Author: Ada, Deep Tide TechFlow

The public market is about to face an unprecedented asset package: a cash cow-level satellite internet business, a monopolistic rocket launch business, along with an AI laboratory that consumes cash equivalent to four times its total revenue in a year, all of which will be stuffed into the same profit and loss statement.

According to the prospectus, SpaceX's consolidated revenue for 2025 is projected to be $18.67 billion, with a net loss of $4.94 billion; in the first quarter of 2026, revenue is expected to be $4.69 billion, with a net loss of $4.28 billion. Compared to $1.4 billion in revenue and a net profit of $791 million in 2024, the collapse of this curve clearly points to one thing: the all-stock merger with xAI completed in February 2026.

It is this transaction that redefines SpaceX from a "profitable aerospace company" to a "cash-consuming AI infrastructure company."

Starlink Generates $3.26 Billion in a Single Quarter, Supporting the Entire Group's Cash Flow

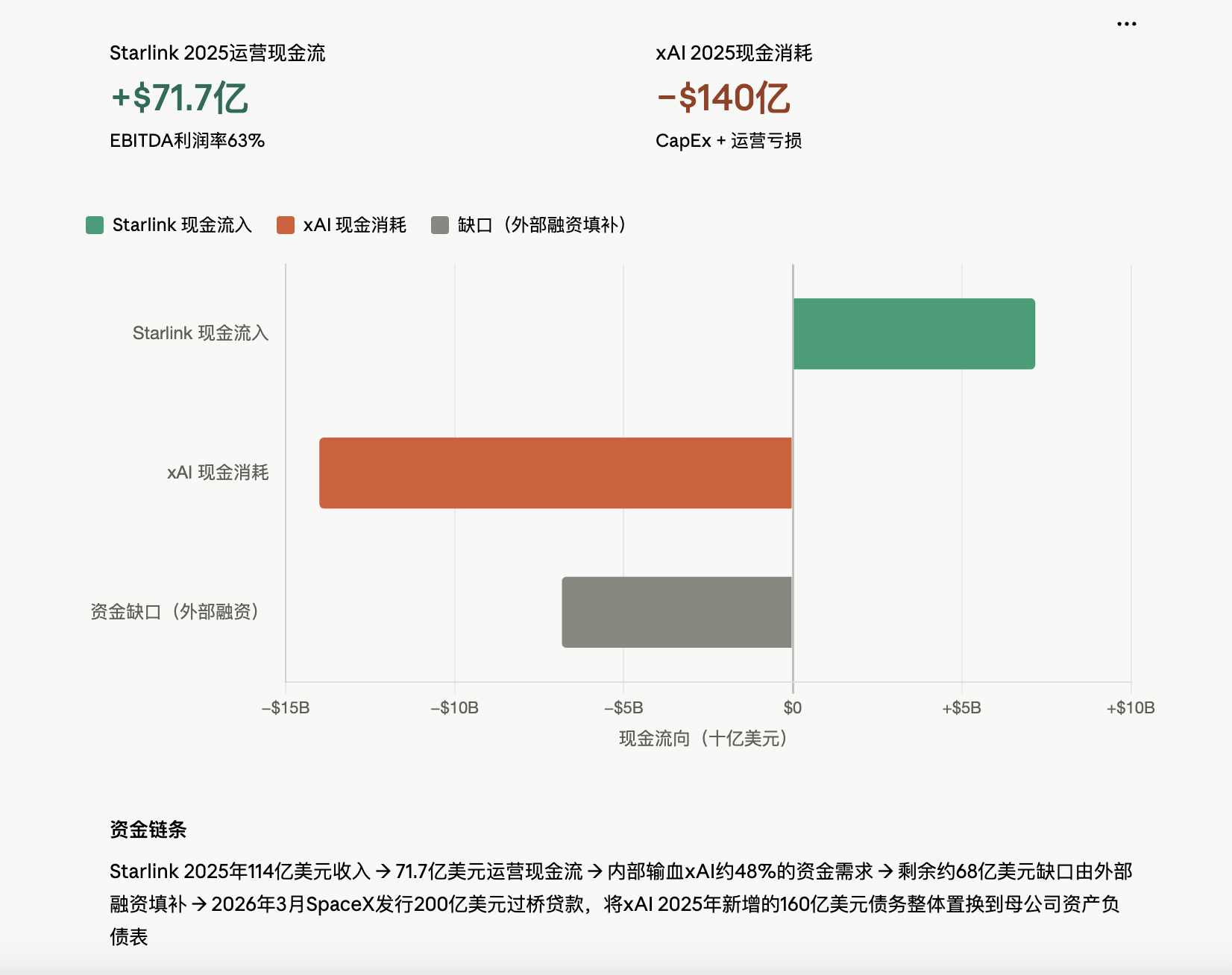

The data disclosed in the prospectus for the first time showcases the profitability of Starlink. This business recorded $11.4 billion in revenue in 2025, a year-on-year increase of about 50%, with an operating profit of $4.42 billion, and an adjusted EBITDA profit margin of 63%, generating approximately $7.17 billion in operating cash flow for the entire year.

Entering 2026, the growth rate further accelerates. In the first quarter, Starlink's revenue is $3.26 billion, with an operating profit of $1.19 billion; the number of subscription users surpasses 10.3 million, distributed across 164 countries and regions, with about 9,600 satellites in orbit. Independent analysis firm Payload predicts that Starlink's total revenue for 2026 will increase by about 80% to $18.7 billion, accounting for 79% of SpaceX's total revenue at that time.

However, the hidden danger lies in the ongoing decline in the value per user. According to prospectus data cited by BigGo Finance, the average monthly ARPU for Starlink's individual subscribers has dropped from $99 in 2023 to $81 in 2025, evaporating by 18% over two years. SpaceX chose an “exchange price for volume” expansion path, slashing the lowest-tier package price from $120/month to $50/month, with some regions even offering terminal devices for free. While this approach has been effective in capturing market share, it has lowered the unit economic model.

The rocket launch business, on the other hand, remains relatively marginal. It contributed $4.1 billion in revenue in 2025, the lowest among the three major sectors, but with NASA's Human Landing System contract and 170 Falcon 9 launch missions in 2025, this business provides an “irreplaceable” strategic moat rather than cash ammunition.

xAI Burned $7.7 Billion in a Quarter

If Starlink is a money printer, xAI is the dark hole behind that money printer draining the power grid.

The prospectus reveals that xAI's revenue in 2025 is only $3.2 billion, with an operating loss of $6.35 billion and capital expenditures soaring to $12.73 billion; the CapEx for this division exceeds the combined capital expenditures of SpaceX’s aerospace core business ($3.83 billion) and the Starlink division ($4.18 billion). Into the first quarter of 2026, xAI's revenue is $818 million, with an operating loss of $2.47 billion, and quarterly capital expenditures skyrocketed to $7.72 billion, far exceeding last year.

xAI consumed approximately $14 billion in cash in 2025, nearly equivalent to the cash generation levels of all other SpaceX departments combined. According to balance sheet data cited by SpaceWar, the group currently has $23.385 billion in servers and network equipment, $2.97 billion in data center infrastructure, and $14.05 billion in construction projects, most of which are piled up for xAI.

The debt structure has also been reshaped by xAI. According to PitchBook, xAI added $16 billion in debt in 2025 for GPU purchases, and in March 2026, SpaceX immediately issued a $20 billion bridge loan to replace xAI's debts on the parent company's balance sheet at a lower cost. This action essentially uses the cash flow credit from Starlink and the launch business to underwrite the expansion of AI computing power.

Anthropic Pays $1.25 Billion Monthly, Turning Competitors' Training Clusters into Its Own Customers

The most dramatic disclosure in the prospectus is the computing power contract between SpaceX's xAI and Anthropic, where the former is a direct competitor in the forefront model field, and the latter is its largest single paying customer.

According to the S-1 document, Anthropic has agreed to pay xAI $1.25 billion per month for 300 megawatts of computing power from the Colossus 1 data center in Memphis, Tennessee, with the contract lasting until May 2029. This data center is specifically built for xAI infrastructure development and will open approximately 220,000 GPU usage rights to Anthropic. Either party to the contract can notify termination 90 days in advance.

Calculated monthly, this contract amounts to an annualized value of $15 billion, with the total cycle value expected to exceed $40 billion. Analysis cited by SpaceWar provides a quantitative comparison: “$15 billion in annual revenue exceeds Starlink's total revenue for all of 2024.” In other words, an external AI client’s computing power contract has already matched the size of SpaceX's originally most profitable whole business.

This arrangement unveils the core of the “vertically integrated AI infrastructure” business model: xAI builds clusters, trains Grok, and sells idle computing power to all buyers, including competitors; SpaceX uses Starlink profits to subsidize construction costs; Anthropic obtains a stable supply of computing power, avoiding bundling with mega-scale cloud service providers like Microsoft and Amazon.

It is worth noting the asymmetry of the 90-day termination clause. For a $15 billion annualized contract, such a short-term termination clause makes Anthropic's commitment seem more like a “computing power option” rather than a long-term lock-in. Investors will have to assess whether this contract is the beginning of xAI’s computing power commercialization or a transitional solution before Anthropic completes its self-built data center.

18,712 Bitcoins Sitting on the Books, No Additional Purchases Since 2024

Another unexpected disclosure in the S-1 is that as of March 31, 2026, SpaceX holds 18,712 Bitcoins on its balance sheet, with a fair value of $1.29 billion, equivalent to about $1.45 billion at current prices.

The total cost basis is about $661 million, corresponding to an average purchase price of $35,324 per coin. Data from CoinDesk shows that this holding has remained unchanged since the end of 2024. SpaceX first incorporated Bitcoin into its balance sheet in 2021, with a peak holding of 25,724 coins, which has since decreased from that high. In contrast, Tesla held 11,509 Bitcoins during the same period, approximately 60% of SpaceX's holdings.

This disclosure places SpaceX among the top 7 to 11 corporate Bitcoin holders globally (rankings vary slightly by criteria). Musk has publicly defined Bitcoin in 2024 as a “fundamental currency” based on “energy,” consistent with his ongoing narratives around solar energy, Starship launches, and orbital data centers as “energy infrastructure.”

However, the detail of “no additional purchases in two years” is worth noting. During a period when Bitcoin prices have risen from about $35,000 to the current approximately $77,000, an increase of over 120%, SpaceX chooses neither to add to nor reduce its holdings, viewing this $1.45 billion asset as a locked strategic reserve rather than a liquid position. Considering the company's net loss of $4.94 billion in 2025 and xAI burning billions in cash each quarter, this "non-utilization" itself is a statement; these Bitcoins are not intended to fill the AI deficit but are seen as hard asset hedges in an uncertain currency environment for the company.

The Closed Loop of Satellite-Power-AI Model: Can It Be Priced in the Public Market?

Putting the four pieces together, Musk presents an unprecedented asset list to public market investors.

Starlink continuously generates cash at a 63% EBITDA profit margin, with expected revenue of $18.7 billion in 2026; the rocket launch business provides a strategic moat on a national security level; xAI burns $14 billion annually for entry into the AI competition, having already signed the $15 billion/year computing power order with Anthropic; on the books, there is also $1.45 billion in Bitcoin as exposure to non-dollar assets. SpaceX's valuation in the private market jumped from $350 billion in 2025 to approximately $800 billion, with the entire valuation post-xAI merger set at around $12.5 trillion, aiming for an IPO target price of $17.5 trillion.

The logic of this business closed loop is that the cash flow of satellite internet feeds the self-built AI computing infrastructure; part of the computing power is used internally (training Grok), while part is sold externally (to paying customers like Anthropic); starting in 2028, the data centers will be moved to space orbit, using Starship's carrying capacity and solar power to avoid ground power bottlenecks. Each link is internally circulating, minimizing dependence on external suppliers and capital markets.

However, risks also lie within the closed loop. xAI's cash burn rate far exceeds its current revenue, and the 90-day termination clause in the Anthropic contract leaves room for quick blood loss; the unit value of Starlink continues to decline, and the group's consolidated net loss reached $4.28 billion in the first quarter of 2026, which is more than 86% of the total loss for 2025. The five underwriters, Morgan Stanley, Goldman Sachs, Bank of America, Citigroup, and JPMorgan, need to answer the question: what exactly are investors paying for, the already validated satellite internet business or the still cash-burning AI computing power bet?

Musk currently holds 12.3% of Class A shares, 93.6% of Class B shares, collectively possessing 85.1% of the voting rights. This means that regardless of how the public market prices it, the decision-making power of this experiment in “vertically integrated AI infrastructure” remains completely in his hands.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。