Connect the entire ecosystem, fight hard for the financial super entrance

Written by: ChandlerZ, Foresight News

In the first half of 2026, the cryptocurrency market showed a rare division. Bitcoin pulled back more than 35% from its peak, the total locked value in DeFi was halved to 72 billion dollars, and several cryptocurrency companies that originally planned IPOs pressed the pause button. According to historical experience, these numbers usually herald the arrival of another winter.

However, during the same half-year of price cooling, another set of data accelerated. The U.S. SEC and CFTC concentrated on releasing signals regarding the regulatory direction for U.S. cryptocurrencies, with the SEC’s new documents explicitly defining 16 crypto assets, including BTC and ETH, as "digital commodities"; the U.S. Depository Trust & Clearing Corporation (DTCC) advanced DTC tokenization services, collaborating with over 50 financial institutions, including traditional finance and crypto entities like BlackRock, JP Morgan, Circle, Ondo Finance, and Robinhood; the total market cap of stablecoins reached a historic high of 322 billion dollars in May, surpassing the foreign exchange reserves of over 95 countries; the number of global cryptocurrency holders reached approximately 700 million.

Prices are contracting, while infrastructure is expanding. The two lines are moving in opposite directions, which might precisely mark that the industry is shifting from speculation-driven to infrastructure-driven.

Founded on July 14, 2017, Binance has accumulated over 300 million registered users in nine years, operating under licenses in more than 20 jurisdictions, experiencing the largest regulatory penalties in the industry, and witnessing the entire process from the ICO boom to institutional entry. On the ninth anniversary, a more valuable question than reviewing history is, what directions has this company bet its resources on? What logic lies behind these judgments? To what extent can they represent the trends of the entire industry?

Where is the market of 3 billion people

Binance's co-CEO Richard Teng repeatedly mentions the same figure in various public appearances: by 2030, 3 billion users. This goal is ten times the current 300 million registered users. According to Binance's growth curve, it reached 100 million users in the first five years, then 200 million in the following two years, and recently broke through 300 million in the past 18 months, with an average of over 180,000 new users daily. The growth rate is accelerating, but going from 300 million to 3 billion still means finding a completely different scale of growth engine.

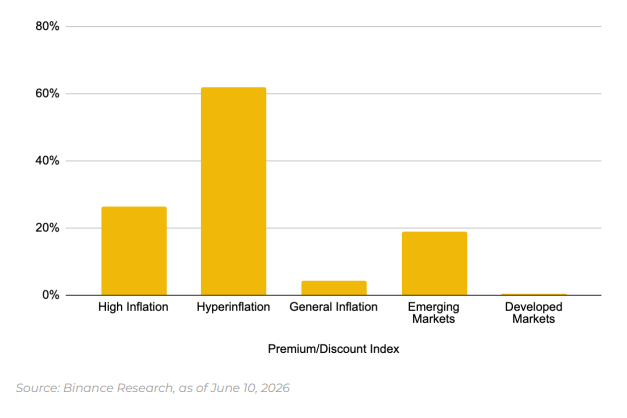

Where does this growth come from? A stablecoin report released by Binance Research in July 2026 provides some clues. The report shows that among Binance's user base, 87% of fiat currency needs to pay a premium higher than the official exchange rate when converting to stablecoins. This gradient of premium corresponds precisely to the level of inflation, with users in hyperinflationary economies (inflation rate over 10%) paying an average premium of 62%, those in high-inflation economies (over 5%) paying 27%, and those in normal inflation environments paying 4%. The average premium for users in developed markets is just 0.3%.

What does a 62% premium mean? A user in Nigeria or Argentina is willing to pay a cost 60% higher than the official exchange rate to convert local currency into stablecoins. The driving force behind this behavior is wealth preservation; in an environment where the local currency continuously depreciates, stablecoins act as a no-threshold dollar savings account, requiring no U.S. bank account, no foreign exchange quotas, and no minimum deposits.

Traditional fintech (such as M-Pesa, Mercado Pago, etc.) also serves the financial needs of emerging markets, but they provide payments and transfers in local currency. When the core demand of users is to escape the local currency for dollar-denominated savings and earnings, crypto services offer products that traditional fintech cannot replace, such as dollar stablecoin savings, cross-border transfers without intermediaries, and 24/7 liquidity.

Willingness to pay a 62% premium to acquire an asset has nothing to do with speculation. In economies with currency depreciation, capital controls, and restricted foreign exchange channels, stablecoins essentially serve as a borderless dollar savings account. The premium users pay is the cost they bear for preserving purchasing power.

Geographic data confirms the scale of this demand; the share of stablecoin P2P transfers in Latin America and the Caribbean doubled from 17% to 38% over the past year, becoming the fastest-growing region. The on-chain value in the Asia-Pacific region grew by 69% year-on-year, while Latin America saw a growth of 63%. Globally, approximately 700 million people hold crypto assets, accounting for 8.5% of the world's population, with India leading with 156 million, Nigeria with 45 million, and Turkey achieving a per capita penetration rate of 25.6%.

Whether the 3 billion user goal can be achieved still faces many uncontrollable variables, such as national regulatory policies, competitive landscape, and macroeconomic trends. But at least from the demand side, a large population globally still faces issues of local currency instability and inadequate financial service coverage, which is a sufficiently large base. In March 2026, the head of Binance's Asia-Pacific region revealed in an exclusive interview with Nikkei Asia in Tokyo that Binance plans to acquire 5 regulatory licenses in Asia within 2026 to prepare for this incremental user base.

The logic behind achieving 3 billion users hinges on the fact that many populations worldwide still have basic financial needs unmet by traditional systems, and crypto services are filling this gap. To enter these markets, the first issue that needs to be resolved is compliance.

A 4.3 billion dollar window of time purchased

In November 2023, Binance reached a settlement with the U.S. Department of Justice, paying a fine of 4.3 billion dollars, and founder CZ stepped down as CEO. This was the largest regulatory penalty in the history of the crypto industry. The general judgment at the time was that Binance's market position would thus be shaken.

More than two years have passed, and the result is contrary to expectations. Binance currently operates under license in over 20 jurisdictions worldwide, with annual compliance spending exceeding 300 million dollars and a compliance team of over 1500 people. In March 2026, it obtained ISO 22301 certification. It currently holds licenses in Australia, India, Indonesia, Japan, New Zealand, and Thailand in the Asia-Pacific region.

Binance's compliance transformation occurred within a unique industry time window. According to the Atlantic Council's "Cryptocurrency Regulatory Tracking Report," by 2024, only 42 countries globally had established or were advancing crypto-specific legislation. By 2026, this number is expected to grow to 68, an increase of 62%. At the same time, the "Crypto Asset Reporting Framework" (CARF) will come into effect in 2027, with the first 48 jurisdictions starting data collection from 2026.

As regulation shifts from hostility to a structured framework, the value of compliance capability fundamentally changes. In a lack of regulatory environment, compliance is a cost; in a well-defined regulatory environment, compliance is a barrier. According to Binance's year-end report for 2025, the number of institutional users on the platform grew by 14% year-on-year, and institutional trading volume increased by 13%; additionally, according to Catherine Chen, head of Binance's VIP and institutional business, as of May 2026, over 15 large financial institutions have accessed or are in the process of accessing Binance's Crypto-as-a-Service platform; furthermore, the institutional-grade collateral program launched by Binance allows qualifying institutional clients to use tokenized money market funds (MMF) issued by platforms like Franklin Templeton as collateral for off-exchange trading.

All these institutional business prerequisites are based on compliance qualifications.

The 4.3 billion dollar fine in 2023, in retrospect, bought a time window. While most competitors are still dealing with regulatory uncertainties, Binance has already established a compliance system that can operate in dozens of legislative countries. The early costs paid are turning into later access advantages.

Stablecoins: From trading tools to financial infrastructure

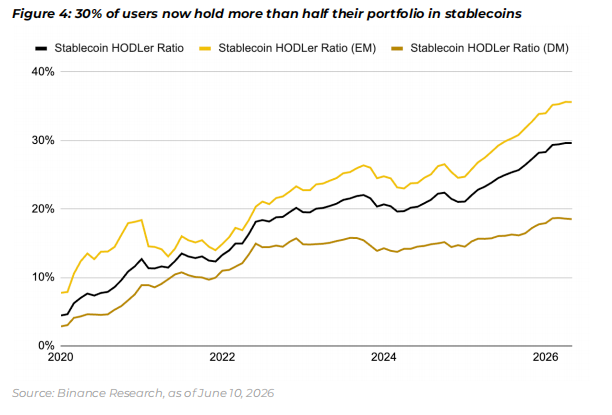

On the Binance platform, a change that has been continuously occurring over the past six years, transcending all bull and bear cycles, is the increasing share of stablecoins in user assets. Among users holding at least 10 dollars in their portfolios, 30% allocate more than half of their assets to stablecoins. This proportion was only 4% in 2020. Whether in the bull market of 2021 or the crash of 2022, this trend has not changed direction. The proportion of users from emerging markets reached 36%, while developed markets gradually rose from 14% to 19%.

This set of data challenges a long-standing assumption that stablecoins are merely transit stations for transactions. If users are only temporarily holding stablecoins during the intervals of buying and selling cryptocurrencies, the allocation ratio of stablecoins should vary significantly with price fluctuations. In reality, it has not. More and more users are treating stablecoins as assets to be held long-term, akin to a dollar savings account with far higher yields than bank deposits.

Binance currently holds 53 billion dollars in stablecoin reserves, leading the second place by 42 billion dollars, with its share rising from 54% at the beginning of 2025 to 57%. This concentration has multiple reasons, including liquidity depth attracting traders, Earn products (which have distributed 1.2 billion dollars in returns to stablecoin holders) retaining savings-type users, and a rich variety of trading pairs reducing the motivation to migrate to other platforms. No single factor can explain it; it is the result of multiple product segments acting together.

After the suspension of BUSD in 2023, Binance abandoned the single proprietary stablecoin route, shifting to an open multi-stablecoin ecosystem, integrating FDUSD, Circle's native USDC, and World Liberty Financial's USD1, among others. In 2026, four of the six fastest-growing stablecoins are primarily circulating on Binance and BNB Chain. 97% of USYC’s supply is on BNB Chain, 95% of United Stable (U) is in the Binance ecosystem, and 87% of USD1 is on Binance and BNB Chain. These stablecoins choose Binance's ecosystem as their main battlefield, with liquidity depth and user base being key considerations; Binance's business value as a distribution channel continues to attract new issuers.

From an industry perspective, the scale of stablecoins has already far exceeded the intrinsic needs of crypto trading. Visa's on-chain analytics team estimates that by June 2026, the adjusted stablecoin transaction volume for a single month reached 17.9 trillion dollars, totaling approximately 88.2 trillion dollars in the first half of the year, a year-on-year increase of 125%. Every weekend, during 60 hours of traditional financial market shutdowns, stablecoin transfer activity averages 76 billion dollars, equivalent to about 38 billion dollars daily, on par with Visa's daily transaction volume. This illustrates that stablecoins have embedded themselves into financial workflows that are not restricted by traditional market timings.

More cutting-edge signals come from AI agent payments, which are currently very small in scale but worth noting in direction; the median payment amount for AI agents on the x402 protocol is merely 0.34 dollars, with the number of merchants growing fourfold to over 7,500 by 2026. AI agents cannot open bank accounts or complete identity verifications, making the permissionless nature of stablecoins one of the natural options for small payments between machines.

RWA is another growth line beyond stablecoins. The total value of on-chain RWA has reached approximately 31 to 33.5 billion dollars (excluding stablecoins), growing nearly threefold within a year. In July, DTCC began production environment testing of tokenized securities with over 50 institutions. BCG and Standard Chartered predict that the RWA market will reach 16 trillion dollars by 2030. Binance currently occupies about 60% of the CEX RWA trading volume, integrating institutional-grade products such as BlackRock BUIDL, Franklin Templeton BENJI, and VanEck VBILL on BNB Chain.

The growth of stablecoins and RWA both depend on the carrying capacity of underlying infrastructure. For Binance, this means that BNB Chain needs to keep pace with business expansion.

Infrastructure catch-up and financial super entrance

Traditional financial institutions spend over 2 billion dollars annually on advanced order management systems, while the corresponding investment in the entire crypto industry is only about 185 million dollars. This gap is reflected in various aspects such as risk control systems, clearing efficiency, custody security, and compliance reporting. As institutional funds accelerate their entry, the maturity of infrastructure will directly determine which platforms can accommodate these funds.

BNB Chain is Binance's core investment direction at the infrastructure level. In the first half of 2026, BSC has completed multiple performance upgrades, including reducing block intervals from 750 milliseconds to 450 milliseconds, lowering memory final confirmation time from 1,125 milliseconds to 650 milliseconds, and increasing the benchmark throughput from approximately 2,800 TPS to about 5,200 TPS. According to its published technical roadmap for the second half of 2026, BNB Chain plans to double the throughput of the BSC mainnet again and develop a new generation Layer 1 architecture for the next decade.

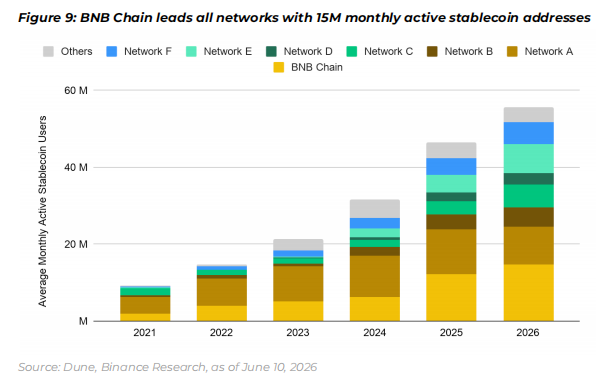

In practical use, BNB Chain handles an average of 10 million stablecoin transactions daily, with 15 million active stablecoin addresses monthly, and has cumulatively processed 5.3 billion stablecoin transactions since 2025, accounting for 24% of the total transaction volume on the network, ranking first. Monthly active addresses grew nearly 30% year-on-year by 2026.

In addition, Binance Pay covers 21 million registered merchants, with monthly transaction volume growing by 114% year-on-year, and stablecoins account for 98% of total payment volume. The median payment amount increased from 10 dollars in 2025 to 18 dollars in 2026. The change from 10 dollars to 18 dollars is not drastic, but considering that early stablecoin payments mainly consisted of top-ups and minor tests, this increase in amount may indicate that more daily consumption and business transactions are starting to be completed through this channel.

In terms of expanding transaction categories, Binance is testing the feasibility of carrying traditional financial assets on crypto tracks. TradFi-Perps started with nearly zero in early 2026, and within five months, the cumulative trading volume surpassed 1.1 trillion dollars, accounting for approximately 11% of total perpetual contracts. Binance holds over 500 billion dollars in trading volume in this category, with a market share of about 47%. This data indicates that there is indeed demand for users to gain exposure to traditional financial assets through crypto tracks, and its scale is considerable.

Binance has currently launched zero-commission trading for over 7,000 U.S. stocks and ETFs, with fractional shares available for as low as 5 dollars. The on-chain tokenized securities product bStocks builds on this by turning stocks held in brokerage accounts into verifiable on-chain tokenized assets.

The distance between derivatives and spot tokenization is greater than it seems. Perpetual contracts are essentially price exposure tools and do not involve real ownership of the underlying assets. Tokenized stocks, however, need to address a series of issues related to securities legal frameworks, cross-border custody, investor protection, and tax compliance. These issues primarily focus on the legal and regulatory dimensions, with the speed of advancement depending on the attitudes of various jurisdictions.

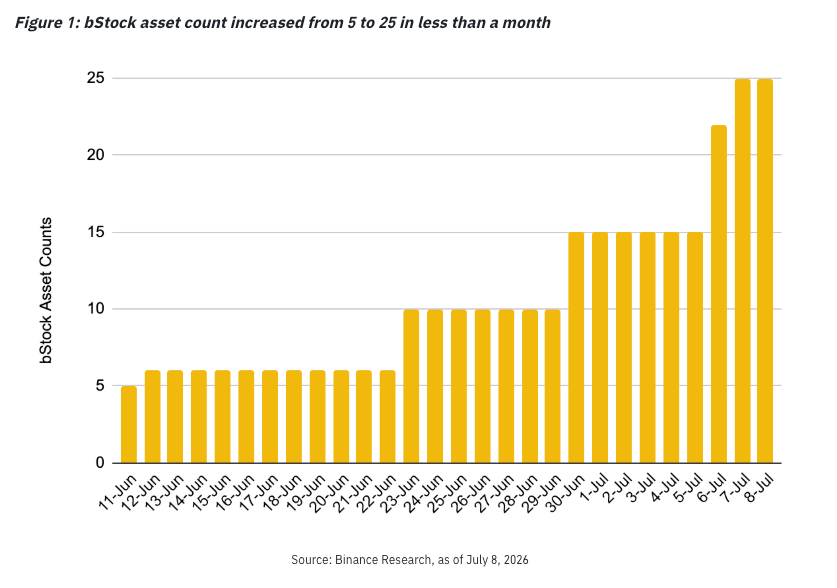

Within less than a month of its launch, the number of tokenized stock assets on bStocks increased from 5 to 25, with the on-chain market value approaching 300 million dollars. Interestingly, among the 190,417 bStocks users, 2,806 participated in cross-market arbitrage, with 206 systematic arbitrage users contributing 198.2 million dollars in rapid matching trading volume, accounting for 96.5% of related transaction volume.

Moreover, the appeal of bStocks is particularly evident during non-trading hours. During regular trading hours, the share of stock spot trading volume is 52%, while bStocks accounts for 48%; however, during non-trading hours, the proportion of bStocks trading volume rises to 58%, surpassing the 42% of stock spots. At the same time, bStocks has also begun to extend into on-chain yield scenarios.

The path of bStocks is significant for Binance beyond just a single product level. When a platform can provide cryptocurrency trading, U.S. stock investment, tokenized asset holding, stablecoin saving, and payment services all within the same account, its nature transforms from an exchange to a super comprehensive entry point for financial services. BNB Chain's performance upgrades provide the technical foundation for the settlement of tokenized assets, while the stablecoin ecosystem offers pricing and settlement currencies, and the compliance system provides qualifications for operations in various markets. The synergy between these three components forms the infrastructure supporting this entry point.

In the world of traditional finance, Morgan Stanley launched the first BTC ETF issued by major U.S. banks in April 2026. This fund holds actual bitcoins and is the first spot bitcoin ETF directly issued by a major commercial bank in U.S. history. JP Morgan plans to allow institutional clients to use their BTC and ETH holdings as collateral for loans, blurring the boundaries between traditional finance and crypto finance in 2026.

Binance's positioning at this intersection depends on how well it can simultaneously meet the demands of both sides: providing a rich variety of traditional asset classes for crypto users and offering sufficiently mature infrastructure and compliance guarantees for traditional financial users and institutions.

Conclusion

From user growth, compliance layout, stablecoin ecosystem to infrastructure construction, there exists a logical chain among these four investment directions of Binance. The financial demand from emerging markets provides a user base, the compliance system opens up market access, stablecoins become the most core usage scenario for these users, and infrastructure and bStocks determine how much capital volume and asset categories this platform can bear.

Nine years ago, the problem for this industry was how to get people to buy Bitcoin. The question for 2026 has changed; crypto technology is evolving from an independent asset class into part of the global financial infrastructure.

How long this process will last and how far it will ultimately go is filled with uncertainties. But at least currently, the most meaningful competition in the crypto industry has shifted from transaction volume rankings to another dimension; the one who can first build the infrastructure connecting the crypto world and traditional finance will define the next stage of the industry landscape. Binance has provided its answer to this question.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。