fintech connectors: currently, interoperability will drive fintech adoption faster than cryptocurrencies. Finally, focus on high-frequency, low-cost transactions: winners will achieve scale through transaction volume rather than profit margins.

For policymakers:

Cross-border fintech licensing and a unified African KYC framework will unlock billions of dollars in trapped capital, necessitating a robust regulatory coordination mechanism. Additionally, to support blockchain-based settlements, governments can trial stablecoin-supported settlement networks instead of restricting cryptocurrencies to curb this bottom-up trend. Finally, accelerate the adoption of PAPSS: strengthen regional banking integration to reduce Africa's reliance on the dollar for internal trade.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。