Preferred stock STRC hits a new low again, will Strategy see a reverse flywheel?

Written by: ChandlerZ, Foresight News

On June 25, Bitcoin officially fell below the $60,000 mark, reaching a lowest intraday price of $58,030, marking a new low since October 2024. ETH also dropped to $1,519, and SOL reported $65.99, with mainstream assets under pressure across the board.

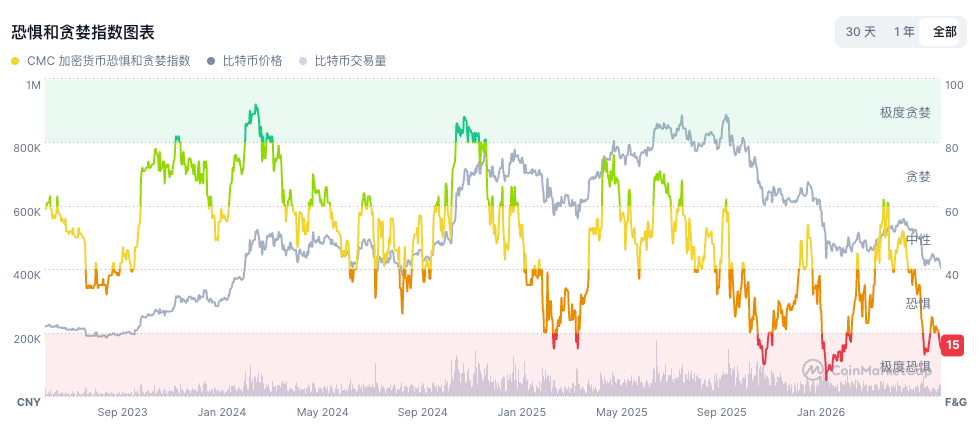

Coinglass data shows that over $1 billion in leveraged positions were liquidated in the past 24 hours, with longs accounting for $788 million. The Fear and Greed Index dropped to 15, indicating an extremely fearful zone.

Bitcoin has retraced over 53% from its all-time high of $126,198 set in October 2025, with the bear market extending into its 8th month.

In the bull market logic of the past two years, there were two key pillars for Bitcoin: one was the flywheel model represented by Strategy's DAT company, which continuously bought Bitcoin through securities financing, and the other was the massive institutional inflows following the launch of U.S. spot ETFs. These two channels collectively built the demand foundation for the last Bitcoin bull market. The current issue is that both of these pillars are becoming unstable.

Strategy's financing flywheel continues to lose momentum

In this downtrend, the most noteworthy variable is the world's largest corporate Bitcoin holder, Strategy.

As of June 21, Strategy held 847,363 Bitcoins, with an average cost of about $75,651, and is currently facing an unrealized loss of over $14.6 billion at current prices. In recent years, the company's core strategy has been to issue stock and preferred stock for financing, then continuously buy Bitcoin. This cycle of "issuing securities, buying Bitcoin, pushing up coin prices, supporting stock prices, and then issuing securities again" has made it one of the most stable institutional buy-side sources in the Bitcoin market, and allowed MSTR’s stock price to exceed $457 at one point in 2024.

However, the key gears of this flywheel are starting to decouple. In July 2025, Strategy issued variable rate preferred stock STRC through a $2.5 billion IPO, aimed at anchoring at a $100 par value. The company could adjust the dividend rate monthly to maintain this anchor. STRC was positioned as a financing product aimed at the mass market, hoping to attract ordinary investors to participate in Bitcoin investment with lower volatility.

However, STRC has continued to weaken since its listing, dropping to about $75 on June 25, a historical low, a discount of 25% from its par value. According to the terms, if STRC falls below $95, it will trigger an automatic interest rate increase of 0.5%, and the current annualized dividend yield has climbed to about 11.5%, with annual dividend expenses increasing by about $53 million. The company's cash reserves are about $1.4 billion, barely enough to cover a little over a year's dividend expenses.

Amina Bank's derivatives trading head, Andreja Cobeljic, analyzed that the direct reason for Bitcoin's recent decline is the weakening of the market cycle, but a deeper driving force is the impact on Strategy's strategic credibility. If STRC continues to struggle to return to its par value, Strategy's ability to finance and buy coins through this channel will be significantly weakened, potentially interrupting the most important source of incremental funds in the Bitcoin market over the past two years.

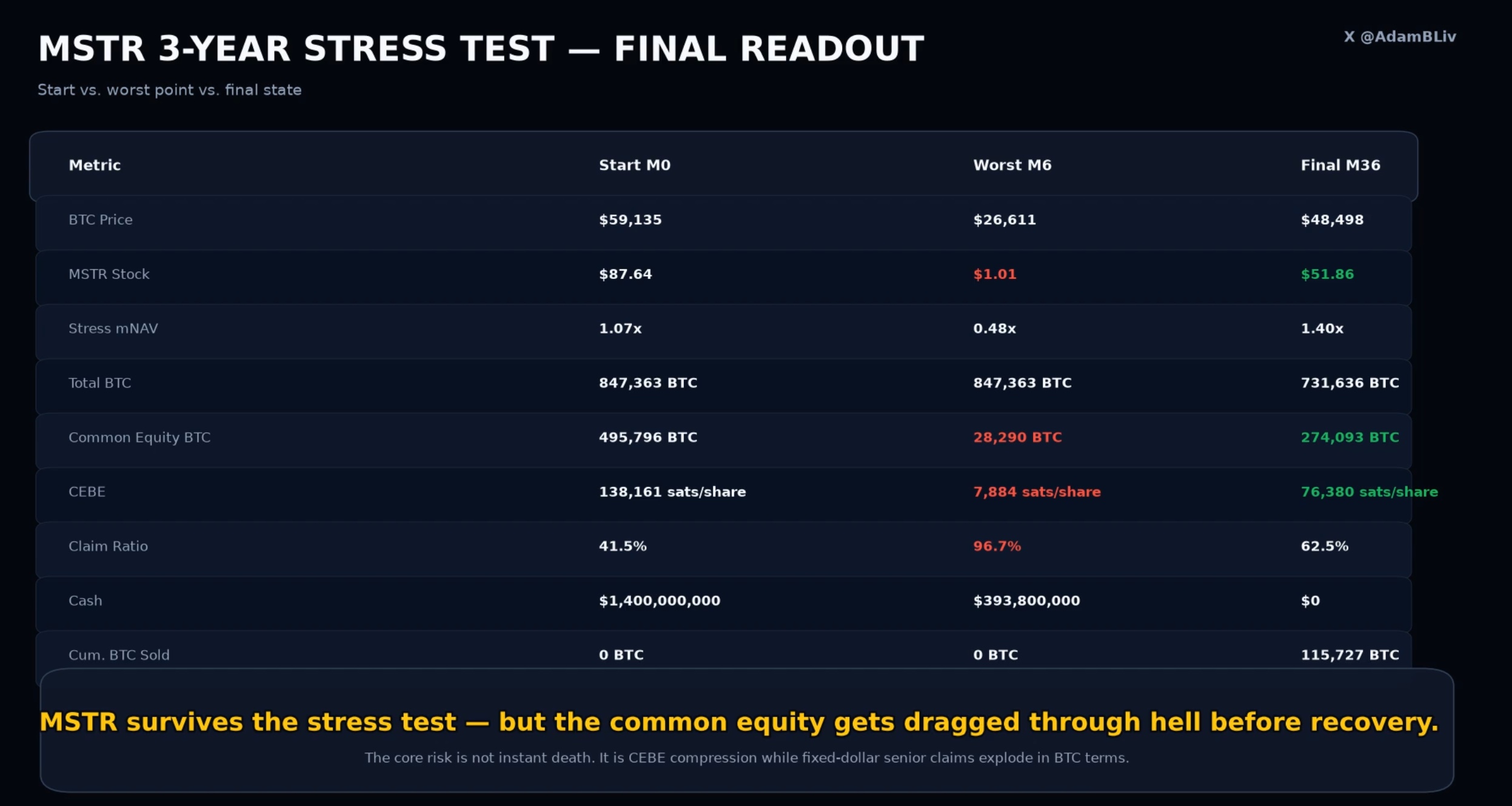

Analyst Adam Livingston conducted a three-year stress test on MSTR based on current data, simulating an extreme scenario where Bitcoin plummets 55% to $26,611 in the 6th month, while the capital markets are entirely closed, preventing Strategy from issuing new stocks or bonds and continuing to buy Bitcoin.

In this scenario, Strategy's preferred debt structure would quickly become critical. Both preferred stock and bonds are fixed dollar claims; when the coin price crashes, their conversion into BTC will balloon significantly. The model shows that the BTC equivalent claims of preferred debt would soar from 350,000 coins to 819,000 coins, accounting for 96.7% of the total holdings, nearly swallowing the entire Bitcoin inventory. The equity available to ordinary shareholders would shrink from 496,000 coins to 28,000 coins, and MSTR's stock price would be simulated to drop to $1.01. Meanwhile, the fixed monthly expenditure of $167.7 million (dividends from preferred stock plus debt interest) would continue to deplete cash, and by the ninth month, cash would be exhausted, forcing the company to start selling Bitcoin to maintain debt operation, resulting in a total sale of about 116,000 coins over three years.

However, the model's conclusion is that Strategy survives. Assuming Bitcoin rebounds to $48,498 three years later, the company would still hold 732,000 BTC, MSTR’s stock price would return to $51.86, and the mNAV would recover to 1.40 times. Livingston's judgment is that the real risk is not the bears screaming "immediate bankruptcy," but rather the inflation of preferred debt priced in BTC during coin price crashes, temporarily consuming almost all ordinary shareholder equity. However, the model ultimately does not conclude a "death spiral."

Institutional retreat, macro tightening, funds shifting to AI

Strategy's issue exists within a larger backdrop of capital withdrawal.

On June 24, U.S. spot Bitcoin ETFs saw a single-day net outflow of $469 million, with BlackRock's IBIT accounting for $239 million, marking the fifth consecutive trading day of net outflows. Cumulatively, approximately $2.8 billion to $3.5 billion flowed out in June, constituting the most severe ongoing capital flight since the product was approved in January 2024.

Bloomberg ETF analyst Eric Balchunas recently stated that Bitcoin is overly dependent on narratives related to ETFs and Strategy (MSTR), and the market should not view them as the main line of Bitcoin's value. He believes both should be complementary rather than the whole cake. When Strategy's buy-side slows down and ETFs start bleeding simultaneously, Bitcoin's demand side lacks the two most critical sources of incremental funds.

Old money is leaving, and new money is also not coming in; the macro environment continues to tighten. On June 25, the PCE price index for May was released, rising 4.1% year-on-year, marking the fastest growth in over three years, while the Federal Reserve maintained interest rates at 3.50% to 3.75%, further delaying expectations for rate cuts this year. On the same day, U.S. stocks initially rose and then fell, with Apple announcing price increases across multiple product lines globally (up to $300) due to storage chip shortages, leading to a 5.1% plunge in its stock price, dragging the Nasdaq from a 2.1% increase to a drop of over 1%. High inflation means that funding costs remain elevated, directly pressuring crypto assets that rely on liquidity expectations.

Deutsche Bank pointed out that this downturn differs from previous cycles in that retail buying has nearly dried up, while institutional funds are massively shifting to AI. On June 25, as Bitcoin fell below $60,000 and Apple plunged, the storage chip sector surged across the board. Micron surged 8.6%, Sandisk rose 10.6%, and SK Hynix was up more than 10% at one point due to its U.S. listing plan. Funds have made directional choices between AI infrastructure and crypto assets.

Capital outflows, missing new buying, and macro pressure, these factors converged in the same week, forming a concentrated impact on the $60,000 support level.

$10 billion options expiring today, market may continue to fluctuate

In addition to the aforementioned pressures, June 26 will also see an immediate catalyst, as Deribit will face around $10 billion in nominal value Bitcoin options expiration, accounting for about 37% of the current open interest. The put-to-call ratio is 0.83, indicating that bullish bets still dominate, but most call options are currently out of the money, while put options are concentrated in the $60,000 to $65,000 and $70,000 to $75,000 ranges, suggesting that bearish bets are more likely to profit.

Deribit's Chief Business Officer Jean-David Pequignot stated that this is an options combination positioned for a mid-term high price, currently facing the test of declining spot prices.

Adam Haeems, head of asset management at Tesseract Group, pointed out that liquidity tends to be weak at quarter-end, and the trend could overshoot in either direction before returning to the mean after market makers hedge their positions, but the more significant test will come in the first week of July after quarter contract settlements and reduced leverage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。