Written by: Rita

Guide to Trends

Last quarter's growth was 95%, and management said it is still accelerating, with next year's free cash flow yield exceeding 5%, and more than half likely to be returned to shareholders. This is NVIDIA's performance. But the stock price just doesn't rise. After intensive communication with Jensen Huang and the CFO during last week's roadshow, Morgan Stanley provided an counterintuitive judgment: the problem is not in the fundamentals, but in the buyers. NVIDIA's market capitalization is now so large that there aren’t enough incremental funds to take over, and the largest potential buyer group may come from those who have rarely bought semiconductors in the past. Meanwhile, NVIDIA is trying a new business model, exchanging credit support for a share of cloud service revenues, creating recurring revenue with a 100% gross margin outside of hardware sales. If this model works, the market's valuation logic for NVIDIA will need to be rewritten.

NVIDIA's Buyer Dilemma

After the roadshow, Morgan Stanley communicated with dozens of investors and found that the core issue is: there is no lack of consensus on fundamentals, but rather a lack of new buyers. While peers are generally seeing significant buying, NVIDIA cannot find incremental funds. The reason is straightforward: the size is too large. Value investors and income-oriented funds may be the remedy. With a quarterly growth of 95%, management stating growth is accelerating, and next year's free cash flow yield exceeding 5% with more than half likely to be returned to shareholders, these indicators naturally align with value-oriented funds, which in the past have rarely bought semiconductors. Morgan Stanley believes this is one of the key variables in unlocking NVIDIA's undervalued potential.

NVIDIA is Becoming a Computing Power Bank

The NeoCloud financing support model proposed by NVIDIA in its blog may be the next big topic. The specific approach is: providing credit endorsement for NeoCloud providers in exchange for a share of cloud service revenues, creating recurring revenue streams outside of hardware sales. Credit support involves costs and risks, but Morgan Stanley pointed out that amidst the current computing power shortage, the market's focus is shifting from “what could go wrong” to “what good outcomes could arise.” If it works, this would create a stream of recurring revenue with a 100% gross margin. The market has not calculated this yet, as the costs and risks of credit support are not reflected on the profit and loss statement.

Memory Shortage Extending Cycle

NVIDIA expects the memory shortage to last for several years and is trying to accomplish tasks with less memory. Morgan Stanley interprets this as a long-term positive for the memory cycle: it suppresses price increases in the short term but extends the cycle of high prosperity. Viewing the current memory cycle with area thinking rather than peak thinking, the “total area under the curve” is still quite considerable. Meanwhile, the global shortage of computing power and electricity is prompting countries to reserve resources for their domestic companies, accelerating the localization of AI data centers, and new deployments are emerging after approvals are granted.

Trends Perspective

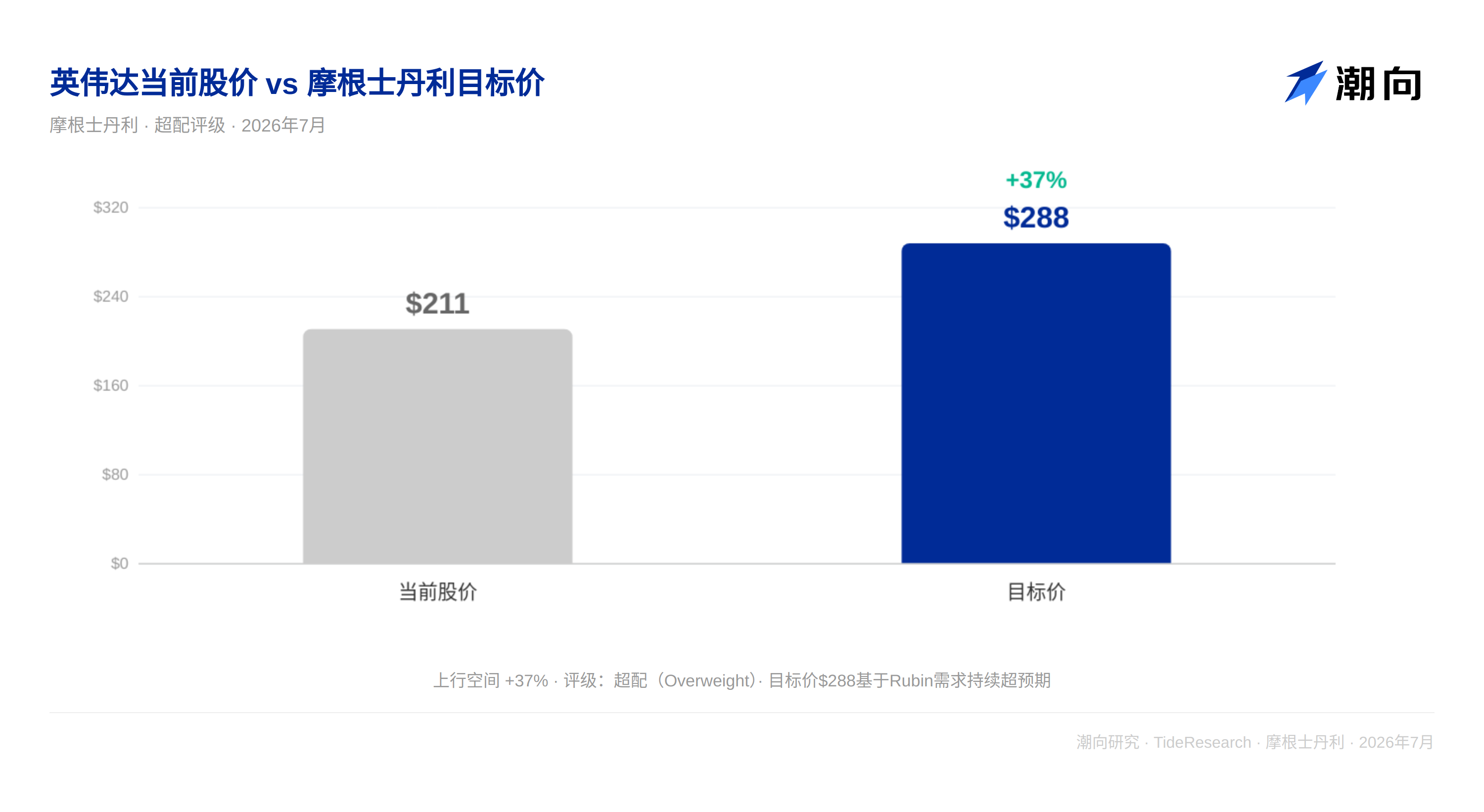

NVIDIA's valuation logic is shifting from "selling chips" to "selling credit." The NeoCloud financing support model transforms NVIDIA from a hardware supplier into a player in the financialization of computing power, providing credit endorsement, exchanging for revenue shares, and obtaining recurring revenue with a 100% gross margin. If this transformation works, the valuation anchor will no longer be quarterly GPU shipments but the yield of the asset pool. Against the backdrop of a computing power shortage, this may be the starting point for NVIDIA's next stage of valuation reconstruction. Morgan Stanley maintains an overweight rating on NVIDIA, with a target price of $288.

Disclaimer

This article is a compilation and interpretation of the third-party brokerage research report (Morgan Stanley, July 13, 2026) by Trends Research. The ratings, target prices, earnings forecasts, and related judgments quoted in this article are the opinions of the brokerage analysts and only represent the positions of their affiliated institutions, not the views of Trends Research, and do not constitute any investment advice.

The market has risks, decisions should be independent. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。