Every Monday, Wednesday, and Friday, focusing on the cryptocurrency market, Japan, South Korea, A-shares, and Hong Kong stocks, reviewing the market with data, seizing opportunities with trends, produced by PANews.

Bitcoin fluctuates down amid war noise, bulls are still waiting for the "60,000 script"

On Monday during the Asian session, Bitcoin briefly fell below $63,000, reaching a low of $62,500. Over the past month, Bitcoin price has consistently maintained a wide range of fluctuations between $59,000 and $66,000. Despite rising oil prices and a decline in global stock markets due to tensions in the Middle East, it has still not broken this range.

Market analysis indicates that about 30% of the pressure on Bitcoin currently comes from the shift of funds into AI and chip sectors. Analysts believe that the price drop on Monday felt more like a leveraged liquidation during the Asian session, with the scale of liquidation being only one-sixth of the most extreme moments in the past 30 days, and the market has not yet experienced panic selling.

From a funding perspective, positive factors are gradually accumulating. The U.S. Bitcoin spot ETF has ended eight consecutive weeks of net outflows, recording a net inflow of $197 million last week; Galaxy Digital's research director Alex Thorn pointed out that all four core indicators related to long-term holders have reached historical highs, including 16.75 million coins in supply held by long-term holders, $836.4 billion in realized market value of long-term holders, and 17.7% of chips held for over 10 years, indicating an increasing degree of chip locking.

On the technical side, the market consensus on the “$66,000 magnetic effect” is warming up. Traders Astronomer, CrypNuevo, Ted Pillows, and others consider $66,000 a critical target level. CrypNuevo pointed out a significant liquidation cluster in the $64,700-$65,100 area, while the largest liquidity target for upward movement is around $66,400; Ted Pillows observed that there is a high concentration of sell orders above $65,000-$66,000, but a large amount of whale buying around $61,000, suggesting that the market is forming a typical “suppressing the rise, accumulating at low levels” structure.

Ardi defines $64,800 as the neck line of the arc bottom pattern over the past month. He believes that the price's long-term proximity to the resistance level without effective suppression from bears indicates that the selling pressure is continuously being consumed. If it effectively breaks above $64,800 and holds, the market is expected to release long-accumulated upward momentum; conversely, if it falls below $62,500, a reassessment of the bottom structure will be necessary.

Notably, the weekly trading volume of South Korea's five major exchanges has fallen to 9.97 trillion won, the lowest since September 2023, shrinking more than 43% compared to early June. Retail trading enthusiasm continues to wane, but Ardi's monitoring data shows that whale accounts have shifted from net short to net long in the past week, while the proportion of retail long positions has decreased from over 70% to 56%, indicating a transfer of chips to large funds.

The short-term market focus will shift to the U.S. June inflation data and the Federal Reserve's interest rate meeting at the end of the month. If inflation continues to cool, it will strengthen market expectations for improved liquidity, and the $66,000 or even $70,000 area may become the next testing target; if oil prices continue to rise due to the Middle East situation and push up inflation expectations, it may put further pressure on risk assets.

Today's Highlights:

Upbit 24-hour trading volume ranking: BTC, XRP, BLAST, T, ETH

Bitcoin spot ETF: ended eight consecutive weeks of net outflows, net inflow of $197 million last week

Ethereum spot ETF: ended eight consecutive weeks of net outflows, net inflow of $84.42 million last week

HYPE spot ETF net inflow of $10.3567 million last week

SOL spot ETF net inflow of $930,400 last week

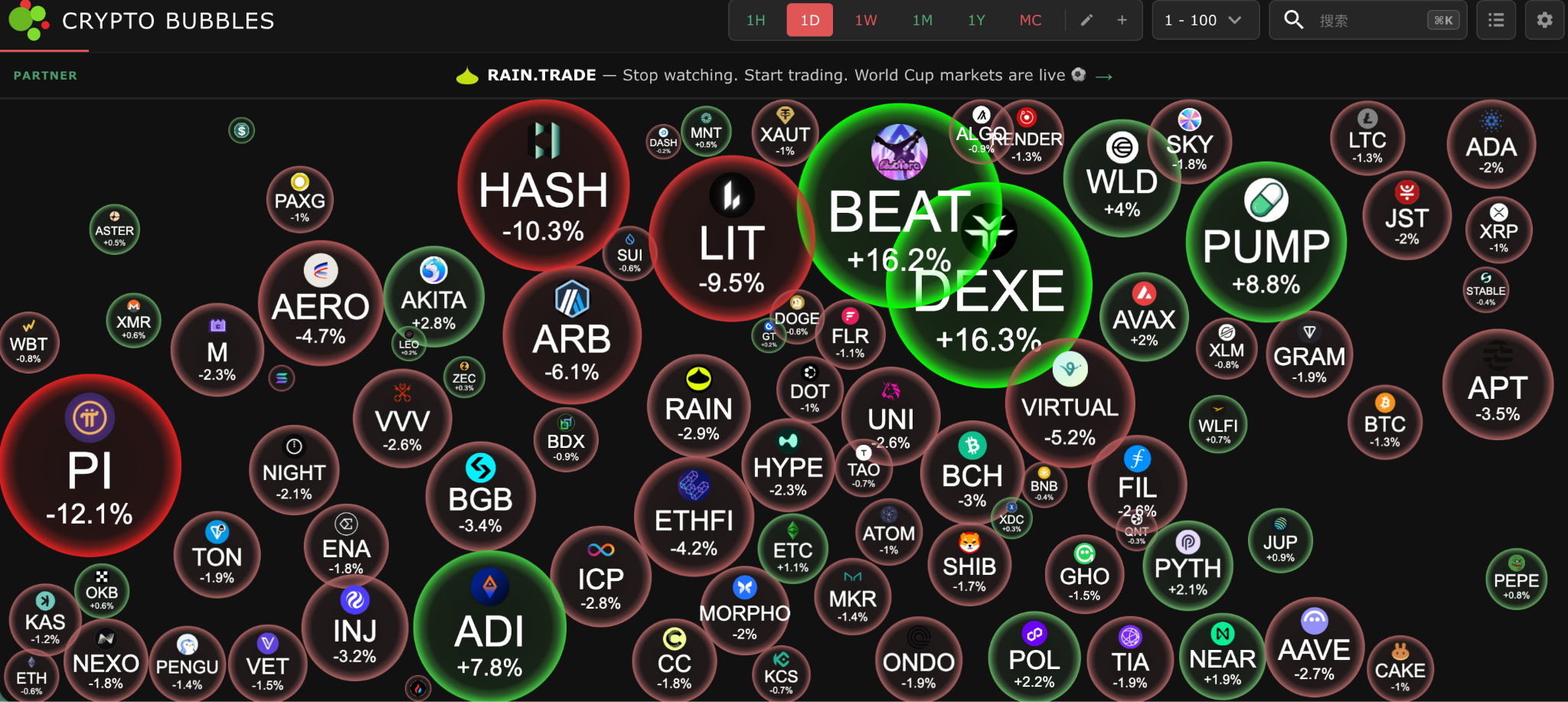

Today’s top gainers among the top 100 cryptocurrencies by market capitalization: DEXE up 16.3%, BEAT up 16.2%, PUMP up 8.8%, ADI up 7.8%, WLD up 3.9%.

SK Hynix's "good news realization" triggers a sell-off, KOSPI experiences a circuit breaker

The largest black swan in the Asian market comes from South Korea, KOSPI index closed down 8.96%, marking the lowest closing level since April 30.

The trigger for this round of sharp decline comes from SK Hynix. Just as its ADR landed on Nasdaq last Friday, soaring nearly 13%, completing the largest IPO by a foreign company in U.S. history, the Seoul market staged a typical "sell the fact" rally.

SK Hynix closed down 15.37%, marking the largest single-day drop in history; Samsung Electronics also fell 10.7%.

Chan H Lee, managing partner of Petra Capital Management, believes that the success of the ADR listing has been priced in by the market, and more reflects profit-taking rather than a deterioration in fundamentals. Analyst Ryu Young-ho from NH Investment & Securities pointed out that the market's expectations for HBM4's shipment growth rate may be overly optimistic, causing investors to begin worrying about the realization of second-quarter earnings.

Meanwhile, market concerns over the high valuation of the AI industry chain continue to ferment. SK Hynix has cumulatively risen more than 25 times since the end of 2022, while its stock price has retreated over 30% from its June peak.

However, the South Korean central bank refutes the "chip cycle peaking theory" in its latest report. The South Korean central bank pointed out that investment in AI infrastructure continues to expand rapidly, and the supply of custom products such as high bandwidth memory (HBM) remains constrained, with the global semiconductor market still in a state of supply not meeting demand. The South Korean central bank also cited opinions from JPMorgan, Goldman Sachs, and Morgan Stanley that the global semiconductor super cycle is expected to continue at least until 2027.

Nikkei falls below 68,000 points, chip stocks become the center of the sell-off

The Japanese stock market was unable to escape the impact of the collective correction of Asian risk assets on Monday.

The Nikkei 225 index fell by 1315 points, a drop of 1.92%, briefly falling below the 68,000-point mark. Rising energy prices, escalating tensions in the Middle East, and concerns about the Bank of Japan's continued push for monetary normalization jointly undermine risk appetite.

As tensions in the Strait of Hormuz re-emerge, the market begins to reprice import-driven inflation risks. Investors worry that rising crude oil prices will increase costs for Japanese companies, while weakening the Bank of Japan's future policy space.

The chip and electronic components sector has become the core of the sell-off. Kioxia plunged over 12.8% in a single day, becoming one of the biggest drags on the Nikkei index. In the foreign exchange market, Reuters reported that the Japanese government's pension investment fund GPIF has no plans to adjust its asset allocation, pushing the dollar above 162 yen. Some institutions believe that if the yen continues to weaken, the Bank of Japan may tend toward hawkish policy statements in the future. Observers of the Bank of Japan generally believe that if energy prices continue to rise, inflationary pressures in Japan will re-emerge, potentially strengthening the market's bets on further interest rate hikes within the year.

The semiconductor sell-off drags down the index, Southern Double Long Hynix plunges 31.59%

A-shares experienced a significant pullback on Monday, the Shanghai Composite Index fell 2.06%, the Shenzhen Component Index fell 3.48%, the ChiNext Index fell 3.10%, and the Sci-tech Innovation 50 Index fell 3.42%, losing the 2000-point threshold. The spillover from the Korean semiconductor crash, rising geopolitical risks in the Middle East, and the excessively large previous gains in AI hard tech have triggered capital concentration for profit-taking.

Semiconductors have become the key factor in the declines, with Zhiyuan Innovation touching its daily limit, with transaction volume surpassing 31 billion yuan; Jinghe Integration fell 7.18%, Langqi Technology fell 5.7%, and Tianxun Wisdom Core fell 3.32%. The market worries that the collapse of the South Korean storage sector will trigger a re-evaluation of the global semiconductor industry's valuation.

Meanwhile, data released by the National Medical Products Administration shows that 38 Class I innovative drugs were approved for listing in China in the first half of the year, with the total amount of innovative drug authorizations reaching $110 billion, both setting historical highs, causing funds to focus on the direction of pharmaceutical innovation.

Goldman's latest research report maintains an overweight view on A-shares. Goldman believes there is no systemic bubble in the overall AI sector of A-shares, but valuations in some semiconductor sub-sectors are already high, needing to beware of crowded trading risks.

The Hong Kong Technology Index also faced pressure, with the Hang Seng Technology Index down 1.07%, while the Hang Seng Index rose slightly by 0.05%. The largest pressure in the market still comes from the AI hardware chain:

The storage sector collectively plunged, Southern Double Long Hynix plummeted 31.59%, and Southern Double Long Samsung Electronics fell 19.05%.

The PCB sector continues to drop sharply, with Jintao Group down 16.73%, Jintao Laminated-Film Board down nearly 20%, and Dazhu CNC down 12.19%.

The optical communication sector continues to retreat, with Yangtze Optical Fiber and Cable falling 14.89% and Xizhi Technology down 9.24%.

The semiconductor sector is under pressure, with Hong Kong-listed Zhiyuan Innovation down nearly 11%, Huahong Semiconductor down 6.09%, and SMIC down 0.25%.

Goldman believes that the Hong Kong internet sector has basically digested the profit pressure brought by AI investments. As cloud business and AI application monetization accelerate, the profit inflection point is expected to gradually appear in the second and third quarters.

In terms of individual stocks, MINIMAX dropped 19%, hitting a historical low. Pop Mart rose nearly 2% due to Duan Yongping's additional holdings, increasing his shareholding ratio to 7.65%; China Hongqiao rose over 3% after a positive earnings forecast; Walvichi Bio-B surged 24%, stimulated by favorable news of priority review for innovative drugs.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。