Written by: Rita

Trend Guide

J.P. Morgan has significantly raised its forecast for global server shipment growth from 2026 to 2028, increasing the growth rate from 15% to 22% for 2026 and from 8% to 25% for 2027. The core driver is AI inference, as companies need a large number of inference servers to implement AI models into actual applications.

The PC market performed better than expected in the first half of the year, but this was a result of brands pulling inventory ahead of price increases and the overdraw of Windows 10 upgrades; demand remains weak in the second half of the year.

The supply bottleneck is the real constraint factor. CPUs, motherboards, memory, PCBs, and power devices are all constrained.

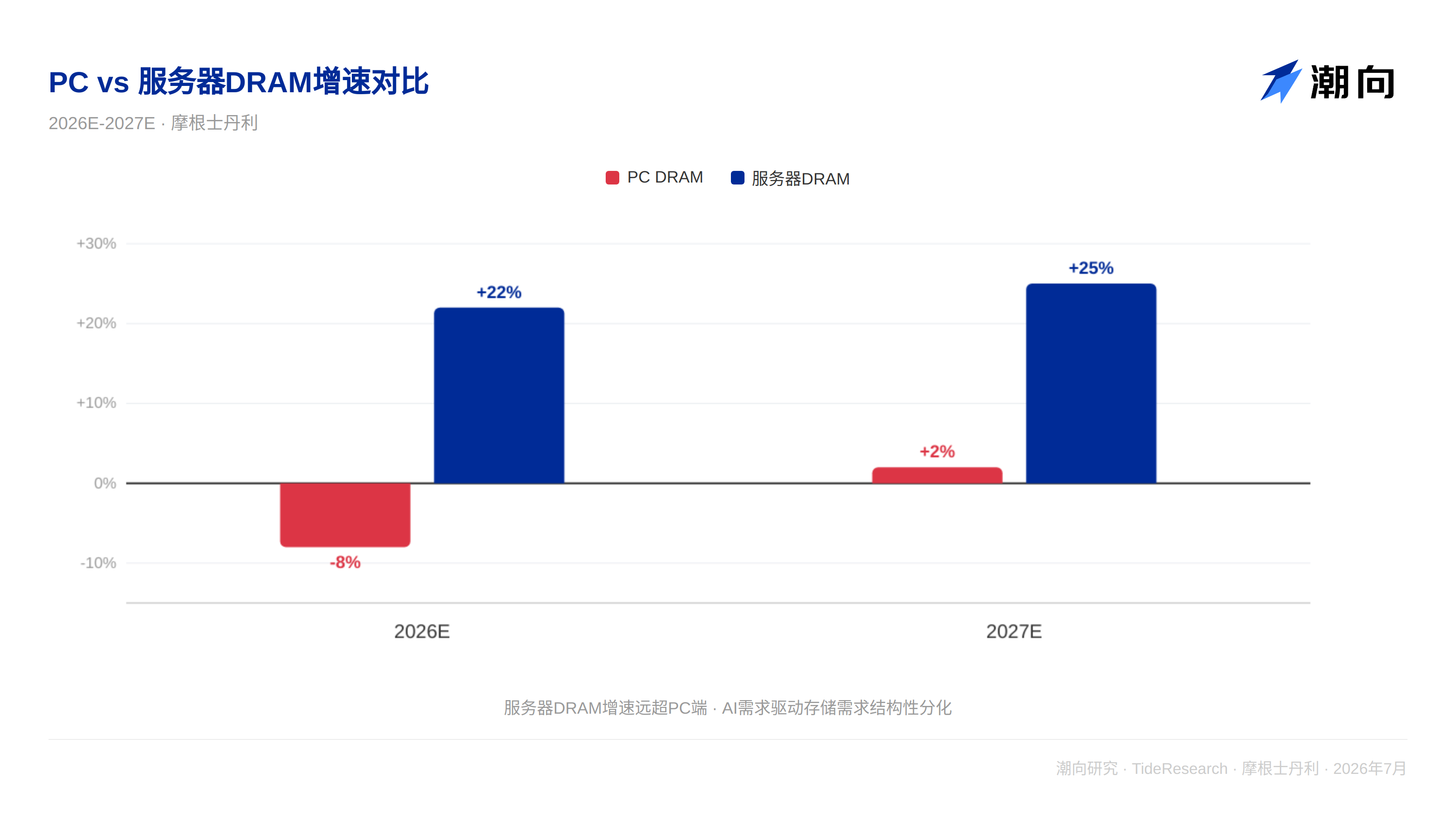

Servers are rising, PCs are falling

J.P. Morgan expects PC shipments to decline by 8% in 2026, while servers will grow by 22%; in 2027, PC shipments will grow by 2%, and servers will grow by 25%.

This divergence is structural. Servers benefit from the continuous growth in AI inference demand. J.P. Morgan estimates that shipments of AI accelerators will have a compound growth rate of 50% from 2025 to 2028, and the demand for CPUs for AI server management nodes will have a compound growth rate of 74%. By 2028, global server CPU shipments will increase from 26 million units in 2025 to 68 million units, representing a three-year compound growth rate of 38%. Among these, the demand for Agentic AI server CPUs will reach 53 million units, becoming the main incremental driver.

In contrast, the PC market is pressured by rising memory prices and overdrawn demand. The BOM cost of high-end laptops has risen by 30% in one year, with the share of memory skyrocketing from single digits to 25%. Brands have raised prices to maintain gross profit, at the cost of sales volume. J.P. Morgan predicts that consumer PC shipments will decline by 14% in 2026, while commercial PC shipments will decline by 4%.

The supply bottleneck and Nvidia's roadmap are two major variables

Demand has increased, but supply is constrained. J.P. Morgan's research shows that server demand has grown by 35% to 40% year-on-year, yet the shipment growth in 2026 can only reach 22%. CPUs, motherboards, memory, PCBs, passive devices, and power components are all facing constraints.

In the U.S. stock market, Dell's AI server backlog has reached $51.3 billion, and J.P. Morgan analysts maintain an overweight rating, raising the target price from $280 to $500. Hewlett Packard Enterprise (HPE) has also had its target price raised by J.P. Morgan, reflecting confidence in AI and high-performance computing demand. Supermicro (SMCI) also benefits from the continued growth in AI server demand.

ODM order visibility has already extended to 2027. Orders not fulfilled this year will carry over to next year, so server shipment growth in 2027 is expected to accelerate further to 25%.

Nvidia's roadmap also brings uncertainty. The Vera Rubin is scheduled for mass production in Q3 to Q4 of 2026, with a total of 70 to 80 thousand NVL72 units expected for the year, and 85 to 95 thousand units anticipated in 2027. The next generation, Vera Rubin Ultra, is expected to be released in the second half of 2027 to 2028, while the Kyber cabinet architecture has faced signal performance challenges regarding PCB and CCL materials, potentially causing delays in the Feynman generation.

Value is migrating towards components

The changes in BOM costs point to a clear direction: money is flowing towards component manufacturers. The prices of the GB300 and VR200 cabinets are 20% to 90% higher than the GB200, with VR200 memory comprising about 20% of BOM, compared to only 10% during the GB200 period. For component manufacturers, this is a window of rising volume and price; for PC brands, this is a source of pressure on gross margins.

In the U.S. stock market's component sector, Arista Networks (ANET) is a core beneficiary in the data center switch segment. Amphenol (APH) has positioned itself in the high-speed connector sector and benefits from increased interconnection density within cabinets. Corning (GLW) has reached a multi-billion dollar fiber optic supply agreement with Amazon, directly benefiting from the expanding demand for data center interconnections. Lumentum (LITE) has exposure in optical communication and optical engine directions. Micron (MU), as a memory supplier, directly benefits from rising BOM costs.

J.P. Morgan's allocation recommendation is straightforward: server components are favored over ODMs. Overall, avoid PCs.

Trend Perspective

The most valuable aspect of this report is that it distinguishes the roles of inference and training within the cycle. It does not conclude merely that "servers are good, PCs are bad". The market had been trading based on training compute power, but is now realizing that the sustainability of inference demand is stronger.

The risk lies in the possibility that the deployment speed of Agentic AI may be slower than expected, making the forecast of 53 million CPUs too high. Additionally, Nvidia's Kyber architecture has encountered signal issues regarding PCB and CCL materials, possibly delaying CPO mass production until 2028. For the optical interconnect industry chain, this represents a time window, not an endpoint.

Regarding PCs, supply chain data for the second half of the year may still fall below expectations, but the market has already partially priced this in.

Disclaimer

This article is a整理与解读 of J.P. Morgan's research report dated July 15, 2026, by Trend Research. The ratings, target prices, profit forecasts, and related judgments quoted in the text are the views of the broker's analysts and only represent their institutional positions, not the views of Trend Research, nor do they constitute any investment advice.

The market carries risks; decision-making should be independent. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。