Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: As July begins, the global semiconductor supply chain is experiencing a new round of collective price increases. More than a dozen giants, including Murata, Infineon, and Texas Instruments, announced price hikes starting July 1, with increases as high as 40%. On the same day, Samsung Group unveiled a 1,000 trillion won (approximately 648 billion USD) domestic investment plan for the next decade, centered around chip manufacturing. The A-share semiconductor sector continued its upward trend today, with Galaxy Microelectronics hitting a 20% limit up.

The demand for AI computing power is rewriting the pricing rules of the global semiconductor supply chain.

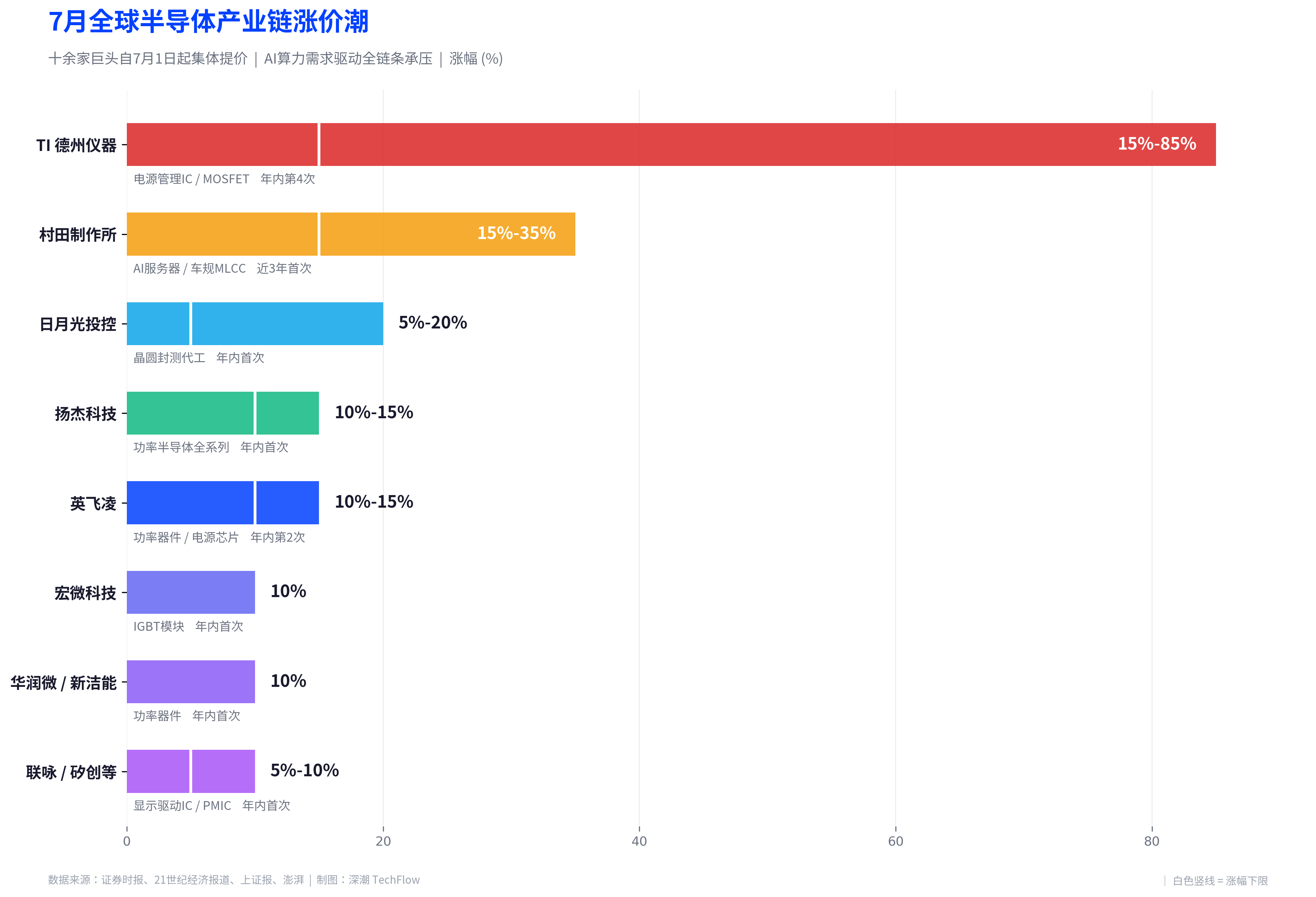

According to reports from several media outlets, including Securities Times and 21st Century Business Herald, starting from July 1, more than a dozen leading semiconductor and electronic component companies, such as Infineon, Texas Instruments (TI), Murata, and Yangjie Technology, will collectively implement a new round of price increases, covering multiple key links from upstream wafer foundries to end chips. Meanwhile, on June 29, Samsung Group officially announced an industrial blueprint for investing 1,000 trillion won over the next ten years at the South Korean presidential office, with approximately 300 trillion won allocated for chip manufacturing. The A-share market saw continued increases today in the semiconductor supply chain, with Galaxy Microelectronics hitting a 20% limit up, and Yangjie Technology and Hongwei Technology rising over 5%.

More than a dozen giants collectively raised prices in July, while AI demand squeezes capacity across the entire industrial chain

The core driving force behind this price increase wave is not the traditional inventory cycle, but the structural squeeze on the global semiconductor supply chain caused by the demand for AI computing power.

Infineon has notified customers that it will raise prices for certain products starting July 1, marking the company's second price increase within 2026. According to Securities Times, Infineon CEO Jochen Hanebeck stated during a conference call in early May that the demand for AI data center power solutions is extremely strong. Infineon's Power and Sensor Systems segment experienced a year-on-year sales increase of 26% to 1.26 billion euros in the second quarter, and the company has raised its sales outlook for fiscal year 2026 from "moderate growth" to "significant year-on-year growth."

Texas Instruments also plans to raise prices for core products such as power management ICs starting July 1, marking the company's fourth price adjustment within 2026. According to China Business News, in the last round of price increases on April 1, Texas Instruments raised prices for core products like power management ICs by 15% to 85%. TI reported a year-on-year revenue increase of approximately 90% in data center revenue for the first quarter, indicating that AI demand is rapidly spreading from GPUs to areas such as power management, server power systems, and high-voltage MOSFETs.

In the passive components sector, Murata, the world's largest MLCC supplier, has previously launched a comprehensive price increase for AI servers and automotive-grade MLCCs, with increases ranging from 15% to 35%. According to Shanghai Securities News, Murata occupies about 70% of the global market share for AI server MLCCs, and its president, Norihiko Nakajima, publicly stated in February this year that the order volume from customers is twice the existing production capacity, which "cannot be satisfied at all."

Domestic manufacturers are also following suit. Yangjie Technology, a leading power semiconductor company, announced that it will raise the prices of its entire product line by 10% to 15% starting July 1, due to continuous price increases in upstream chip wafers, bulk metals, and packaging raw materials. According to The Paper, this round of price increases almost covers all IC design companies in Taiwan, with multiple Taiwanese IC design manufacturers such as MediaTek, Silergy, and Silan Semiconductor issuing price increase notices consecutively.

Bernstein noted in its latest tracking report that the price increases are driven by three factors: the power demand of AI servers squeezing capacity, upstream foundry price increases, and geopolitical factors pushing up raw material and energy costs. This round of price increases is not an isolated incident but a cyclical resonance across the entire industry.

Samsung's 648 billion dollar "largest investment in history," with chip manufacturing at its core

As the price increase wave in the supply chain accelerates, the world's largest memory chip manufacturer, Samsung Group, officially announced an investment plan that sets a record for South Korean enterprises on June 29 at the Blue House.

According to Financial Associated Press, quoting the South Korean "Daily Economic News," Samsung Group plans to invest over 1,000 trillion won (approximately 648 billion USD) in South Korea over the next ten years, equivalent to half of South Korea's GDP. South Korean President Yoon Suk-yeol presided over the "Korean Great Leap Three Major Super Projects National Report Meeting," attended by Samsung Electronics Vice Chairman Han Jong-hee, SK Hynix CEO Park Sung-wook, and other corporate executives.

The investment blueprint covers four major areas: semiconductor chips, AI data centers, energy storage batteries, and high-end display panels. According to Investing.com, Samsung plans to invest approximately 300 trillion won to build a large chip manufacturing plant in Jeollanam-do, South Korea, and will invest over 350 trillion won in AI data center projects. The site selection avoids the capital region's industrial clusters, responding to the South Korean government's regional balanced development policy.

Samsung's financial strength supports this scale of investment. According to Eastmoney, Samsung Electronics' operating profit for the first quarter of 2026 reached 57.2 trillion won, soaring 756% year-on-year. Analysts forecast that its annual operating profit for 2026 will soar to 550 trillion won, and the cumulative operating profit during the semiconductor boom cycle from 2026 to 2028 is expected to exceed 1,500 trillion won.

SK Hynix is also ramping up efforts. This week, the company announced plans to issue American Depositary Receipts (ADRs) on Nasdaq on July 10, raising up to 45.45 trillion won (approximately 20.1 billion RMB). The funds raised will be used for the construction of the first-phase wafer fab of the Yongin semiconductor cluster, the advanced packaging plant in Cheongju, and equipment investments. According to Yicai Global, the South Korean government announced the construction of four chip plants in the southwestern region on the same day, with an investment of approximately 800 trillion won, expected to double DRAM production capacity within five years.

Global semiconductor market scale sprinting to one trillion dollars, "structural inflation" replacing cyclical recovery

The industrial background of this price increase wave is that the global semiconductor market is experiencing unprecedented expansion.

According to data cited by 21st Century Business Herald, global semiconductor sales reached 298.5 billion USD in the first quarter of 2026, a year-on-year increase of 79.2%, and the full year is expected to exceed one trillion USD. The World Semiconductor Trade Statistics (WSTS) organization's latest spring forecast has significantly raised the global market size for 2026 to 1.51 trillion USD, representing an increase of nearly 90% year-on-year. SEMI reports that global semiconductor equipment shipment value reached 36.55 billion USD in the first quarter of 2026, with a year-on-year increase of 14%, marking the highest quarterly record in history.

Several industry insiders interviewed by China Business News indicated that the current situation is not a super cycle fully driven by a comprehensive boom in consumer electronics as seen in 2020 to 2021, but a more accurate definition is "structural inflation under AI dominance." AI, as the strongest demand engine, has raised the entire semiconductor supply chain's cost center and resource threshold, with memory and logic chips increasing due to AI, while passive components, power management ICs, and others have increased because they must make way for AI or are impacted by cost factors.

According to statistics from TrendForce, the average utilization rate of 8-inch capacity among the top ten global wafer foundries has risen to nearly 90%, significantly improving from nearly 80% in 2025. Capacity tightness is also being transmitted to the testing and packaging stages, with leading packaging and testing company ASE Group planning to raise wafer testing and packaging service prices after the second half of 2026, with expected increases of 5% to 20%.

A-share semiconductor continues to rise, with the ETF up over 136% this year

Under the dual catalysts of the price increase wave in the supply chain and Samsung's massive investment plan, the A-share semiconductor sector continued its strong performance today.

According to Daily Economic News, on June 29, the semiconductor supply chain continued to rise, with Galaxy Microelectronics hitting a 20% upper limit, Shengkong Co. rising over 10%, and Hongwei Technology, Yangjie Technology, Yake Technology, and Fuman Micro rising over 5%. The previous week, TSMC's notification to raise wafer foundry prices had triggered a collective rally in the semiconductor sector, with Changjiang Electronics Technology hitting a historical high during three trading days.

From the ETF fund flow perspective, semiconductors have become one of the largest thematic trades in the A-share market in 2026. According to Securities Times, among the top twenty ETFs in terms of rising percentage in the entire market in the first four months of 2026, twelve are related to semiconductor themes, accounting for over 60%. The China-Korea Semiconductor ETF from Huatai-Pinebridge has risen 66.51% this year, leading the entire market; the sub-sector ETFs in innovative chip design, innovative chips, and innovative semiconductor equipment have all surpassed a 30% increase during the same period.

Funds continue to flow into the semiconductor direction. In the past five trading days, over 7.1 billion yuan has flowed into the ETF related to the semiconductor materials and equipment index. The circulating size of the innovative chip ETF managed by Harvest has grown from 38.6 billion yuan at the end of the first quarter of 2026 to about 45.5 billion yuan.

Risks to watch include that Goldman Sachs has warned that "the substantial valuation dividends in the storage sector have been largely realized in advance," and Hong Hao from Lianhua Asset Management also pointed out that storage leaders like SK Hynix have "increased sensitivity of stock prices to marginal bad news." The A-share semiconductor ETF trading congestion is at a high level; although Samsung and SK Hynix's large-scale expansion plans temporarily boost sentiment, they may change the core narrative of "supply-demand imbalance" in the medium term.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。