Written by: Rita

Trends Guide

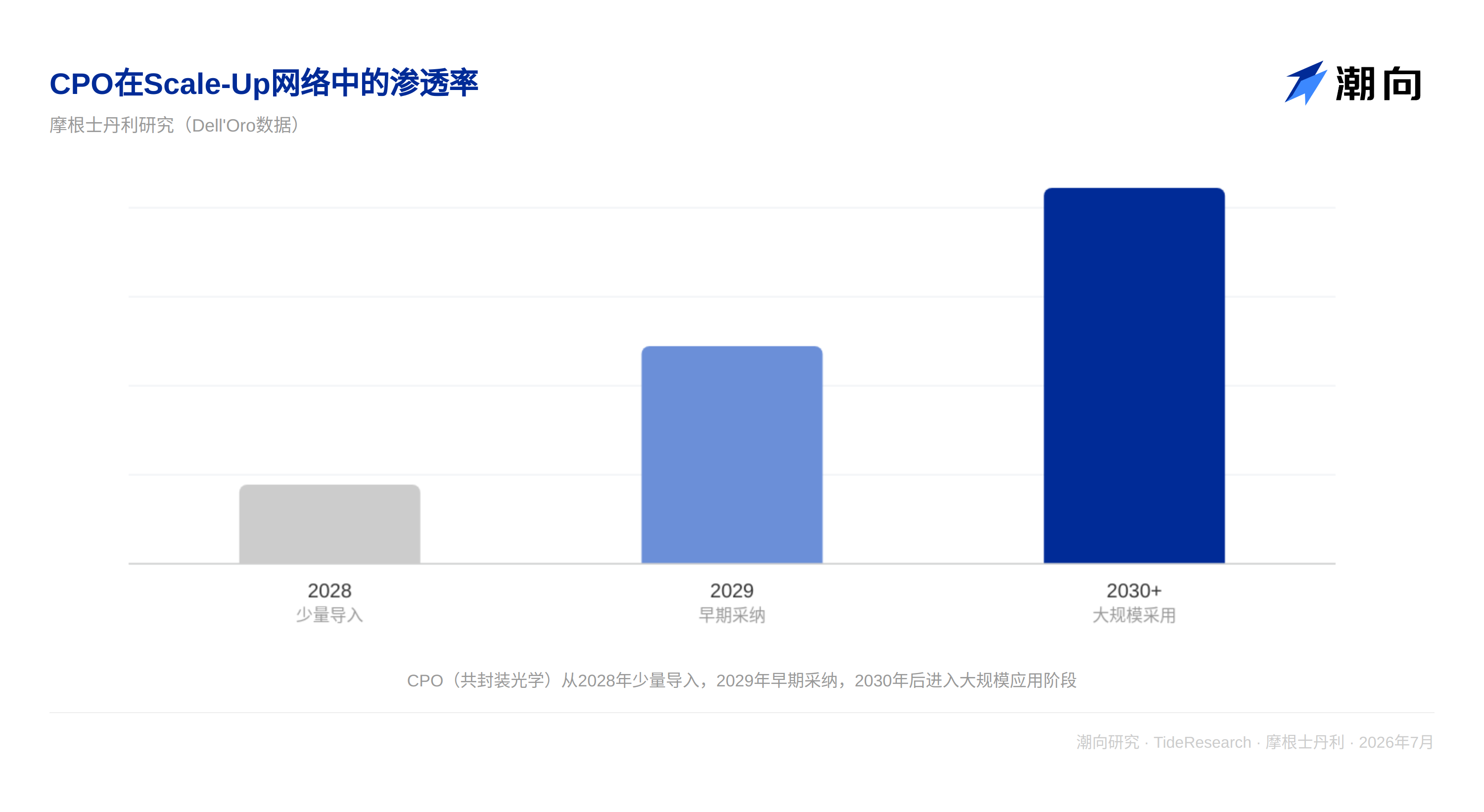

Optical communication stocks have recently fallen, with the market concerned that the introduction of CPO (Co-Packaged Optics) in Scale-Up networks will be "delayed." Morgan Stanley's latest report provides a counter-consensus judgment: there will be only a small introduction in 2028, and true large-scale adoption of CPO will have to wait until 2029 and beyond. The market has projected the timeline too quickly; this is not a delay. Before that, copper cables still have a two-year window. What drives this timeline is not technical bottlenecks, but the expansion of AI cluster scale, starting with 72 GPUs for NVIDIA Blackwell and reaching 1152 for Feynman, as communication demand continues to rise, but copper cables can still hold on for a while thanks to innovations such as PAM4, DSP, and retimers. This is the key coordinates for understanding infrastructure investment in AI over the next two years.

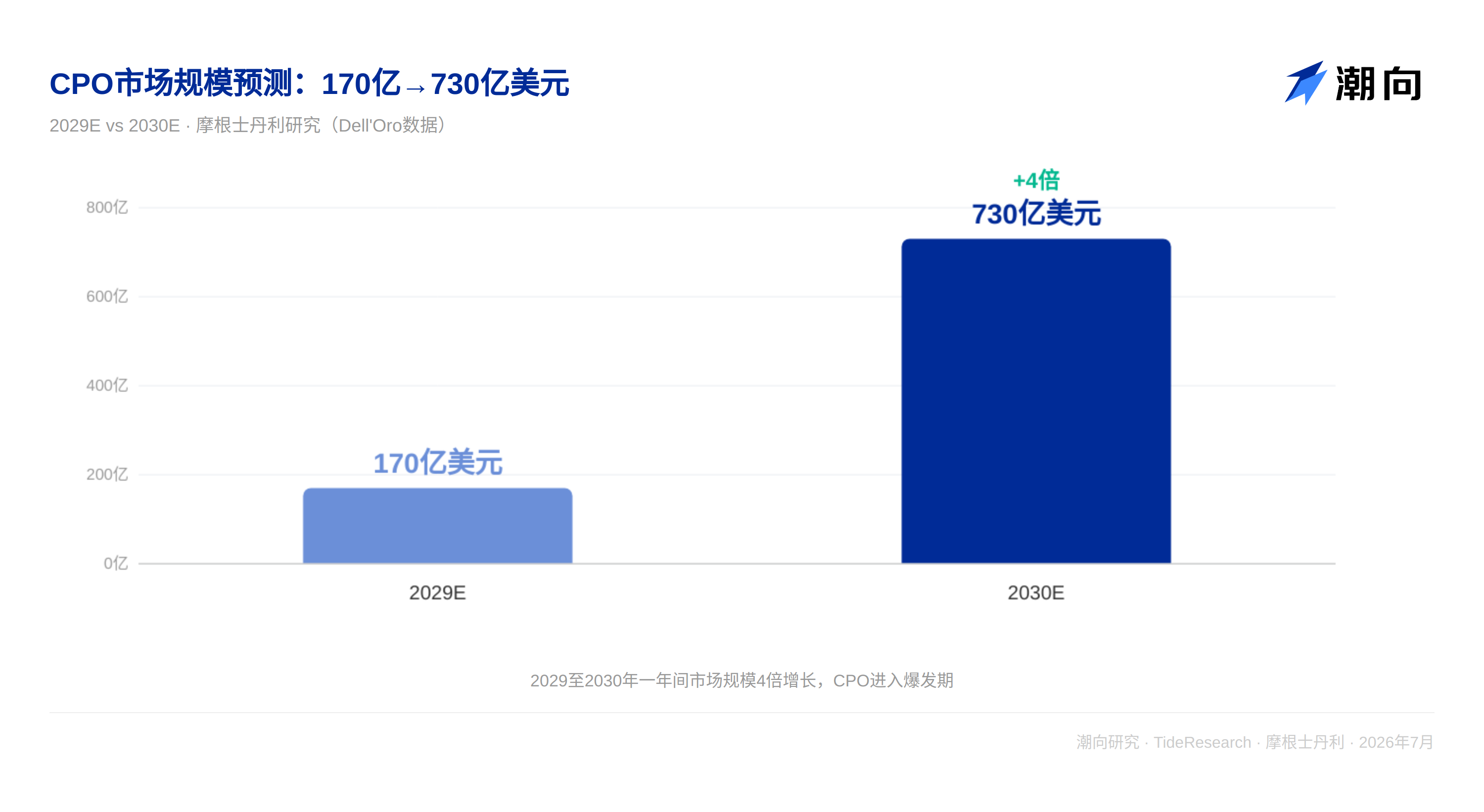

Market quadruples in a year, but CPO cannot hurry

When Morgan Stanley first proposed the Scale-Up network opportunity last year, the market size for 2029 was estimated at $17 billion. A year later, this figure has been raised to $73 billion by 2030, more than quadrupling. However, the penetration curve of CPO has not risen along with the slope of the market size. Morgan Stanley predicts that in 2028 there will be only a small introduction of CPO in Scale-Up networks, with the real inflection point in 2029 and beyond. The core reason is that CPO involves the reconstruction of the supply chain for packaging, optical engines, and lasers, rather than just upgrading individual components; it is a migration of the entire ecosystem. NVIDIA's Feynman generation is the time anchor for large-scale deployment of CPO.

Copper cable’s "expiration" is repeatedly postponed

Copper cables have always been the preferred choice in data centers: low cost, reliable, and low power consumption. Its "expiration" has been declared multiple times, but each time new technology revives it; PAM4 modulation allows more bits to run over copper cables, more powerful DSP keeps signals intact over longer distances, and retimers pull signals back before attenuation makes them unreadable. Morgan Stanley believes that copper cables will stay longer in Scale-Up than the market expects. The real competitor for copper cables is not CPO, but the physical scale of AI clusters themselves. As clusters expand from 144 to 576, then to 1152, the communication distance between racks is lengthening, and the signal rate is jumping from 100G to 200G, 400G; the physical limit of copper cables will ultimately be reached.

Non-NVIDIA ecosystem is forming, with copper and optics each taking a share

2026 is the starting point of the non-NVIDIA Scale-Up market. AMD MI400, AWS Trainium 3, and Microsoft Maia are beginning mass production, creating incremental opportunities for third-party network vendors. On the copper side, Astera Labs' Scorpio-X has already shipped in Trainium 3, accelerating volume in the second half of 2026. On the optical communication side, the CPO/NPO product lines of LITE, COHR, and GLW are positioned for the window after 2028. Morgan Stanley believes that the October OCP conference will be the real catalyst for CPO sentiment, and Q2 earnings season may not be the right time yet. Morgan Stanley has an overweight rating on NVIDIA, Broadcom, Astera Labs, and Keysight.

Trends Perspective

The real judgment is that the discussion of CPO has been overly compressed by the market. Investors are accustomed to tracking technological penetration on a quarterly basis, but the migration of CPO is calculated on a generational scale. NVIDIA has crossed four generations of architecture from Blackwell to Feynman, and CPO happens on this time scale. The window period for copper cables is inherently this long; it is just that the market is used to describing it as a "delay." The breakout point for optical communication companies (LITE, COHR, GLW) is not in 2027, but after 2029. And before that, testing equipment vendors like Keysight are beneficiaries from another dimension; whether copper wins or optics win, testing is a prerequisite, and the diversity of architectures itself is its growth engine.

Disclaimer

This article is a summary and interpretation of a third-party brokerage research report (Morgan Stanley, July 13, 2026) by Trends Guide. The ratings, target prices, profit forecasts, and related judgments quoted in this article are the views of that brokerage's analysts and represent the stance of their institution, not the views of Trends Guide, nor do they constitute any investment advice.

The market carries risks, and decisions should be independent. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。