Author: Jae, PANews

On July 17, the South Korean stock market was closed for a day due to Constitution Day, but the smoke of battle has not dissipated. Stocks related to Samsung Electronics and SK Hynix still faced sell-offs in other markets. At the close of the Hong Kong stock market, the leveraged ETFs that doubled down on Samsung and Hynix dropped by about 20% each. The Korean capital market is undoubtedly experiencing an epic "de-leveraging" tsunami in the summer.

Over the past two weeks, the fervent myth of "全民炒股" (全民炒股 translates to "everyone trading stocks") has been ruthlessly crushed by cold liquidation data. Just two months ago, the 2x leveraged ETFs for SK Hynix and Samsung Electronics were packaged as a wealth shortcut "共享国运" (sharing national fortune), with regulators personally loosening restrictions and retail investors flocking in an attempt to get a share of the semiconductor bull market. However, as industry expectations shifted and market corrections occurred, these leveraged tools instantly transformed into a "meat grinder."

Faced with the dual blows of market uncontrollability and a "suspension of credit" from banks, President Yoon Suk-yeol intervened urgently, and the regulatory authorities launched "seven heavy blows" overnight, but before that, hundreds of thousands of retail investors were already deeply trapped in the darkest moment of principal loss.

$1.45 billion evaporated, 460,000 accounts lost all principal, with over 60% being young investors

In mid-July, for retail investors betting on the South Korean semiconductor sector, every trading day broke painful records.

In just nine trading days, the cumulative floating loss in the leveraged ETFs favored by retail investors exceeded 8.8 trillion won (about $5.95 billion). Among them, individual investors accounted for as much as 60% of the holdings in leveraged products. This means that the "explosive" drop was almost entirely ignited in the accounts of ordinary retail investors who had the weakest risk tolerance.

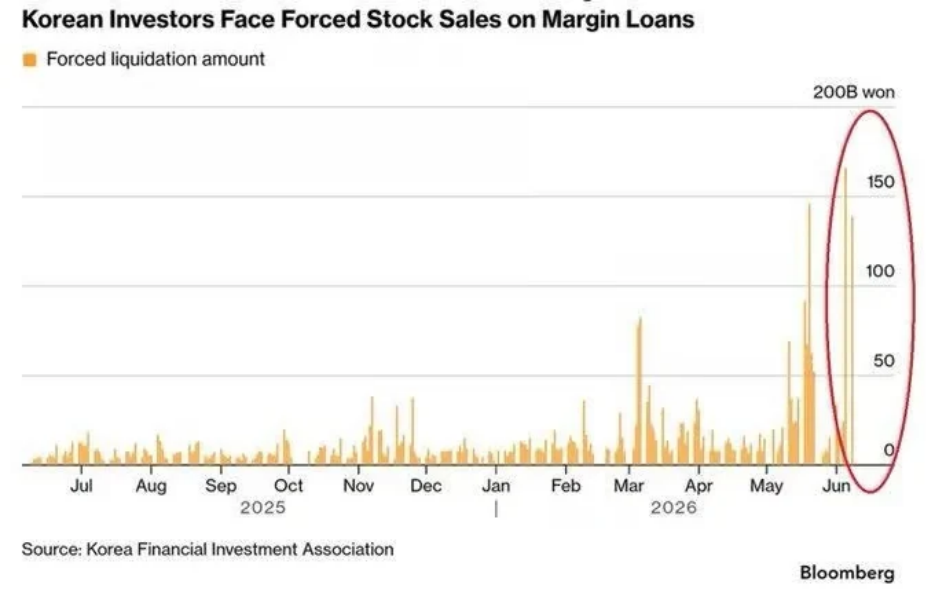

According to Bloomberg statistics, in the past month, South Korean retail investors suffered economic losses of up to $1.45 billion (about 2 trillion won) due to high-leverage trading. However, an even more brutal wave of forced liquidation was still to come, as more than 1.2 million retail leveraged accounts across the market triggered the "death line" for margin calls. Unable to meet the additional margin requirements within the stipulated time, 460,000 accounts were forcefully liquidated by brokerages, with young investors aged 20-30 making up 62% of the total liquidated accounts. Not only did their principal drop to zero, but an absurd tragedy of "owing money to the brokerages" also emerged, as young investors learned a heavy lesson from the market.

This wave of forced liquidation peaked in mid-July. From July 1 to 13, the total amount of forced liquidations reached 451.9 billion won (about $305 million). On July 9, the single-day amount of forced liquidations peaked at 142.2 billion won (about $95.2 million), with a forced liquidation ratio skyrocketing to 10.2%. On July 13, the total forced liquidation amount across the market surged to 344.2 billion won (about $232 million), setting a record for the year.

Market panic intensified simultaneously. SK Hynix, which retail investors nearly all bet on, dropped over 15% on July 13, marking the largest single-day drop in 18 years, while its 2x leveraged ETFs plummeted by 30%. The Korean Composite Stock Price Index, KOSPI, slumped nearly 9% in a single day, triggering a circuit breaker for the seventh time this year, with a cumulative decline of as much as 25% from the historical high in June.

The market's panic sentiment snowballed, growing larger under the amplification of the leverage mechanism. The widespread forced liquidations among retail investors were not solely driven by falling stock prices. The built-in daily rebalancing mechanism of individual stock leveraged ETFs was the "disaster engine" that transformed the correction into a stampede.

Related reading: Leveraged products trigger huge changes in the stock market, how did the South Korean stock market become a "casino"?

Even worse, many retail investors lacking risk control awareness chose to "grit their teeth" during the decline, constantly adding to their positions in an attempt to average down costs. Typical "gambler-style" operations increased their exposure, ultimately accelerating their descent into the abyss of liquidation.

Bank credit cut off, central bank interest rate hike adds insult to injury

On-market leveraged trading is the blade of the meat grinder, while off-market credit exhaustion is the blood pump that drains the last drop of blood from retail investors.

The phenomenon of South Korean households "borrowing money to trade stocks" has been going on for a long time. During the bull market in the first half of the year, retail investors were extremely keen to enter the market through housing mortgages and consumer loans to leverage, but to curb the malignant expansion of household debt, South Korean regulators set a hard cap of 1.5% on the annual growth rate of household loans for commercial banks.

This red line morphed into a tightly pulled noose mid-year. By the end of June, the household loans of South Korea's five major commercial banks increased by 3.7 trillion won (about $2.502 billion), consuming 85.3% of the annual lending quota. The remaining quota was only about 639.5 billion won ($431 million), and even two banks had exceeded their caps early. In the second half of the year, not only could they not issue new loans, but they were also required to recover existing loans, forcing the quotas to decrease.

This also meant that when the stock market crashed in July and 1.2 million accounts triggered margin call notifications, retail investors suddenly realized: they could no longer borrow money. Without incremental funds to add, they faced the only path of forced liquidation by brokerages.

As if that weren't enough, an unexpected interest rate hike from the South Korean central bank came. On July 16, the South Korean central bank dropped a bombshell amid extremely weak market liquidity: it announced a 25 basis points increase in the benchmark interest rate to 2.75%, marking the first shift to tightening in three and a half years. Although the policy's initial intent was to narrow the interest rate differential with the US, alleviate foreign capital outflows, and stabilize the won exchange rate, the action of raising rates amid the liquidation wave was akin to pouring salt on the wounds of de-leveraging.

That day, KOSPI fell sharply by 6.37%, while SK Hynix plummeted by 11.53%, triggering a negative feedback loop of de-leveraging.

Seven measures to halt, not defuse but cut off the supplies

The large-scale loss of principal quickly escalated into a political event, with a member of the People's Power Party, Ahn Cheol-soo, previously denouncing on social media that KOSPI had "degenerated into a casino."

Faced with the shame of being called a "national fortune casino" and the tragic situation of hundreds of thousands of families losing their wealth, South Korean President Yoon Suk-yeol personally named the leveraged ETFs of Samsung and SK Hynix, ordering the financial sector to quickly formulate countermeasures.

On July 16, a package of iron-fisted new regulations resembling "shock therapy" was urgently rolled out by the F4 agreement mechanism, which consists of the Financial Services Commission, Financial Supervisory Service, Ministry of Finance, and central bank, aimed at cooling this leveraged fever.

It is noteworthy that the regulators did not choose to directly force the existing ETFs to delist. Forcing a "disconnection" in panic could trigger an even more severe liquidity stampede. The true logic of regulation is: to not actively burst the existing bubble, but instead to raise the entry barriers and cut off new funds, allowing the market to enter a prolonged passive clearing period.

As new regulations are about to be implemented, the system of the individual stock leveraged market in South Korea is being forcibly reshaped, and the frenzy of speculation is expected to temporarily subside. However, the risks have not truly dissipated: currently, there is still over 35 trillion won (about $23.55 billion) of outstanding margin financing in the South Korean stock market. Against the backdrop of credit tightening and rising interest rates, existing leveraged accounts have effectively lost their buffer.

The financial chill in Seoul has awakened the retail investors submerged in market frenzy. Leveraged innovations devoid of real income support from investors and strict regulatory constraints are essentially just building wealth bubbles. When a large downward line strikes, all fictional prosperity will be liquidated by the market, and those who ultimately bear the cost are often the most vulnerable retail investors.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。