Author: Jae, PANews

A report from a traditional bank has ignited the somewhat quiet DeFi track.

Geoff Kendrick, head of global digital asset research at Standard Chartered Bank, released his first coverage report on the DEX (decentralized exchange) Uniswap on June 15, providing a radical prediction that caught the attention of the crypto market: the governance token UNI will soar approximately 40 times to reach the 100-dollar mark by the end of 2030.

At that time, UNI's trading price was only about 2.6 dollars.

Once ridiculed as an "air governance token," UNI is being repriced by Wall Street as a productive asset with network effects. While the 40-fold long-term narrative is enticing enough, the journey to the destination may not be smooth sailing.

The Wall Street Script for UNI's 40-Fold Growth: Four Numbers, One Main Line

In the deconstructive logic of Standard Chartered Bank, Uniswap is being embedded into a valuation framework that deeply integrates traditional finance with the on-chain world.

RWA Tokenization Exponential Growth (340 Billion → 4 Trillion)

The starting point for this growth is the wave of RWA (real-world assets) being brought on-chain. Standard Chartered predicts that the global market for tokenized assets will experience exponential growth, surging from around 340 billion dollars now to 4 trillion dollars by the end of 2028. Asset management giants like Fidelity and BlackRock are transferring traditional assets including stocks, government bonds, and money market funds onto the blockchain en masse, and the liquidity of on-chain tokenized assets will expand at a speed far exceeding industry expectations.

This is equivalent to building a larger reservoir for the DeFi track: first accumulating the asset scale, and only then will subsequent financial activities such as trading, lending, and staking have sufficient targets to support them.

DeFi Penetration Rate (3.5% → 30%) Boosting TVL (37 Times)

Tokenization of assets is only the first step; stagnant waters need to turn into flowing water. Simply put, only when assets flow into DeFi protocols can they be transformed into the income and value of those protocols. Standard Chartered estimates that currently, only about 3.5% of tokenized assets are invested in the DeFi ecosystem, and this ratio is expected to rise to 30% by 2030.

Driven by both native crypto asset growth and the rise of RWA coming on-chain, by 2030 the overall DeFi TVL (Total Value Locked) will explode 37 times from the current level, reaching approximately 2.7 trillion dollars.

Fee Switch Providing Price Support (40 Times)

As the home of on-chain liquidity, Uniswap will become the biggest beneficiary of this influx of funds, with its token UNI expected to rise from 2.6 dollars to 100 dollars, yielding nearly a 40-fold increase.

Standard Chartered's long-term price path for UNI is: 6.5 dollars by the end of 2026 → 20 dollars by the end of 2027 → 40 dollars by the end of 2028 → 65 dollars by the end of 2029 → 100 dollars by the end of 2030.

In the past, UNI was jokingly referred to as an "air coin" due to its lack of cash flow capture ability despite having governance rights. At the end of last year, Uniswap activated its fee switch, officially entering a deflationary era.

The report pointed out that Uniswap destroyed 100 million UNI tokens in one go on December 28 of last year, along with an additional 5 million UNI, reducing the total supply from 1 billion to 895 million, and the circulating supply consequently dropped to 622 million. This reduction in supply will support the price of UNI.

Additionally, Uniswap generated approximately 21 million dollars in protocol fees. The linear relationship between fees and trading volume means that as tokenized assets flow into the protocol, the fee switch will automatically trigger more burning. This indicates that UNI is transitioning from a "pure governance tool" to a "productive asset with deflationary attributes," directly narrowing the valuation multiple gap between Uniswap and publicly listed exchanges like Coinbase.

Notably, Geoffrey Kendrick also made a vivid business analogy in the report: comparing Uniswap to YouTube and Coinbase to Netflix.

Coinbase (Netflix Model): Centralized operation, heavy asset investment, requires high capital support, listing and compliance must go through multiple screenings, high marginal cost of expansion, and the types of assets covered are easily limited;

Uniswap (YouTube Model): Open liquidity pool structure, where any user can be a "content creator" (liquidity provider). The platform does not need to pay high costs for asset listings. In scenarios such as stablecoin trading, liquid staking derivatives, and niche tokens, this type of open model creates network effects and long-tail advantages that centralized exchanges (CEX) cannot match.

This bilateral effect of increasing prosperity is precisely the moat that allows Uniswap to maintain its leading position long-term.

More importantly, Standard Chartered believes that Uniswap is by no means a simple "retail DEX application," but rather an integratable market infrastructure. Once the RWA scale expands, traditional financial institutions will be able to directly "insert" assets into Uniswap's liquidity pools for trading. This functionality is something the traditional financial market itself cannot achieve.

Uniswap Becomes Traditional Funds' First Choice Interface, Yet Faces Attacks from Emerging DEXs and Aggregators

While Wall Street's forward-looking filter is appealing, the actual situation of Uniswap in the crypto market is not as smoothly linear as presented in the report.

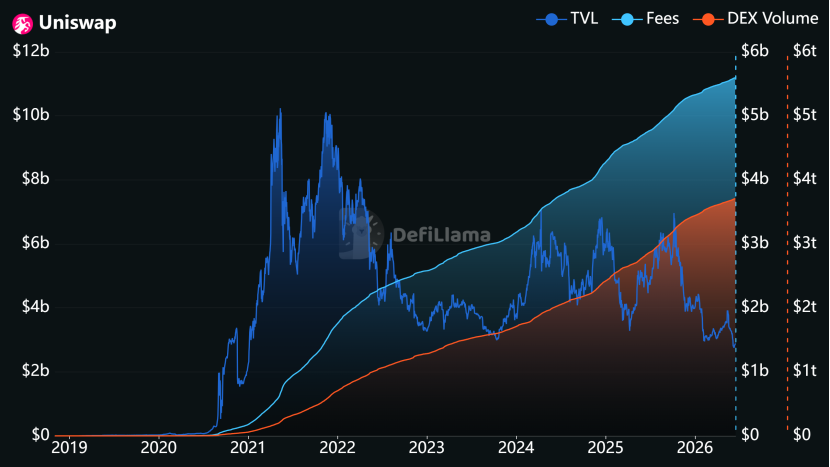

Since its establishment in 2018, Uniswap has accumulated a trading volume of over 3.7 trillion dollars, with total fees reaching 5.6 billion dollars and a TVL of about 2.88 billion dollars.

From a market share perspective, Uniswap's DEX throne remains secure. Whether on the Ethereum mainnet or across various L2 ecosystems, Uniswap dominates in trading volume and liquidity depth, with no competition able to form a substantial threat.

More important signals come from the institutional side. In February of this year, BlackRock's tokenized money market fund BUIDL announced the launch of trading on UniswapX and strategically purchased UNI tokens. With the popularity of UniswapX, features like off-chain routing, gas-less trading, and MEV (miner extractable value) resistance significantly bridge the experience gap between DEX and CEX, making it the preferred entry point for traditional funds on-chain.

Coincidentally, last Friday (June 12), Fidelity deployed the liquidity of its stablecoin FIDD onto Uniswap. The protocol's concentrated liquidity model is currently the most efficient pricing mechanism on-chain. Once compliant RWA assets come on-chain in large quantities, Uniswap is expected to become the on-chain "New York Stock Exchange," mastering the voice of asset pricing.

Wall Street's waters are flowing toward the chains. And Uniswap is the faucet. Wall Street institutions are using Uniswap as the on-chain interface for compliant assets, and UNI is aligning more with the pricing logic of "on-chain routing infrastructure."

Although the vision of reaching 100 dollars is quite alluring, two significant mountains still lie in the path of Uniswap toward its peak, which could delay or even nullify this long-term check.

Traffic Hijacking by Emerging DEXs and Aggregators (Competitive Risk): DEXs from the Solana faction like Jupiter and Raydium are quickly encroaching on large amounts of retail traffic thanks to meme frenzy and extremely low trading costs. At the same time, aggregators like 1inch and CowSwap are intercepting users on the front end, causing Uniswap to become a "backend liquidity pool" in some ecosystems, continually weakening its brand premium and user perception.

Delay in Tokenization Implementation (Macro Risk): Standard Chartered's high valuation heavily relies on the assumption that "DeFi TVL will reach 2.7 trillion dollars by 2030." If the global legislative progress on tokenization falls short of expectations or a large-scale security incident or systemic risk occurs, the penetration speed of RWA will slow significantly, and the realization cycle of this grand narrative may be severely delayed.

Returning to the most intuitive pricing aspect, the current trading price of UNI is less than 3 dollars, down more than 92% from its historical peak in May 2021.

The fee switch has brought deflation but has not reversed the price trend. The market's indifference to the DeFi narrative, the exhaustion of liquidity, and the high macro interest rates have all put extreme pressure on UNI's valuation.

However, this may be the source of Standard Chartered's "40-fold space": starting from a low base.

Standard Chartered's first coverage of UNI with a target price of 100 dollars is more about the directional significance than the price itself. In reality, whether the prediction is accurate or not is not important; what matters is that Wall Street's perception of DeFi is changing: from the early years of "barbaric growth and speculative bubbles" to a rational business judgment of "capital efficiency, network effects, and cash flow value."

It should be noted that Wall Street reports often emphasize macro logic while being shorter on micro risks. For investors within this space, while the allure of a 40-fold endpoint is clear, the road to 2030 is sure to be filled with thorns.

Whether UNI can truly capture the 4 trillion dollar tokenization dividend depends on how well it can navigate the intricate dance between decentralized principles and global regulatory compliance in the real world.

Compared to a 40-fold increase, the four-year wait is where true faith will be tested.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。