In response to external skepticism regarding the AI bubble and business models, OpenAI CEO Sam Altman admitted that the company performed poorly over the past year and took responsibility, but promised that next year would bring the best performance in its history. Skeptic Ed Zitron previously warned that the real bubble is the "OpenAI bubble," and if it fails, it will impact AI investment logic like "Lehman Brothers," triggering a massive reevaluation of data centers and tech stocks.

Written by: Li Jia, Wall Street Journal

OpenAI CEO Sam Altman publicly acknowledged that the company's performance over the past year did not meet expectations and primarily attributed the responsibility to himself, while stating that the next 12 months will be the best year since the company's inception. This rare statement comes amid increasing external doubts about OpenAI's business model and AI investment returns.

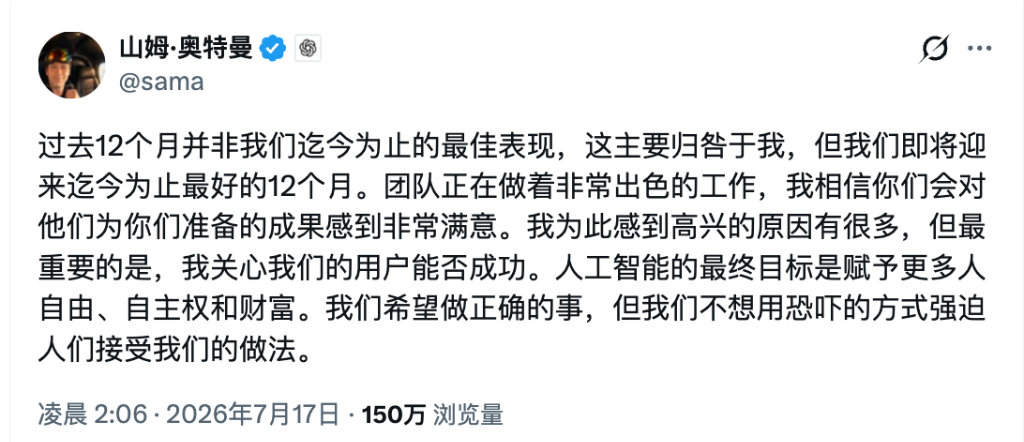

On July 17, Altman posted on social media platform X, stating: "The past 12 months have not been our best year ever, which is mainly my fault, but we are about to have our best year yet." He emphasized that the mission of AI is to empower more people with freedom, autonomy, and wealth, rather than driving user choices through fear.

Meanwhile, the debate surrounding AI business models continues to simmer. According to a previous article from Wall Street Journal, long-time AI skeptic Ed Zitron recently referred to OpenAI as a "systemically important institution" in this round of AI investment cycle, believing that if its business model encounters problems, the impact may spread to data centers, AI infrastructure, and even global tech stocks. Altman's public statement has brought this discussion back into the market spotlight.

Altman's Self-Reflection and Apology, Users Expect Product Effectiveness

Altman did not disclose specific details of missteps but was quite direct in attributing the less-than-expected performance to his leadership. He stated that the team is working on "amazing work" and hinted that upcoming new products would satisfy users.

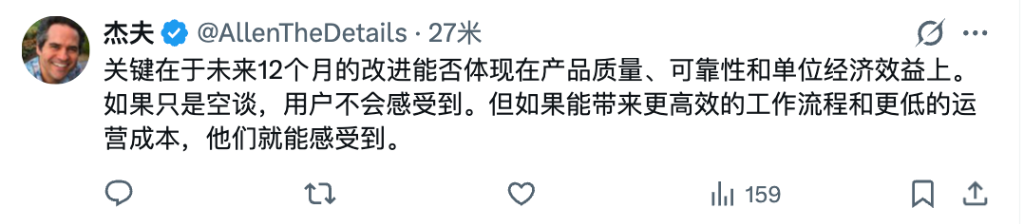

This statement triggered mixed reactions on social media. Some users appreciated his candidness, but others argued that more critical than a public statement is whether the next 12 months can deliver on promises regarding product quality, system stability, and commercialization efficiency.

User Jeff (@AllenTheDetails) commented: "If it's just empty talk, users won't feel it; if it's better workflows and lower service costs, they will feel it." Another user @onecloudtech stated: "Users still have confidence in the product, but trust needs to be built through repeated product releases."

"AI Bubble Equals OpenAI Bubble"? Zitron Launches Radical Doubt

The background of Altman's post is the growing public pressure regarding OpenAI's business model. Long-time AI skeptic Ed Zitron recently published a long article which presented the most radical assessment yet: the real AI bubble is essentially the "OpenAI bubble."

He believes that since the launch of ChatGPT at the end of 2022, OpenAI has effectively become the "credit anchor" of the entire generative AI era - investors’ confidence in steadily growing demand for massive data centers, GPUs, and the eventual profitability of large model companies relies on OpenAI's continued rapid growth.

Zitron's concerns center on three points: first, the inference costs are still too high, and expanding the user base may mean simultaneous increases in losses; second, the rate of capital expenditure expansion is far outpacing the improvement of cash flow, as many data center projects will take years to recoup costs; third, OpenAI will continue to rely on external financing for many years to come, and if the financing environment tightens, the business model will face greater pressure.

It is worth noting that these views reflect Zitron's personal judgment, and OpenAI has not endorsed them. However, these concerns do reflect the real discussions in the market regarding AI's return on investment (ROI).

AI Infrastructure Boom Hides Risks: If Demand Expectations Lost Their Anchor, the Supply Chain May Face Valuation Adjustment

Zitron's worries extend beyond OpenAI itself to the entire AI infrastructure supply chain.

Over the past two years, the U.S. tech industry has seen an unprecedented surge in data center construction. Major cloud providers like Microsoft, Google, Meta, and Amazon are continuously increasing their capital expenditures, while companies like Oracle and CoreWeave are taking on more AI computing power construction tasks, with many projects relying heavily on long-term leases, project financing, private credit, and corporate debt.

Zitron believes that if the demand from core customers like OpenAI falls short of expectations, or if the capital markets reassess AI returns, companies reliant on the growth of AI infrastructure demand, such as Oracle and CoreWeave, could be the first to feel the impact, as the market previously assigned high valuations to these companies largely based on the expectation of sustained AI demand explosion.

In addition, Anthropic and SoftBank also fall under discussion. Zitron points out that while Anthropic and OpenAI have different paths, they both require continuous massive funding and rely on large tech companies for computing power; SoftBank, having made large bets on AI infrastructure, chips, and model companies, will face market scrutiny of its vast AI asset portfolio if the industry enters a valuation adjustment period.

Whether There Is a Bubble Remains Undecided, Market Attention Shifts from "How Much Money Was Spent" to "How Much Money Was Earned"

The debate about whether AI has entered a bubble phase has been ongoing on Wall Street for a long time, with no definitive conclusion yet.

Howard Marks, co-founder of Oak Tree Capital, recently stated that he has shifted from initially doubting whether AI might just be a bubble to appreciating its long-term value more. He believes that the reasoning, contextual understanding, and interaction capabilities that modern AI demonstrates possess unprecedented characteristics and cannot be simply likened to historical speculative bubbles, positioning AI as a general technological platform akin to the internet and electrification.

Some academic research offers a more neutral conclusion: the current AI market features both genuine technological advancements and localized overvaluation and premature capital expenditures, being closer to a "technological revolution overlapping with localized bubbles" rather than mere speculative fervor.

For investors, the key indicators to track are shifting from the scale of capital expenditures to another set of data: corporate AI revenue growth, AI product payment rates, the speed of declining inference costs, data center utilization rates, and AI investment return cycles. Whether Altman's promises can be validated along these dimensions may become a crucial reference for the market to reassess AI transaction valuation logic.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。