Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: Ondo Finance has become the first crypto protocol to issue tokenized stocks based on DTCC's tokenization service, upgrading its underlying assets from offshore SPV synthetic exposure to DTC direct-held securities. The platform's TVL surpassed $1 billion within 8 months, capturing over 70% of the tokenized stock market share. However, the ONDO token remains purely a governance token, with no fee-sharing mechanism, and its price has dropped over 85% from historical highs, with 1.94 billion tokens unlocking in January 2027. The platform is growing rapidly, but the token is still waiting for a new opportunity.

On July 15, Ondo Finance announced the launch of the first batch of tokenized stocks based on DTC tokenized equity, with underlying assets being Circle's listed stock (CRCL) and the SPDR S&P 500 ETF Trust (SPY). This is not just another partnership announcement; it represents a substantial upgrade of Ondo's tokenized stock product structure.

Previously, Ondo's tokenized stocks were issued through a bankruptcy-remote SPV established in the British Virgin Islands, with the underlying securities held in custody by U.S. registered broker-dealers. Now, part of the underlying assets can generate DTC tokenized equity through the DTCC tokenization service, allowing free conversion between traditional and tokenized forms. These transactions were executed on July 15 in the DTC production environment, with over 30 institutions participating, covering use cases such as stock conversions, securities lending, and stock delivery against delivery.

In simple terms: Ondo's tokenized stocks are transitioning from "synthetic exposure wrapped in offshore SPVs" to "tokenized equity directly endorsed by U.S. securities infrastructure."

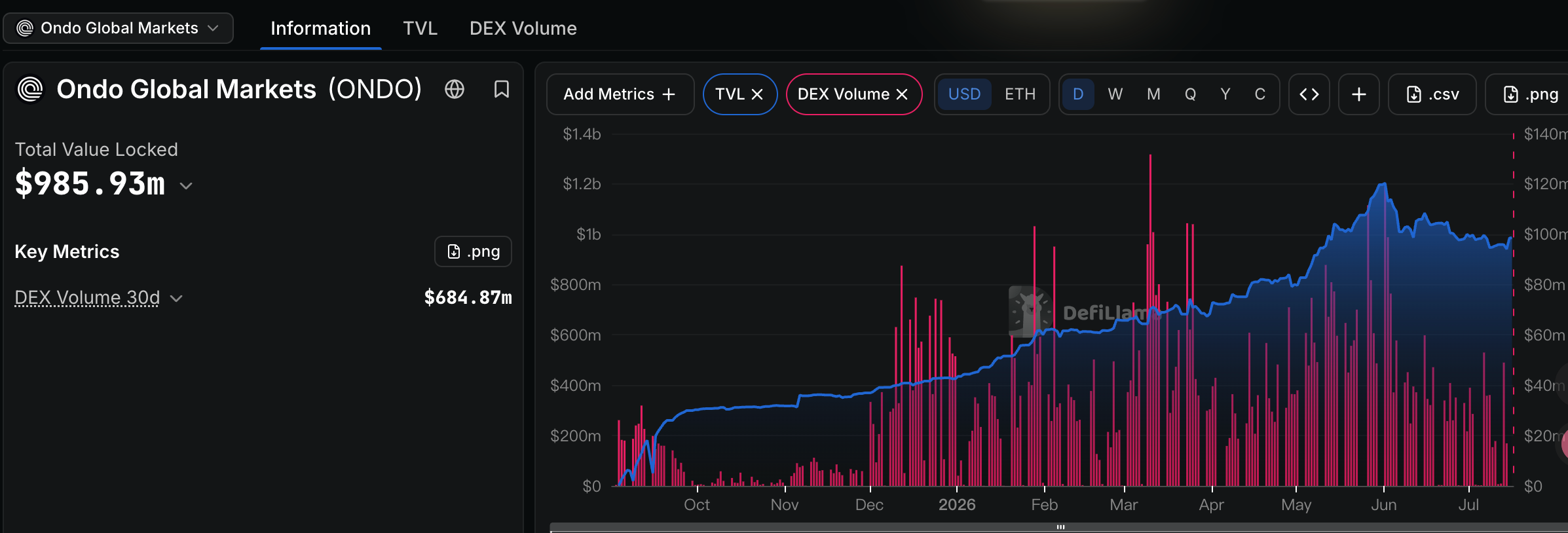

TVL surpasses $1 billion in 8 months, absolute leader in the tokenized stock sector

First, let's look at the data from the Ondo platform itself.

Ondo Global Markets (now renamed Ondo Stocks) launched in September 2025, and within just 8 months, the TVL surpassed $1 billion, with cumulative trading volume exceeding $18 billion and a market share of over 70%. Ondo CEO Ian De Bode compared this pace against industry background: it took stablecoins about three years to reach $1 billion TVL, tokenized government bonds took around two years, while tokenized stocks only took eight months.

As of now, Ondo Stocks covers over 430 types of tokenized U.S. stocks and ETFs, deployed on Ethereum, Solana, and BNB Chain, distributed through channels like Binance, Bitget, MetaMask, and Blockchain.com. Each token is backed 1:1 by underlying securities, tracking total returns (including dividends), and supports minting and redemption five days a week, 24 hours a day. At the beginning of July, Ondo further enabled 24/7 instant minting and redemption for six core assets (NVDAon, TSLAon, GOOGLon, SPYon, QQQon, CRCLon) on Solana.

De Bode's expectation for the end of the year is that the global tokenized stock market TVL will reach between $2.5 billion and $3 billion. If Ondo maintains a 70% market share, this means its own TVL will be between $1.7 billion and $2.1 billion.

Regarding competitors, Backed Finance, Swarm, and Dinari lag significantly behind in terms of TVL and asset counts. Ondo's lead is not only due to its first-mover advantage but also its compliance moat: Ondo has secretly submitted a registration statement to the SEC, and if approved, will become the first transfer agent for tokenized stocks subject to SEC reporting requirements. Additionally, Ondo has acquired a U.S. brokerage to internalize its compliance capabilities; its tokenized securities have been approved for trading in markets covering 30 European countries and are listed on the Binance multilateral trading facility in the Abu Dhabi Global Market (ADGM).

What has changed with DTCC integration?

DTCC is the core post-trade infrastructure of the U.S. securities market, with its subsidiary DTC holding assets of over $114 trillion. In December 2025, DTC received a three-year no-action letter from the SEC, authorizing it to provide tokenization services for Russell 1000 components, major index ETFs, and U.S. Treasury securities.

The CRCLon and SPYon issued by Ondo have their underlying DTC tokenized equity generated through DTCC's tokenization service, serving as a "digital twin" of the existing tokenized stocks’ underlying securities. The securities held by DTC can be converted between traditional and tokenized forms.

This means three changes for Ondo's products:

First, the legal rights level has been elevated. Previously, the legal rights of Ondo's tokenized stocks derived from the debt instrument structure of the BVI SPV, and token holders did not have direct shareholder voting rights. With DTC's integration, the underlying securities possess ownership and dividend rights equivalent to traditional book equity, with clearer legal positioning.

Second, composability expands. DTC tokenized equity can flow between DTC participant wallets, meaning Ondo's tokenized stocks may potentially integrate with traditional financial institutions' collateral management and securities lending workflows. On the same day, J.P. Morgan completed the tokenization conversion of the QQQ ETF and submitted margin to CME Group using tokenized assets, marking the first acceptance of tokenized assets as collateral by a central clearing counterparty.

Third, and most critically, in the initial phase, tokenized securities only support free-of-value transfers between DTC registered wallets, and tokenized securities are not currently counted towards DTC's collateral value and end-of-day settlement value. Full on-chain transactions with digital cash settlement will be developed in subsequent phases. DTCC's full rollout is scheduled for October.

In other words, DTCC has given Ondo a ticket to enter the traditional financial infrastructure, but this ticket currently only opens some functionalities.

DTCC news drives ONDO up over 16% in a single day, with intensive short-term catalysts

After the DTCC news was released, the ONDO token rose by approximately 16.6% within 24 hours, reporting at $0.3666, with a 24-hour trading volume surging by 228% compared to the previous day, reaching about $155 million.

The market's reaction logic is clear: the soft launch of DTCC's tokenization service has transformed Ondo from a "crypto-native RWA protocol" to a "tokenized issuer accessing U.S. securities core infrastructure," altering institutional credibility.

I believe this catalyst has not fully played out in the short term. DTCC's tokenization service will fully launch in October, at which point DTC-held tokenized securities will have access to more complete settlement functions, including collateral management and DVP transactions.

As the first crypto protocol to issue tokenized stocks based on this service, Ondo has already seized the window for institutional connections and product iteration. Moreover, Ondo has secretly submitted a registration statement to the SEC, which, if approved, will make it the first transfer agent for tokenized stocks subject to SEC reporting requirements, which in itself is an independent price catalyst event.

Research institution De Bode expects that the global TVL of tokenized stocks will reach between $2.5 billion and $3 billion by the end of the year. If Ondo maintains over 70% market share, this means that Ondo Stocks' TVL will approach the $2 billion level, doubling from the current approximately $978 million. His long-term reference point is Robinhood's approximately $350 billion in custodial assets, believing that the ceiling for tokenized stocks is far above current levels.

However, in the long term, for long-term investors, I believe the investment logic of ONDO is essentially betting on the leader premium in the RWA tokenization sector.

ONDO has a total supply of 10 billion tokens, with about 4.87 billion currently in circulation. In January 2025 and January 2026, large unlocks of 1.94 billion tokens each occurred. The next round of unlocks is expected in January 2027, with the release pace continuing until 2029. Historical unlock events have triggered short-term price volatility (with a continuous sell-off triggered in January 2025 and a 10% drop on the day in January 2026), but the market's capacity to digest the unlock events is gradually increasing.

Currently, ONDO is a governance token, with protocol revenues (OUSG management fees, USDY earnings, Ondo Stocks transaction fees) flowing to the underlying business entities. If the fee mechanism can be activated, it will provide substantial positive benefits for the token price.

The leader in RWA tokens is still waiting for a market answer among short-term catalysts.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。