Summary of 2024, Outlook for 2025

Author: Coinbase | Plain Language Blockchain

In just the past year, the United States has approved Bitcoin and Ethereum spot ETFs, and significant progress has been made in the tokenization of financial products, the growth of stablecoins, and the integration of global payment frameworks. These achievements did not happen overnight; while they may seem like the result of years of effort, more signs indicate that this is just the beginning of a larger transformation.

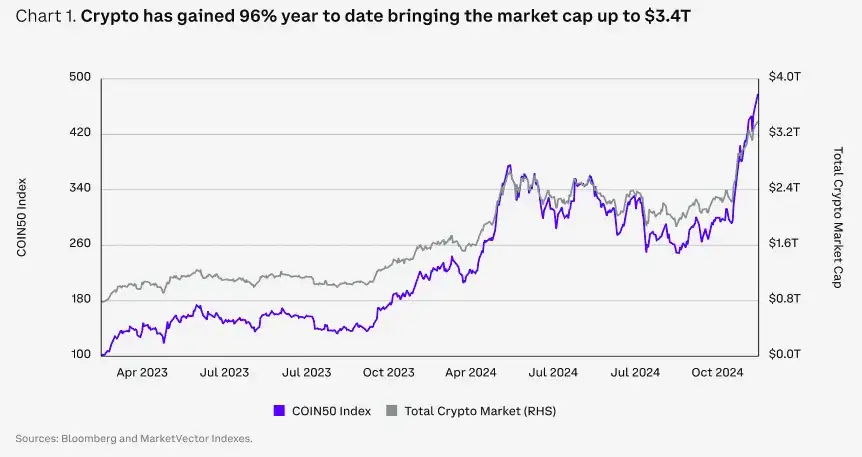

From a market perspective, the upward trend in 2024 differs from previous bull markets. On the surface, "web3" is gradually being replaced by the more fitting term "onchain"; more fundamentally, demand driven by fundamentals is gradually replacing narrative-driven investment, closely related to the deepening participation of institutional investors.

Bitcoin's market dominance has significantly strengthened, and decentralized finance (DeFi) has broken the boundaries of blockchain technology, driving the formation of a new financial ecosystem. Global central banks and major financial institutions are also exploring how to enhance the efficiency of asset issuance, trading, and record-keeping through crypto.

Looking ahead to 2025, the crypto market is poised for transformative growth. Coinbase covers various aspects of the crypto ecosystem, from altcoins, ETFs, staking to gaming, providing a comprehensive and in-depth analysis for the outlook of the crypto market in 2025. Below are key excerpts.

01

Macroeconomic Trends in 2025

1) The Federal Reserve's Demand and Goals

Donald Trump's victory in the 2024 U.S. presidential election has become the biggest catalyst for the crypto market in the fourth quarter of 2024, driving Bitcoin prices significantly higher, exceeding the three-month average by 4-5 standard deviations.

Looking ahead, we believe that the impact of fiscal policy in the short term may not be as significant as the long-term trends of monetary policy, especially as the Federal Reserve approaches a critical decision-making moment. It is expected that by 2025, the Federal Reserve may continue to ease monetary policy, but the pace of easing may be influenced by future fiscal expansions, such as tax cuts and tariffs that could drive up inflation. Although the overall CPI (Consumer Price Index) has fallen to 2.7%, the core CPI remains around 3.3%, above the Federal Reserve's target.

The Federal Reserve aims to achieve a slowdown in price growth through "de-inflation" while maximizing employment, i.e., controlling the pace of price increases. However, American households prefer to see prices fall, but deflation could lead to economic recession, posing greater risks.

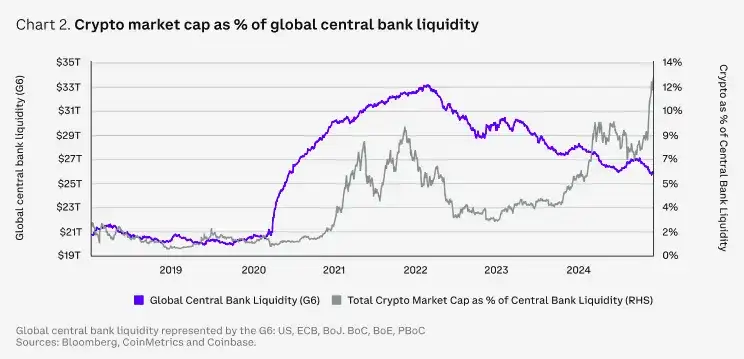

The most likely scenario currently is a soft landing, thanks to declining long-term interest rates and the unique advantages of the U.S. A rate cut by the Federal Reserve is almost a foregone conclusion, and easing credit conditions will also support crypto performance in the next 1-2 quarters. Additionally, if the next government implements budget deficit spending, with more dollars circulating in the economy, risk appetite (including the purchase of crypto) may further increase.

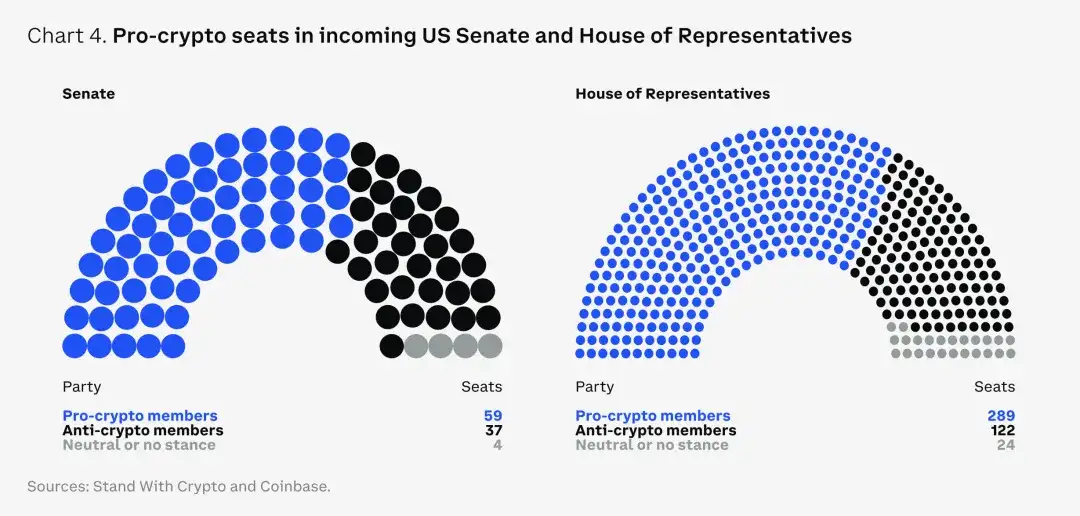

2) The Most Crypto-Friendly U.S. Congress in History

After years of political ambiguity, we believe the next legislative session could be a key moment for the U.S. to finally establish regulatory clarity for the crypto industry. This election sent a strong signal to Washington: the public is dissatisfied with the existing financial system and desires change. From a market perspective, bipartisan support for crypto in both the House and Senate means that U.S. regulation is likely to shift from being a hindrance to a driving force, becoming a positive factor for crypto performance in 2025.

The new focus of discussion is the establishment of strategic Bitcoin reserves. After the Bitcoin Nashville Conference in July 2024, Wyoming Senator Cynthia Lummis introduced the "Bitcoin Bill," and Pennsylvania also launched a similar bill allowing up to 10% of state general funds to be invested in Bitcoin or crypto assets. Michigan and Wisconsin have included crypto in pension investments, and Florida is following suit. However, creating strategic Bitcoin reserves may face challenges, such as legal restrictions on the Federal Reserve holding crypto assets on its balance sheet.

Meanwhile, the U.S. is not the only region making regulatory progress. The rising global demand for crypto is also changing the landscape of international regulatory competition. Looking overseas, the EU's Markets in Crypto-Assets Regulation (MiCA) is being implemented in phases, providing a clear regulatory framework for the industry. Many G20 countries and major financial centers, such as the UK, UAE, Hong Kong, and Singapore, are also actively developing regulatory rules to adapt to digital assets, creating a more favorable environment for innovation and growth.

3) Crypto ETF 2.0

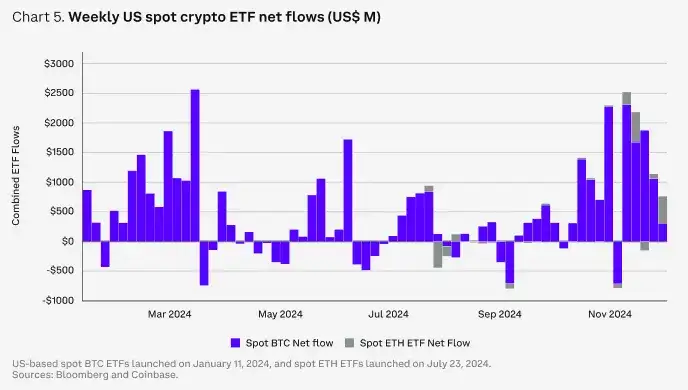

The approval of spot Bitcoin and Ethereum ETFs in the U.S. is a significant milestone for the crypto market. Since their launch, these products have seen net inflows of $30.7 billion (approximately 11 months), far exceeding the $4.8 billion performance of the SPDR Gold ETF in its first year in 2004. According to Bloomberg, this places crypto ETFs in the top 0.1% of approximately 5,500 ETFs launched in the past 30 years.

These ETFs have created new demand for Bitcoin and Ethereum, increasing Bitcoin's market share from 52% at the beginning of the year to 62% by November 2024. The latest 13-F reports show that almost all types of institutional investors—such as endowments, pensions, hedge funds, and family offices—are participating in these products. Meanwhile, U.S. options products launched in 2024 provide investors with lower-cost risk management tools.

Looking ahead, the industry's focus is on whether issuers will expand the asset range of ETFs to include more tokens like XRP, SOL, LTC, and HBAR, but we believe these potential approvals may only benefit a limited group of assets. More importantly, what impact would it have if the U.S. Securities and Exchange Commission (SEC) allows ETFs to use staking features or relax restrictions to allow ETF shares to be created and redeemed through physical assets rather than just cash? The current cash model leads to settlement delays, deviations between share prices and net asset value (NAV), and higher trading costs. In contrast, a physical model is expected to improve price alignment, narrow bid-ask spreads, reduce trading costs, and minimize price volatility and tax implications, thereby enhancing market efficiency.

4) Stablecoins: The "Killer Application" of Crypto

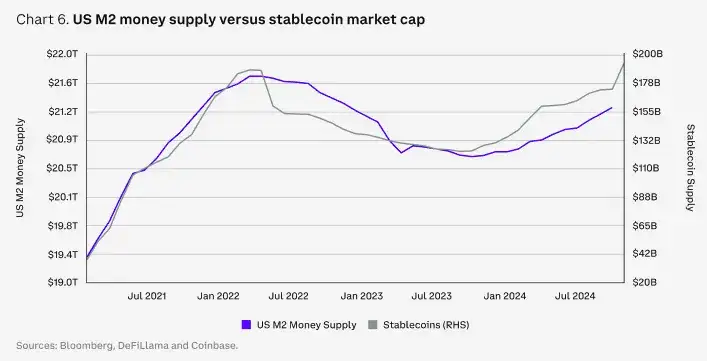

In 2024, the stablecoin market experienced significant growth, with a total market capitalization increase of 48% as of December 1, reaching $193 billion. Some market analysts believe that, following the current development trend, the stablecoin market is expected to grow to nearly $3 trillion within the next five years. Although this prediction may seem overly ambitious, almost equivalent to the current size of the entire crypto market, it only represents about 14% of the $21 trillion U.S. money supply, making it not impossible.

We increasingly believe that the next wave of true adoption of crypto may come from the stablecoin and payment sectors, which also helps explain why stablecoins have received such enthusiastic attention over the past 18 months. Compared to traditional payment methods, stablecoins can provide faster and lower-cost transactions, making them increasingly used in digital payments and remittances, with many payment companies accelerating the construction of stablecoin infrastructure. In fact, we may be approaching a moment when the primary use of stablecoins will no longer be limited to transactions but will expand to global capital flows and business interactions. Additionally, the widespread financial applications of stablecoins have also attracted political attention, especially regarding their potential to help address the U.S. debt issue.

As of November 30, 2024, the total trading volume of the stablecoin market reached $27.1 trillion, nearly three times the $9.3 trillion recorded during the same period in 2023 (11 months). This includes a large number of peer-to-peer (P2P) transfers and cross-border business-to-business (B2B) payments. An increasing number of businesses and individuals are beginning to use stablecoins like USDC to meet compliance requirements and deeply integrate with payment platforms like Visa and Stripe. In fact, Stripe acquired the stablecoin infrastructure company Bridge for $1.1 billion in October 2024, marking the largest deal in the crypto industry to date.

5) The Tokenization Revolution

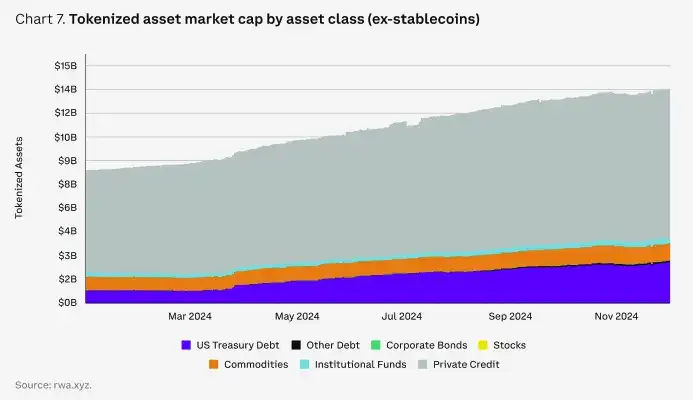

Tokenization made significant progress in 2024. According to data from rwa.xyz, the tokenization of real-world assets (RWA) grew from $8.4 billion at the end of 2023 to $13.5 billion by December 1, 2024, an increase of over 60% (excluding stablecoins). Analysts' forecasts suggest that this market could grow from a minimum of $2 trillion to a maximum of $30 trillion over the next five years, representing an increase of nearly 50 times. Asset management firms and traditional financial institutions, such as BlackRock and Franklin Templeton, are increasingly adopting the tokenization of traditional assets like government bonds on public and permissioned blockchains, enabling near-instant cross-border settlements and 24/7 trading.

Some companies are attempting to use tokenized assets as collateral for other financial transactions (such as derivatives trading), which not only simplifies operations (e.g., margin calls) but also reduces risk. Furthermore, the trend of RWA tokenization has expanded from U.S. Treasury bonds and money market funds to areas such as credit raising, commodities, corporate bonds, real estate, and insurance. Ultimately, tokenization is expected to shift portfolio construction and investment processes onto the blockchain, further simplifying the entire investment process, although this goal may take several years to achieve.

Of course, these efforts also face some unique challenges, including liquidity fragmentation across multiple blockchains and a constantly changing regulatory environment, but significant progress has already been made in both areas.

Overall, we expect tokenization to be a gradual and ongoing process, but the benefits it brings are widely recognized. Now is the best time for companies to experiment, ensuring they can stay ahead in the wave of technological development.

6) The Revival of DeFi

"DeFi is dead, long live DeFi." Decentralized finance (DeFi) suffered significant blows in the last market cycle, as some applications relied on token incentives to attract liquidity, offering high yields that were unsustainable. However, over time, a more sustainable financial system is gradually emerging, one that includes real-world use cases and possesses transparent governance structures.

In our view, changes in the U.S. regulatory environment could be key to reigniting the prospects of DeFi. Specifically, this may include establishing a regulatory framework for stablecoins and providing pathways for traditional institutional investors to enter the DeFi market, especially as the synergy between off-chain and on-chain capital markets deepens. In fact, DEXs currently account for about 14% of CEX trading volume, up from 8% in January 2023. Moreover, the possibility of decentralized applications (dApps) sharing protocol revenue with token holders is becoming increasingly feasible in a more favorable regulatory environment.

Additionally, the disruptive role of crypto in financial services is gaining recognition from more key figures. In October 2024, Federal Reserve Board member Christopher Waller spoke about how to make DeFi complementary to centralized finance (CeFi), suggesting that distributed ledger technology (DLT) could make record-keeping in CeFi more efficient and faster, while smart contracts could enhance CeFi's capabilities. He also noted that stablecoins could bring benefits in payments and as "safe assets" on trading platforms, although they need to take appropriate measures to address risks such as bank runs and illicit finance.

All of this indicates that DeFi is likely to extend beyond the crypto user base and into the traditional finance (TradFi) sector.

02

Disruptive Paradigms

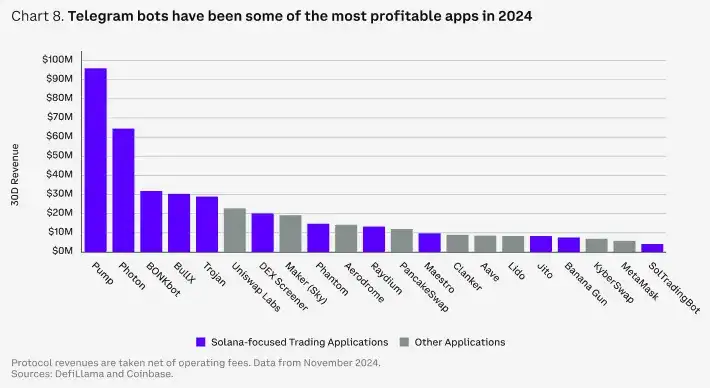

1) Telegram Trading Bots: The Invisible Profit Center in Crypto

After stablecoins and native L1 trading fees, Telegram trading bots have become the most profitable segment in the Crypto space in 2024, even surpassing the net protocol revenue of major DeFi protocols like Aave and MakerDAO (now known as Sky). This trend is primarily driven by increased trading and Memecoin activity. In fact, Memecoins have become the strongest-performing segment in the crypto space in 2024 (measured by market cap growth), with trading activity for Memecoins (on Solana DEX platforms) also surging in the fourth quarter of 2024.

Telegram trading bots are chat-based trading tools. Users can create custodial wallets directly in the chat window and manage deposits and transactions through buttons and text commands. As of December 1, 2024, users of Telegram trading bots are primarily concentrated on Solana (87%), followed by Ethereum (8%) and Base (4%). (Note: Most Telegram trading bots are not associated with The Open Network (TON), which integrates with Telegram's native wallet.) This means that the users these bots serve tend to prefer trading or performing other operations on the Solana blockchain.

Like most trading platforms, Telegram trading bots typically charge around 1% per transaction. However, due to the high volatility of trading assets, users do not seem dissatisfied with these higher fees. By December 1, 2024, the cumulative fees of the highest-earning Photon bot had reached $210 million, close to the $227 million charged by Pump, Solana's largest Memecoin launch platform. Additionally, other major bots like Trojan and BONKbot earned $105 million and $99 million, respectively. In contrast, Aave's total protocol revenue for the entire year of 2024 was $74 million (net income after fees).

We believe the appeal of these bots primarily comes from their convenience in DEX trading, especially for tokens that have not yet been listed on CEXs. Many bots also offer additional features, such as "sniping" capabilities when tokens launch and integrated price alerts. The Telegram trading experience is very user-friendly, with nearly 50% of Trojan bot users using it for more than four days (compared to only 29% of users who stop using it after one day), resulting in an average revenue per user of $188.

While the increasing competition among Telegram trading bots may eventually lead to lower trading fees, we believe that Telegram bots (and other core interfaces discussed below) will continue to maintain their status as leading profit centers in 2025.

2) Prediction Markets: The Sure Bet

Prediction markets may be one of the biggest winners of the 2024 U.S. election cycle, with platforms like Polymarket outperforming traditional polling data that predicts election outcomes. We believe this is a victory for crypto, as blockchain-based prediction markets demonstrate significant advantages over traditional polling data, showcasing the unique application potential of blockchain technology. Prediction markets not only highlight the transparency, speed, and global accessibility brought by crypto technology, but their blockchain foundation also enables decentralized dispute resolution and outcome-based automatic payment settlements, distinguishing them from traditional non-blockchain prediction platforms.

Although many believe these decentralized applications (dApps) may lose popularity after the elections, we have already seen their applications expanding into other areas such as sports and entertainment. In finance, they have proven to be more accurate than traditional surveys in reflecting economic data, such as inflation and non-farm payroll data, suggesting they may continue to develop post-election.

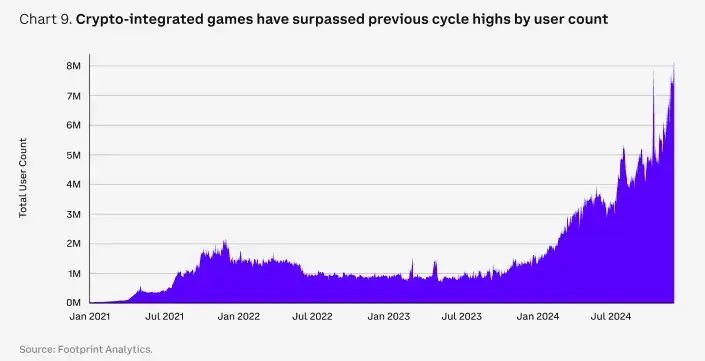

3) Gaming: Controversy Drives Attention

Gaming has always been one of the core themes in the crypto space due to the potentially transformative impact of on-chain assets and markets. However, attracting a loyal user base, especially those loyal players of traditional games, has been a challenge for crypto games. Many players in crypto games are more focused on profit rather than pure entertainment, making it difficult to attract more non-crypto users. Additionally, many crypto games rely on web browser distribution and require the use of self-custody wallets, limiting their audience primarily to crypto enthusiasts rather than mainstream gamers.

However, compared to the last cycle, games integrating crypto technology have seen significant improvements. The key change has been the shift from the initial concept of "fully on-chain ownership of games" to selectively placing assets on-chain, unlocking new features without compromising the overall gaming experience. In fact, we find that many well-known game developers now view blockchain technology as a supplementary tool rather than a core marketing selling point.

"Off the Grid" is a representative of this trend. Although the game's core blockchain component—the Avalanche subnet—was still in testing at launch, it became the top free game on the Epic Games platform. The core appeal of the game lies in its unique gameplay rather than blockchain tokens or item trading markets. More importantly, we believe this game paves the way for crypto-integrated games to enter a broader market, as it is now playable on Xbox, PlayStation, and PC (via the Epic Games Store).

Mobile platforms have also become an important distribution channel for crypto-integrated games, including native apps and embedded applications (such as Telegram mini-games). Many mobile games also selectively integrate blockchain features, but most activities are actually run on centralized servers. Typically, these games can be played without the need for external wallets, lowering the entry barrier and allowing users unfamiliar with crypto to participate.

In our view, the lines between crypto games and traditional games may continue to blur. Upcoming "crypto games" are likely to be games that integrate crypto rather than those that focus entirely on crypto, and we believe they will place greater emphasis on the refinement of gameplay and distribution channels rather than a "play-to-earn" mechanism at their core, which may drive broader adoption of crypto technology, though we are uncertain how it will directly drive demand for liquidity tokens. In-game tokens are likely to be isolated across different games, and we believe that non-crypto enthusiast gamers may not want external investors to influence the in-game economy.

Article link: https://www.hellobtc.com/kp/du/12/5593.html

Source: https://mp.weixin.qq.com/s/hkVVmJVY91D50welhz6Eow

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。