Author: CryptoSlate

Translated by: ShenChao TechFlow

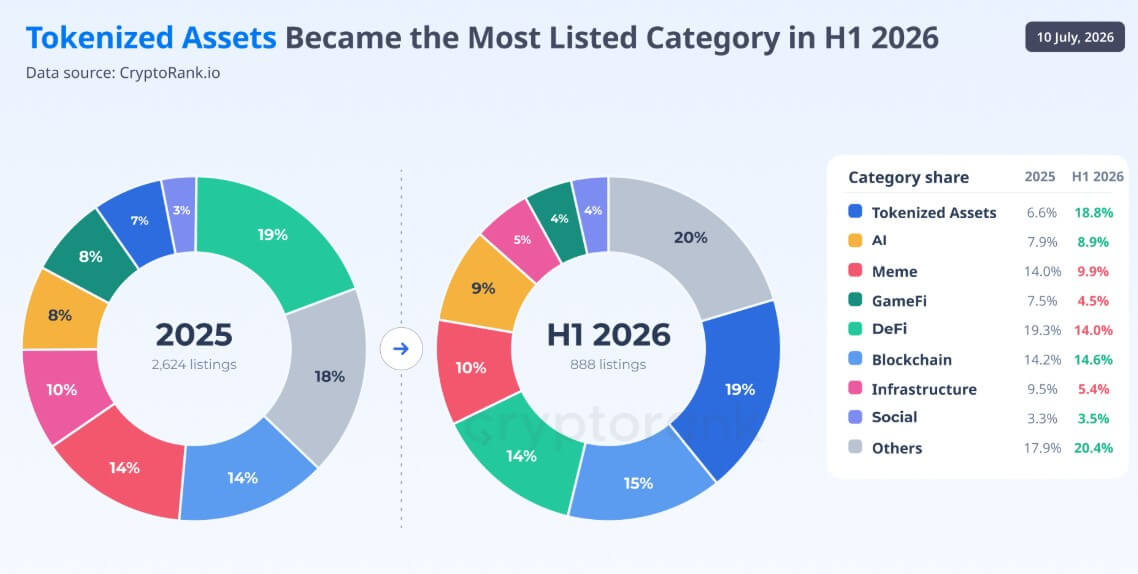

ShenChao Introduction: Cryptocurrency exchanges are transitioning from a hub for meme coins to distribution platforms for Wall Street products. In the first half of 2026, tokenized assets became the largest category of new listings on exchanges, accounting for nearly 20%, compared to less than 7% in 2025. This shift occurs as retail investors in the U.S. stock market hit a new low in net buying since the pandemic, while global RWA perpetual contract trading volume soared to a new high of $311 billion in June — capital is voting with its feet, choosing tokenized stocks that can be traded 24/7 and in fractional amounts, instead of traditional brokerage accounts.

Tokenized assets became the largest category of new listings on major centralized exchanges in the first half of 2026, with nearly one in five new tokens being tokenized assets, according to CryptoRank data. This category accounted for less than 7% in 2025.

This wave of expansion is primarily driven by platforms like xStocks, bStocks, and Ondo’s tokenized stock market.

Their rise marks a sharp pivot in exchange strategy — over the past few years, meme coins, game tokens, and other crypto-native assets dominated the pipeline for new listings.

This shift occurs while retail participation in U.S. stock trading cools. Over the past month, U.S. retail investors have net bought $13 billion in stocks, a record low since the pandemic began, according to financial analytics firm VandaTrack.

Net buying decreased by $18 billion from early 2026 levels, a decline of 58%. Individual stock purchases fell by 71% to $3.2 billion.

The U.S. data covers different markets and investor demographics and differs from global tokenized asset data. However, cryptocurrency exchanges are indeed expanding stock-linked products for users seeking continuous trading, fractional access, and exposure beyond traditional brokerage infrastructure.

Tokenized stock trading has scaled

The rapid growth of derivatives activity has given exchanges clearer reasons to expand Wall Street-linked products.

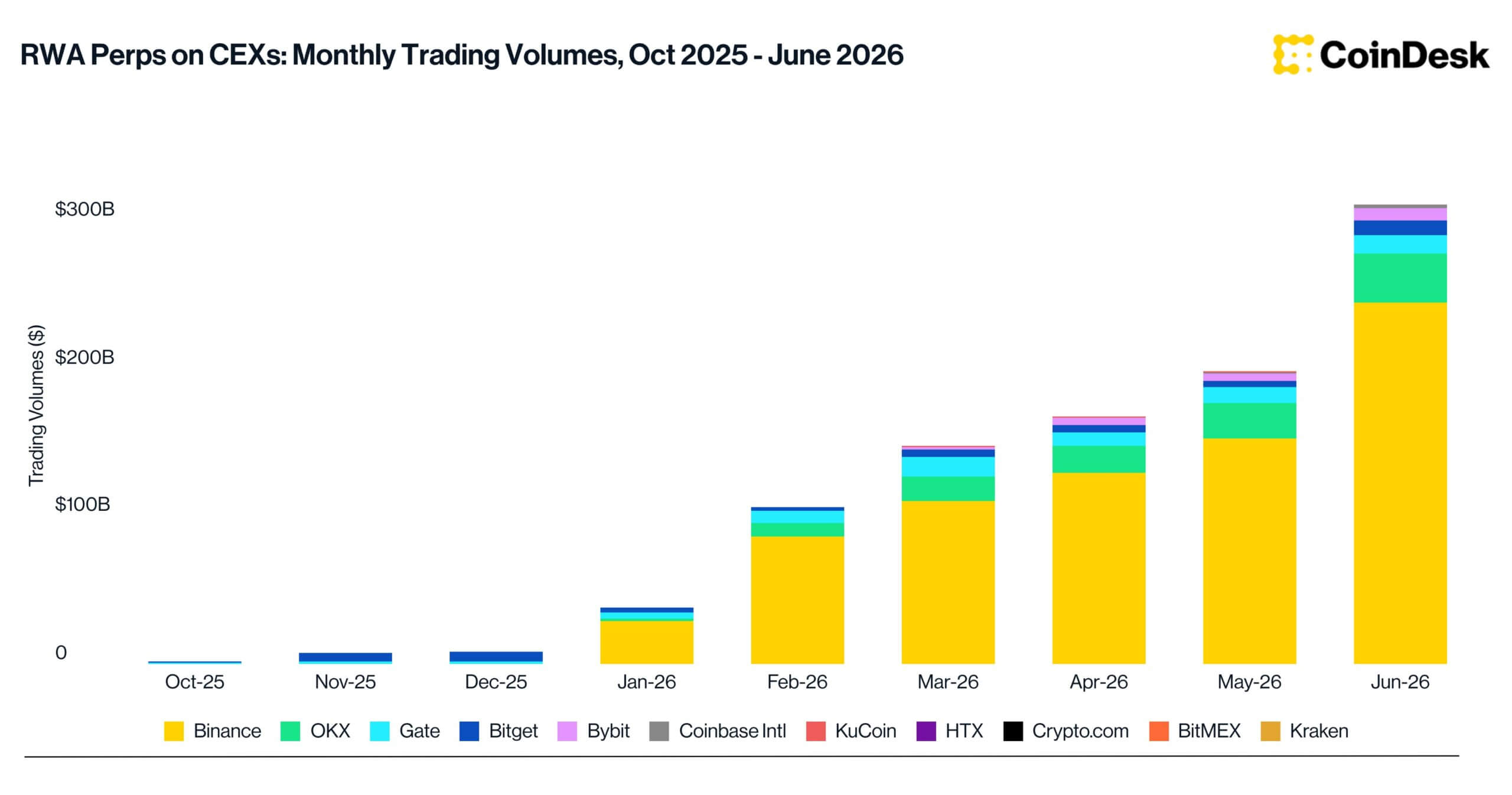

Trading volume for real-world asset perpetual contracts on centralized cryptocurrency exchanges rose 57% in June to a record $311 billion, according to CoinDesk exchange data. Binance accounted for $245 billion, with a market share of 78.6%.

This category had almost no activity at the end of 2025, then it expanded sharply in the first half of 2026.

SpaceX's initial public offering helped accelerate the demand for exposure to traditional financial instruments based on crypto, especially among traders seeking access beyond the limitations of traditional brokerage and stock market infrastructures.

Perpetual contracts allow users to speculate on asset prices without holding the underlying securities and without an expiration date. They have become one of the most active products on crypto exchanges, with leverage and 24-hour trading both amplifying trading volume and volatility.

Meanwhile, growth is not limited to derivatives.

Data from RWA.xyz shows that the market size for tokenized stocks grew over 470% in the past year to about $1.87 billion. The monthly transaction volume for these assets also climbed to $8.4 billion, indicating that tokenized stocks are attracting activity beyond the new listing pipeline.

Kraken stated in February this year that total trading volume for xStocks had exceeded $25 billion. This figure includes trading on centralized and decentralized exchanges, as well as minting and redeeming, with on-chain activity exceeding $3.5 billion.

These numbers indicate that as the number of new listings grows, there is measurable activity for both tokenized stocks and derivatives linked to traditional assets.

Fewer new listings on exchanges, Wall Street assets replace crypto darlings

The rise of tokenized assets accompanies a general slowdown in new listings on exchanges, as well as a retreat from the speculative segments that defined the last crypto cycle.

Cryptorank reported that major centralized exchanges had 351 new listings in Q2 2026, the lowest quarterly figure since Q3 2023. New listings have decreased for the second consecutive quarter, marking the second time since early 2024 that the number of delistings has exceeded new listings.

This slowdown follows a record year in 2025 — at that time, new listings peaked with the historical highs of Bitcoin. Exchanges did not replace the lost trading volume with another wave of crypto-native projects but turned to tokenized versions of traditional financial assets.

Tokenized assets became the largest category of new listings in the first half of 2026, while in 2025 they accounted for less than 7% of new listings. In just Q2, exchanges added 42 tokenized assets, following only blockchain infrastructure and decentralized finance.

Meanwhile, categories that dominated the last bull market continue to lose momentum.

New listings for meme coins have decreased for six consecutive quarters. Exchanges added 196 meme coins in Q4 2024, but this number fell to 41 in Q2 2026, a decline of 79% and the lowest quarterly data since Q3 2023.

GameFi has seen an even sharper contraction. New game tokens listed have dropped 84% from the peak in Q2 2024 to only 15 in Q2 2026.

Meanwhile, the broader category of tokenized assets as defined by CryptoRank — including stocks, commodities, and other RWAs — shows stronger persistence than many dominant narratives from the last cycle.

For context, about 7% of the tokens listed in 2025 had been delisted by mid-2026, across all categories. NFT projects had the highest delisting rate at 19%, followed by GameFi at 14% and meme coins at 11%.

No assets from the 172 tokenized assets listed in 2025 by CryptoRank had been delisted by mid-2026.

This lower delisting rate indicates that tokenized assets have thus far been more enduring on exchanges compared to categories like NFT, GameFi, and meme coins. It also supports the notion that exchanges are viewing products linked to mature financial markets as a longer-lasting category for new listings.

Crypto platforms entering traditional brokerage territory

The divergence between weak net stock buying in the U.S. and rising global tokenized stock activity suggests that access to traditional markets is becoming more fragmented.

Cryptocurrency exchanges can combine spot trading, leveraged derivatives, tokenized assets, and stablecoin settlement on a single platform. This structure allows users to switch between exposure to cryptocurrencies and traditional markets without transferring funds to separate brokerage accounts.

Tokenized products can also allow for continuous trading and provide fractional access to assets that may be difficult for some international investors to obtain.

These advantages come with legal and structural differences.

Tokenized stocks may represent claims supported by underlying shares, synthetic tools tracking their prices, or other contractual arrangements. Investors may not receive voting rights, custody rights, or shareholder rights related to directly holding the stocks.

Perpetual contracts provide price exposure but not ownership and may expose traders to risks of leverage, funding rates, and liquidation.

Regulatory restrictions also limit availability in multiple jurisdictions. Many tokenized stock products are unavailable to U.S. residents, even if they track shares of U.S. listed companies.

However, new listing and trading volume data indeed show that centralized exchanges are broadening their roles. Platforms that competed to distribute new crypto-native tokens in the first two market cycles are increasingly competing to distribute financial products linked to stocks, commodities, and other mature markets.

The next major cycle of new listings on exchanges may rely less on issuing thousands of new coins and more on products linked to existing financial assets in a never-closing trading venue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。