作者:Haseeb >|<

编译:深潮TechFlow

为“指数增长的辩护”正名

过去,我常对创业者们说,你在项目发布后收到的反应不会是“讨厌”,而是“冷漠”。因为默认情况下,没有人会在意你推出的新区块链。

但现在,我必须停止这么说了。本周,Monad 刚刚发布,而我从未见过一条刚上线的区块链引发如此多的“讨厌”。我已经在加密领域专业投资超过7年了。在2023年之前,我见过的几乎每一条新链上线时,迎来的要么是热情,要么是冷漠。

然而现在,新链一诞生,就会被“讨厌”的合唱声包围。我所见过的对 Monad、Tempo、MegaETH 等项目的批评者数量——甚至是在它们主网还未上线之前——确实是一种全新的现象。

我一直在试图分析:为什么这种情况现在开始发生?这又反映了这个市场的心理状态?

“药比病更糟”

提前提醒一下:这可能是你读过的关于区块链估值最模糊的一篇文章。我没有任何华丽的数据指标或图表来打动你。相反,我将试图反驳加密推特(Crypto Twitter)上的主流思潮,而在过去几年里,我几乎一直站在这些思潮的对立面。

在2024年,我感觉自己反对的是一种“金融虚无主义”。金融虚无主义是一种认为这些资产根本没有意义的信念,认为一切最终都不过是“梗文化”,我们所构建的一切本质上都是毫无价值的。

幸运的是,那种“金融虚无主义”的氛围已经不再存在了,我们终于摆脱了这种困境。

但现在的主流心态可以称之为“金融犬儒主义”:好吧,或许这些东西确实有一些价值,也许并非全是“梗文化”,但它们的估值被严重高估了,华尔街迟早会发现这一点。并不是说所有区块链都毫无价值,而是它们的实际价值可能只有当前交易价格的五分之一甚至十分之一(你看过这些市盈率了吗?)。所以,你最好祈祷华尔街不要戳穿我们的虚张声势,因为一旦他们揭穿,这一切都将灰飞烟灭。

现在,有许多看涨的分析师试图通过乐观的一级区块链(L1)估值模型来对抗这种情绪,拼命抬高市盈率、毛利率和现金流折现(DCF),试图扭转这种悲观的趋势。

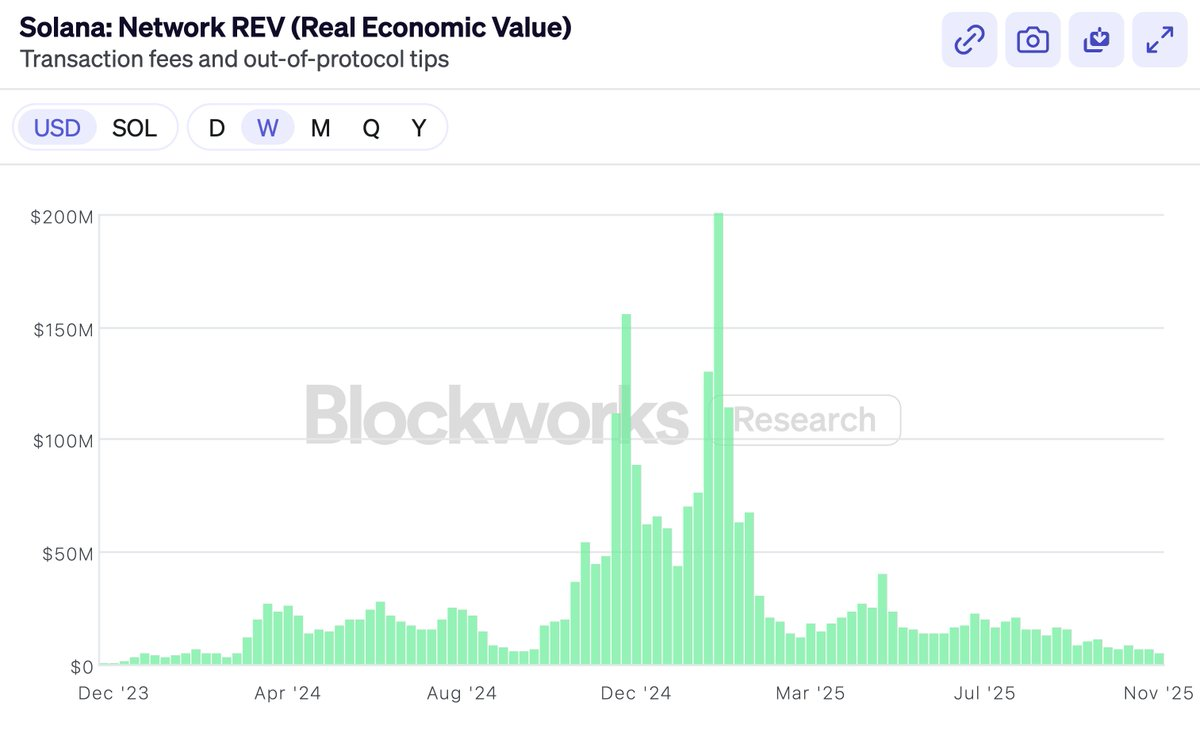

去年年底,Solana(索拉纳)非常自豪地采用了 REV(Realized Economic Value,实现经济价值)作为一个能够最终证明其估值合理性的指标。他们骄傲地宣布:我们——只有我们——不再对华尔街虚张声势了!

然而,当然,几乎就在 Solana 采用 REV 后不久,这一指标就迅速崩盘了(尽管有趣的是,$SOL 的表现比 REV 本身要好得多)。

这并不是说 REV(Realized Economic Value,实现经济价值)本身有问题。REV 确实是一个非常聪明的指标。但这篇文章的重点并不是讨论指标的选择。

接着是 Hyperliquid 的推出。一个去中心化交易所(DEX),它有真正的收入、回购机制和市盈率(PE 倍数)。于是,市场的声音响起了——看吧,我早就说过!终于,第一次有了一个真正盈利并拥有合理市盈率的代币。(别提 BNB,我们不讨论它。)Hyperliquid 将吞噬一切,因为显然以太坊(Ethereum)和索拉纳(Solana)并没有真正赚钱,我们现在可以停止假装为它们估值了。

Hyperliquid、Pump、Sky,这些以回购为核心的代币都很出色。但市场一直都有投资交易所的能力。你随时可以购买 Coinbase 的股票,或者 BNB,或其他类似产品。我们也持有 $HYPE,我也同意它是一个非常棒的产品。

但这并不是人们投资 ETH 和 SOL 的原因。一级区块链(L1)不像交易所那样拥有高额利润率,并不是人们购买它们的理由——如果他们想要那样的利润率,他们可以直接去买 Coinbase 的股票。

所以,如果我并不是在批评区块链的财务指标,也许你会以为这篇文章是要指责代币工业体系的“罪恶”。

显然,在过去一年里,每个人都在代币上亏了钱,包括风投机构(VCs)。今年山寨币(Alts)的表现非常糟糕。因此,加密推特(Crypto Twitter)上的另一半主流声音开始争论谁该为此负责。是谁变得贪婪了?是风投机构贪婪吗?是 Wintermute 贪婪吗?是币安(Binance)贪婪吗?是流动性挖矿的农民们贪婪吗?还是创始人们贪婪?

当然,答案和以往一样,从未改变过。

每个人都贪婪。每一个人——风投机构(VCs)、Wintermute、流动性挖矿的农民、币安(Binance)、意见领袖(KOLs),他们都贪婪,你也一样。但这并不重要。因为任何一个正常运作的市场都不需要参与者违背自身利益行事。如果我们对加密行业的未来判断是正确的,那么即使每个人都贪婪,投资依然可以成功。试图通过分析“谁更贪婪”来解释市场下跌,就像举办一场无意义的“猎巫审判”。我可以保证,没人是从 2025 年才开始变得贪婪的。

所以,这也不是我想写的内容。

很多人希望我写一篇关于为什么 $MON 应该值 X 或 $MEGA 应该值 Y 的文章。但我对此并无兴趣,也不会建议你去买任何特定的资产。事实上,如果你本身就对这些项目没有信心,那么你可能根本不该买它们。

那么,新挑战者链(新兴公链)会胜出吗?谁知道呢。但如果它确实有胜出的可能性,那么它的定价就会基于这种可能性。如果以太坊(Ethereum)市值是 3000 亿美元,索拉纳(Solana)市值是 800 亿美元,那么一个有 1%-5% 几率成为下一个以太坊或索拉纳的项目,其价格也会按照这种概率进行定价。

加密推特(CT)对此感到震惊,但这其实与生物科技领域并无不同。一种治愈阿尔茨海默病可能性不足 10% 的药物,即便有 90% 的概率无法通过三期临床试验最终归零,市场仍会给它数十亿美元的估值。这就是数学的逻辑——而事实证明,市场在做数学计算这方面很擅长。二元结果的定价基于概率,而不是基于当前的收益表现或道德评判。这就是“闭嘴,计算”(shut up and calculate)式的估值逻辑。

我真的不觉得这是一个值得写的有趣话题。“5% 的胜出概率?不可能,这明明是 10% 的概率!”对于任何个别代币来说,市场而非文章才是评估这种概率的最佳方式。

所以,我真正想写的内容是:加密推特似乎已经不再相信公链本身是有价值的。

我并不认为这是因为人们不相信新链能够赢得市场份额。毕竟,我们刚刚见证了 Solana 在不到两年的时间里从废墟中崛起并主导了市场份额。这并不容易,但显然是可能的。

更大的问题在于,人们开始相信,即使一条新链赢得了竞争,也没有值得争夺的奖品。如果 $ETH 只是一个“梗”(meme),如果它永远无法产生真正的收入,那么即使你赢了,它也不可能值 3000 亿美元。这个竞争本身就不值得参与,因为这些估值全是虚假的,在你去领取“奖品”之前,一切都会崩塌。

对链估值持乐观态度已经变得过时了。当然,这并不意味着没有人乐观——显然,总有人是乐观的。毕竟,每个卖家背后都有买家,尽管加密推特(CT)上的“酷孩子”们热衷于嘲讽一级公链(L1),但仍然有人愿意以 $140 买入 SOL,以 $3000 买入 ETH。

然而,现在有一种普遍的看法,认为所有聪明人都已经放弃购买智能合约链了。聪明人知道这场游戏已经结束了。如果不是现在结束,那也很快会结束。现在还在买的人被认为是“冤大头”——比如优步司机、Tom Lee,或者那些说“万亿美元市场”的 KOL们。也许还有美国财政部。但“聪明的钱”(smart money)不会再进场了。

这完全是胡扯。我不相信这种说法,你也不该相信。

因此,我觉得我有必要写一篇“聪明人宣言”,来解释为什么通用型公链是有价值的。这篇文章不是关于 Monad 或 MegaETH 的,而是为 ETH 和 SOL 辩护。因为如果你相信 ETH 和 SOL 是有价值的,那么剩下的一切自然会顺理成章。

作为一名风投(VC),为 ETH 和 SOL 的估值辩护通常并不是我的工作,但该死的,如果没有人愿意站出来做这件事,那我就来写这篇文章吧。

感受“指数增长”的力量

我的合伙人 Bo 曾亲身经历中国互联网的爆发式增长,那时他是一名风险投资人(VC)。这些年来,我听过无数次“加密就像互联网”的类比,听到都已经麻木了。但每当我听到他的故事时,总会让我想起,在这些重大趋势上出错的代价有多么高昂。

他经常讲的一个故事,是关于2000年代初期,当时所有早期投资电子商务的风投(当时这个圈子还很小)聚在一起喝咖啡。他们争论:电子商务的市场到底会有多大?

会主要集中在电子产品上吗(也许只有技术宅会用电脑购物)?女性会用吗(可能她们太注重触感了)?食品呢(或许生鲜食品根本无法管理)?这些问题对早期风投来说至关重要,因为它们决定了该投什么项目以及愿意支付什么价格。

当然,最终的答案是,所有这些人都大错特错。电子商务最终销售一切,而目标用户就是全世界。但在当时,没有人真正相信这一点。即使有人相信,说出来也会显得荒谬至极。

你只能等足够长的时间,让“指数增长”来告诉你真相。即便在那些相信电子商务的人之中,真正认为它会变得如此庞大的也寥寥无几。而那些少数真正相信的人,几乎都因为坚持不卖出而成为了亿万富翁。至于其他的风投——正如 Bo 告诉我的,因为他就是其中之一——都卖得太早了。

在加密领域,相信“指数增长”已经变成了一件过时的事情。

但我依然相信加密领域的指数增长。因为我亲身经历过它。

这是亚马逊从 1995 年到 2019 年的利润表(P&L),整整 24 年。红色代表收入,灰色代表利润。你看到末尾那小小的波动了吗?灰色线开始向上,那是亚马逊在成立 22 年后,第一次真正开始盈利的时候。

亚马逊成立 22 年后,这条灰色的净利润线才第一次从 0 上翘。而在此之前的每一年,都有专栏文章、批评者和做空者声称亚马逊是一个永远赚不到钱的庞氏骗局。

以太坊刚刚满 10 岁。而这,是亚马逊前 10 年的股票表现:

十年的震荡。在这期间,亚马逊一直被质疑者和不信任者所包围。电子商务是风投补贴的慈善事业吗?他们只是在向那些追求便宜货的消费者出售低价、低质量的小商品,这有什么意义?它们怎么可能像沃尔玛(Walmart)或通用电气(GE)那样真正赚钱?

如果你当时在讨论亚马逊的市盈率(P/E Ratio),那你完全搞错了方向。市盈率属于线性增长的范畴,而电子商务并不是一个线性趋势。因此,那些在 22 年间以市盈率为依据进行争论的人,全都大错特错。不论你支付了多少,不论你何时买入,你的看涨程度都不够。

因为这就是指数增长的特性。当涉及真正的指数型技术时,不管你认为它能变得多大,它总是会变得更大。

这正是硅谷比华尔街理解得更透彻的地方。硅谷成长于指数增长,而华尔街则习惯了线性增长。而在过去几年里,加密行业的重心逐渐从硅谷转移到了华尔街。这种变化是显而易见的。

当然,加密行业的增长看起来并不像电子商务那样平滑。它更为波动,呈现出间歇性爆发的特性。这是因为加密行业与金钱息息相关,深受宏观经济因素的影响,同时也面临比电子商务更为剧烈的监管拉锯。加密行业直击国家的核心——货币,因此,它对政府的冲击比电子商务要大得多,也更让人不安。

但指数增长的趋势并不会因此而减少。这或许是个粗糙的论点,但如果加密行业确实是指数型的,那么这个粗糙的论点就是正确的。

拉远视角。

金融资产渴望自由。它们渴望开放,渴望互联互通。加密技术将金融资产转化为文件格式,让发送一美元或一只股票变得像发送 PDF 一样简单。加密技术让一切可以与一切对话,使其全天候运作、全球化、互联且开放。

这种模式一定会胜出。开放永远会胜出。

如果互联网教会了我一件事,那就是这一点。既得利益者会奋力抗争,政府会大声反对,但最终,他们会在这种技术所带来的普及性、创造力以及纯粹的效率面前妥协。这正是互联网对其他行业所做的一切。而区块链将以同样的方式吞并整个金融和货币领域。

是的——只要时间足够长——所有的一切。

有句老话说:“人们高估了两年内会发生的事情,却低估了十年内会发生的事情。”

如果你相信指数增长,如果你将视角拉远,那么一切仍然显得便宜。而更应该让你感到谦逊的是,每一天,那些持有者都在超越卖出者和质疑者。大资本的时间视野比加密推特(CT)上的短线交易者让你相信的要长得多。大资本通过历史学会了不要轻易放弃对重大技术的押注。你知道吗?那个最初让你买入 $ETH 或 $SOL 的动人故事?大资本也相信那个故事,并且从未停止相信。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。