Written by: qinbafrank

The tragedy of the deleveraging stampede has already occurred. At this time, let's review how deleveraging happened. From a personal perspective, this round of deleveraging started with the Korean stock market. Although the U.S. stock market began deleveraging on July 1, looking back, the first major bearish candle on June 23 marked the beginning of deleveraging. Today, let’s organize the timeline and analyze how this round of deleveraging in the Korean stock market happened.

1. Before June 23, the market had all the conditions for a stampede

To understand the subsequent collapse, we must first look at the market structure formed from May 27 to June 22.

1. Single-stock double-leveraged products concentrated funds further into Samsung Electronics and SK Hynix

On May 27, the Korean market introduced single-stock double-leveraged and inverse ETFs with Samsung Electronics and SK Hynix as underlying assets. By June 19, individual investors had net bought around 82 trillion Korean won in long-leverage ETFs, with approximately 46 trillion in SK Hynix and 37 trillion in Samsung Electronics; during the same period, the net purchase of inverse ETFs was only around 3 trillion.

More critically, the funds were not simply entering the market from cash but were obviously shifting from more diversified semiconductor ETFs and KOSPI index ETFs to single-stock leveraged products. By June 19, the asset size of the SK Hynix leveraged ETF had reached 91.5 trillion Korean won, and the related products of Samsung Electronics had reached 52.2 trillion Korean won.

This resulted in three structural changes:

1) Investors shifted from diversified industry exposure to concentrated exposure in the two stocks;

2) Regular stock volatility was further amplified by double leverage;

3) The larger the ETF scale, the greater the subsequent daily rebalancing transactions.

The Korea Capital Market Institute estimated that the asset size of SK Hynix-related leveraged ETFs increased by about 43.1 trillion Korean won from June 10 to June 19, of which about 36 trillion was not new subscriptions but net value inflation caused by the increase in the underlying assets. This means that even without new investors entering the market, the market’s rise would automatically create greater rebalancing demand.

2. The two stocks were approaching “half of KOSPI”

The market capitalization ratio of Samsung Electronics and SK Hynix in the KOSPI increased from 34% at the end of 2025 to 49% on May 26, and further reached 52% by July 15.

This is not traditional debt leverage, but it constitutes a very strong index structural leverage:

If the two stocks drop by 10%, even if the other companies do not move, it may directly drag down the KOSPI by about 5%.

As of July 15, the total market capitalization of 16 single-stock leveraged or inverse products increased from 4.4 trillion Korean won at the time of listing on May 27 to 11.9 trillion Korean won, while the daily trading volume increased from 10.4 trillion to 13 trillion Korean won.

3. The regulator's statement on June 22 became a turning point for confidence

On June 22, the head of the Financial Supervisory Service of Korea publicly acknowledged that the approval of relevant products was “prepared too hastily” and stated that measures to stabilize the market were being studied.

The regulator also explained that the initial approval of domestic single-stock leveraged products was not only to incorporate foreign product demand into the domestic regulatory system but also to attract Korean retail funds back from the U.S. and Hong Kong markets, alleviating pressure on the depreciation of the Korean won, although the actual exchange rate effect was limited.

By the end of May, the total scale of retail leveraged investments in Korea had reached about 60 trillion Korean won.

The market implication of this statement is not “the regulator will soon ban trading” but rather:

- The expectation of policy support for product expansion is disrupted;

- The expansion space for brokers and asset management companies’ products is questioned;

- Foreign capital begins to worry that regulation will change the market liquidity structure;

- The market seriously assesses the risk of double ETFs’ inverse feedback for the first time.

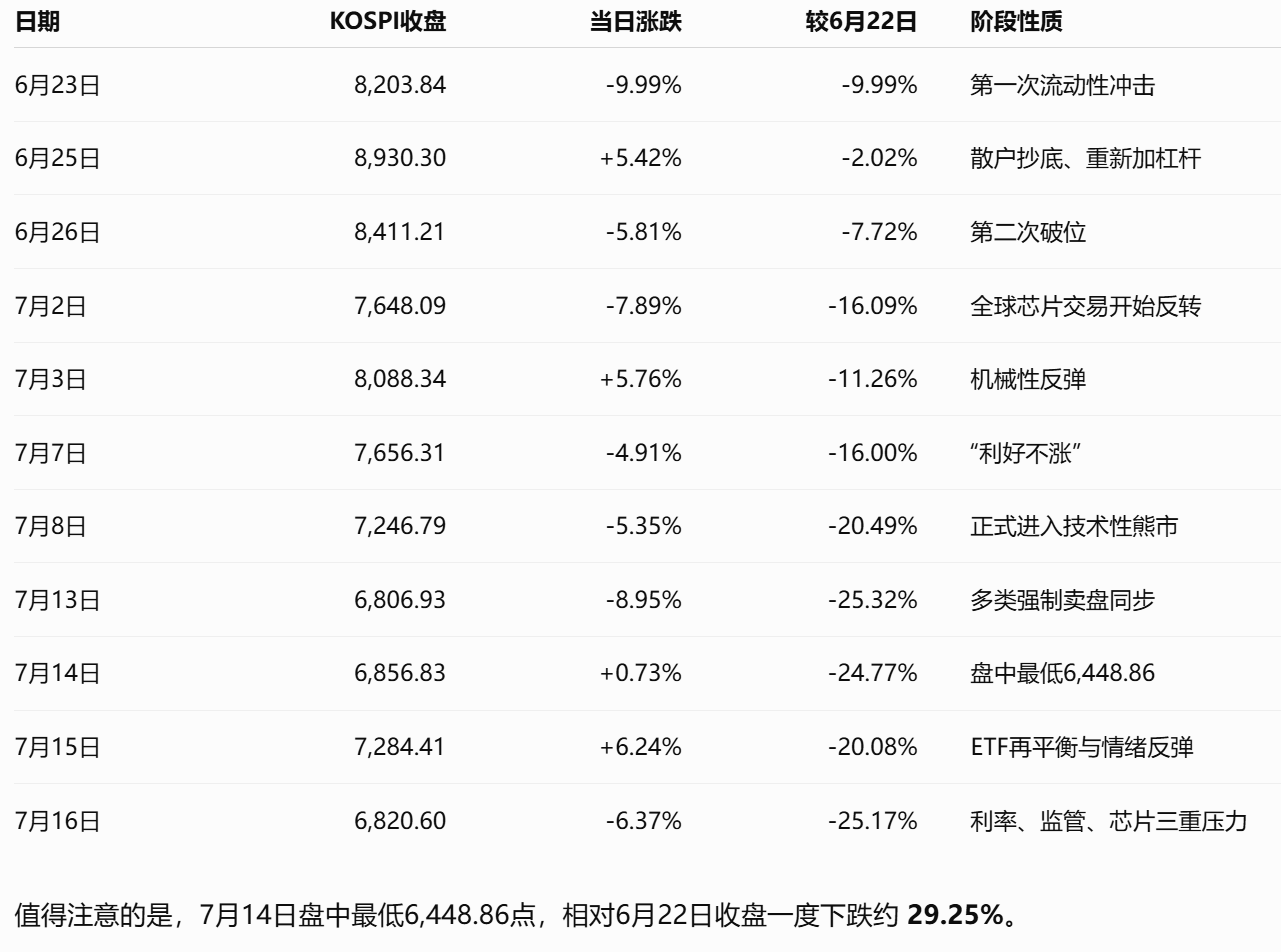

2. Main index path

Below are the most important price nodes in this round. The relative decline is based on June 22's 9,114.55 points.

3. Dissecting the deleveraging process by timeline

First phase: June 23—prices first collapsed, and debts did not decrease

On June 23, the KOSPI fell 9.99% in a single day, with both Samsung Electronics and SK Hynix dropping over 12%, triggering a 20-minute market-wide trading halt.

The immediate triggering factors included:

- The previous day's strong warning from the regulators regarding leveraged ETFs;

- Foreign capital started to sell off the two major chip leaders;

- Global tech stocks adjusted simultaneously;

- The market had been on a continuous rise, leading institutions to seek to take profits and control weight.

Because Samsung Electronics and SK Hynix accounted for more than half of the KOSPI, the selling pressure on these two stocks quickly shifted from a stock-specific issue to an index issue.

However, an important and very dangerous phenomenon occurred that day:

- The amount of forced liquidations rose from about 19.9 billion Korean won the previous day to 42.427 billion Korean won;

- The uncollected accounts receivable increased by 181.6 billion Korean won, reaching 1.4792 trillion Korean won;

- The credit financing balance remained around 38 trillion Korean won.

In other words, the first day's sharp drop did not lead investors to generally repay debts. On the contrary, some investors continued to use short-term credit funds to add positions during the decline.

The essence of this phase

This was a price deleveraging but not a balance sheet deleveraging.

Prices fell rapidly, leading to declines in ETF net values and collateral values; yet retail investors did not retreat but continued to buy the dip. The existing leverage was not cleared, and new leverage was entering.

Emotionally, the market still interpreted the decline as a short-term technical misfire caused by regulatory comments, rather than a trend reversal.

Second phase: June 24 to 25—forced liquidations and renewed leverage occurred simultaneously

On June 24 and 25, the KOSPI rose by 3.26% and 5.42%, respectively, and by the close on June 25, it was only about 2% away from the June 22 high.

But beneath the surface rebound, two completely opposite things were happening internally.

One side was forced liquidations

On June 24, the publicly reported forced liquidations reached about 1,107.93 billion Korean won. This mainly came from short-term credit trades that had not been timely funded.

The other side was new financing

On the same day, the credit financing balance actually increased by about 5,392 billion Korean won, reaching a record 38.6328 trillion Korean won.

This means:

Old accounts were being forced to liquidate, while new or surviving accounts were borrowing more money to buy the dip.

Thus, June 24 became the peak season for the entire market's credit financing balance, rather than just before the plunge on June 23.

Why did the leveraged ETFs amplify the rebound?

Double long ETFs must restore their double target exposure daily.

Assuming the ETF’s initial net asset value is A and it holds an exposure worth 2A in stocks or derivatives:

- If the underlying drops by 10%, the ETF net asset value will decrease to about 0.8A;

- The original exposure’s market value becomes approximately 1.8A;

- The new target exposure should be 1.6A;

- Thus, it needs to sell approximately 0.2A.

Conversely, when the underlying rises, the ETF must increase its purchases.

Estimates by the Korea Capital Market Institute indicate that the rebalancing trading volume for single-stock double ETFs is roughly proportional to “the previous day's AUM × the percentage change in stocks that day,” and both the spot and futures markets will adjust in the same direction.

Therefore, the rebound from June 24 to 25 was driven by:

- Retail investors buying the dip;

- Short covering;

- Leveraged ETFs rebalancing upwards;

- Brokers and market makers conducting hedge adjustments;

This was not a healthy rebound after completing deleveraging, but rather resembled a re-leveraging during the deleveraging process.

Third phase: June 26 to 30—foreign capital withdrew, retail investors picked up the shares, and risks began to shift to the household sector

On June 26, the KOSPI fell again by 5.81%. On June 29, although the closing was down only 0.20%, the intraday volatility was significant, with the Korea Volatility Index VKOSPI rising to a historical high of 97.99, compared to only 28.85 at the end of 2025.

The most significant change in this phase was not a single trading day but a shift in the shareholding structure.

Foreign capital was not merely being “bearish on Korea” but was reducing concentration.

In the first half of 2026, foreign capital net withdrew about 70.8 billion USD from the Korean stock market; about 12.63 billion USD was net withdrawn in June alone.

These sell-offs came from various institutions:

- Mutual funds sold about 7.5 billion USD;

- Pension funds sold about 4.35 billion USD;

- Hedge funds sold about 1.87 billion USD.

Analysis shows that these funds were not entirely due to a judgment that the Korean economy or semiconductor profits would collapse but because:

- The rise in Korean and Taiwanese chip stocks was excessive;

- The weight of Samsung Electronics, SK Hynix, and TSMC in global funds rapidly inflated;

- Both passive and active funds needed to control concentration in a single country, sector, and stock;

- Some funds were hedging exchange rates and rebalancing their benchmarks;

- Long-term institutions were taking profits.

Retail investors become the last marginal buyers

Korean individual investors net bought approximately 42.4 trillion Korean won worth of KOSPI stocks in June.

Thus, the core funding structure in June was:

Foreign capital, pension funds, and mutual funds reducing risks, while Korean retail investors picked up those positions through cash, financing, and leveraged ETFs.

This temporarily supported the index but also produced two consequences:

- Risks shifted from global institutional balance sheets to Korean households' balance sheets;

- The average risk tolerance of remaining market holders weakened, making them more sensitive to margin calls and price fluctuations.

Fourth phase: July 1 to 3—global semiconductor trading reversed, ETFs began to systematically sell low and buy high

On July 1, the KOSPI dropped 2.04%, and further plummeted 7.89% on July 2.

On July 2:

- SK Hynix dropped 14.6%;

- Samsung Electronics dropped 9.1%;

- Western Digital fell over 13.5%;

- U.S. semiconductor stocks also saw substantial adjustments the previous night.

The market began to shift from “current semiconductor profits are excellent” to questioning:

- Rumors of Meta selling computing power raised concerns about surplus capacity;

- Can U.S. cloud computing companies sustain high-intensity AI capital expenditures;

- Is large-scale data center construction entering a phase of marginal slowdown;

- Will the new capacity of Samsung Electronics and SK Hynix lead to supply surplus in the future;

- How long can the current rise in memory prices last;

- Whether the speed and duration of profit growth have already been fully reflected in stock prices.

It is essential to distinguish between industry sparks and market amplifiers in this round

Industry-level sparks include:

- Global semiconductor profit taking;

- The sustainability of AI capital expenditures being questioned;

- Memory price growth rate may have peaked;

- New capacity planning may change future supply and demand.

However, what truly expanded the drawdown to nearly 8% was the market structure:

- Foreign capital selling chip-weighted stocks;

- Double ETFs being forced to reduce exposure due to the underlying drop;

- Market makers in futures and spot simultaneously selling for hedging;

- The index's drop widened, causing financing account collateral ratios to decline;

- Risk models, stop-losses, and algorithmic funds further reduced positions.

On July 3, the KOSPI rebounded 5.76%, which can be similarly explained as a counter-operation to the above mechanism: retail investors buying the dip, short covering, and ETFs re-entering positions.

Thus, this phase formed a typical:

When falling, ETFs must sell; when rebounding, ETFs must buy; the market is not gradually converging but experiencing amplified fluctuations in both directions.

The Korea Capital Market Institute also emphasized that all fluctuations cannot be solely attributed to ETFs, as the volatility of U.S. and Japanese memory stocks also surged significantly during the same period, and geopolitical conditions, inflation, and global interest rate uncertainties are equally crucial. ETFs are amplifiers, not the sole cause.

Fifth phase: July 6 to 8—“good news no longer bullish,” sentiment shifted from technical adjustment to worries about profit sustainability

July 7 marked the second key inflection point on the emotional level

Samsung Electronics announced preliminary guidance indicating that second-quarter operating profit might increase by about 19 times year-on-year, but that day, Samsung Electronics still dropped 6.9%, with intraday losses exceeding 10%; SK Hynix fell 6.1%.

This indicates that the market had entered a phase where “good news cannot push stock prices higher”:

- It's not that earnings are poor;

- But previous expectations were too high;

- Investors began to worry that current earnings are at a cyclical peak;

- Good news was used to realize profits, rather than chase prices up.

That day, foreign capital net sold approximately 29 trillion Korean won, while individual investors net bought about 32 trillion Korean won. More alarmingly, the KOSPI market's credit financing balance remained around 29.7 trillion Korean won, slightly below the late June peak of 29.8 trillion Korean won.

In other words, the index had already dropped approximately 16% from its peak, but the KOSPI credit financing debt had hardly decreased.

Risks began to spread to other industries

July 7 was not only about semiconductor declines:

- LG Energy Solution expected a 77% drop in second-quarter operating profit due to weak electric vehicle demand, with a share price drop of 6.4%;

- Hanwha Marine dropped 22.7% due to Canada choosing a German plan for a submarine project.

This indicates that the market had begun to expand concerns from semiconductor product structure issues to:

- Battery industry profit slowdown;

- Uncertainties in defense and shipbuilding orders;

- Risk budgets for high-valuation growth stocks decreasing;

- Negative news for individual stocks being priced in more aggressively.

July 8 officially entered a bear market

On July 8, the KOSPI dropped 5.35%, a relative decline of over 20% from the June 22 high.

On that day, the U.S. Philadelphia Semiconductor Index previously dropped by 4.7%, and the market continued to worry about the sustainability of AI investments, memory price growth slowing, and profit peaks. The Korean Minister of Finance began to publicly state that they would closely monitor the risks associated with single-stock leveraged ETFs.

A notable detail is that on that day, foreign capital slightly net bought about 335.9 billion Korean won after selling for 13 consecutive trading days; at the same time, the Korean won appreciated due to SK Hynix’s dollar exchange demand associated with fundraising in the U.S.

This indicates that this round cannot be simply understood as “foreign capital withdrawal—Korean won depreciation—stock market decline” as a single-line logic. Corporate cross-border financing, foreign exchange hedging, and stock rebalancing may occur simultaneously, leading to short-term divergence between stock and exchange rate signals.

Sixth phase: July 9 to 10—forced liquidation data significantly increased, and leverage risks spread to the U.S. and Hong Kong

On July 9, the KOSPI slightly rose by 0.62%, but the publicly reported actual forced liquidations reached about 1,421.97 billion Korean won, marking the fourth highest since such statistics were recorded.

Throughout 2026, there were 6 trading days with forced liquidations exceeding 1 trillion won, 5 of which occurred post the listing of single-stock leveraged ETFs on May 27. On July 9, the market's credit financing balance still had about 36.63 trillion Korean won, with approximately 28.84 trillion in the KOSPI and about 7.80 trillion in KOSDAQ.

This reflects a clear lag in forced liquidations:

- Stocks fall first;

- Investors receive margin call requirements;

- Accounts are not promptly supplemented;

- Brokers then execute forced sales in the following trading days.

Therefore, it is critical not to solely focus on the forced liquidation amounts from the day of the crash; the 5-day average and subsequent days are more important.

SK Hynix’s U.S. listing opened a new cross-market leverage channel

On July 10, SK Hynix's American depositary shares began trading on NASDAQ, with this financing scale of about 26.5 billion USD. At least 10 fund management institutions submitted applications to issue single-stock leveraged or inverse ETFs around SK Hynix ADR.

This enabled the risk of the same stock to start transmitting across multiple time zones:

- Seoul's common stock;

- Hong Kong double-leveraged products;

- U.S. ADRs;

- U.S. single-stock leveraged ETFs;

- Korean spot and futures;

- Market makers’ cross-market hedging.

It should be noted that there is currently no publicly available exchange data that can accurately prove how each cross-market arbitrage impacts Seoul’s stock prices. However, structurally, the new listings and products are likely to increase:

- Overnight price discovery;

- ADR and local stock price differential trading;

- Market makers' hedging;

- Daily rebalancing of overseas products;

- Next morning's Seoul opening gap risk.

Seventh phase: July 13 to 15—multiple selling pressures occurred simultaneously, followed by a mechanical rebound

July 13 was the most typical “waterfall deleveraging” in this round

The KOSPI fell by 8.95%, closing at 6,806.93 points:

- SK Hynix dropped 15.37%;

- Samsung Electronics fell about 10%;

- Foreign capital net sold about 17.261 trillion Korean won;

- Institutions net sold about 21.964 trillion Korean won;

- Individual investors bought back about 38.809 trillion Korean won.

The day's sell-off was driven by the following factors:

- “Good news realization” after SK Hynix ADR listing;

- Foreign capital reallocating between ADR and Korean common stock;

- The market continued to worry about the sustainability of AI capital expenditures by U.S. tech companies;

- The debate over memory cycle peaks intensified;

- Renewed escalation in tensions between the U.S. and Iran;

- Rising oil prices and inflation expectations, with global interest rate expectations trending hawkish.

Meanwhile, the Hong Kong-listed SK Hynix double-leveraged ETF dropped over 30% that day. ETFs selling in the same direction further enlarged the declines of SK Hynix's common stock and the KOSPI.

The selling structure of that day can be summarized as:

Foreign capital and institutions actively reducing risks + leveraged ETFs passively reducing exposure + financing accounts facing margin calls + brokers’ forced selling + algorithmic stop-losses = waterfall selling.

However, individual investors still net bought nearly 39 trillion Korean won, so this was closer to a price and liquidity surrender, but not a full surrender in the sense of retail behavior.

On July 14, market conditions approached the lowest point, but balance sheet reduction remained limited

On July 14, the KOSPI hit an intraday low of 6,448.86 points, down approximately 29.25% relative to the June 22 closing; however, it closed slightly up 0.73%.

At that time:

- Individual investors had net bought approximately 132 trillion Korean won in KOSPI stocks in July;

- Net purchases in June amounted to 424 trillion Korean won;

- The KOSPI credit financing balance remained about 28 trillion Korean won;

- Compared to the peak of 29.8 trillion Korean won on June 24, it only decreased by about 6%.

Thus, even with an intraday drop of nearly 30%, KOSPI financing debt only reduced by about 6%.

The surge on July 15 did not prove the end of deleveraging

On July 15, the KOSPI rose by 6.24%:

- SK Hynix rose nearly 13%;

- Samsung Electronics rose nearly 8%;

- Semiconductor equipment firm Hanmi Semiconductor surged approximately 25% at one point.

Driving factors included:

- U.S. inflation data came in below expectations;

- The U.S. tech sector rebounded;

- Analysts reiterated a structural shortage of AI memory;

- The market believed that recent sell-offs partly stemmed from ETF position unwind, rather than a collapse in semiconductor fundamentals.

Some industry perspectives contend that current DRAM supply can only meet about 75%—80% of demand, with the gap possibly widening by 2027; meanwhile, another group of investors remains concerned about capital spending slowing for U.S. cloud providers, new capacity, and future decreases in memory price growth.

Therefore, the rebound on July 15 represented two simultaneous phenomena:

- The re-emergence of the fundamental bullish narrative;

- The re-leveraging of double ETFs, short covering, and program trading.

This resembles a mechanical re-leveraging rebound during the deleveraging process, and cannot be directly interpreted as the final bottom.

Eighth phase: July 16—regulation, interest rates, and semiconductors simultaneously pressuring, deleveraging began to institutionalize

On July 16, the KOSPI fell by 6.37%, closing at 6,820.60 points:

- Samsung Electronics fell 8.77%;

- SK Hynix fell 11.53%;

- Foreign capital net sold approximately 19.288 trillion Korean won;

- Institutions net sold around 30.537 trillion Korean won;

- Individual investors net bought about 47.816 trillion Korean won.

There was clear differentiation across sectors:

- Electrical electronics fell 9.43%;

- Manufacturing down 7.51%;

- Machinery equipment down 4.70%;

- Construction down 3.30%;

- Telecommunications up 3.39%;

- Food and tobacco up 2.12%;

- Paper and wood up 2.00%;

- Textiles and clothing up 1.01%.

This indicates that the day was not about indiscriminate liquidity collapse, but rather funds shifted from semiconductors, equipment, and high-beta growth sectors to defensive sectors.

The Bank of Korea raised interest rates

The Bank of Korea increased the benchmark interest rate from 2.50% to 2.75%, a 0.25 percentage point hike.

Reasons given by the central bank include:

- Strong growth in exports and investments;

- The semiconductor industry’s prosperity driving economic growth;

- June CPI reaching 3.2%;

- Core inflation at 2.5%;

- Risks related to exchange rates and financial stability remain.

This rate hike was not specifically aimed at repressing the stock market, but it will influence leverage through three channels:

- Increased opportunity cost of securities financing and other borrowing funds;

- Raising the discount rate used for stock valuation;

- Reducing the ability and willingness of retail investors to continue borrowing for buying dips.

The financial regulatory policy officially shifted

On the same day, the Financial Services Commission of Korea announced restrictions on single-stock leveraged products.

Immediate implementation:

- Suspension of new listings of single-stock leveraged, inverse, and related products;

- Prohibition of brokers and asset management institutions from advertising and engaging in marketing activities.

Gradual implementation in August:

- The price deviation management standard for LPs was tightened from 3% to 2%;

- New product business restrictions on LPs and asset management companies for serious misconduct;

- Investment education increased from 2 hours to 3 hours;

- Strengthening warnings about loss, long-term holding risks, and price deviations;

- By around August 5, minimum base deposits would increase from 10 million won to 30 million won;

- By around August 19, collateral based on stocks and other assets would no longer be permitted, requiring 30 million won in cash.

Plans for November to implement:

- The minimum trading unit for domestic single-stock leveraged products would be raised from 1 to a tentative 20 units.

These policies have a dual impact on the market.

In the long run, they will:

- Lower new leverage demand;

- Increase entry thresholds;

- Reduce marketing incentives;

- Improve ETF market price deviations;

- Limit unlimited expansion of product supply.

In the short term, they may also prompt investors unable to meet new cash thresholds to reduce positions ahead of time, reinforcing the psychological expectation that “regulation no longer supports leveraged market conditions.”

Thus, July 16 marks the transition of deleveraging from spontaneous market behavior into an institutional stage led by regulation and coordinated with interest rates.

So in terms of results:

The KOSPI dropped from 9,114.55 points on June 22 to 6,820.60 points on July 16, a cumulative decline of 25.17%;

The total market's credit financing balance decreased from approximately 38.63 trillion won on June 24 to about 34.37 trillion won, a drop of about 11%;

In other words, the price drop was about 2.3 times that of the debt reduction.

This indicates that the rapid deleveraging occurred first at the price and product level, while the debt reduction on investors' balance sheets was slightly lower.

4. Overall Judgment

This is not merely a “semiconductor valuation correction,” but a negative feedback loop formed by the simultaneous interaction of “foreign capital rebalancing, retail financing buying the dip, daily rebalancing of single-stock leveraged ETFs, forced liquidations, industry expectations reversal, policy shifts, and tightening monetary policy.”

Leveraged ETFs are not the initial spark, but they are a very important amplifier;

Credit financing is not the direct cause of every daily drop, but it determines whether the decline can evolve into a chain of forced liquidations.

In early July, we discussed compression-style deleveraging: multilayered leverage is expressed simultaneously, leading to all expressions increasing delta when rising; when reversing, all expressions decrease delta simultaneously, creating extreme symmetry of “consensus reinforcement” and “crowded stampede.” Everyone adds positions in the same direction and will also reduce in the same direction. Liquidity seems abundant, but is, in reality, extremely fragile. Once prices can no longer continue to rise, the delayed counter-evidence will concentrate and explode.

In essence, it is not a matter of liquidity tightening or fundamental issues arising.

It is really about a reversal of expectations; once marginal buying disappears, those stock prices propped up by emotional premiums will be squeezed out, resulting in a pullback; then leveraged funds are forced to reduce positions, leading to a stampede.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。