Hyperliquid has had 99% of its transactions in non-crypto contracts over the past seven months, and major exchanges are accelerating their deployment of global asset trading.

Written by: Prathik Desai

Translated by: Saoirse, Foresight News

The market is always evolving, which is its inherent property. Ultimately, the scale of market development will always exceed the categories it originally served. The butter-and-egg exchange that originated in Chicago in 1898 has now developed into the world's largest derivatives market, the Chicago Mercantile Exchange (CME). Amazon originally built a warehousing and payment system solely to sell paperback books, and today this system is no longer limited to a single category. The book business may have long become insignificant in Amazon's overall revenue.

This pattern of development is still applicable today: first establishing infrastructure for a single business, then discovering that the system can adapt to more fields, and thus continuously expanding the boundaries of business to accommodate all trading categories supported by the infrastructure.

Today, cryptocurrency exchanges are in this transformative stage.

The underlying architecture originally built for token trading can also be used for trading crude oil, silver, stock indices, stocks of companies planning to go public, and event contracts. The trading market for perpetual contracts without access thresholds, which did not exist two years ago, has seen 99% of its trading volume over the past seven months come from non-cryptocurrency contracts.

This trend is evident throughout the industry. Major exchanges are racing to transform into multi-asset brokerage platforms, while blockchain networks have become the cost-effective path to achieve this goal.

Cost-Optimized Path

Whether it is perpetual futures contracts or prediction market contracts, there is essentially no difference between the underlying assets being bitcoin or crude oil. All you need is a wallet with stablecoins to trade meme coin futures or bet on the results of Apple's quarterly report. Blockchain trading networks do not differentiate between asset attributes, just like the internet and logistics networks, which never limit the categories of transactions on the Amazon platform.

Given this, why would traders abandon traditional trading platforms to trade silver and stocks on exchanges that have been established for only a few years? The reasons are similar to why people choose online shopping: convenience and cost advantages.

Amazon eliminated intermediary steps, allowing sellers in different locations to ship directly to buyers. Sellers can compete by lowering prices, and buyers can freely choose from various products and add them to their shopping carts, completing payment without leaving home (or from anywhere).

The low-cost advantages that blockchain initially provided for crypto trading now also apply to stock settlement, commodity clearing, and cross-border stock trading.

Blockchain markets operate year-round, with 24/7 uninterrupted trading, enabling global traders to adjust asset pricing at any time based on various events. In recent months, we have witnessed its influence on the non-crypto asset market multiple times.

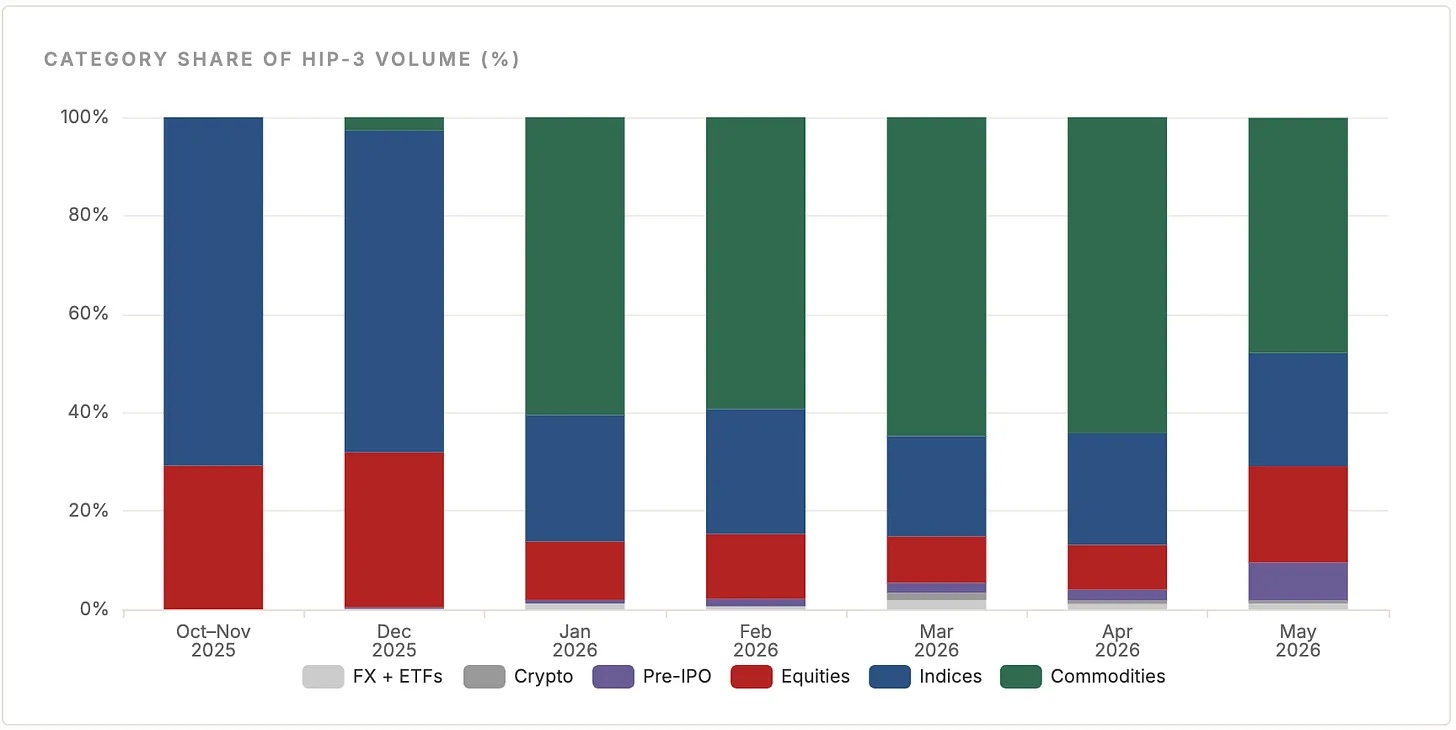

Since October 2025, the access-free trading market (HIP-3) under Hyperliquid has seen total trading volume reach approximately $270 billion across seven trading sites. Among this, 99% of trading volume comes from commodities, stocks, foreign exchange, stock indices, and contracts for companies planning to go public, with pure cryptocurrency trading volume consistently below 1%, and the range of trading categories on the platform continues to expand month by month.

Source: Hydromancer

During the last weekend of February this year, as the conflict between the U.S. and Iran escalated and the global major commodity exchange CME had already suspended trading, Hyperliquid's West Texas Intermediate (WTI) perpetual contracts were still trading as usual. In just three weekends, the trading volume on this platform surged from $25 million to over $550 million. A recent report from TD Securities indicated that before CME reopened on Monday, Hyperliquid had already absorbed about 80% of the fluctuations in crude oil prices that followed.

Earlier this year, during the rise of precious metal prices, the daily trading volume of silver perpetual contracts even approached $1 billion. Even when traditional markets were closed, the blockchain-based trading platform continued to operate normally.

This phenomenon exists not only in the perpetual contracts field but also in the stock trading market.

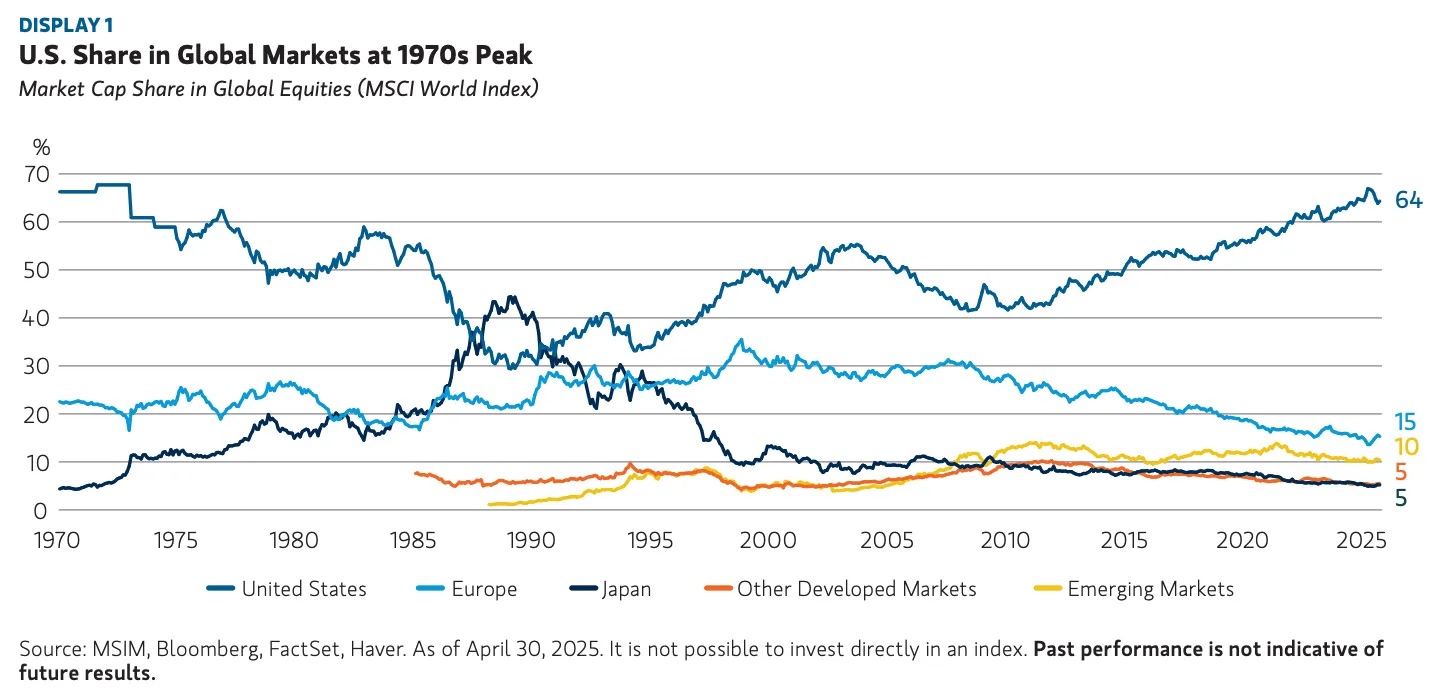

The total market capitalization of U.S. stocks accounts for over 60% of the global stock market's total capitalization. However, for the majority of global investors, investing in U.S. stocks requires the assistance of intermediaries, handling foreign exchange conversions, meeting minimum capital thresholds, and dealing with numerous account type restrictions.

Global market capitalization share changes

Everyone wants to participate in the development dividends of the world's largest economy and share in its growth outcomes. This also explains why nearly all cryptocurrency exchanges hope to provide users with trading channels for U.S. stocks and U.S. stock derivatives.

On June 1, Binance announced the launch of zero-commission trading for 7,000 U.S. stock securities for its 300 million registered users, supporting fractional shares trading starting at $5. The vast majority of users on the platform are based outside the United States, and now they can participate in U.S. stock investments simply by using a wallet containing stablecoins.

Kraken’s xStocks platform has also proven that asset tokenization can significantly lower the barriers to stock investment. The platform has completed the tokenization of over 100 listed company stocks, with a total trading volume of $25 billion, and on-chain holding users reaching 80,000.

Meanwhile, blockchain has also opened up channels for pricing pre-IPO companies in the traditional market. SpaceX plans to raise around $75 billion and is expected to set a record for the largest IPO ever; on June 1, Anthropic secretly submitted its IPO application, and OpenAI is likely to follow soon after. Before these companies officially go public, their market pricing is non-transparent and only open to professionally qualified investors.

I mentioned in my article "Private Asset Pricing" that the market has always been eager for fair pricing of quasi-listed company assets.

Companies like OpenAI and Anthropic have extremely high brand recognition, scaled revenue, and hundreds of millions of users; aside from not having publicly circulating shares, they possess all the characteristics of a publicly listed company. Brand promotion has led the public to have varied opinions about these companies, yet ironically, almost everyone finds it difficult to participate in their valuation transactions, creating a gap that is unprecedentedly huge.

Blockchain provides multiple tools that enable the market to price these types of unlisted companies.

Now, several platforms evolved from cryptocurrency exchanges are beginning to launch perpetual contracts, prediction market contracts, and tokenized IPO participation channels for unlisted companies.

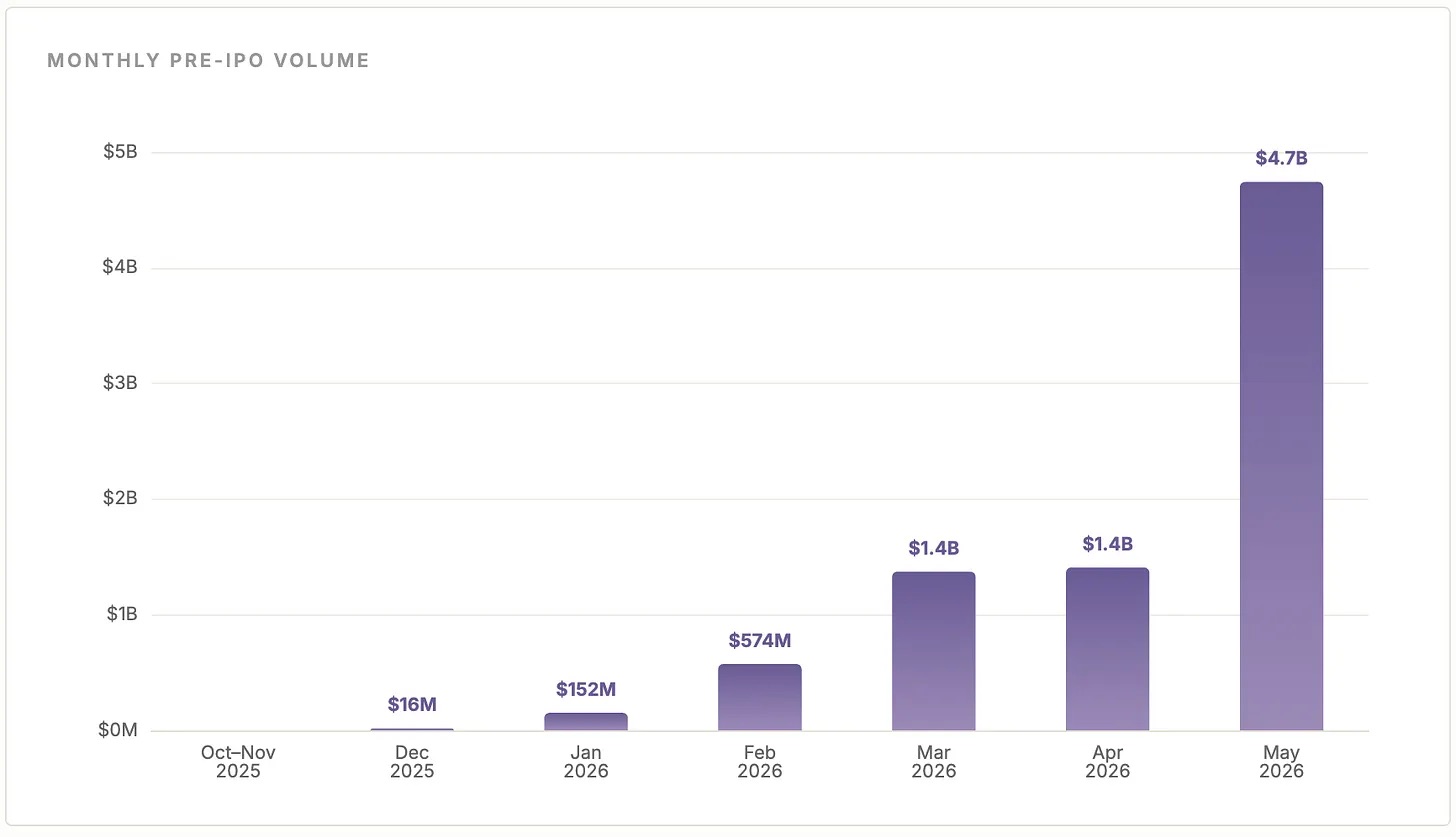

Several market makers have launched perpetual contracts for companies like SpaceX, Cerebras, and Anthropic on Hyperliquid. In the past six months, trading volume for these types of contracts has surged by approximately 300 times, from $16 million to $4.7 billion. The trading volume of perpetual contracts for pre-IPO stocks has increased from 0.2% of the total trading volume on the HIP-3 platform in December 2025 to 7.7% in May this year.

Source: Hydromancer

These trading platforms not only operate year-round and have lower trading costs but also provide traders with reliable deep liquidity.

During the escalation of the situation in Iran, Hyperliquid's West Texas Intermediate crude oil contracts reached a daily trading volume of hundreds of millions of dollars, with buy-sell spreads consistently maintained at low levels. From January to April 2026, the open contract volume of this crude oil perpetual contract grew from $1.8 million to $560 million.

Traditional exchanges can also rely on user deposits to provide cross-margin mechanisms and ample liquidity. Binance, through connecting with the PreStocks platform, opened trading channels for pre-IPO stocks, while Payward (the parent company of Kraken) supports user investments in tokenized IPO projects.

Less than 24 hours ago, Coinbase followed Kraken and Binance by launching perpetual contracts for pre-IPO stocks, with the first instrument being SpaceX.

The Path of Full-Stack Financial Technology

The bidirectional integration of traditional finance and crypto lanes is giving rise to a number of platform companies with full-stack financial technology capabilities. Native crypto platforms are continuously launching traditional asset categories, and traditional exchanges are also rapidly building blockchain underlying facilities.

In the crypto industry, over the past 12 months, Kraken has spent more than $2.7 billion completing multiple acquisitions, aiming to transform into a comprehensive multi-asset brokerage. In March 2025, it acquired NinjaTrader for $1.5 billion, setting a record for the largest acquisition of a CFTC-licensed futures brokerage.

Subsequently, Kraken also acquired Backed Finance, bringing the issuance, trading, and settlement processes of the xStocks stock tokenization business in-house. By early 2026, the number of tokenized stocks available for trading on the platform expanded from 60 to 100. Following this, the company completed five acquisitions in the fields of payment, clearing, and automated trading infrastructure.

Then, Kraken launched a payment application called Krak, which covers 160 countries and supports over 300 types of assets, allowing users to use cryptocurrency for consumption, transfers, and also gain returns from asset management.

Coinbase has also built a complete system for similar businesses. At its product launch in December 2025, Coinbase launched zero-commission stock trading across all 50 states in the U.S. and integrated prediction market services through Kalshi. In August 2025, it spent $2.9 billion to acquire Deribit, taking over the world's largest crypto options trading market. Now, Coinbase is building its stablecoin USDC and its own Layer 2 chain, Base, into a universal settlement layer that covers various financial scenarios like smart automated payments and stock trading.

These platforms all entered the financial industry with cryptocurrency as their entry point, but now they hold user distribution networks that traditional institutions took decades to build. Binance has 300 million registered users, and Kraken services cover 190 countries and 15 million customers. In the process of expanding multi-asset brokerage services, their large user base is their strongest competitive moat.

When Binance launched trading for 7,000 U.S. stock securities, it did not need to cultivate market demand from scratch. Trading permissions for stocks and pre-IPO equity were directly opened to existing users who had repeatedly topped up with stablecoins and completed identity verification. For crypto brokerage platforms, the marginal cost of adding stock business is merely a fraction of what traditional brokers incur to acquire a new customer.

Traditional established financial institutions are also actively seeking change to avoid being eliminated by the times. On the same day that Binance announced U.S. stock trading services, the world's largest derivatives exchange CME Group announced that all its crypto futures and options products would start 24/7 trading.

The DTCC, with a custody asset scale of $114 trillion, will launch a pilot project for tokenized securities in July this year, with a full rollout in October. The pilot subjects include Russell 1000 index constituent stocks, mainstream index ETFs, and U.S. Treasuries, with more than 50 institutions including BlackRock, JPMorgan, and Circle participating in the project.

The New York Stock Exchange is collaborating with Securitize to build an around-the-clock tokenized stock trading market; Nasdaq also received approval from the SEC in March to conduct tokenized stock trading within its existing trading system.

This bidirectional integration is particularly intriguing: Traditional institutions like CME implement 24/7 trading because the crypto market has proven that financial transactions do not require market closure periods; crypto exchanges launching traditional assets like crude oil, silver, and stock indices is because market demand will naturally flow towards the trading channels that are more liquid and have lower pricing costs.

Blockchain serves as the universal underlying bridge connecting traditional finance and the crypto world.

The Evolution of the Fusion of Crypto and Financial Technology

Like all emerging technologies, public discourse surrounding the application prospects of cryptocurrencies has long been mired in a binary and one-sided discussion: Either people believe that crypto will build an entirely independent new financial system, or they determine that it will ultimately collapse. However, the true development path of the crypto industry lies between these two extreme speculations, similar to the development history of the internet.

Once upon a time, the public either completely denied the internet or praised it as a new world that would overturn everything. But as time passed, the internet gradually became infrastructural, becoming ubiquitous yet invisible, with almost every global industry operating based on it. No one now argues about the usefulness of the internet; it has become a universal underlying vehicle supporting various new technologies to be implemented.

Now, cryptocurrencies are reproducing the same development trajectory. The various technologies that cryptocurrencies have derived may not have fulfilled the visions of the early cypherpunk groups, but I suspect the vast majority of pioneers are not really bothered by this; at least I personally do not care.

While the crypto-native market is repeatedly discussing the price cycles of Bitcoin (BTC) and the narrative of bear markets, a parallel external track is gradually permeating through various links of the financial system: payment underlying facilities, smart automated business, integrated price discovery platforms, and the currently hot multi-asset brokerage business. The development of these sectors is completely unaffected by whether Bitcoin is priced at $60,000 or $100,000.

Charlie Booth from Hepworth Iron Capital clearly articulated the logical differentiation and evolution between the endogenous tracks of the market and the exogenous tracks in a guest commentary published in "Token Dispatch" last week.

What I pay the most attention to is this: the technology originally built for token trading can now allow ordinary retail investors to participate in Apple stock trading on a Saturday with just $5, relying on stablecoins for settlement, with a transaction fee of less than a cent. The underlying architecture supporting this entire service was initially designed just for meme coins.

Such innovative scenarios will only be established when the new infrastructure possesses crushing advantages over the old system. We all know how entrenched industry habits are difficult to change, but the global market is discovering that blockchain is the optimal solution for significantly optimizing financial operational efficiency: In some scenarios, it reduces costs and increases efficiency for outdated financial systems, while in others, it completely replaces decayed, outdated traditional systems. Clinging to old models simply to resist change is utterly meaningless.

Any industry operated by humans that deliberately resists changes that can optimize the existing system is effectively cutting off its own future. Humanity has an inherent desire to transform inefficient systems, and any tool capable of enhancing efficiency, no matter how novel or radical it appears, will ultimately be accepted by the market. Blockchain happens to cut into many inefficient pain points in the financial industry, possessing ample room for optimization. That traditional leading institutions like Nasdaq, the New York Stock Exchange, and CME are all laying out blockchain is sufficient proof that blockchain will occupy a core position in the future financial system.

Today, all exchanges are transforming into comprehensive brokerage platforms or are about to complete that transformation. Not every platform initially planned this route, but it is a common development goal for them. So where will the industry move next? When all platforms can trade stocks, derivatives, prediction market contracts, and cryptocurrencies within the same app, who will ultimately prevail? The core competition lies in the platforms' ability to integrate across assets and whether they can meet the four fundamental financial needs of users: consumption payments, transfers, receivables, and asset appreciation and profit.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。