K-shaped Fundamentals: Betting Logic in Extreme Times

History is the ruthless victory over the brainless.

I think I've found the answer, the question being: "In the context of the RWA increasingly embracing blockchain and stablecoins steadily moving towards payments, the crypto industry or token market has completely lost the fundamental basis for capital valuation."

This is actually quite strange; blockchain is indeed the future of finance, but the focus of the era has shifted to "technological competition." Even if the AI bubble bursts, there are new frontiers such as nuclear fusion, commercial space travel, and biomedicine.

Blockchain is in an awkward position; Western counterparts have no direct counterparts in the East, which leads to a failure of competitive mechanisms, resulting in a lack of upward momentum in the market, reducing it to a dumping ground for tokens or a meme nihilism.

We cannot change this; no matter how magnificent the mechanisms are, we cannot carry sovereign-level assets, encapsulating digital RMB, tokenized national bonds, or A-shares on-chain.

After coming to this understanding, the question actually becomes simpler: how does a niche but long-term certain market return to a market valuation system?

The Collapse of the Middle Class

East-West opposition, hard technology rises.

These are the two major themes of today’s crypto industry, just as the 2008 financial crisis was a midwife for Bitcoin.

Under ideal conditions, stablecoins serve as a link between opposing worlds, similar to the role of Eurodollars during the Cold War, communicating the rigid demands between two camps.

Currently, both sides are still determining boundaries; the turbulence will continue for some time, and one can even think that stablecoins are ultimately a kind of meal replacement for Chinese concept stocks.

Before reaching the boundary, we still need entrepreneurs and VCs to work hard to find a place to settle down and patiently wait for the moment to make a comeback.

The rise of hard technology will not take away liquid capital from the crypto circle; rather, it will create new speculative targets. Blaming the desolation of the crypto market on the rise of AI is a form of mental laziness.

- The ceiling of the crypto industry is limited; only 55 companies can reach a $1B valuation, while there are currently 1,603 unicorn companies globally.

- The crypto industry is more like a super-sized Alt Pre-IPO system that cannot reach Nasdaq; you can try Binance first.

Don’t get a sense of industry disillusionment; it’s normal for humans to search for survival. The "runaway" Meta doing AI is just as powerful as the previous fundraising of Oasis Labs with $45 million; treat them as a bellwether for the maturity of an industry.

Outside the token mechanism, Pre-IPO can also work, and it will seriously impact the pricing logic of foreign assets, while permissionlessness will again spark economic games. This is not isolation; it will become more routine.

The real crisis lies outside the consensus, namely, that the fruits of innovation in the crypto industry will be rapidly monopolized, leading to one or two main players growing rapidly in each track, and then it ends.

Binance, as a trading bank, took five years (2017-2022) to become the industry leader, but I doubt that the next generation of products will have such a long time to develop, or that the competition among new giants will be extremely fierce.

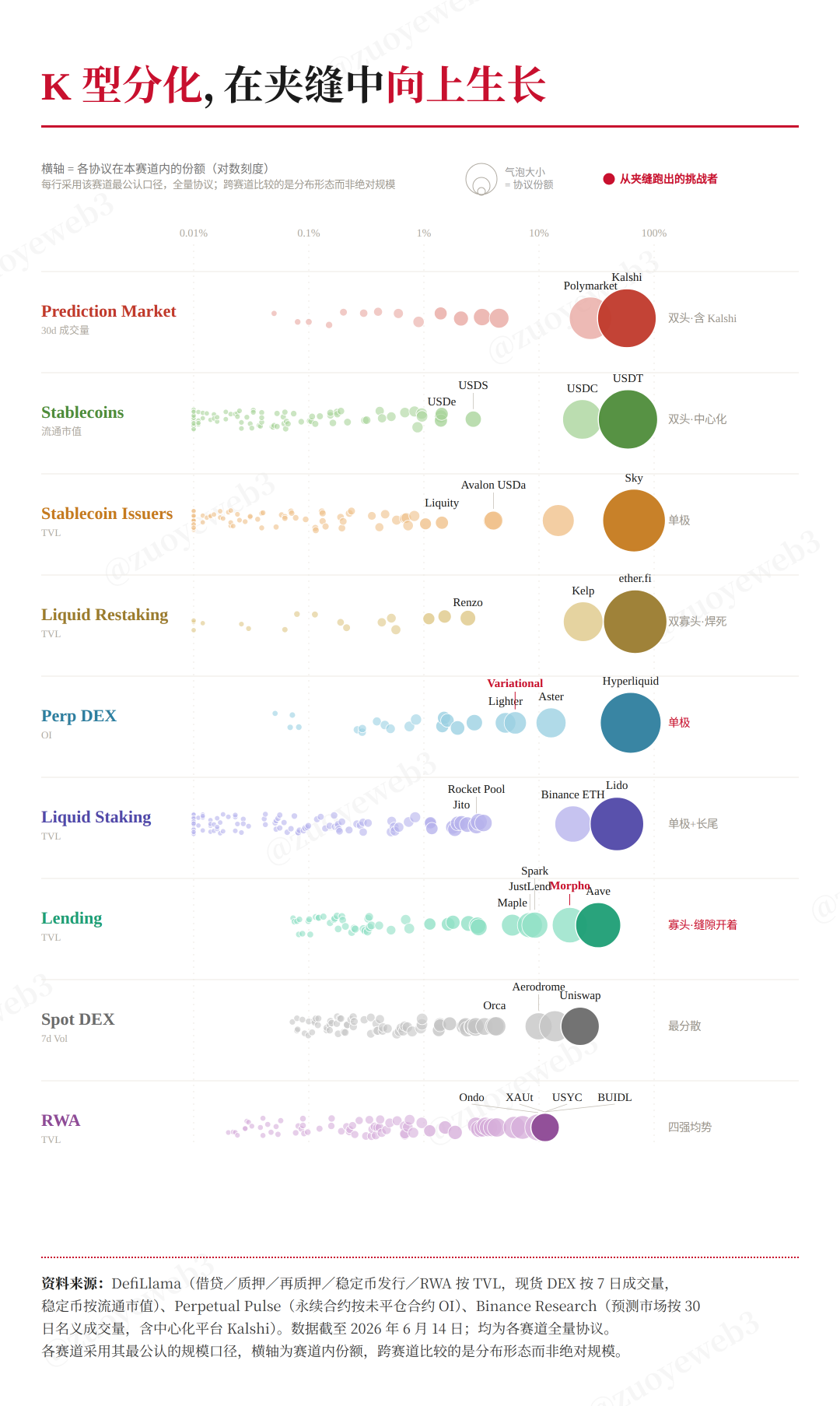

Image caption: The era of K-shaped differentiation

Image source: @zuoyeweb3

It’s not just stablecoins, exchanges, lending, and other old tracks; PerpDEX, HIP-3, and prediction markets are even faster. TradeXYZ has already ended the HIP-3 conflict, while $USDH has only actually survived for about a few months.

As crypto is a virtual product industry, it no longer serves as an asset target and must seek real uses, receiving external assets, which in turn creates greater volatility.

Volatility itself is not terrifying; the problem lies in our inability to profit from it. Each track is too quickly defined, leaving less and less room for individual speculation.

Moreover, in the upcoming AI landing era, the process will accelerate further. Looking back since the narrative of Vibe Coding, the most severe impact on all humanity is the "middle class":

- White-collar office skills are gradually being replaced by agents.

- The technical abstraction layer of SaaS is steadily being overtaken by large models.

- Companies lack patience to nurture the gap between junior and senior talent.

The above three are beneficiaries of the era's black swan, but this also means that the distance between startups and Mag7 is compressed to infinity. SpaceX's valuation reached $2 trillion in 24 years, while Anthropic hit $1 trillion in just five years.

To refine this, the new forces in the crypto industry will find the time to enter the 55 company $1B club even shorter, but you must choose the right new track and ensure to end the battle quickly.

One piece of good news is that the collapse of token economics has quickly led the crypto industry from "technological idealism" to "financial services," where whoever can find more funding can quickly replace the old predecessors.

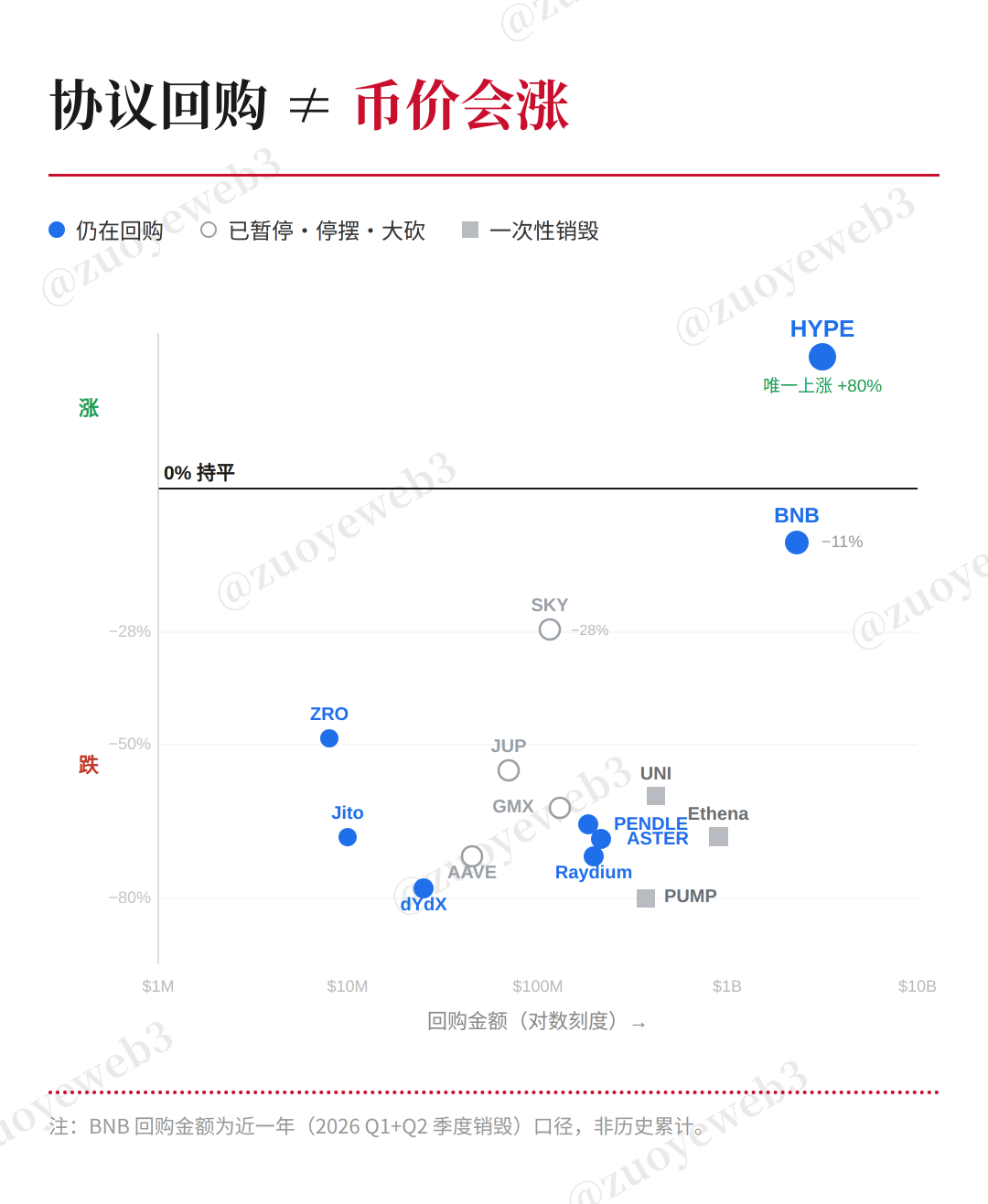

Image caption: The norm is that the coin price does not rise

Data source: @CoinMarketCap

In the past year, buybacks have been unable to stop the overall downward trend in the token industry. In contrast, American stock buybacks have been the foundational driving force for the past thirty years.

If a market's obvious buy-in cannot convince others to hold assets, it means that the underlying motivation source has reached a point of total innovation.

From the perspective of VC, let’s predict the source of innovation.

Riding on the Back of a Silver Dragon

When light-speed venture capital brought in Claire Zau specifically for podcast production, A16Z had already transformed into a top-tier asset management company. In Q1 2026, the top six VCs in America took nearly 80% of the fundraising amounts, corresponding to 0.1% of the top five startups taking 73% of the capital amount, reaching $195.6 billion.

The spending of AI companies, to a large extent, aligns with the profit sources of "hair-pulling" parties—both are fed by VC money, hoping that AI ultimately does not turn into shitcoins.

To date, it is hard to discern whether this K-shaped differentiation is triggered by AI or if it ultimately creates a capex frenzy in the AI era.

In our usual memories, venture capital is an early, small-scale, and experimental technological bet, but under the operations of A16Z, it has turned into a gamble that one cannot afford to lose.

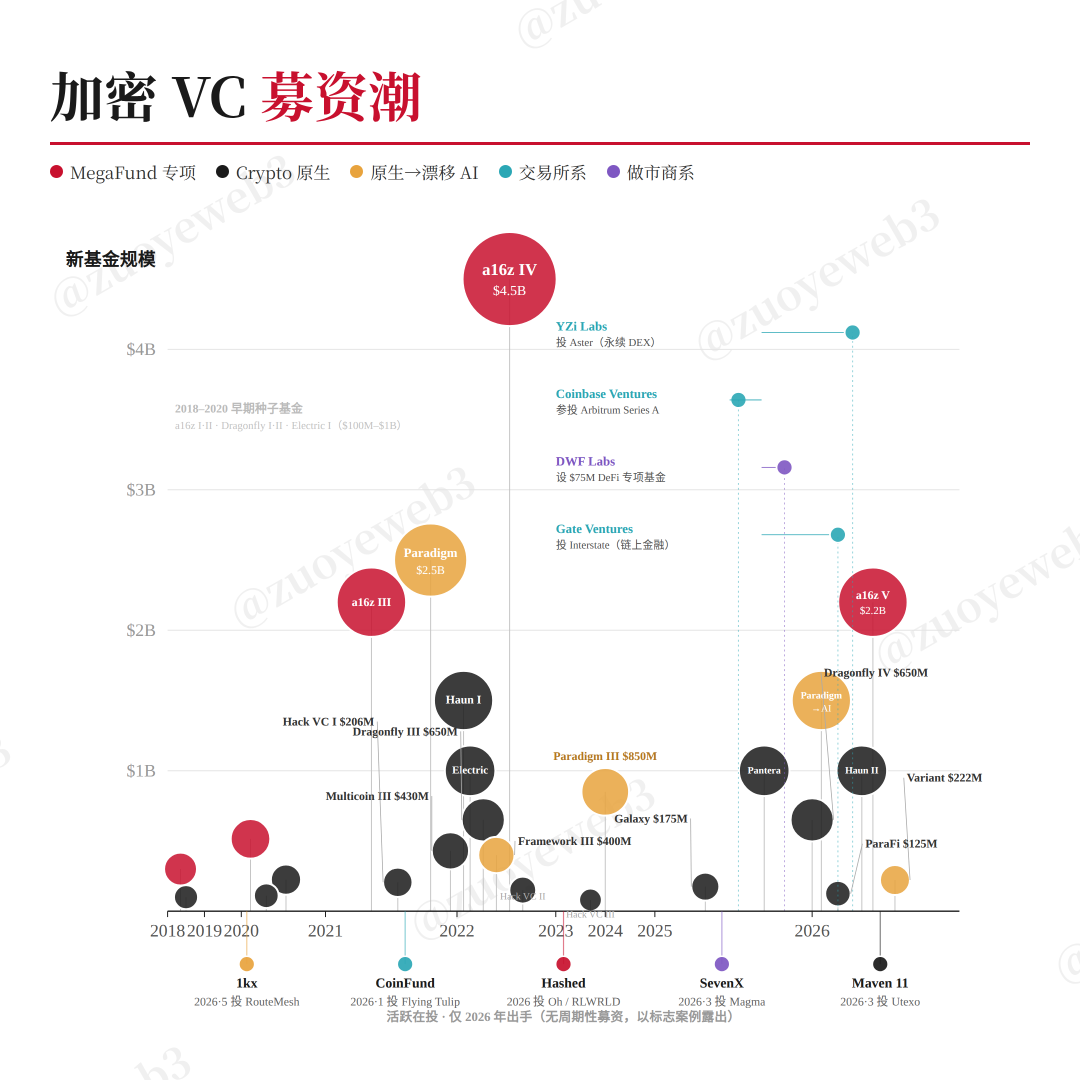

Image caption: New trends in fundraising

Data source: @PitchBook

In such extreme scenarios, VCs that can successfully raise funds and invest have turned venture capital into a quasi-Ponzi funding game.

The shiny return rates for VCs need to be divided into three parts: the old LPs exit DPI, the existing holdings IRR, and the fundraising APY. DPI represents real APY, while new LP funds are attracted as TVL.

We cannot find the next suitable project for "hair-pulling" from RootData's fundraising programs, and we can't even distinguish the proportion of funding received; the entire crypto industry has fallen into an investment era devoid of signals.

Alternatively, it could transform into a secondary research agency for US stocks, which is also an important driving force behind Pre-IPO and on-chain US stocks.

No one can create industry-level investment entry signals. Vitalik's vision of reshaping DeFi mechanisms with options is hard to evaluate as right or wrong, but the complexity of the mechanism itself is a signal.

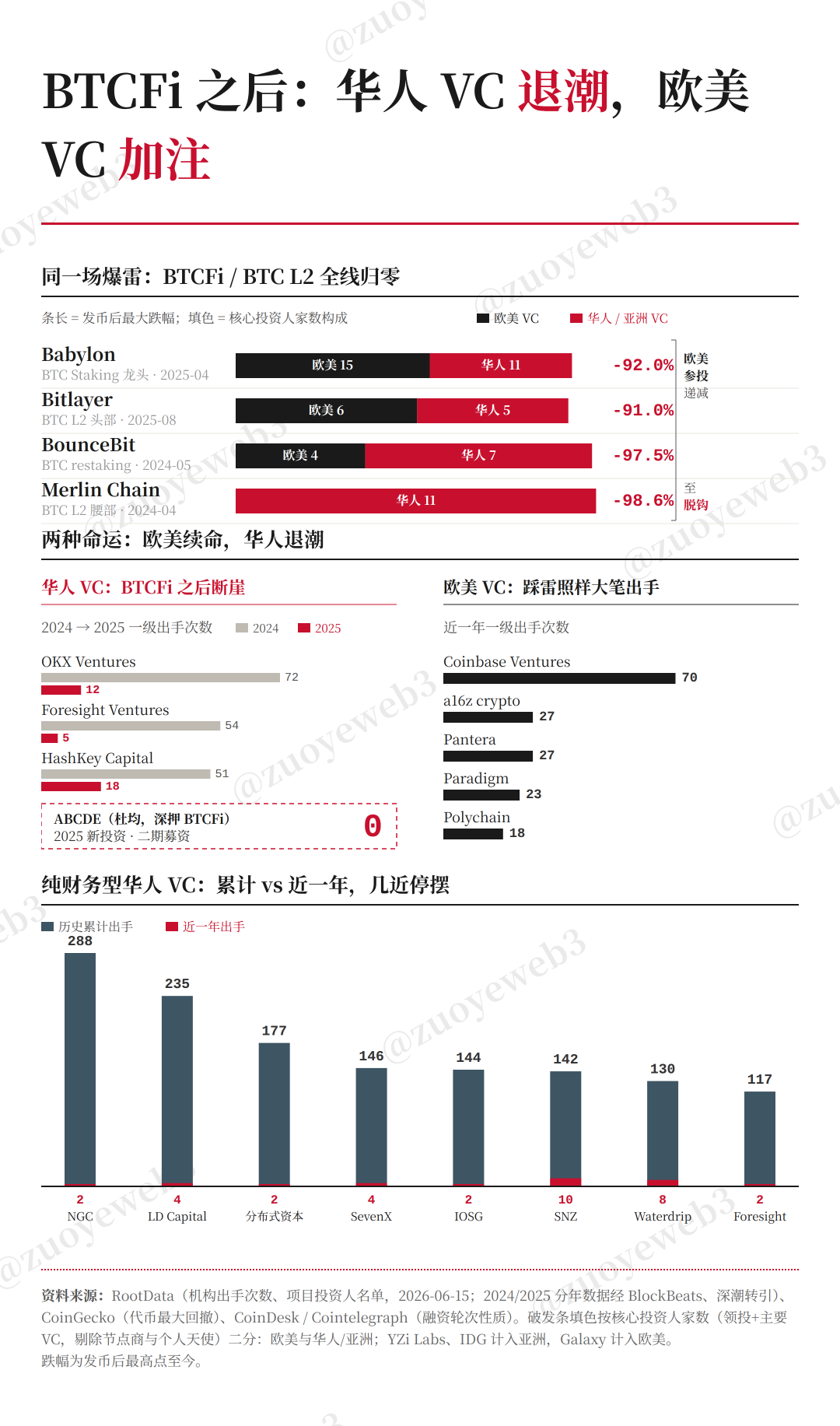

However, I can outline the process of signal collapse for Chinese entrepreneurs. The BTCFi wave at the end of 2024 saw many Chinese VCs raise their flags, completely unable to exit, a despair that even junk exchanges cannot escape.

Image caption: BTCFi breaks Chinese VCs

Image source: @zuoyeweb3

Before this, Chinese VCs took on a dual role of project discovery and initial pricing. Once a project gained approval from Chinese VCs, it could step into the visibility of more "mainstream" or "wealthier" US VCs, achieving higher valuations.

However, after enduring the battering from ETH L2 and BTC L2, American VCs can still rely on capital advantages to seize the pricing power for the upcoming stablecoins and RWA.

After this, Chinese VCs will basically miss out on the new round of competition in Perp DEX. Only VC from Chinese exchanges can barely participate, but regarding the overall industry landscape, Chinese entrepreneurs can only be trapped in the trading track, while broader financial services like payments (stablecoins) and RWA face dual entry barriers from both Chinese entrepreneurs and investors.

The good part of "Water Margin" is giving up, while the bad part of the crypto world is the cycle.

The agent wave has surged; the lobster craze is basically receding, and coding agents are becoming overshadowed by hardware chips. However, pay attention to a long-term trend: we have not seen the application paradigms under the new technology wave yet.

The K-shaped differentiation law remains effective; the reconstruction and transformation of the crypto circle by agents is almost certain to happen quickly in some hot spot, with a specific track being born, finishing the decisive battle within 2 to 3 months.

If this cycle does not give birth to such phenomena, we can just continue to lie low. Once signals arise, investors and entrepreneurs can feel the super-fast rhythm of a $1B funding pool, which is also the eternal allure of the crypto world.

Conclusion

This is the most difficult era for entrepreneurs; either you go solo or a giant monopolizes. There is no longer a slow growth space for growth stocks, and time has become an urgently needed lever that compresses deadlines.

Giantization means industry maturity, which will reduce speculative space but also provide sufficient margin for error, allowing new emerging forces to continue to be sparked.

We compress the time and space to constrain the topics we need to discuss—macroeconomic political changes and the surging AI wave. This has not made the crypto market disappear, but the sense of moral dislocation is becoming increasingly severe.

From a personal sensation, there are huge problems in the market structure; the entire industry lacks consumption. From the introduction of index futures to exchange wealth management activities, no one needs retail investors to hold assets long-term, but rather constantly "urges" users to leverage.

This is quite disjointed; the consequence of offering more choices is that users must constantly choose and cannot pause for a moment; otherwise, the market will collapse immediately.

The market is very cold, but capitalization is accelerating rather than stagnating. I wonder if crypto can generate the next concentrated wave of thousandfold returns.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。