Preface:

The Web3Port Foundation is a cryptocurrency fund dedicated to the blockchain and Web3 ecosystem, committed to promoting the widespread adoption of Web3 technology through strategic investments and incubating innovative startups and projects.

We have recently conducted research on the Web3 payment track and the PayFi track, understanding the overall situation of the track through the study of the concepts, payment types, and typical cases of Web3 payments/PayFi tracks, to assist in business investment decisions. The content is for industry learning and communication purposes only and does not constitute any investment reference.

Web3 Payments

With the expansion of stablecoin volume and the expansion of application scenarios, Web3 payments have become a hot track in the cryptocurrency market. Web3 payments cover numerous business scenarios and categories, including stablecoins, wallets, asset custody, trading, payments, deposits and withdrawals, credit cards, etc. Traditional financial institutions and Web3 entrepreneurs have combined blockchain technology and cryptocurrencies to build numerous Web3 payment projects and use cases.

Concept:

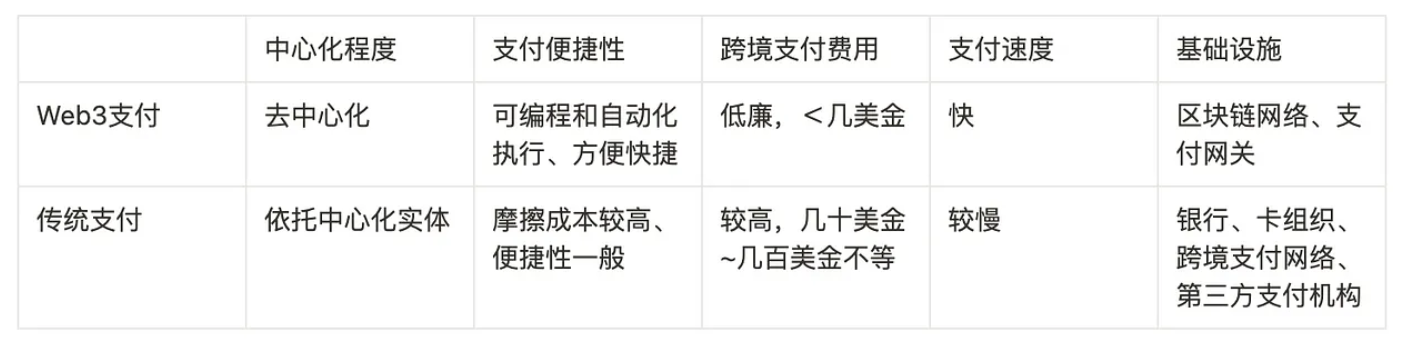

Traditional Payments: Currency transactions conducted through the traditional financial system, usually involving centralized institutions such as banks, credit card companies, and payment processors (such as PayPal, Visa, Mastercard, etc.). The payment process is verified, cleared, and settled by these financial institutions. Traditional payments include cash payments, bank transfers, credit card payments, debit card payments, electronic checks, and e-wallets.

Web3 Payments: Web3 payments are a payment method based on blockchain and cryptocurrency technology, completing transactions through smart contracts, decentralized applications (DApps), and cryptocurrencies. Web3 payments do not rely on traditional financial institutions but instead transfer value directly between users through decentralized networks.

Traditional Payments VS Web3 Payments

Traditional Payments are a set of payment methods based on an account system, with the transfer of value recorded in the accounts of intermediary institutions (such as banks, third-party payment companies). Due to the large number of participants, the process of fund transfer is very cumbersome, and the friction cost is also very high, resulting in high costs.

Web3 Payments are based on the infrastructure of the blockchain network, allowing cryptocurrencies to be transferred between senders and receivers, solving problems such as high costs, low efficiency of cross-border transfers, and high costs in traditional payments.

Types of Web3 Payments

The specific scenarios of Web3 payments include consumers using encrypted assets for on-chain interactions, making payments to enterprises/merchants, cross-border transfers, and encrypted asset payments between enterprises. In summary, there are mainly two types of Web3 payments:

- Deposit and Withdrawal Payments (On Ramp & Off Ramp), which refers to the exchange and payment between cryptocurrencies and fiat currencies. Deposits refer to exchanging fiat currency (Fiat) for cryptocurrencies, while withdrawals refer to exchanging cryptocurrencies for fiat currency.

- Cryptocurrency Payments, including 2 types:

- On-chain native payments: **Refers to using cryptocurrencies to participate in transactions in Web3 native scenarios, such as purchasing NFTs with cryptocurrencies, participating in LaunchPad offerings, swapping between different cryptocurrencies, on-chain transaction fees, etc.;

- Off-chain entity payments: **Refers to directly using cryptocurrencies to purchase goods or services in the offline physical economy, such as using cryptocurrencies to pay for offline consumption orders, cross-border transfer transactions, etc.;

Web3 payments connect fiat currency and cryptocurrencies through deposit and withdrawal payments, and enable the circulation of encrypted assets in payment and consumption scenarios through cryptocurrency payments (on-chain/off-chain payments), thereby building a complete payment ecosystem loop.

Business Models of Web3 Payments

Based on the demand and types of Web3 payment scenarios, common profit models for Web3 payment projects/companies include the following:

- Deposit and withdrawal fees: Users need to pay deposit and withdrawal fees through third-party payment institutions for cryptocurrency and fiat currency transactions. Generally, third-party payment institutions charge a fee of 0.6% of the transaction amount, which is ultimately borne by consumers/merchants and shared among the participants in the payment process (third-party payment institutions, aggregators, issuing banks, and international card organizations).

- Access service fees. This scenario involves aggregating payments and settlement networks, gradually opening up/accessing Web3 payment businesses and scenarios, including wallets, custody, payments, transactions, and stablecoins, and ultimately covering their entire ecosystem to form a logical loop, while charging access service fees.

- Blockchain Gas network fees: When using Web3 payments, the final result of the payment needs to be confirmed and processed on-chain, resulting in blockchain network gas fees.

- Foreign exchange spreads. This only involves cross-border payment products, and as a payment channel for fund transfers between different country currencies, it can avoid banks directly exchanging currencies for users when there are cross-currency transactions, thereby obtaining exchange rate spreads.

Among them, deposit and withdrawal fees and access service fees are the main profit models for Web3 payment projects/companies. These two profit models are highly dependent on network effects (referring to the phenomenon where the value of a product or service increases with the increase in the number of users). The more users and merchants using Web3 payments, the larger the transaction volume, the more revenue can be generated. At the same time, with the increase in the number of users and transaction volume, the market share and influence of the Web3 payment network built by Web3 payment projects/companies will also increase, further promoting their brand and market influence.

Participants in the Web3 Payments Track:

Participating Roles

- Cryptocurrency exchanges: Exchanges generally conduct payment business by issuing credit cards in cooperation with centralized financial systems. In 2020, exchanges such as Coinbase, Binance, and Crypto.com began to offer payment services, cooperating with Mastercard or Visa to issue cryptocurrency credit cards, allowing users with cryptocurrency assets to make global credit card purchases.

- Independent deposit and withdrawal payment institutions: Such as Moonpay, BitPay, Paypal, Stripe, Mastercard, etc., gradually opening up/accessing Web3 payment businesses and scenarios around their main business, including wallets, custody, payments, and stablecoins, and ultimately covering their entire ecosystem to form a logical loop.

- Web3 aggregated payment platforms and Web3 banks: Aggregating multiple independent deposit and withdrawal payment institution interfaces to form an aggregated platform, and providing multi-account banking services for Web3 users. For example, Alchemy Pay is a hybrid cryptocurrency payment gateway solution that supports bi-directional exchange and payment of fiat and cryptocurrency; Fiat24 creates an on-chain bank account for users, providing a series of Web3 banking services such as deposits and withdrawals, encrypted consumption payments, savings, transfers, and currency exchange.

- Cryptocurrency retail terminals: Including cryptocurrency ATMs (head project Bitcoin Depot) and offline convenience store retail terminal POS (typical project Pallapay)

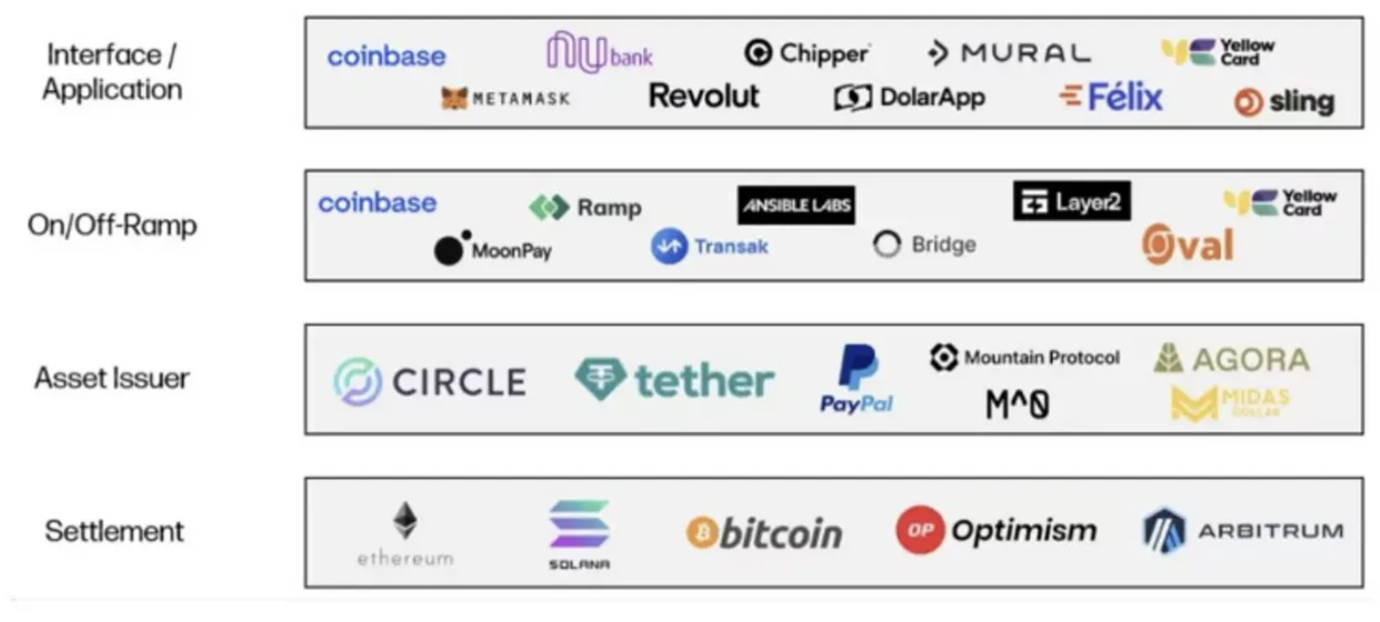

According to Galaxy Ventures' research, participants in the Web3 payment track can be divided into 4 categories from a technical stack perspective:

Typical Projects and Cases:

- Alchemy Pay: Alchemy Pay is a company that provides cryptocurrency and fiat payment solutions, aiming to connect the traditional financial system with the decentralized finance (DeFi) world. Alchemy Pay provides a hybrid payment gateway for merchants and consumers to transact using cryptocurrencies and fiat currencies, simplifying the use and adoption of cryptocurrencies. It plans to expand global coverage of cryptocurrency payments and has obtained over 20 regulatory licenses worldwide. Currently, it has over 2 million users and supports cryptocurrency payments in 180+ countries and regions.

- Fiat24: Fiat24 is a financial technology company licensed by the Swiss Financial Market Supervisory Authority (FINMA). It has launched a Web3 banking protocol driven by smart contracts, creating an on-chain bank account (IBAN+Card) for users and providing a range of Web3 banking services and crypto services including deposits, encrypted consumption payments, savings, transfers, and currency exchange.

- Helio: A platform focused on cryptocurrency payments and Web3, providing tools for receiving, processing, and managing cryptocurrency payments. It is a leading Web3 payment platform on Solana, with over 450,000 unique active wallets and 6,000 merchants. With its Solana Pay plugin, millions of Shopify merchants can now settle payments using cryptocurrencies and convert USDY to other stablecoins such as USDC, EURC, and PYUSD in real-time.

- Moonpay: Moonpay is a global cryptocurrency payment infrastructure provider that allows users to purchase cryptocurrencies using credit cards, debit cards, bank transfers, and other methods. It is a leading project for cryptocurrency deposits and withdrawals, with over 20 million registered users, supporting cryptocurrency payments in over 160+ countries and regions, and facilitating the exchange of over 80 cryptocurrencies and 30+ fiat currencies. It holds payment business licenses in most jurisdictions and has processed over 6 billion transactions.

- BitPay: Founded in 2011, BitPay is a cryptocurrency payment processing company dedicated to helping merchants and individuals use Bitcoin and other cryptocurrencies for payments and transactions. It offers a range of services that enable merchants to accept cryptocurrency payments and convert them into fiat currency, making it easier for users to use cryptocurrencies for daily consumption. BitPay currently enables merchants to accept payments from customers in 229 countries and regions using 16 different cryptocurrencies, and has processed over 10 million transactions with a total value exceeding $5 billion.

- Coinify: Coinify is a cryptocurrency trading and payment processing service provider. Its payment solution allows merchants to accept payments in 10 supported cryptocurrencies and receive payments in their chosen fiat currency. The company operates in over 180 countries and serves over 45,000 merchants.

- CoinPayments: Founded in 2013, CoinPayments is one of the world's leading cryptocurrency payment service providers, serving over 100,000 merchants from 190+ countries/regions. Its payment solution enables merchants to accept payments in over 175 cryptocurrencies. The company also provides various tools for merchants, including shopping cart plugins, payment buttons, APIs, invoice generators, and sales tools. As of October 2022, the company has processed over $10 billion worth of cryptocurrency payments.

- PayPal: In August 2023, PayPal launched the stablecoin "PayPal USD" (PYUSD), pegged to the US dollar, as a bridge for exchanging between fiat and cryptocurrencies for transfers, payments, and other business operations.

- MetaMask: MetaMask itself does not provide direct fiat currency exchange functionality, but through integration with third-party services such as MoonPay, Wyre, and Transak, users can easily convert between fiat and cryptocurrencies (deposit and withdrawal operations). The MetaMask Portfolio DApp has aggregated functions such as Sell, Buy, Stake, Dashboard, Bridge, and Swap, helping users manage assets conveniently and perform unified on-chain asset operations.

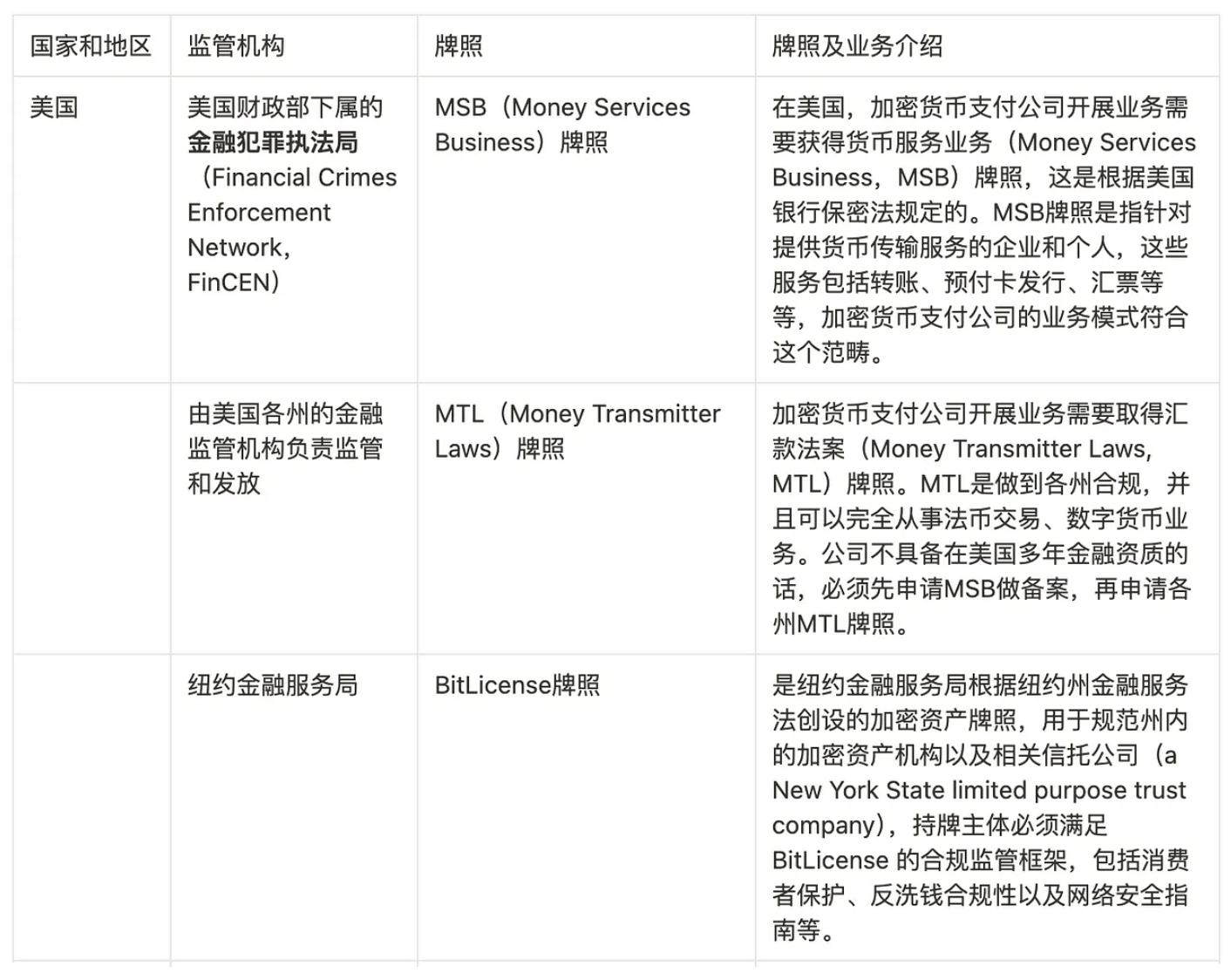

Regulatory Compliance for Web3 Payments

Regarding regulatory compliance for the Web3 payment track, it is mainly necessary to meet licensing, qualifications, and licensing compliance requirements before the project can conduct Web3 payment business in accordance with standards.

Different countries and regions have different regulatory requirements for Web3 payment businesses. Therefore, Web3 payment track projects that want to conduct related business in certain countries and regions need to apply for the corresponding licenses.

PayFi Track Concept, Business Scenarios, and Case Studies

PayFi Concept

Lily Liu, Chair of the Solana Foundation, introduced the concept of PayFi at the Hong Kong Web3 Carnival:

"The motivation of PayFi is to realize the initial vision of Bitcoin payments. PayFi is not DeFi, but a new financial market built around the time value of money, a new financial paradigm and product experience that traditional finance cannot achieve."

PayFi can be understood as the fusion of DeFi and Web3 payments, with a focus on helping users maximize the time value of money. PayFi is applicable to applications in Web3 transactions, offline consumption scenarios, retail environments, creator monetization, accounts receivable, payment processing, private credit pools, etc., creating a new paradigm for on-chain finance through the interoperability, programmability, and composability of blockchain.

PayFi Market Outlook:

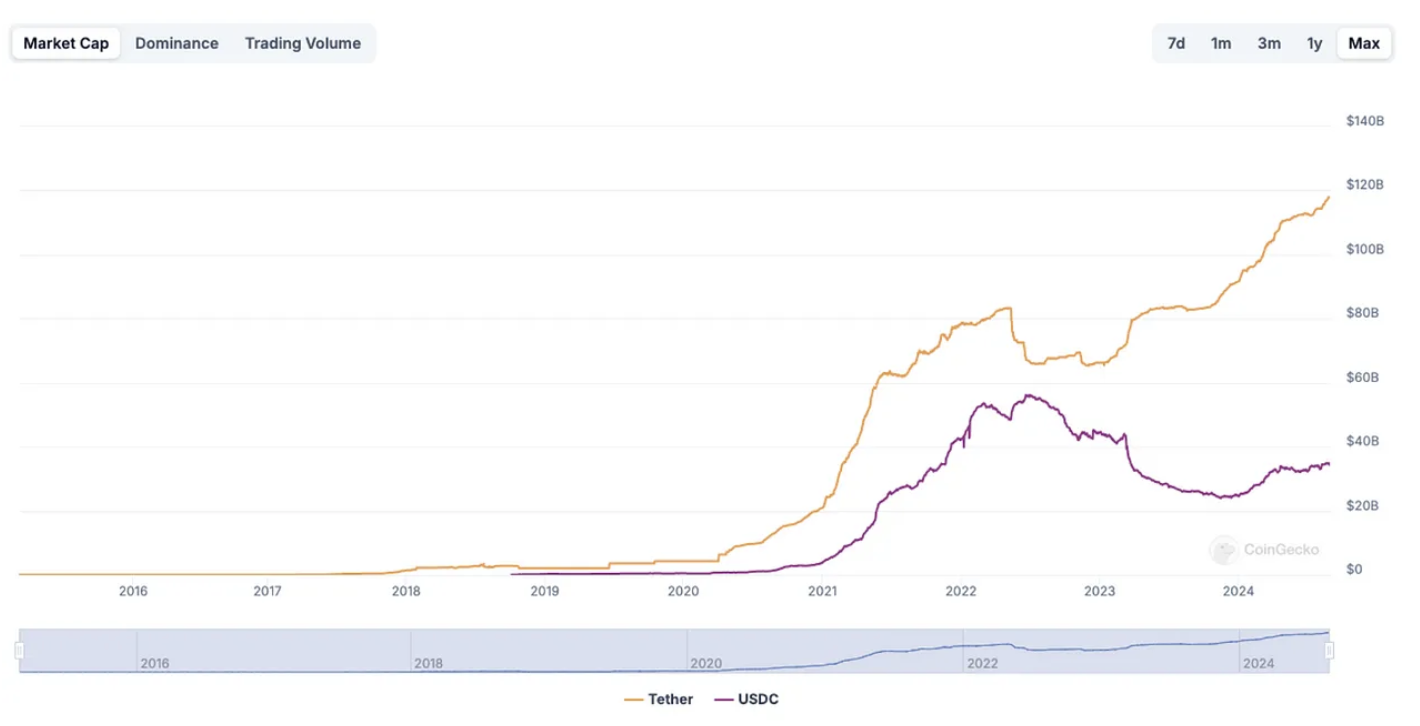

Since 2015, stablecoins have experienced exponential growth, providing effective payment and settlement for the $2 trillion cryptocurrency market. Currently, the overall market value of stablecoins has surpassed $171 billion, with Tether USDT's market value growing from over $83 billion in 2022 to the current $117.9 billion, a 42% increase, demonstrating the significant demand for stablecoins in the cryptocurrency market.

In addition to serving as a pricing unit in cryptocurrency transactions, stablecoins are gradually making strides in traditional payment tracks and cross-border financial trade, reshaping the global payment landscape. The PayFi market, which combines stablecoins and Web3 payments, will further expand the demand for stablecoin use cases, providing financial support for on-chain and off-chain payment applications.

PayFi can:

- Bringing trillions of offline traditional payment volumes onto the chain to better optimize the time value of money.

- Providing sustainable risk-adjusted returns: single to double-digit returns.

- Rapidly scaling with extremely low systemic risk to increase asset liquidity.

- Leveraging the convenience of smart contracts to provide more efficient and diverse new financial paradigm applications.

PayFi Business Scenarios and Case Studies:

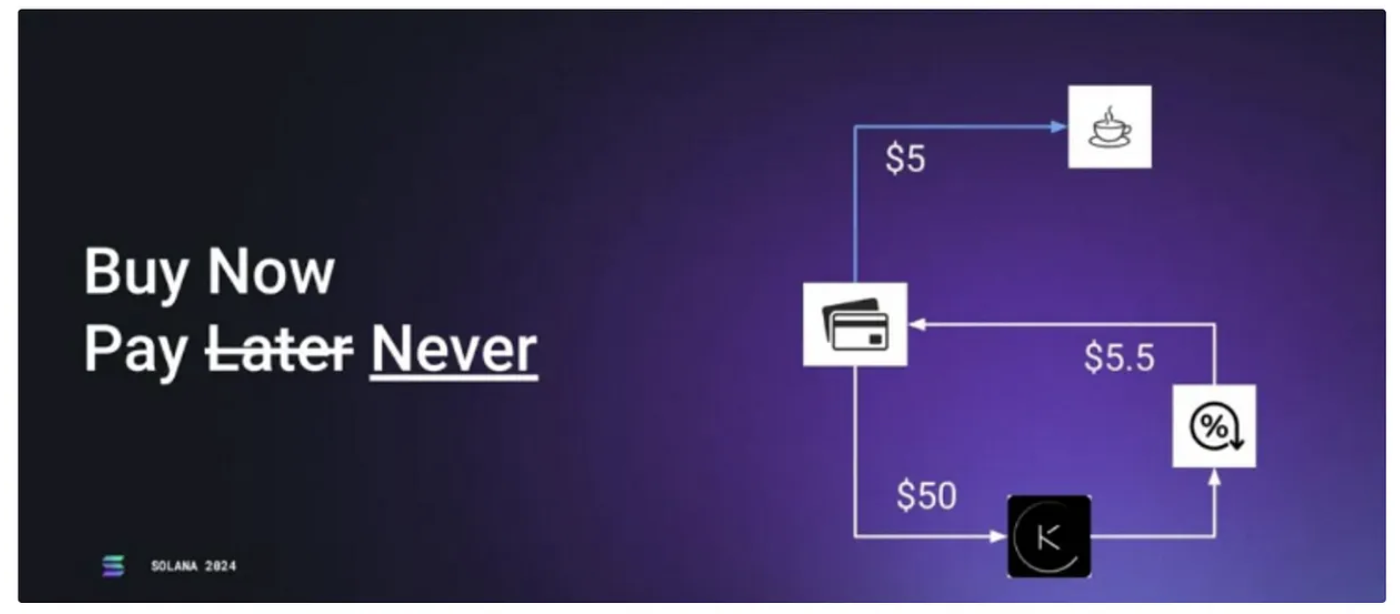

1. Innovative Web3 Payments Integrated with DeFi:

Combining on-chain DeFi finance and instant settlement capabilities, allowing users to use real-time earnings from on-chain DeFi finance to pay for immediate offline consumption expenses.

Case Study: Buy Now Pay Later: Users deposit $50 in an on-chain DeFi protocol and earn interest of $5.5, which can be used for instant settlement and payment to buy a (free) cup of coffee.

2. Web3 Banking:

Combining Web3 and Web2 banking business to provide digital banking services to users.

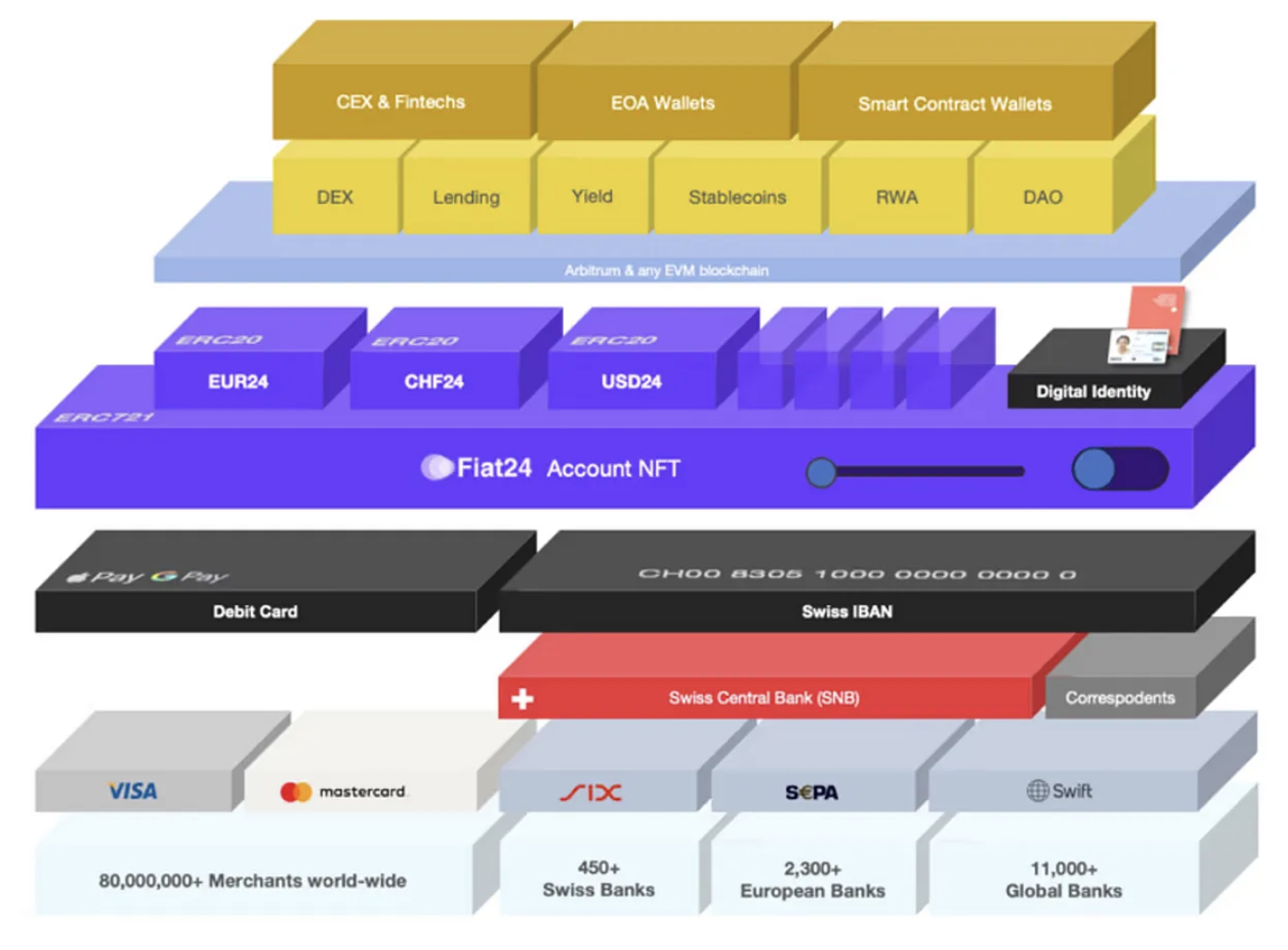

Case Study: Fiat24 is a blockchain-based financial services platform dedicated to providing decentralized digital banking services to users. Fiat24 establishes Swiss bank accounts (Cash Accounts) for KYC-verified users, integrating Web3 payment services for currency acceptance and Web3 payments. Additionally, Fiat24's Swiss bank accounts are directly connected to the Swiss National Bank, the European Central Bank, and the VISA/Mastercard payment network, enabling traditional banking services such as fiat savings, currency exchange, and merchant settlements.

3. RWA Finance:

Bringing offline RWA assets onto the chain to capture the time value of assets and provide more asset investment categories and returns for crypto users.

Case Study: Ondo Finance is an RWA tokenized US Treasury bond protocol, aiming to provide institutional-grade financial products and services to everyone. Ondo Finance tokenizes low-risk, interest-bearing, and scalable fund products (such as US Treasury bonds, money market funds, etc.) to provide a way for on-chain investors to earn stablecoin returns. For non-US users, it has introduced USDY (USD Yield Token), the world's first interest-bearing token backed by US Treasury bonds. USDY can be used for various purposes, including lending, cash management, payments, and earning returns. USDY has made breakthroughs in Web3 payments, allowing users and merchants to use interest-bearing assets for payments or settlements, enabling merchants to earn interest by accepting USDY as a settlement method. More and more projects are starting to use USDY to promote wider adoption of crypto payments.

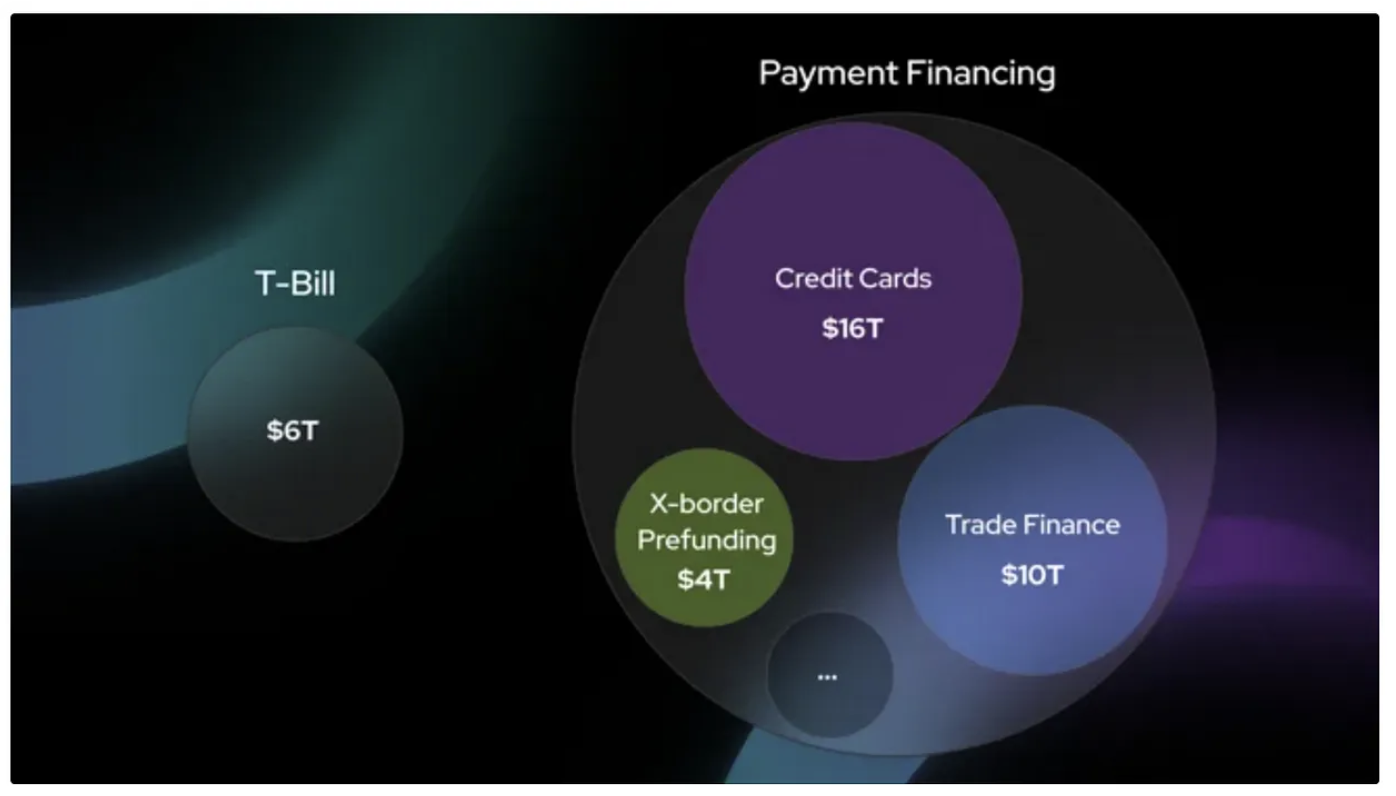

4. Payment Financing:

Using DeFi lending funds to meet financing needs in real payment transaction scenarios, achieving on-chain settlement of payment financing returns.

Case Study: Huma Finance is a PayFi network that allows businesses and individuals to obtain financing and liquidity support for global payments by connecting them with global investors on-chain, using future income as collateral for loans. Specific use cases include cross-border payment financing, digital asset credit cards, RWA instant settlement, trade financing, and DePIN financing.

5. PayFi Crypto Payment Network:

Building a crypto payment network using Web3 payments and blockchain DID identity to adapt to offline payment scenarios.

Case Study: PolyFlow is a modular decentralized protocol for crypto asset operations, aiming to build a PayFi crypto payment network. Through modular design, it has introduced two key components, Payment ID (PID) and Payment Liquidity Pool (PLP), which abstract and separate the information flow and fund flow of payment transactions to extract value. PID is a digital identity system used for KYC identification, identity authentication, compliance access, and data rights, while PLP processes service provider fund flows through smart contracts to manage funds and payment settlements. Polyflow incentivizes merchants and liquidity providers by providing near-risk-free DeFi returns for payment transactions. This model not only opens up new revenue streams but also encourages broader stakeholders to participate in the DeFi ecosystem, driving the development and adoption of crypto payments.

6. Consumer Crypto Payment Applications:

Using on-chain credit and Web3 payments to transform traditional consumer scenarios.

Case Study: Blackbird is a Web3-based loyalty platform for the food and beverage industry, leveraging Blackbird Pay (on-chain credit card) and $FLY (on-chain loyalty points) to build on-chain payments and loyalty programs. It uses payment business as a lever for growth to drive the development of the entire ecosystem. Currently, 40,056 wallets hold 125,571 Blackbird restaurant membership cards (NFT), and 142 restaurants have generated check-in activities.

7. Streaming Payments:

Streaming payments are an emerging payment method that allows the continuous, real-time transfer of value (usually currency or cryptocurrency) from the payer to the payee over a period of time, rather than completing the entire payment at once. Streaming payments are mainly applicable to billing for continuous services or salary payments, such as hourly billing for work, usage-based network services, content subscriptions or consumption, ongoing contracts, and lease payments. In the future, streaming payments will have a profound impact on value flow, working capital management, IoT payments, and even the valuation models of large companies.

Case Studies:

- Sablier is a token distribution protocol that allows the creation of token streams using the Sablier protocol for token ownership, payroll, airdrops, grants, etc., enabling recipients to track and withdraw stream funds at any time. This payment method allows users to make continuous real-time payments down to the second, enabling seamless, frictionless transactions and increasing financial flexibility for users, businesses, and other entities. Sablier uses the passage of time itself as a trust constraint mechanism, unlocking business opportunities that were previously unattainable.

- Zebec is a decentralized infrastructure network designed to create a future where real-world value flows freely and seamlessly, enabling individuals, businesses, investors, and teams to immediately access funds and tokens; providing instant financial control and promoting a more inclusive and accessible financial environment. Zebec's integrated products include RWA payments (real-time payroll and cross-border remittances), on-chain payment infrastructure (Zebec Cards), and connected DePIN (PoS retail devices, providing convenient, real-time, integrated crypto payment processing solutions for merchants and consumers).

Reference Articles:

1. Web3 Payment Research Report: Industry Giants' Full-scale Attack, Expected to Change the Existing Crypto Market Landscape

https://mp.weixin.qq.com/s/oWec4gDu8Hqk86aLs3K9Qw

- Web3 Payment Research Report: From E-Cash, Tokenized Currency, to the Future of PayFi

https://mp.weixin.qq.com/s/gzr9q9kM3j-R0ec7sCb3NQ

3. Comprehensive Interpretation and Trend Analysis of Web3 Payment Track | ZONFF Research

https://mp.weixin.qq.com/s/5QuHqzvTNmG546CeGbt6og

- Blackbird's Trojan Horse: Turning Crypto Consumer Companies into Payment Companies, Leveraging Payments to Drive Growth Flywheels

https://www.web3brand.io/p/web3brand-blackbird-crypto-payment

- IOSG Weekly Brief | Streaming Payments - A New Paradigm of Blockchain-Enabled Payments #154

https://mp.weixin.qq.com/s/TOZ48uRmTfRbf17wDxnQew

- Cryptocurrency Payment Development Research | THUBA Research

https://mp.weixin.qq.com/s/_5oQMNT8I1OsW8ZgmkAebg

- The Current Status of Cryptocurrency Payments in 2022: Despite the Bear Market, Cryptocurrency Payment Demand Continues to Rise

https://mp.weixin.qq.com/s/xgs1XpHKfaWP_32pZY0wdA

- [Long Read in English] A Comprehensive View of the Cryptocurrency Payment Market: Which Trends and Innovations Are Worth Paying Attention To?

https://x.com/kayphillips/status/1713941226624307691

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。