Every Monday, Wednesday, and Friday, focusing on the cryptocurrency market, Japan, South Korea, A-shares, and Hong Kong stocks, reviewing the market with data and seizing opportunities through trends, produced by PANews.

Cryptocurrency market enters a period of directional selection, Bitcoin impacts the $65,000 mark

Bitcoin continues its rebound rhythm, at one point approaching $64,000 during trading, gradually recovering losses caused by the escalation of Middle Eastern situations and risk-averse sentiment. Institutions such as CryptoQuant and Swissblock believe that there is a clear recovery in derivatives demand, but spot ETF funds remain weak, and institutional capital has not fully flowed back.

Multiple traders pointed out that Bitcoin's current support level is around $61,000, while the resistance level is at $66,000. Notable analyst Ted mentioned that a large amount of short liquidity is gathering between $64,500 and $66,000, and if it can successfully reclaim $65,000, it may further challenge $72,000 to $74,000 in the next 3 to 4 weeks; conversely, a large number of long stop losses are positioned between $59,500 and $61,500. Ardi believes that $64,800 is the core resistance that will determine whether the next round of upward momentum can start, while $61,300 is the short-term lifeline, and once it falls below that, it will reopen downside space.

Daan Crypto Trades stated that Bitcoin still stands firmly near the weekly 200-week moving average (approximately $62,800), and the high timeframe support remains effective; as long as the weekly price does not effectively fall below $55,000, the medium to long-term trend is not damaged.

Today's Highlights:

Adam Back's BSTR merger vote with Cantor SPAC is postponed again to July 10

Linea (LINEA) will unlock approximately 1.08 billion tokens on July 10, worth about $2.7 million

io.net (IO) will unlock approximately 13.29 million tokens on July 11, worth about $2.3 million

Upbit 24-hour trading volume ranking: BTC, XRP, SLX, ETH, OPG

Bitcoin spot ETF: -$95.3017 million

Ethereum spot ETF: -$52.0804 million, ending five consecutive days of net inflow

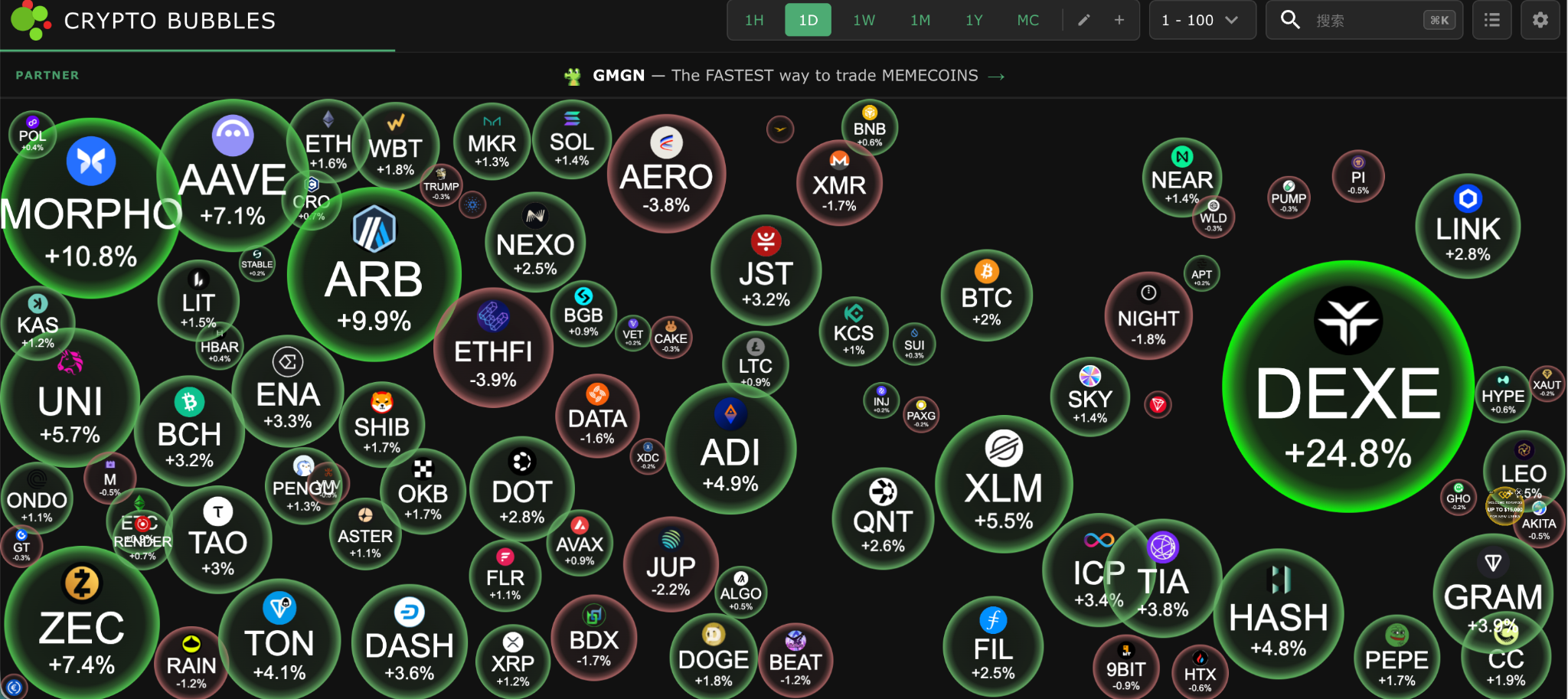

Today's top 100 cryptocurrencies with the largest increase: DEXE up 24.8%, MORPH up 10.8%, ARB up 9.9%, ZEC up 7.4%, AAVE up 7.1%.

Pension reform expectations boost yen and Japanese bonds rebound

The Japanese stock market continues to restore risk appetite, with the Nikkei 225 index closing up 1.20%. Market sentiment is clearly buoyed by the overnight rebound in U.S. chip stocks and the collective strengthening of the Asian AI industry chain. At the same time, Japan's Finance Minister Shunichi Suzuki openly stated the hope to encourage the government pension investment fund (GPIF) and other pensions to increase allocations to Japanese domestic financial assets, leading to a rapid appreciation of the yen, a decline in Japanese government bond yields, and a rare synchronous rise in stocks, bonds, and currencies.

After the announcement, the dollar against the yen once fell to around 161.28, and the yields on Japan's 10-year and 20-year government bonds both fell by about 10 basis points during the day. The market began to re-trade expectations of further interest rate hikes by the Bank of Japan, with the June PPI growing year-on-year by 7.1%, marking the fastest growth rate in over three years, further strengthening market expectations for the normalization of Japanese monetary policy.

However, multiple institutions remind the market to remain cautious. David Forrester, senior strategist at Credit Agricole, believes that merely relying on policy statements cannot reverse the yen's long-term weakness, and true support for the exchange rate still requires further interest rate hikes from the Bank of Japan, fiscal reform, and genuine asset adjustments from GPIF. Bart Wakabayashi, head of State Street Tokyo, also believes that the current situation is more emotionally driven, and there remains significant uncertainty regarding policy implementation.

On the individual stock front, the robotics industry has become a new focal point. Bernstein stated that Japanese automotive companies are accelerating their layout for humanoid robots, with Mitsubishi Motors announcing a joint effort with a startup to advance humanoid robot mass production. Institutions forecast that by 2050, the global humanoid robot market size is expected to reach $729 billion, and automotive manufacturers, leveraging their expertise in actuators, batteries, sensors, and AI control systems, will become significant beneficiaries.

Next week, the Japanese market will continue to focus on the yen's movements, expectations of interest rate hikes from the Bank of Japan, and whether GPIF will further disclose asset adjustment details. The market generally believes that if inflation in Japan continues to rise, expectations for the normalization of the Bank of Japan's policies will continue to heat up.

KOSPI in South Korea continues to rise, SK Hynix slightly drops by 0.27% at the close

The South Korean stock market continues to lead Asia, with the KOSPI index closing up 2.52%, rising more than 5% at one point, triggering a temporary suspension mechanism for KOSPI 200 futures. The AI industry chain continues to attract global capital inflows, with the rebound of U.S. chip stocks and SK Hynix's historically significant ADR financing collectively driving the South Korean technology sector's continuous strength.

SK Hynix is about to list on NASDAQ, expecting to raise about $26.5 billion through ADR, becoming one of the largest historical ADR issuances globally. Douglas Research Advisory analysts estimate that the premium rate of SK Hynix ADR compared to South Korean local stocks may reach as high as 17% in the short term, and overseas capital allocation demand is expected to further enhance the company's valuation.

However, SK Hynix slightly dropped by 0.27% at the close, as the market saw more profit-taking, while Samsung Electronics rose by 2.5%, continuing to benefit from AI PC chip news. South Korean media reported that Samsung is developing an AI PC-specific chip code-named GAIA and has provided samples for testing to Lenovo and HP, with mass production expected as early as next year, further strengthening its layout in AI terminals.

The leverage funds in the South Korean market are also rapidly heating up. With SK Hynix ADR's listing, the U.S. market is expected to launch at least 6 double-leveraged ETFs next week. John Cho, a fund manager for South Korean equities at JPMorgan Asset Management, stated that the rapid expansion of single-stock leveraged ETFs is not a healthy sign, as retail momentum trading is significantly amplifying market volatility.

Christopher Wood, global head of equity strategy at Jefferies, believes that the recent fluctuations in the South Korean stock market belong to a "healthy adjustment," and the AI capital expenditure cycle has not yet ended; what will truly determine the market direction in the future will be the upcoming capital expenditure and performance data announcements from global cloud computing giants.

Next week, the market will focus on the funding performance after the formal listing of SK Hynix ADR, and whether U.S. tech stocks and the AI industry chain can continue to drive the South Korean semiconductor market.

A-shares semiconductor pullback, aerospace stocks surge, Hong Kong chip stocks weaken

Today, A-shares exhibited an index adjustment along with active individual stocks. The Shanghai index closed down 1.00%, the Shenzhen component fell 2.29%, the ChiNext index dropped 4.37%, and the Sci-Tech innovation 50 index plummeted 5.53%. However, there were still over 3,700 individual stocks rising in the entire market.

The semiconductor sector overall retreated, with Zhaoyi Innovation having a transaction volume exceeding 59 billion yuan, creating a historical high; it ultimately fell over 7.7%; electronic chemicals, advanced packaging, glass substrates, and other previously hot directions collectively adjusted.

In contrast, the commercial aerospace sector became the biggest highlight of the day. China successfully achieved controlled recovery of a substage of the Long March 10 B carrier rocket for the first time and completed the world's first network recovery, indicating significant breakthroughs in domestic reusable rocket technology. Stimulated by the news, the commercial aerospace sector saw a comprehensive outbreak in the afternoon, with Aerospace Universe hitting the 20% limit up, China Satcom, China Satellite, XD Aerospace Electric, Aerospace Science and Technology, and Zhongtian Rocket all hitting the limit, with multiple satellite ETFs collectively hitting the limit during the day. Institutions believe that breakthroughs in reusable rocket technology mean launch costs may decline by more than 40%, ushering commercial aerospace into an accelerated industrial stage.

Innovative drugs also performed actively, with Changshan Pharmaceutical hitting the 20% limit up, and Zhongsheng Pharmaceutical, Zhaoyan New Drug, and Shuanglu Pharmaceutical hitting the limit; AI application directions remain resilient, with Skyworth Digital and Huansheng Century hitting the limit.

E Fund believes that the medium to long-term upward trend of A-shares has not changed, but as the mid-year report season approaches, the market will enter the performance verification stage, with high-prosperity core assets deserving more attention.

However, Hong Kong stocks continue to outperform A-shares, with the Hang Seng Index rising about 2% at one point. Goldman Sachs believes that Hong Kong stocks have entered the AI era and are in the midst of a structural bull market, with this year's IPO financing scale likely to reach a new high.

Chip stocks weaken: Zhaoyi Innovation fell over 20% to lead the decline, Tianjin Chuangxin fell nearly 19%, Montage Technology fell about 10%, SMIC fell 5.77%.

AI concept stocks fell: Zhipu fell over 20% to lead the decline, MiniMax completed about 16 billion Hong Kong dollars in financing and achieved several times of oversubscription, but due to dilution of stock allocation, the stock price fell over 10%; Xunce fell over 16%, Minglue Technology dropped about 9%.

Next week, the market will focus on China's second-quarter GDP, industrial added value, total retail sales of consumer goods, and other macro data, while also watching the IPO issuance progress of Changxin Technology, mid-year report performance disclosures, and whether policies promoting AI and commercial aerospace can continue to drive market risk appetite recovery.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。