Author: Huang Fan, Qinsuo's Moments

Teacher Qin wrote "The Great Bubble || A Broad Perspective", and we continue to explore this topic. The domestic and foreign capital markets in the past two years are clearly in the midst of a great AI era. Domestic investors enthusiastically participate, shouting slogans like "Stand in the light, remember in the core" and "All-in AI", fearing they might miss out on this "historical opportunity" under such a grand narrative.

In such fervor, any doubt in the investment community can easily lead to being labeled as "old Deng"—this term has become a derisive nickname in the capital market for those investors who are not fully invested in AI, with people believing that the "old Dengs" will inevitably miss the era's dividends due to their conservative rigidity.

Meanwhile, the global AI market is also heating up: the Philadelphia Semiconductor Index, which represents the health of the chip industry, has nearly tripled in the past year; in the domestic market, the GEM and Sci-Tech Innovation Board indices, representing "light" (optical modules) and "core" (GPU, storage chips), have also risen sharply, with the Sci-Tech Innovation Board index increasing by over 50% in the first half of this year, and its valuation reaching an astounding 240 times (data from Dongfang Caifu at the end of June 2026).

Most investors are busy in the market, chasing up and selling down, as if stock codes are the wealth code of this era, capable of making one rich overnight. However, as an "ancient ancient deity" having crawled through the financial circle for thirty years, I firmly believe: the essence of investment has never been a contest of who understands the code better, but rather a contest of who can penetrate the fog of technology and see the cycles of capital clearly.

I entirely agree that AI technology will exponentially enhance human productivity. But remember: the greatness of technological revolutions does not equate to the inevitability of investment profits. In the face of this global AI tide, let's take a moment to calmly clear the bubbles and return to common sense for deep thinking.

The AI Gold Rush and the Profit Traps of "Selling Shovels"

If we view the current AI wave as a gold rush, we must admit that the ones truly making big money are those providing AI infrastructure hardware, akin to the vendors "selling shovels" to gold miners.

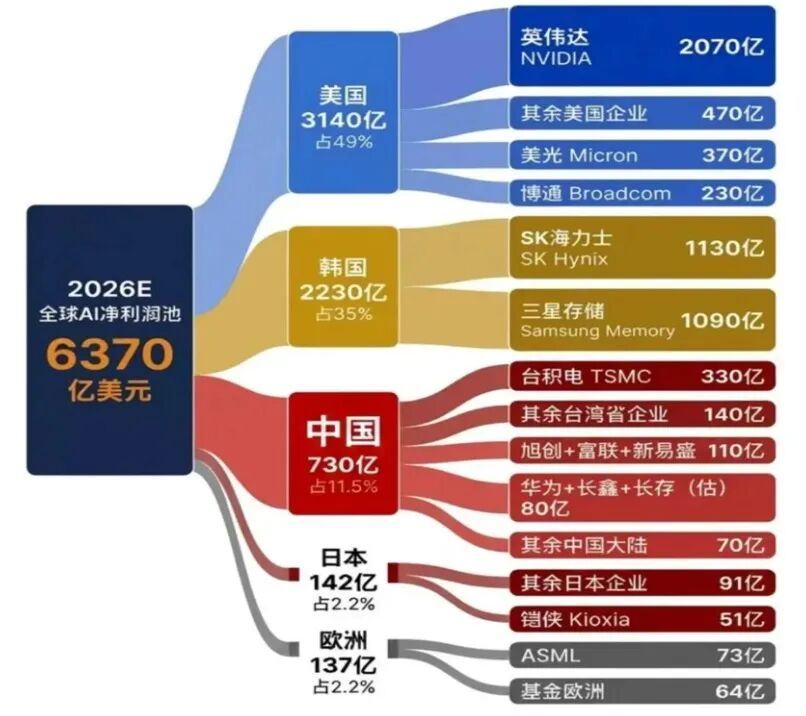

First, we can observe the predicted performance of the global AI enterprise profit pool in 2026:

| Image source: Network AI generated

Data on the global AI enterprise profit landscape in 2026 indicates that the profits of AI enterprises in the United States and South Korea are expected to account for 84% of the global total.

Among them, NVIDIA alone accounts for nearly one-third, while many supply chain companies, such as TSMC, Zhongji Xuchuang, and Newray, are also making a fortune thanks to NVIDIA's ecosystem.

This set of data reveals a harsh fact: although the AI boom sweeps globally, the distribution of dividends is extremely polarized.

If we look at AI as a gold rush, those currently making money are mostly the companies selling shovels; however, the large firms responsible for building big platforms and implementing C-end applications have yet to earn anything substantial, and many haven't even started making profits.

What does this indicate? It shows that the application scenarios for AI are currently still in the "concept stage," while computing infrastructure (GPU, storage, communication) has entered the "realization phase."

Currently, the domestic and foreign markets demonstrate an extreme "hardware worship". The surge in overseas Philadelphia Semiconductor Index and the domestic Sci-Tech Innovation Board essentially reflects early pricing for the "ultra-long bullish cycle" of AI infrastructure. However, we must be wary: when hardware supply heavily relies on a few oligarchs and the downstream applications have not yet established a business closure, this growth model is likely unsustainable.

Presently, major AI platforms and application giants in the U.S. (such as Amazon, Microsoft, Google, Meta, Oracle, etc.) have astonishing capital expenditures, with mainstream market estimates totaling around $800 billion. These application giants are pouring money madly to ensure they don’t fall behind in computing power, while the rise in storage chip prices continuously drives this budget higher.

However, will these giants' huge capital expenditures be able to smoothly recoup their costs in the future? Currently, there is enormous uncertainty. If for one or two years they continuously invest without reliable revenue sources, cash flow will eventually run dry, leading to a significant drop in the valuation levels of these giants. When that time comes, can they continue to increase capital expenditures? This situation resembles gold miners during the gold rush—if they keep finding no gold, will they continue to spend a fortune on so-called "hard technology" shovels? The answer is obvious.

In the Frenzy of Carbon-Based Life Forms, Investors Must Stay Calm

Currently, the capital expenditure growth of tech giants is stunning. But as investors, we need to question a core issue: is this capital expenditure truly sustainable? If we ignore valuations and thoughtlessly follow the hard tech companies, aren't we just participating in a high-stakes gamble?

In the past history of technology, we've seen too many hard tech companies that were once thriving but ultimately fell: from Nortel, which monopolized internet fiber optics, and network equipment giant Cisco, to the former mobile carriers Motorola, Nokia, and BlackBerry…

In the torrent of continuous technological iterations, the truly cyclical enterprises can be counted on one hand. Currently, the AI giants, as the biggest financiers of hardware companies, are facing a classic dilemma: they hope to maintain future growth potential through continually increasing capital expenditures; but if future computing demand cannot be converted into sustainable payments from C-end users or stable cash flow from B-end enterprise applications, this growth logic will completely break down.

We need to closely monitor the following key risk points: is there excess infrastructure? If the pace of computing capacity expansion far exceeds the landing speed of applications, will there be massive asset impairment in 2027? Can profit models close the loop? All technological innovations ultimately must culminate in free cash flow.

Currently, the heavy asset AI model significantly differs from the light asset internet model of the past; once cash flow dries up, the valuation logic will face collapse. However, at this time, the dominant voice in the capital markets is often: "We all know there is a bubble and risk in the AI hardware track, but the risk of missing a historical opportunity is greater!"

To this, I unequivocally hold a different opinion. If we only see AI as a wave of tech stock trends, it indeed appears "unmissable". However, if we observe it within a longer historical cycle, it, like every general technological revolution, advances in waves—

First comes the frantic race for infrastructure, then the reconstruction of platforms, and finally the popularization of applications and rewriting of social organizational methods.

This is not merely a cycle of ordinary industry prosperity, but a technological long wave that deeply reorganizes the production function. Long wave technological revolutions never imply that stock prices will soar in a straight line. The internet boom and bust cycle around the year 2000 is the best mirror.

Looking back at history, the Nasdaq Index skyrocketed 86% in 1999, peaked at 5048 points on March 10, 2000, and then plummeted to 1139.90 points by October 4, 2002, a drop of 77%. The index only returned to a new historical high in April 2015.

In other words, the internet indeed created historical investment opportunities for us, but participants who entered at the end of 1999 and the beginning of 2000 clearly made a mistake—they misjudged the price they paid in current terms as excessively high against future anticipated income. This is precisely where today's AI investments warrant caution.

Indeed, AI will change the world in the future, but we must question at this stage: can an expansion model dependent on massive capital expenditure be sustained? This bears a resemblance to the expansion cycle logic seen in real estate, new energy, and even commodities—once demand erupts, supply quickly expands; but once industry thresholds aren’t sufficient to keep capital out, it swiftly transitions from "shortage" to "oversupply".

Therefore, even the strongest AI hard technology cannot soar without repeated verification and significant volatility. Let's focus on reviewing the rise and fall of three typical giants in the last round of the internet wave to serve as a reference:

1. Nortel: The "King of Selling Shovels" in the Bubble. At that time, it was the global leader in communication equipment, with its core product around the turn of the century being the most advanced fiber optics—which was an essential "shovel" for the internet age, comparable in status to today's NVIDIA. At the peak of the tech bubble in 1999, Nortel's market value once reached $250 billion, with nearly 10,000 global employees.

However, as later the capital expenditures of downstream giants failed to sustain, Nortel's most advanced fiber optics went unsold. After accounting scandals and a series of strategic missteps, the company ultimately filed for bankruptcy in 2009, leaving stock investors with nothing.

Nortel is a typical case of "mistaking temporary prosperity for perpetual growth and treating financing ability as core competitiveness," ultimately being backfired by both cyclical flaws and governance issues as a champion of infrastructure.

2. Cisco: The "Long Runner" that Overdraws the Future. Cisco's business is more diversified, providing both communication connection devices and ground solutions such as routers. In the fiscal year 2000, Cisco had secured solid profitability of several billion dollars, yet even that could not support its staggering market value of $400 billion at the time.

After the bubble burst, Cisco’s market value dropped to around $100 billion, and even two decades later, it has not regained its former glory. This shows that even with consistently good operations and real profits, an excessively high valuation can prematurely draw on decades of future potential. Investors who purchased at high prices during that time still suffered long-term losses.

3. Microsoft: The "Platform King" that Transcends Cycles. Microsoft is a success story that survived the last round of industrial revolution and maintains its leading position to this day. Its cyclical success pathway is worth pondering: although deeply embroiled in anti-trust lawsuits in 2000, Microsoft had an incredibly broad product matrix and invested a large $3.78 billion in R&D that year (around 16.4% of revenue).

During the more than a decade post-bubble burst, Microsoft underwent two critical self-reinventions—the first towards cloud platforming, and the second towards AI platforming. As early as 2016, Microsoft defined "Intelligent Cloud" as a core pillar; by fiscal year 2025, Azure revenue exceeded $75 billion for the first time, with total cloud-related income reaching $168.9 billion.

Microsoft's success demonstrates that what's genuinely scarce is not a particular generation of hardware advantages but rather the capacity to reorganize each technological revolution into a platform ecosystem.

However, it's worth noting that even a transcendent giant like Microsoft saw its market value drop 75% from $600 billion at the peak in 2000 to less than $150 billion by the 2009 low, and it took until 2016 to reach that $600 billion starting point again.

If we dissect today's AI industry, the structure is also very clear: industry levels represent current statuses and risk characteristics.

- First level: Infrastructure chips, computing power, storage, data centers, and so on are currently the most sought after, and companies in this area are among the first to make real money; however, they are also at risk of being overvalued, and due to the fast pace of technological iterations, once they fall behind, they are easily eliminated.

- Second level: The platform layer, including cloud computing, operating systems, development frameworks, and data entry points, is dominated by giants with strong capital strengths, which are the most central positions but currently are most easily underestimated. The real long-term winners are often the companies that can leverage technology to establish sustainable platform ecosystems repeatedly.

- Third level: Application end, including robotics, autonomous driving, AI terminals, and vertical large models, is filled with the most imagination and where investors tend to flock; however, the survival environment is the harshest. For example, a representative company of a large model expects only over $700 million in revenue in 2025 and is still in a stage of heavy loss. Yet its highest market value during the Hong Kong stock listing was inflated to trillions. Companies like this have unclear business models, the slowest revenue realization, and the most alternate paths, leading to a very low survival rate. Most of those quickly eliminated in the last internet wave belong to this level.

Therefore, understanding AI should not only consider "how strong the hard technology is" but also which value capture stage it currently occupies. Even the companies currently strongest in technology and most profitable in the infrastructure boom do not equate to their capability to weather cycles and bring long-term good returns to investors.

How to Survive the Burst of Bubbles and Cycle Changes

Like past industrial revolutions, the current round of AI industrial revolution is giving rise to enormous capital bubbles.

Typically, bubbles go through three stages:

1. The current infrastructure bubble;

2. The next stage platform reevaluation bubble;

3. The far-off application explosion bubble.

Although each round of bubbles will eventually burst, the upward spiral trend of AI industrial capabilities will not change. At present, the bubble mainly revolves around "hard technology" related to infrastructure.

So the core question is: when will the massive capital expenditures of AI giants translate into real cash flow? What happens if revenues do not keep up with expenditures?

History has long provided the answer: either valuation falls, or cycles clear out. Therefore, I believe that rather than actively pursuing the apparent current infrastructure bubble, it would be wiser to calmly wait for the bubble to burst and then selectively choose those "survivors".

For instance, operating system platforms from the PC era, social and e-commerce platforms from the mobile internet era, and the large models, cloud computing, as well as toolchain platforms of the AI era. Only those giants equipped with comprehensive infrastructure, platform, and application capabilities possess a high probability of long-term survival amid the sandstorm.

Even as we enter the great AI era, I believe the "Old Deng-style" investment strategy—"select, wait, guard"—remains valid:

1. "Select": Choose good companies in good tracks. We must learn to distinguish between "technological leadership" and "business moats." In the AI era, technological iterations occur rapidly, and single products or models are easily replaced. We should focus on companies with deep accumulations in the integration of hardware and software, data barriers, and business ecosystems, rather than merely chasing those companies that pile on computing power through cash burning.

2. "Wait": Calmly await reasonable prices for core assets. We don’t need to feel anxious about lagging behind the times just because we aren't "standing in the light, remembering in the core" at this moment, nor do we need to pay exorbitant premiums to force our way onto certain AI tracks.

Investing is a marathon; AI hard tech is the current star, but it is certainly not the only script. Returning to common sense and focusing on cash flow is crucial. In the midst of a major wave, new tracks and high-growth companies will continue to emerge, and as long as we have cash when opportunities arise, we will never lack opportunities.

3. "Guard": Hold tight to a core asset portfolio aligned with the AI wave. The iteration and being iterated of tech companies are historical norms. If we believe in AI's future, rather than blindly betting on one or a few seemingly dazzling tech companies, it's better to engage in phased investments through a broad base index (like the Nasdaq market representing the core tracks and core companies of global hard tech) and hold for the long term.

To put the current survival rules more bluntly, my advice is:

The most worthwhile choices now are definitely not the companies that tell the best stories; and the ones most worth holding onto are certainly not the targets currently soaring the highest.

What we should genuinely seek and continuously follow are not the short-term "shining stars" that are pumped up into bubbles, but those that can stand at the industry's center in the next industrial expansion, even after the bubble bursts and cycles cleanse—those "future blue chips." Because only they are not simply reaping the short-lived thematic dividends but genuinely harvesting the long-term national fortune of the entire AI era.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。