First seize the market, then wait for regulatory improvements, this is Robinhood's strategic thinking.

Written by: Thejaswini M A

Translated by: Luffy, Foresight News

Engaging in illegal gambling privately in a barbershop has been illegal for a hundred years. But once operated by the state, it becomes a legal lottery. If a certain product is explicitly prohibited from direct sale by law, how can it be monetized stably? Capital will always flow to channels that exploit loopholes in regulations.

Last week, Robinhood CEO Vlad Tene officially launched its public blockchain and stock tokens at a press conference themed "The World is Flat." This theme sounds clever, but the so-called stock assets purchased by users are essentially "castles in the air."

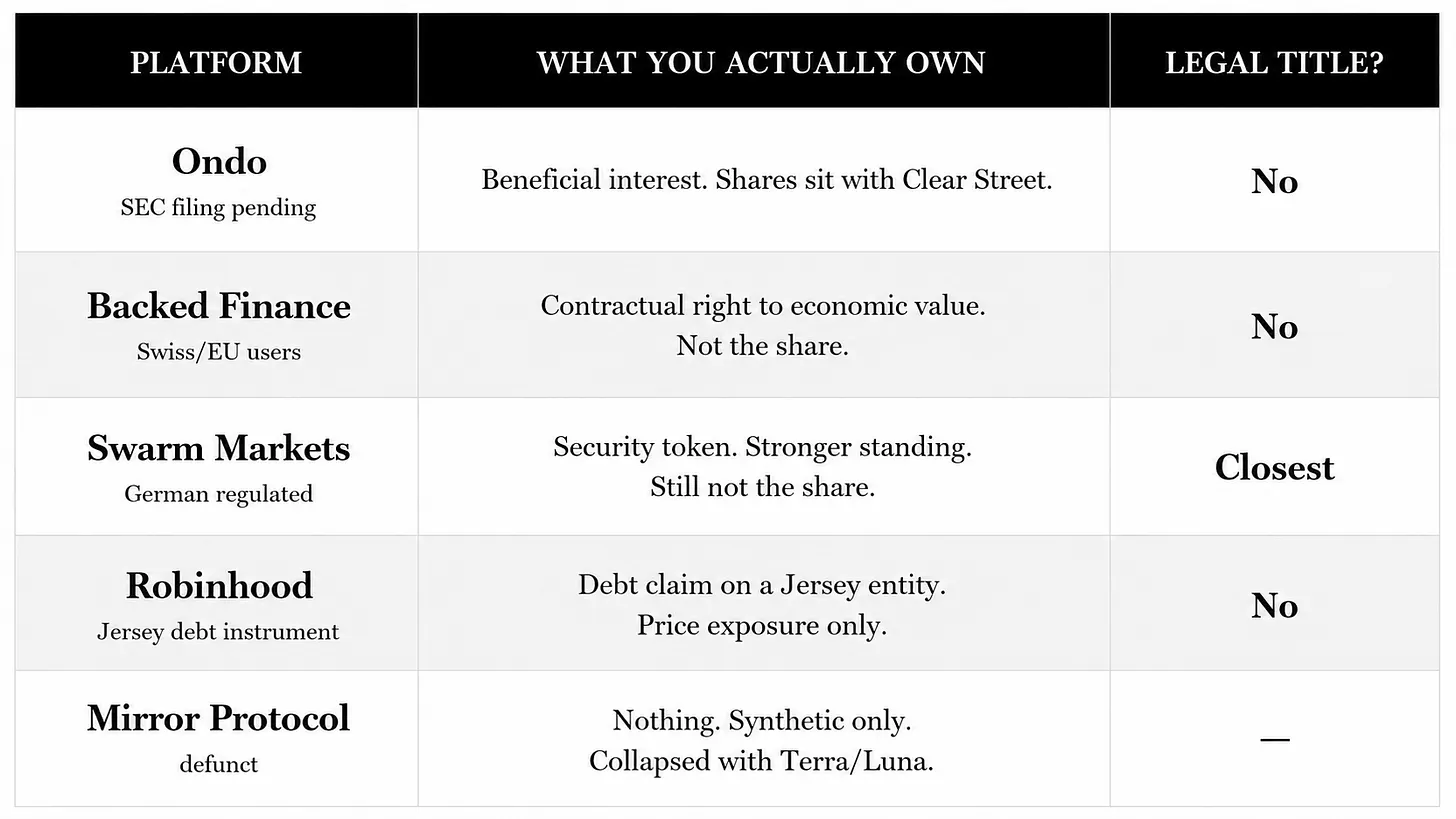

When you purchase Nvidia stock tokens, you can only track the fluctuations in Nvidia's stock price, but you do not enjoy any statutory shareholder rights. Once Nvidia's operations collapse, you have no claim to the company's assets. The tokenization model inherently carries such risks, and Ondo has already submitted relevant filing documents to the SEC, but the corresponding regulatory schemes remain unresolved.

The truth about Robinhood's product is that what you buy is not equity, but merely debt securities.

These debt securities are issued by Robinhood Assets (Jersey) Limited. Users are essentially lending money to this shell company located in a tax haven in the English Channel, and this shell company compensates you based on the rise and fall of the corresponding stock.

Let's rewind to the CANNES event in June 2025, when Robinhood, to create buzz for its product, distributed OpenAI and SpaceX private equity stock tokens for free to European users. The equity of these companies is not publicly available, and ordinary investors have no normal channels to subscribe. After OpenAI publicly issued a risk warning upon seeing tokens using its name, stating that it had never authorized the circulation of such assets; OpenAI co-founder Elon Musk even directly called such tokens fakes. At that moment, Robinhood CEO Tenev also admitted that these tokens are not equity in strict terms, but can only provide users with price exposure.

Since it can directly create equity tokens, why package it as debt and issue it through a Jersey shell company? The answer lies in the SEC's regulatory rules. Equity represents ownership of the business, enjoying rights such as voting, dividends, and asset liquidation claims; debt is the company's obligation to compensate you, and creditors do not have ownership rights in the business.

Robinhood's stock tokens are classified as "debt instruments resembling equity," and holders are not legal shareholders of the listed company. Even if you purchase the Nvidia token, Nvidia itself is completely unaware of your existence.

What you actually hold is a debt certificate issued by the Jersey shell company, which promises to settle earnings based on Apple's stock price. If Apple's stock price rises by 20%, this company will correspondingly pay 20% profit; however, once this Jersey shell company goes bankrupt, you can only become an ordinary creditor, waiting in line for recovery in liquidation. The real Apple stocks held by the shell company may cover your debt claim, or it may be insolvent, ultimately losing all principal, everything depends on the complex processes of bankruptcy liquidation.

If Apple itself declares bankruptcy, your situation will be even worse: you do not hold any Apple stocks, only a debt claim tied to Apple's stock price, and if the underlying asset value drops to zero, the claim will naturally be worthless.

Robinhood did not hesitate to design this complex structure, which can be traced back to the company's most brutal crisis in history: the January 2021 GameStop short squeeze. A large number of retail investors rushed to go long on the stock, but Robinhood directly shut down the buying channel. The US stock T+2 settlement mechanism resulted in a multi-billion dollar margin gap on the platform, unable to meet the requirements for clearing guarantees, thus it had to urgently restrict trading. A large number of retail investors felt abandoned by the platform, Congress specifically summoned Tenev for questioning, and the brand's trustworthiness has never fully recovered since then.

Five years later, this token product is seen as Tenev's solution: blockchain achieves second-level settlement, completely abolishing the T+2 settlement cycle, eliminating the need for significant margin calls and theoretically never needing to shut down the buy button again. Since early 2026, he has consistently promoted this logic, and Robinhood had already submitted a 42-page regulatory proposal for token assets to the SEC in 2025, calling for the introduction of specific industry rules.

In January 2026, three major SEC divisions jointly released guidance for the classification of token securities, dividing relevant products into two categories: the first category being native equity tokens: companies directly put their stocks on the blockchain, and holders possess full shareholder rights; the second category is associated securities: third parties issue tokens simulating stock prices, without any shareholder statutory rights and obligations. The SEC clearly stated that such products can be packaged as structured notes (debt products), and holders will bear additional counterparty risks that common shareholders do not face. If the issuer goes bankrupt, all losses are borne by the investors themselves.

In March of the same year, the SEC and the Commodity Futures Trading Commission (CFTC) jointly announced that the classification regulatory framework established in January remained unchanged. Robinhood deliberately chose to issue the second category of associated securities in Jersey Island, precisely avoiding regulatory red lines.

The regulatory document also mentions a class of similar products: securities-type swap contracts, which are essentially over-the-counter bets on stock prices. However, federal regulations strictly limit participation to qualified institutions and high-net-worth professional investors, ordinary retail investors cannot participate.

On the other hand, debt-type structured notes have no investor threshold restrictions, so even a 19-year-old with only $10 can participate. Robinhood ultimately chose this packaging model with the broadest audience and least regulatory resistance.

At the same time, users in the United States are completely excluded. Stock tokens are open to users in over 120 countries, with the United States, Canada, the UK, Switzerland, and the UAE not included in the service range.

The European market has a different compliance structure. The classic stock tokens launched in Cannes in 2025 adhere to EU MiFID II regulations and are issued by Robinhood's European entity, with tokens corresponding 1:1 to actual stocks held in custody. The number of targeted assets has now expanded from 200 to over 2000, with a minimum entry cost of only 1 euro. This means that Robinhood can completely operate compliant physical stock tokens in Europe, and the Jersey debt structure is a proactive choice.

This model heavily relies on the transparent pricing logic of the public market, as only live traded listed companies like US stocks have fair market prices. Companies like Anthropic and OpenAI that are not publicly traded do not have publicly available prices, and token valuations can only rely on subjective estimates by institutions; companies have no obligation to disclose information, making risks completely uncontrollable.

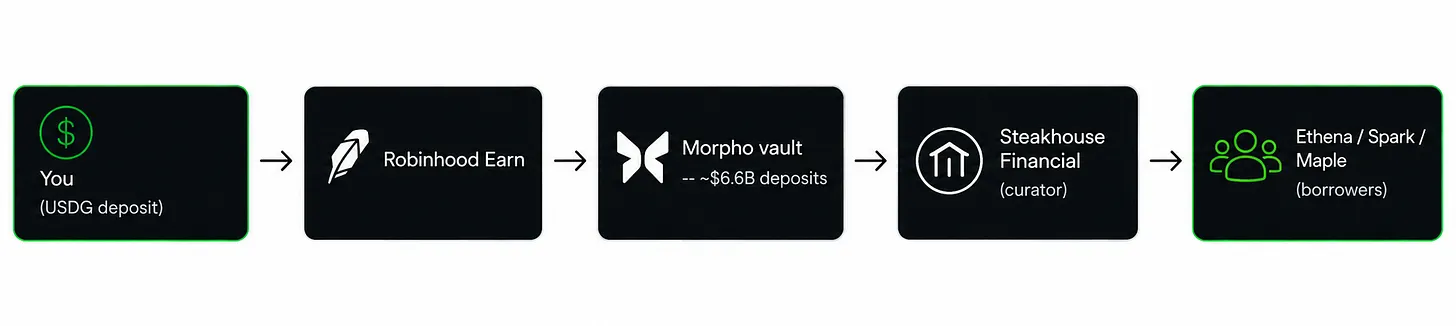

Additionally, Robinhood's newly launched Robinhood earning product independently offers an annualized return of 7%, limited to US users. Users lend stablecoin USDG, which first flows into the Morpho lending vault operated by Steakhouse Financial, and is then distributed to various DeFi protocols like Ethena and Maple. The Morpho vault has deposit scales of approximately $6.6 billion, with returns fluctuating based on market lending demands.

Robinhood insured against smart contract theft with Lloyd's of London, but the policy does not cover risks of return rates dropping to zero. When market lending demand shrinks, returns will decline in sync with money market fund rates. User funds must go through multiple intermediaries including Robinhood, Steakhouse, and Morpho, and once USDG unpegs or borrowers default on a large scale, insurance cannot cover the losses, which is also a common inducement for principal losses in such products.

The tokens are stored on-chain, supporting staking and lending, which seems convenient, but smart contracts cannot directly read stock prices and depend on oracles for pricing. If the oracle feeds false prices, the contracts may inaccurately liquidate user assets or issue loans improperly. Between 2024 and 2025, oracle price manipulation was a key method for large-scale theft in DeFi, with dozens of projects losing tens of millions of dollars as a result.

In the entire product system, the only real, fully-fledged shareholder voting rights belong to Robinhood's own stock HOOD traded on NASDAQ's traditional channels. The platform kept the real equity to itself.

The underlying business logic is clear. With every token transaction, Robinhood earns the spread; the public chain belongs to itself, and the new overseas business can continuously beautify the listed company's financial report, operating completely without restrictions from US regulatory oversight. The token business without actual equity has lower regulatory costs and cleaner profits.

Robinhood's public chain is built on the Arbitrum Orbit network, using ETH to pay Gas fees, and has not issued a native platform token, avoiding token speculation risks, while the platform does not need to profit from a native token. The company's long-term plan is to create a one-stop settlement channel for stocks, ETFs, stablecoins, commodity perpetual contracts, and future private equity, achieving 24/7 on-chain trading. Robinhood was initially just an order distribution intermediary; if the planning is realized, it would integrate the functions of an exchange and a clearinghouse.

Objectively speaking, current regulatory rules are rapidly iterating. The new SEC chair, Atkins, has reversed the previous "sue first, regulate later" regulatory approach and is drafting an innovative regulatory sandbox exemption bill, with the "CLARITY Act" submitted for Senate review since June. Once the bill is enacted, the regulatory gray area where Robinhood currently resides will continue to tighten.

This approach has already become common in the industry. In its early years, Coinbase and Kraken expanded their businesses in regulatory gaps, and then filled in compliance qualifications only after regulatory details were completed and industry demand validated. Today's Jersey debt tokens appear more like a transitional unfinished product from Robinhood.

Just two days before the launch of Robinhood stock tokens, on July 2, Ondo launched compliant tokenized stocks on Ethereum, issued by an SEC-registered transfer agent, with tokens fully backed by actual stocks, allowing holders to enjoy on-chain voting rights, covering over 250 companies. Coinbase also launched this product simultaneously, allowing US users to trade legally, with dividends directly issued to user accounts.

The operational cost of a complete compliance model in the US is higher and fully subject to regulatory constraints, while Robinhood has already borne this compliance cost in Europe. Thus, the debt structure of Jersey Island is a choice for Robinhood, where future regulations may either force product upgrades or competitors may launch compliant real stock tokens in the US to attract clients.

First seize the market, then wait for regulatory improvements, this is Robinhood's strategic thinking.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。