Ethereum is replicating the development path of the internet and Linux.

Written by: Etherealize

Translated by: Luffy, Foresight News

The Cycle of History: The Cathedral Ultimately Cannot Compete with the Open Market

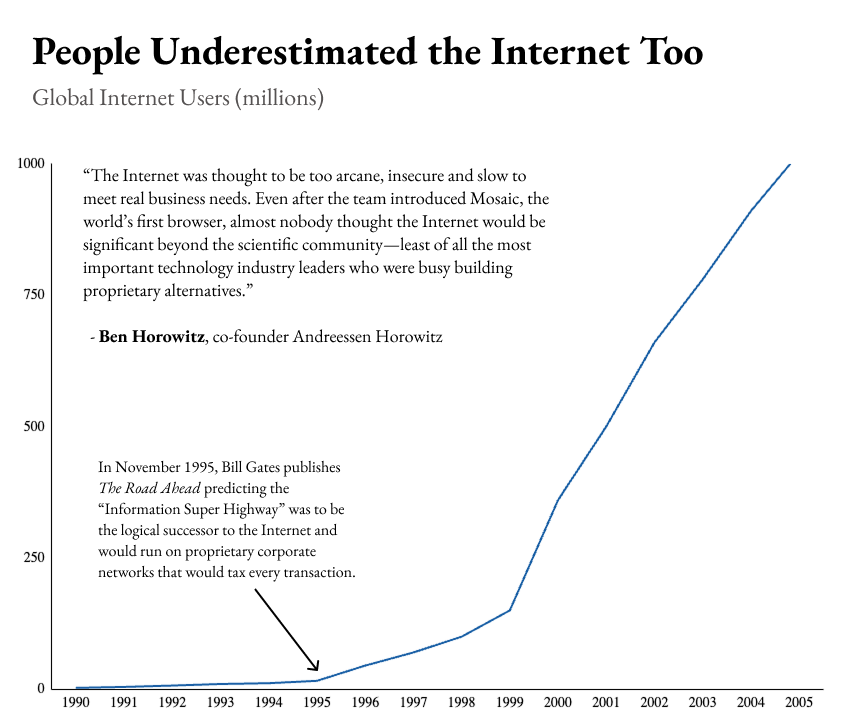

In 1995, the overwhelming majority of authorities in the tech industry were convinced that the internet would eventually lose to enterprise-exclusive private networks. History has proven them wrong; today, the skeptics of Ethereum who sing its demise are likely to misjudge again based on the same logic. The most representative figure at that time was Bill Gates, who proposed in his book "The Road Ahead" that the future of digital commerce would not rely on an open internet but rather on private proprietary networks controlled by companies like Microsoft and Oracle. This was the mainstream consensus of the industry at the time. a16z co-founder Ben Horowitz wrote: "Almost no one thought the internet could escape the realm of research, let alone a host of top tech giants who were all busy building their own private networks to compete with it."

The Linux system also followed a remarkably similar development path. In the late 1990s, Sun Microsystems monopolized the high-end Unix server market, but by the early 21st century, low-cost general-purpose hardware equipped with the open-source Linux operating system quickly eroded most of its market share.

Today, a similar historical script is playing out in the field of financial infrastructure. Major companies are sensing opportunities and potential threats, racing to build private blockchains. In the short term, private chains seem to have the upper hand: faster transaction speeds, better user experiences, and large business development teams continuously promoting implementation. However, over time, open, trustworthy, and neutral alternatives will gradually erode their market share. The reasons are twofold: 1) No company can permanently keep up with the pace of innovation in permissionless systems; 2) No legitimate institution wants to establish itself on infrastructure controlled by competitors.

In 1997, Linux core contributor Eric Raymond explained in his essay "The Cathedral and the Bazaar" the underlying logic of why open permissionless infrastructure triumphs in the long term. The previously recognized classic theory in the industry came from Fred Brooks' "The Mythical Man-Month": software must be developed by a single architect orchestrating a small, closely collaborating team, or else communication costs will explode exponentially. However, Raymond observed that thousands of unknown developers could synchronize to develop different modules of the Linux kernel, and the final product's scale even dwarfed commercial companies with market valuations in the billions. Traditional software is like a finely crafted "cathedral"; whereas the "bazaar" is Fred's definition of the Linux distributed development model: open, decentralized, filled with the chaotic energy of free iteration. When Linus Torvalds made the kernel source code public and accepted code patches from anyone, he inadvertently pioneered this development paradigm. In Raymond's words: "Release early, release often; delegate as much as possible; and remain open." The operating system built on this model supported the vast majority of internet services in the early 21st century.

Raymond's explanation is that the bazaar model avoids the problem of exploding communication costs: Developers do not need to collaborate directly; everyone synchronizes work around the codebase, interacting through patches and version updates; project maintainers integrate all submissions to form a unified standard, upon which other developers base their work. He wrote: "Brooks' Law's underlying logic has not failed, but when the number of developers is sufficiently large and communication costs are extremely low, the negative effects brought by this law are completely overshadowed by other non-linear growth effects."

Raymond also pointed out that the bazaar model breaks down identity barriers between users and developers. In the cathedral model, users are merely customers, reporting bugs only through customer service tickets; in the bazaar model, users are co-creators, who submit fix proposals or provide detailed technical descriptions for others to follow up. In the open-source community, "any problem will always have someone who can see the whole picture." A vast array of participants working collaboratively ultimately results in an overall efficiency that surpasses any centralized competitor: "The Linux ecosystem, in many ways, resembles a free market or a natural ecological system, where countless individuals act to maximize their own interests, yet spontaneously form a self-correcting, orderly functioning system that is far more sophisticated and efficient than any centralized planning can achieve."

The Ethereum ecosystem perfectly confirms this law. Fabian Vogelsteller, when developing a wallet, found various token interface standards to be chaotic, so he wrote the ERC-20 standard, which is now used by all stablecoins; the NFT universal standard ERC-721 originated from the CryptoKitties development team; the largest decentralized exchange, Uniswap, was initially just a blog idea by Vitalik Buterin, built by Hayden Adams, a mechanical engineer with no background in finance. These individuals promoted network upgrades without needing anyone's permission. As Sun Microsystems co-founder Bill Joy once said: "No matter what company you’re in, the vast majority of top talent is working for other companies." And the permissionless system allows innovation to emerge from any corner.

The core distinction between the bazaar and the cathedral lies in: the bazaar's integration layer is lightweight, fully public, operating based on credibility instead of authoritative top-down control. Core leaders like Linus Torvalds or Vitalik Buterin gain their authority by voluntarily following developers; developers are willing to follow because core decisions can be audited, publicly criticized, and if necessary, the community can fork the project to start anew. The internet relies on the Internet Engineering Task Force (IETF) and the Internet Assigned Numbers Authority (IANA) as a lightweight centralized coordination layer; Wikipedia has a complete editing and review process. All projects relying on permissionless innovation for continuous development have achieved genuine open contributions, while also pairing with structured integration mechanisms to mitigate concerns about chaotic disorder. Moreover, the coordination layer must maintain credibility rather than forced control, or the system will collapse quickly.

The bazaar model also requires the underlying infrastructure to be unable to be monopolized by a single entity. If Torvalds attempted to privatize the Linux kernel, global developers would immediately fork the project and continue iterating elsewhere. Raymond further refined this theory in "The Wild Space of Pioneering." The open-source system gives rise to rules similar to Locke's land property theory: the developer who writes the initial code first obtains the founding rights of the project; continuous contributions maintain ownership; and formal community transmission completes the transfer of rights. Open source licenses are the formal guarantee of this set of rules, while community consensus acts as a soft constraint. Once either is missing, developers will shift to other open-source projects that do not encroach on their labor results.

The Non-Replicable Core Barrier of Ethereum

In the Ethereum community, Vitalik summarizes these underlying requirements as "trusted neutrality." A coordinating mechanism that meets trusted neutrality must possess four major characteristics: rules are completely transparent, rules apply equally to all participants, rules are difficult to change arbitrarily, and anyone adhering to the rules can participate freely. These four characteristics are distilled from mature systems capable of attracting massive co-creators like the internet, Linux, and Wikipedia. However, private networks, closed ecosystems, and enterprise-exclusive blockchains cannot simultaneously meet these four criteria.

When viewed over a long time dimension, systems with trusted neutrality often ultimately prevail: open webpages replaced corporate private networks, Linux replaced private Unix systems, and Wikipedia replaced the Encyclopaedia Britannica. In every iteration, private alternatives possess substantial real advantages: focused product positioning, abundant capital reserves, dedicated customer service, and professional marketing and business development teams. However, as open ecosystems continue to mature, these advantages will gradually dissipate, and the network effects will completely reverse. Once an open system accumulates sufficient developer tools, practical applications, and credibility to establish stable and unchanging market perceptions, closed systems will be unable to compete.

Today, this development rule is permeating every layer of financial infrastructure. SWIFT, Visa, Mastercard, and the currently promoted consortium chains are all different in product form and development history, yet they share the identical underlying logic: controlled by centralized entities, concealing platform risks.

For forty years, SWIFT has always been jointly owned by member banks and is supposed to maintain neutrality, yet in 2012, the U.S. pressured it to cut off access for Iranian banks, and in 2022, it was again required to block several Russian financial institutions. Despite being registered in Belgium and governed by the banking sector collectively, SWIFT ultimately remains constrained by the U.S., and countries worldwide have seen this flaw clearly. Subsequently, China accelerated the promotion of the Cross-Border Interbank Payment System (CIPS), Russia built a domestic financial transmission system (SPFS), India expanded the Unified Payments Interface (UPI), and Brazil’s Pix became the core infrastructure for BRICS payment systems. Visa and Mastercard were initially alliances of banks, but have now become transaction toll booths, charging merchants fees ranging from 1.5% to 3.5%. Current consortium chains (Canton, Tempo, Arc, etc.) all possess the same fatal flaw: the interests of the platform operators may conflict with the upper layer developers at any time.

"The original concept of consortium chains—multiple banks and large enterprises jointly building dedicated blockchains—has essentially declared failure." Vitalik explained, "Such systems will simultaneously accumulate all the downsides of both centralization and decentralization." He noted that the initially participating banks appear to be equal co-builders, but the twentieth entity to enter is simply joining a system controlled by competitors. Enterprises must bear all the development costs of distributed systems while gaining none of the core values of blockchain's emergence: open composability and trusted neutrality. Past failed cases have confirmed this judgment. From 2017 to 2019, several banking alliances attempted to reconstruct the trade finance system based on blockchain: We.trade, endorsed by more than ten institutions including HSBC and Deutsche Bank, went bankrupt in 2022; Marco Polo, which absorbed over thirty banks, entered liquidation the following year; Contour soon followed, shutting down operations. The Australian Securities Exchange invested six years and about AUD 250 million to build a permissioned ledger using Digital Asset (now the developer of Canton Chain), ultimately abandoning the project in 2022. In contrast, Ethereum, which is not controlled by anyone, has never experienced a network-wide outage in over a decade, and its ecosystem continues to expand.

This is also the fundamental reason developers choose Ethereum. According to Electric Capital’s statistics, since its inception, Ethereum has had over 1 million developers participating in ecosystem building, with 232,000 active developers in the past year alone—no other public chain can come close. Some of the growth comes from the conventional positive cycle: Ethereum's supporting development tools, industry standards, and job opportunities are highly concentrated, making newcomers naturally choose to learn development here, thereby attracting more tools and job opportunities to land. However, the decision of developers and institutions to actively choose Ethereum places greater emphasis on its extreme decentralization and trusted neutrality attributes. For example, last year Robinhood chose to build a layer-2 network on Ethereum rather than developing a lower-level public chain in-house. Johann Kerbrat, head of the company’s crypto operations, stated, "Nowadays, many companies are building their own lower-level L1 public chains. We once aspired to fully control the entire system, but building a truly secure decentralized foundation is extremely difficult; while Ethereum inherently comes with this security foundation, it's essentially free. Many newly established L1s on the market can't even claim to be decentralized, and their security performance is questionable; fundamentally, they are just slower improved databases, and we see no core value in them."

Erik Voorhees, founder of the privacy AI inference platform Venice AI, expressed similar views a few days ago. The platform has over 3 million users and generates annual revenue of tens of millions of dollars. When asked why they chose to develop on Base, a layer-2 network built on Ethereum, he said, "We had no hesitation. Among all smart contract platforms, Ethereum's ecosystem is the purest, most resilient, and most complete."

The core characteristic of blockchain is sovereign independence. The revolutionary aspect of Bitcoin is that it is the world's first computational platform with sovereign attributes. Before Bitcoin's birth, all computer systems belonged to individuals, enterprises, or governments, and must comply with the will of the owners and territorial laws. Sovereign systems purely follow their set rules, and no single entity can forcibly change Bitcoin's rules. In the past, sovereignty belonged to monarchs and states, but now, computing platforms have achieved sovereign independence for the first time. This is also the source of the high regard for decentralization in the crypto industry: decentralization is the only path to sovereign independence. A chain with only ten validating nodes has its rules dictated by those ten entities; while Ethereum has hundreds of thousands of independent validating nodes scattered across major jurisdictions globally, paired with multiple independent client implementations, and the foundation has explicitly relinquished governance power, crossing the threshold of sovereignty—there is no party that can claim sole ownership of the network. The core value of sovereign independence lies in: the global financial system can rely on Ethereum to build upper-layer applications, and all participants need not worry about other entities, governments, or foundations arbitrarily changing the rules to harm their interests.

Global Institutions Are Betting on Ethereum's Open Ecosystem

Ethereum's leading advantages in sovereignty and trusted neutrality come from a historical path dependency that other public chains cannot replicate. Ethereum adopted proof-of-work at its launch in 2015 and continued for seven years before switching to proof-of-stake in 2022. Network ownership was fully decentralized through public crowdfunding in 2014, allowing anyone with consumer-grade graphics cards to participate in mining—no single entity holds a large enough token stake to control the network (this is the key prerequisite for achieving sovereign independence in a proof-of-stake system). Currently, most consortium chains rely on venture capital for initiation, with tokens concentrated and distributed to internal founding teams, giving a few entities absolute control over the consensus mechanism. Competitors can replicate the underlying technical architecture but cannot replicate the developmental history of Ethereum.

Thereafter, Ethereum's leading advantages continue to amplify: sovereignty and trusted neutrality attract developers; an influx of developers brings more complete development libraries, tools, and job markets, further lowering development thresholds and attracting more practitioners; various applications accumulate liquidity and tokenized assets, promoting institutional participation. Different layers of the ecosystem empower each other, while competitors entering the market must simultaneously build a complete industrial chain, as Ethereum's scale advantage continues to compound.

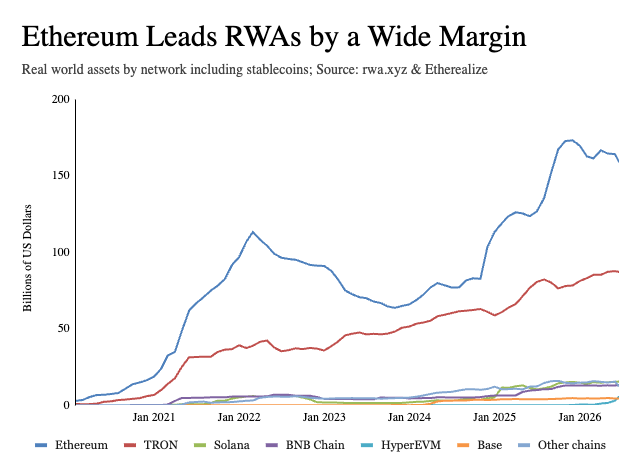

The industry's most mature participants have already placed their bets on Ethereum: Coinbase and Robinhood have built layer-2 networks based on Ethereum; BlackRock and JPMorgan have launched tokenized currency funds BUIDL and MONY, both deployed on Ethereum; core DeFi protocols like Aave, Maker/Sky, Maple, and Uniswap are all primarily based on Ethereum; and the leading stablecoin issuers worldwide also rely on Ethereum for settlements. According to Token Terminal's "Ethereum Industry Report Q1 2026", among the five major public chains, Ethereum supports 79% of active DeFi lending business, 62% of stablecoin issuance scale, 73% of tokenized funds, and 84% of tokenized commodity assets.

Upper-layer applications on Ethereum are also permissionless, further amplifying their advantages. For example, Uniswap's permissionless listing mechanism allows thousands of long-tail assets to gain pricing and liquidity, services that centralized exchanges will never offer; Aave's lending market is open and highly composable, generating a full suite of specialized liquidity pools, risk management ecosystems, and business boundaries that far exceed the limits of what the project core team can develop alone. Closed systems require platform operators to anticipate all application scenarios in advance, while open systems do not.

Regarding the viewpoint that "permissionless systems will ultimately prevail," the most compelling counter-argument is not on the technical side but rather on the special attributes of the financial industry: enterprise-controlled private networks may be an advantage rather than a flaw for the finance sector. Once a payment fails or asset flows abnormally, regulatory agencies need to pinpoint the responsible parties; the idea of "no one controlling" sounds more like a significant risk when legal matters are involved rather than an advantage. However, this line of questioning confuses two completely independent systems: the accountability mechanism is built on the application layer, while the settlement layer need not assume that function. For example, the ERC-3643 token standard directly incorporates KYC identity verification and cross-regional transfer restrictions into smart contracts; issuers can set wallet whitelists, limit asset transfers, freeze, or recover tokens; privacy technology likewise, zero-knowledge proofs enable institutions to complete settlements on public chains while concealing transaction details. In contrast, data on consortium chains can only be accessed by the enterprises themselves and their competitors.

In the early days of internet development, the public was generally skeptical of its security sufficiency to support commercial transactions. After the HTTPS protocol improved security capabilities, the vast majority of commercial activities fully migrated to open networks, and related doubts disappeared entirely. The judgments of the skeptics regarding early internet flaws were not wrong, but they underestimated the potential of open networks to self-evolve.

Today, those banks and fintech companies building private chains are repeating the mistakes of AOL and Microsoft from years ago: attempting to replicate an open system while building a walled, closed ecosystem, relying on the platform to collect rent. This model is destined to fail, as constructing the walls of control simultaneously isolates external innovations.

Netscape is the true success story. Netscape never attempted to monopolize the internet; rather, it created a browser that guided global users to access the open network. Relying on the explosive growth of the internet, Netscape once became a core enterprise of its era. Ethereum possesses an almost unreplicable attribute of trusted neutrality and already has the potential to become the global financial settlement layer. The optimal development strategy for the industry is to build applications on permissionless infrastructure rather than to compete directly with it.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。