As the Federal Reserve unexpectedly took a significantly hawkish turn and mainstream Wall Street firms successively withdrew their expectations for easing, Citigroup insists on a contrarian judgment, believing that a rate cut within the year remains a highly probable event, locking in the baseline scenario for the resumption of the easing cycle in October.

At the June FOMC meeting, 9 out of 18 Fed officials indicated a rate hike in the dot plot for this year, far exceeding market and analyst expectations. Chairman Waller formally removed the wording of "easing bias" in the post-meeting statement and refused to provide any forward guidance. In response to this shock, the swap market quickly moved the expectation of the first rate hike from March 2027 to October of this year, with the market currently pricing in about a 37 basis point increase for the remainder of the year, and the 2-year Treasury yield saw its largest one-day increase since March.

Facing this hawkish shock, Wall Street institutions have shifted their positions. Deutsche Bank officially withdrew its easing forecast in its latest research report, expecting the Fed to hike rates once in both September and December, totaling 50 basis points, raising the rate to 4.1%, and warning that action could be taken as early as July; Goldman Sachs Vice Chairman and former Dallas Fed President Rob Kaplan warned that if inflation data continues to be stubborn, the Fed may restart rate hikes as early as fall, very likely appearing in a series of 2 to 3 consecutive actions.

The Citigroup team led by Andrew Hollenhorst maintains a baseline forecast that is completely opposite to the market: the next action will be a rate cut rather than a rate hike, with the baseline scenario being a 25 basis point cut in October, followed by another 25 basis points cut in December and January 2027. Citigroup’s core argument is that the sharp decline in oil prices is eliminating the primary upside risk to inflation, the trend of initial jobless claims is replicating the seasonal weakening pattern of 2024 and 2025, while core PCE is increasingly showing as an “outlier” among various inflation indicators, with its strength reflecting more of a rise in stock prices rather than broad consumer price pressure.

One of Citigroup's Logics: Declining Oil Prices are Eliminating Inflationary Risks

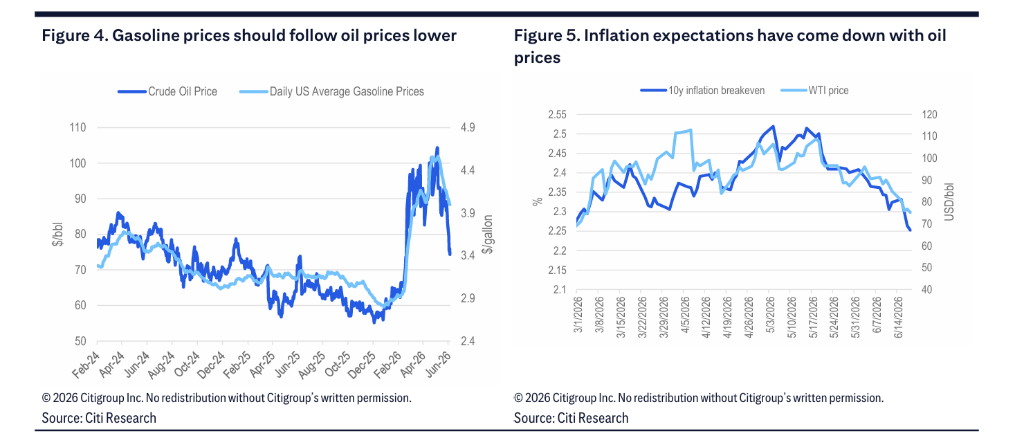

The first core argument for Citigroup's rate cut forecast comes from the rapid decline in oil prices. The bank believes that lower oil prices will drive gasoline prices down, thereby eliminating the previous main sources of inflationary pressure. Since market inflation expectation indicators have fallen in tandem with oil prices, the 10-year inflation breakeven rate has dropped to levels seen before the onset of conflict.

Citigroup points out that if Fed officials had more time to digest the latest changes in energy prices, the hawkish nature of this FOMC meeting would have been significantly reduced. The bank believes that as the effects of falling oil prices gradually manifest in data, inflation data will trend towards moderation in the coming months, helping to push more Fed officials to shift towards a more dovish stance before September, creating conditions for rate cuts before the end of the year.

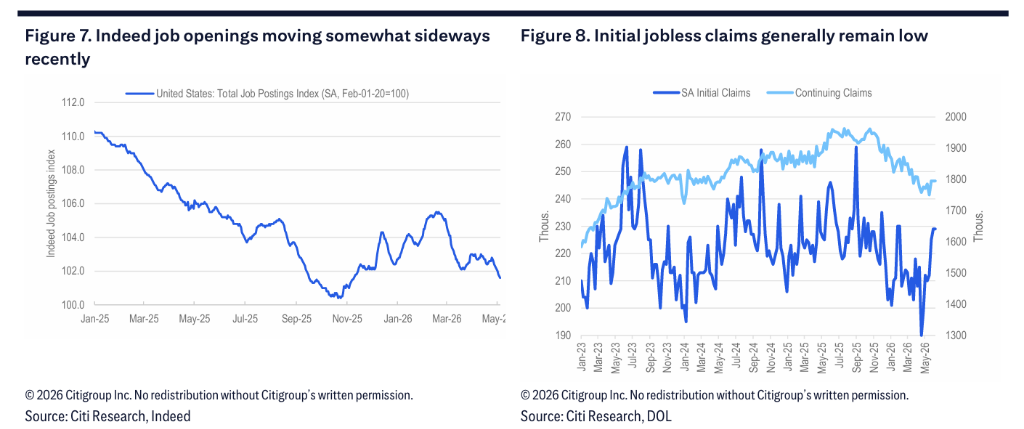

Citigroup's Logic Two: Signals of a Weakening Labor Market are Replicating Historical Seasonal Patterns

The second core argument from Citigroup focuses on the emerging early signals of weakness in the labor market.

Initial jobless claims and the number of people continuing to receive unemployment benefits have both shown an upward trend for several consecutive weeks. Citigroup notes that this pattern occurred in 2024 and 2025, which subsequently triggered a series of weak monthly employment reports and rising unemployment rates, with rising unemployment rates being a key driver of Citigroup's expectation for a rate cut by the Fed within the year. The bank anticipates that initial jobless claims (for the week ending June 20) will remain around 224,000, with continuing claims rising slightly to 1.813 million, and the 4-week moving average will continue to rise. While the current absolute levels are still not high, if the upward trend continues, it will align with the judgment of a gradually weakening labor market.

In terms of the overall economy, Citigroup's tracked GDP growth forecast for the second quarter is 2.5%. In terms of consumption, retail sales control group data for May grew by 0.7% month-on-month, still resilient, but actual disposable income growth has slowed to nearly zero growth, with the savings rate remaining low, indicating that the risks of a decline in spending growth are accumulating.

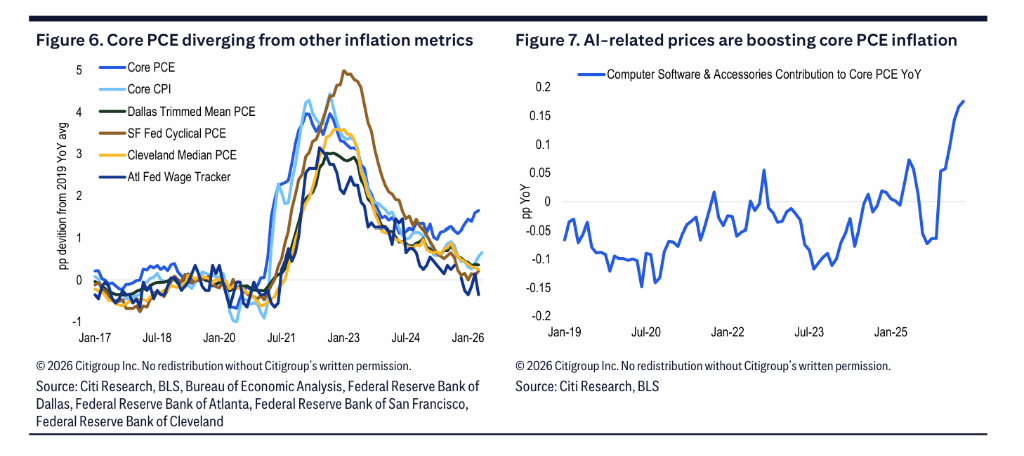

Citigroup's Logic Three: Core PCE is an "Outlier," the Inflation Picture is Not Unified

The third logical pillar that Citigroup firmly maintains against the trend relates to the core PCE data itself.

Core CPI for May recorded only 0.21% month-on-month, showing moderation; but Citigroup expects the upcoming May core PCE month-on-month rate to be as high as 0.37%, indicating a significant divergence between the two. Citigroup believes that the current strength of core PCE has specific reasons: this indicator is highly influenced by AI-related prices and is directly boosted by rising stock prices—May PPI data showed a month-on-month surge of 4.8% in portfolio management fees, mainly reflecting the rebound of stock prices from early April lows to early May highs rather than true price pressures on the consumption side.

From a horizontal comparison, the trimmed mean PCE from the Dallas Fed, the cyclical PCE from the San Francisco Fed, the median PCE from the Cleveland Fed, and the core CPI all show a more moderate inflation trend compared to core PCE. Citigroup believes that core PCE is increasingly becoming an "outlier" among various inflation indicators, rather than a reliable signal reflecting broad consumer price pressures.

Citigroup expects that as AI-related prices tend to stabilize in the second half of the year, the gap between core PCE and core CPI will gradually narrow, and the overall trend of inflation will become more supportive of policy easing. Under its expected path, the year-on-year growth rate of core PCE is expected to gradually decline from the current level of around 3.3% to a range of 2.1%-2.2% around mid-2027.

Wall Street "Surrender": Deutsche Bank Predicts Two Rate Hikes, Goldman Sachs Warns of a Series of Tightening

However, in the face of Waller's hawkish shock, Wall Street institutions have collectively changed their positions. Deutsche Bank's Chief U.S. Economist Matthew Luzzetti's team clearly noted in their report that the previous delay in raising forecasts was primarily due to two major uncertainties: the high economic outlook uncertainty caused by the Iranian situation, and the unclear monetary policy response function of newly appointed Fed Chair Waller. The results of the June FOMC meeting dispelled both these concerns.

Deutsche Bank significantly raised its inflation forecast, updating its core PCE expectations for the end of 2026 and 2027 to 3.2% and 2.5%, respectively, and revising the baseline forecast: the Fed will hike rates once in both September and December, totaling 50 basis points, raising rates to 4.1%; thereafter, remain unchanged for the entirety of 2027, only beginning to cut rates in the first half of 2028. Deutsche Bank also warned of hawkish risks: if Waller has publicly committed to "fixing" the price stability issue but the committee does not act in a timely manner, his credibility will be tested—this means that a rate hike could occur as early as July, and if the effects of last year's consecutive rate cuts are to be completely reversed, the total rate hike for the year may need to expand to 75 basis points.

Goldman Sachs Vice Chairman Rob Kaplan clearly stated that if inflation data does not cool from now until September, a fall rate hike will be a "wise move". He emphasized that the Fed's policy adjustments rarely occur in isolated actions, and rate changes typically occur in a series of 2 to 3 actions: "If action is taken in September, you need to be prepared for possibly one or two more rate hikes." Kaplan's warnings, based on historical experiences from multiple monetary policy cycles, have sounded the alarm for the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。